2019 is year of accumulation BTC,ETH

Mid 2021 to end 2021 is for selling

2023 is year of accumulation BTC,ETH

Mid 2025 to end 2025 is for selling

2027 is year of accumulation BTC,ETH

Mid 2029 to end 2029 is for selling

If you aren't following all of Ben's content, you are making a mistake. Especially if you are still learning and want to learn awesome new tips and tricks

$SIVE is the GameStop of 2026, and Serenity is its Wallstreetbets.

$SIVE is not a strong company. Its technology lacks meaningful differentiation. Execution has been consistently weak. Manufacturing capabilities remain mediocre at best.

The much-touted $700M pipeline is largely meaningless. Garbage in, garbage out. Having reviewed numerous startups and established players over the years, I have seen pipelines that generate little to no revenue time and again. It is straightforward to inflate these figures: one introductory meeting with a junior contact, an entry in Salesforce, and an inflated LTV projection, sufficient to impress investors who chase headline numbers.

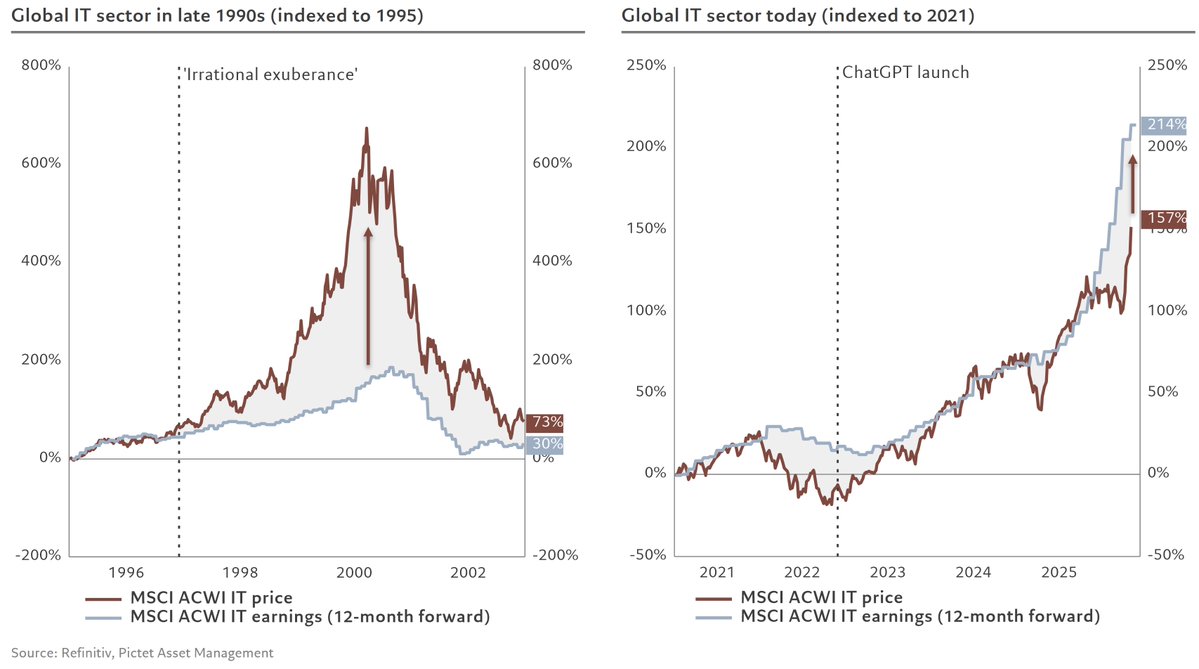

More importantly, when companies like $SIVE command such rapid valuation growth, it confirms we are in a substantial bubble. If you wish to gamble, that is your choice. This is a free market. One can always visit a casino and play roulette. Your capital, your risk.

$SOXX sits at all-time highs. With multiple semiconductor cycles behind me, I have observed this pattern repeatedly. Debates about “this time is different” can continue indefinitely. My advice remains straightforward: exercise caution. Avoid investing in weak companies. There are no hidden gems. $POET, $SIVE, $LWLG, $AEVA, and similar names are fundamentally flawed.

SpaceX starts trading this Friday.

Here's what history says happens next.

This is the post-IPO performance of every major tech listing of the last decade. Every name you know. Every name you use.

Look at the last column: maximum drawdown in year one.

– Facebook: -54%

– Snap: -56%

– Uber: -68%

– Pinterest: -70%

– Lyft: -79%

– Rivian: -88%

– Robinhood: -90%

Median first-year drawdown across the entire list: -54%.

Average: -55%.

Not the speculative junk. The whole class. Including the eventual winners.

Zoom eventually rose 142% in year one. It still drew down 40% along the way. Palantir gained 153%. It still fell 53% at one point. CrowdStrike, Datadog, MongoDB. All ended year one higher. All put their holders through a 40 to 67% drawdown first.

There has not been a single major tech IPO in a decade that didn't hand you a brutal drawdown in the first twelve months. Not one.

Now SpaceX joins the list, at the richest valuation in IPO history.

You don't have to buy it today.

The IPO is the seller's moment, not the buyer's.

Wait for the base.

copying product features is similarly hard to coming up with new features

it requires understanding if and why something works, which is super time consuming

copying is only easy when something reaches a billion arr

I was recently chatting with my business school alum working at Salesforce ($CRM). Note that Salesforce is in the application layer of Jensen's 5 layered AI cake: Energy - >Chips - > Infrastructure - >Models - > Applications.

A few interesting things he shared:

1. Application folks have a massive structural advantage: low Capex. Unlike infra folks, they are not forced to burn billions buying chips. Rent compute power when there is clear customer ROI.

2. Management is completely "Eating their own cooking". Agentforce is their software to automate customer service. They are their own first customer and have reduced customer service agents from 9K to 5K already. Agentforce is deflecting 50% of routine tickets.

3. I didnt know. But Salesforce is a cash flow machine. Their cash flow quadrupled to about $15B in last 5 years.

4. Internal sentiment is pretty bullish. Managment is buying out about $50B of stock while retail panics over seat contraction.

Fascinating to hear how different the internal reality is compared to public narrative. Probably a long term compunder hiding in plain sight.

500,000 SoCs are peanuts. In order for a company to be able to address small customers, the company needs to have several capabilities e.g.

1. Easy to use tools and SDKs

2. Extensive documentation

3. Low touch/ No touch support

4. Distis across geographies

Qualcomm isn't built for that. It is a completely different business model than how Texas Instruments, NXP and ST Micro are run.

The support from this community means a lot to me.

To give back, I’m increasing the giveaway.

I will distribute a total of 1,000,000 $BUG to 10 people.

Each winner will receive 100,000 $BUG.

How to join:

• Write “$BUG” on a piece of paper

• Hold it in your hand

• Record a short video saying “I love BUG”

• Post the video in the replies

• Like and comment your SOL address

I will randomly choose 10 winners from the video replies.

Thank you for being part of this journey.

Let’s keep building.