The market continues to ignore the fact that the US will have to pay its debt at very high interest rates. It's logical that central banks are looking to gold as a hedge.

USD 4100 (+/- 60 USD ) hit on March 23 2026 should hopefully form the double bottom for #Gold . After this bottom over next few days , it should be onward & upward IMO toward USD 5000+ in coming months.

#GOLD

😎👍

Hard to ignore results like this. 👀

Continuity from surface to 900m+ points to a large, well-preserved #porphyry system.

Add high-grade #breccias and multiple open directions?

That’s how district-scale potential begins to emerge. 🧵👇

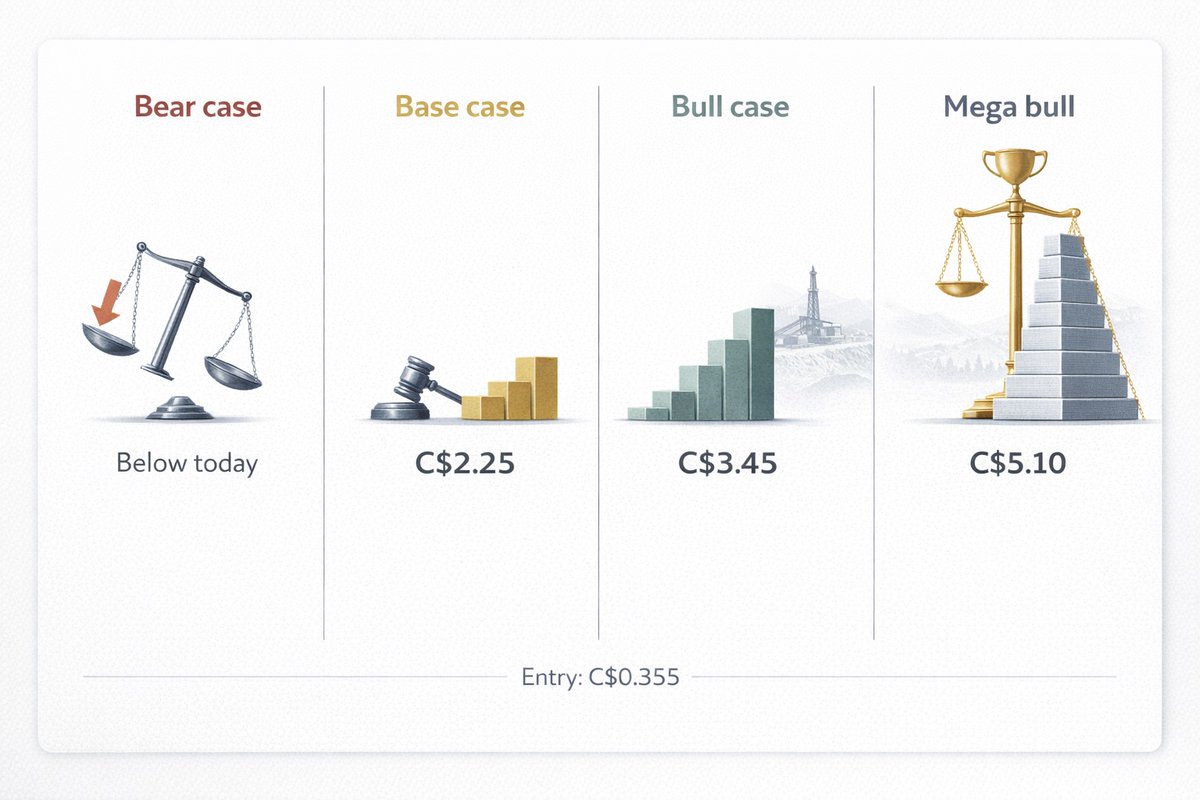

If you are following the public GoldSilverAI portfolio you may have seen that I bought a new position in Silver Bull Resources $SVB.TO at C$0.355 in the beginning of the week.

This is not a normal mining setup for me. It’s an arbitrage-style situation.

I used to own Silver Bull because Sierra Mojada always looked like one of the more interesting undeveloped silver-zinc assets in the sector. But the reason I’m buying it now is the legal setup.

Silver Bull has been locked out of its project since the 2019 blockade, and the dispute with Mexico is now in its final stage. The company is waiting on a final arbitration award by the end of May 2026.

Nothing is certain in cases like this. It’s binary, and legal outcomes always carry real risk. But after following the case, I think Silver Bull has a good chance of winning. The breach itself looks quite clear to me, and Mexico does not seem to have presented much of a defense on that point.

Let’s look at the possible outcomes:

🔴 Bear case:

Silver Bull loses, or wins so little that after legal economics there is not much left for shareholders.

Value per share: far below today’s price

🟡 Base case:

The tribunal takes the conservative route and mainly compensates Silver Bull for sunk costs, adjusted for inflation and pre-award interest. On the numbers I’ve seen, that gets to around US$175M. After the funder’s share and management’s cut, that works out to roughly US$99M for equity holders.

Value per share: ~C$2.25 (6.3x my entry)

🟢 Bull case:

The tribunal does not stop at sunk costs, but also recognises part of the project’s lost upside. In that scenario, you can justify something closer to a 1.5x uplift on the adjusted sunk-cost framework.

Value per share: ~C$3.45 (9.7x my entry)

🚀 Mega bull case:

The tribunal accepts a broader fair-market-value approach and gives more weight to what Sierra Mojada could have been worth as an asset, not just what was spent on it.

Value per share: ~C$5.10/share (14.4x my entry)

The fact that Silver Bull still trades around C$25M valuation this close to the decision could mean the market sees high bear-case risk. But it could just as easily mean the case is still poorly understood and underfollowed.

That disconnect is why I took the position.

Still, this is a very high-risk bet. Anyone buying $SVB needs to be comfortable with the possibility that it could go to zero if the decision goes the wrong way.

On the other hand, I could also see the stock rerating sharply before the ruling as more investors wake up to the setup. If it does, I will likely trim part of my position to reduce risk.

The Coming Commodity Supercycle

The shift is happening... and its accelerating. We are currently transitioning from a equity cycle to a commodity cycle

2020-2024 accumulation

2025-2026 the breakout

2027-2035 established supercycle

Here's why... The world is $346 trillion dollars in debt and counting while on average the secular erosion of all global currencies is +/-5% YoY. Add in geopolitical tension, demand driven by ai, underinvestment and electrification. These are the implicit catalysts driving the supercycle. The S&P 500 trades at 22x earnings but on average, high quality gold miners are trading at just 6-8x multiples (cheap). Fiat dies in deflation, the equity multiples collapse in recession and hard assets win in both. When $125 trillion in global equities realizes this, they will scramble into physical commodities with 30% deficits. The returns on investment will be life changing if your positioned properly.

P.s. While everyone is watching silver we want to warn that we believe a supply-side collision will break the momentum temporarily in 2026. Buy the reversion to the mean with our conviction.

This is a very well written article by Mr. C of Hong Kong, China.

Following the outbreak of the US-Iran war, gold prices unexpectedly fell instead of rising. This caught many investors off guard — particularly those who believed that gold should be bought during times of geopolitical turmoil — resulting in heavy losses.

The market has offered various explanations for this counterintuitive phenomenon. Some attribute the decline in gold prices to a severe liquidity crunch. The fear triggered by the war prompted investors to sell assets aggressively to raise cash. As a result, apart from oil prices surging sharply, almost all other asset classes experienced heavy selling pressure, causing prices to fall rapidly. Leveraged investors, in particular, may have faced margin calls. With gold being one of the few positions still showing a profit, many were forced to sell their gold holdings to meet these calls and cover urgent liquidity needs.

Another explanation is that the sharp rise in oil prices could fuel inflation, prompting the Federal Reserve to reverse course and resume interest rate hikes. Since gold yields no interest and incurs storage costs, higher interest rates would highlight the opportunity cost of holding it, encouraging capital to exit the gold market.

A third theory suggests that countries already facing economic difficulties saw their currencies come under severe pressure after the war broke out. Central banks of these nations had little choice but to sell gold reserves and use the proceeds in US dollars to buy back their own currencies in order to support exchange rates. Turkey was cited as a clear example of this behavior.

Additionally, the countries directly involved in the conflict are major oil producers with substantial “petrodollars” that they normally invest globally. Once hostilities began, their oil exports were disrupted, causing a sharp drop in revenue. As a result, they were forced to sell gold to generate emergency liquidity, adding further downward pressure on gold prices.

While all the above explanations sound plausible, the true underlying cause of the gold price decline remains unclear. In any market, both bullish and bearish factors always coexist. Therefore, regardless of whether prices rise or fall, it is never difficult to find seemingly logical explanations after the fact. The real question is whether these explanations can reliably guide future investment decisions.

If we follow the logic of the reasons mentioned earlier — that war causes gold prices to fall — then one might assume that any signs of peace or reconciliation would lead to a rebound in gold prices. However, I believe this may not necessarily be the case. In my view, whether gold prices rise or fall after the war will ultimately depend on which side emerges victorious.

The victor will seize the spoils of war, gain control over the redistribution of regional resources, and exert significantly greater influence over the global order.

I believe the main reason gold prices fell sharply in the early stages of this conflict is that the United States achieved a swift and decisive victory. By eliminating Iran’s top leadership in one stroke, the US created the possibility of regime change and the installation of a pro-American government in Iran. Should the US succeed in this strategic objective, it would bring the majority of the world’s oil resources under its effective control. If America could then persuade Russia to join it in containing China, China’s rise might be stalled due to energy shortages. This would remove China as a major strategic threat, allowing the United States to solidify its position as the unchallenged global hegemon. In such a scenario, no country would dare push for de-dollarization. Anyone showing the slightest defiance could be dealt with in the same manner as Iran.

@Pontus91 No, the claim isn't correct.

Gold didn't crash in 1979—it surged ~126% that year (from ~$226/oz to $512/oz) amid the Iranian Revolution & oil crisis. It peaked at ~$850 in Jan 1980, then dropped ~60% over 1980-82 due to Volcker's rate hikes (not the 1979 events).

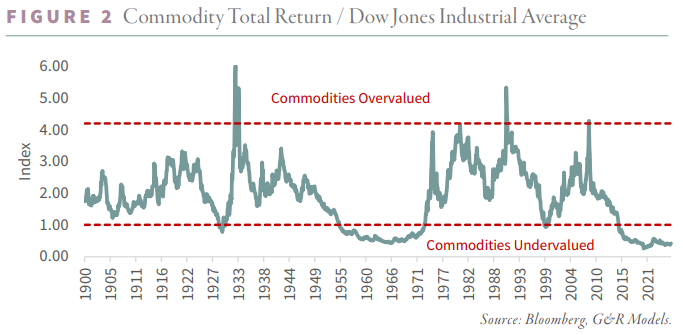

People act like the commodity trade is already crowded.

But even after the move in gold, silver, copper, and a lot of resource names, commodities still look historically cheap relative to the Dow.

That is usually not how a fully mature bull market looks.

Inevitably, #PreciousMetals miners finally felt the combined heat of rising #RiskAversion, surging #CrudeOil prices, geopolitical mayhem, and falling equities. They are equities too, after all. 🥲

In my opinion, as I’ve written here many times before, this correction was simply overdue. They just found a convenient trigger to ignite it. It’s not surprising to give back 20% in a month after rocketing 311% higher in 9 months, like #SILJ did. Even the more composed #GDXJ pulled off a 260% rise across 13 monthly bars, with only two red candles in between. 😵

And we’re talking about lazy ETFs here. The right single names did far better than that. So no, if you managed your risk properly, you really shouldn’t be too bothered by the last couple of weeks.

Unless you bought after the 2025 space launch... but at that point, #RiskManagement is probably not your main issue. 😅

I don’t think it’s a coincidence that we finally spilled some blood right after the best quarterly results ever. 😌

Those headlines brought in legions of newly minted gold bugs who knew nothing about the sector and simply chased the story. They need to be slaughtered before the trend resumes, as markets always do. 😬

Fundamentals for the mining companies have not changed dramatically, not even with #WTIC around $100. Crude oil is not a dominant driver of #AISC, even if it is large enough to matter.

Energy typically accounts for roughly 10–20% of mining costs, varying widely between mines. That means oil sensitivity is roughly this: a 10% move in oil translates into about a 1–2% move in AISC.

#Miners surely didn’t like oil jumping 50% in a couple of weeks, but they absolutely liked #gold rising 200% and #silver 300% over the last three years even more. ☺️

Relax and enjoy your weekend, even if your portfolio is bleeding a little. It’s a good time to assess your risk and overall exposure, making sure your position sizing fits the new market conditions so you don’t end up putting your amygdala in charge at the worst possible moment. 🤠