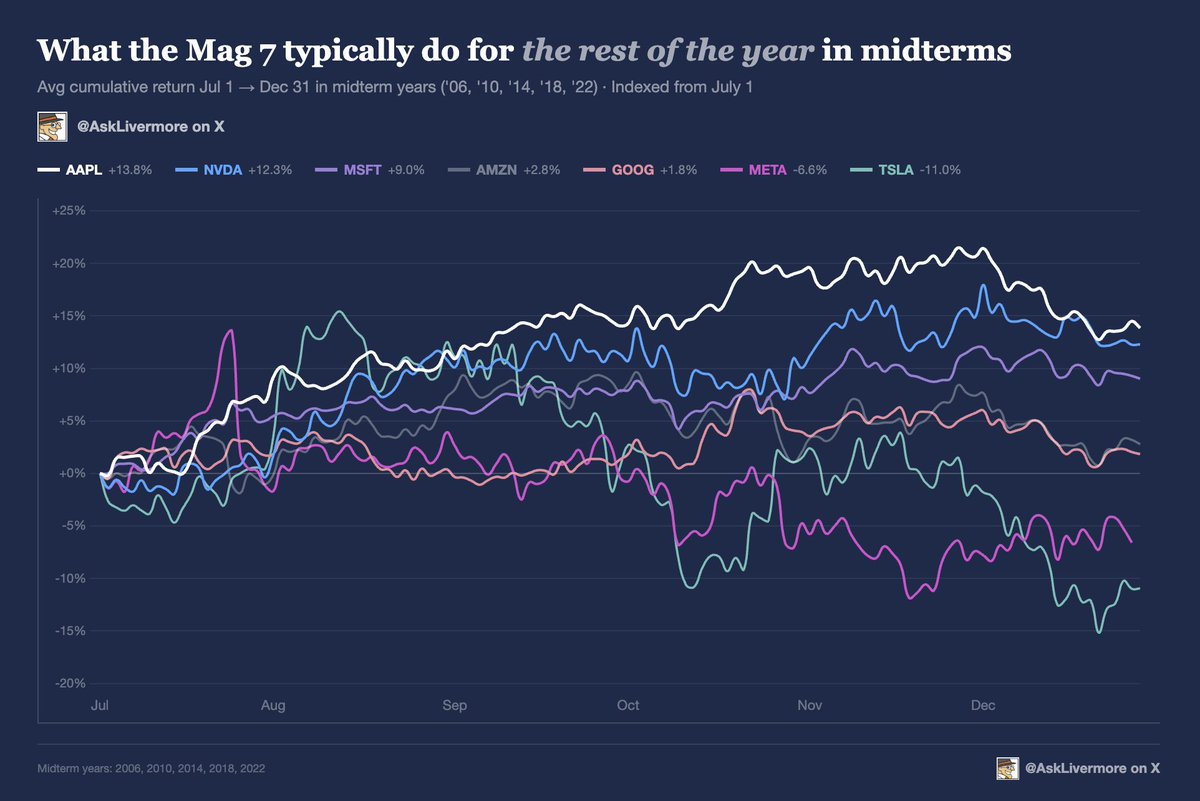

This is what Mag 7s typically do for the REST of the YEAR during a mid-term year.

Here's what happens - and why:

1. $AAPL (+13.8%): the king of the second half

• iPhone launch cycle (announced Sep, ships Oct) gives it a built-in CATALYST right when the post-midterm rally kicks in

• plus Apple's buyback PROGRAM puts a floor under the stock during the weak months

2. $NVDA (+12.3%) - the surprise second-half performer

• semiconductor capex gets PAUSED in the first half when businesses get nervous

• but once midterm uncertainty clears, that pent-up demand SNAPS back hard in Q3/Q4

• the second half is where NVDA makes ALL of its midterm year gains

3. $MSFT (+9.0%) - the steady grinder that accelerates late

• nobody cancels their Microsoft licenses during political uncertainty

• but the real move comes Oct-Dec when enterprise budgets get DEPLOYED before year-end

• reliable, boring, and quietly one of the best H2 performers

4. $AMZN (+2.8%) - modest but positive

• the second half brings holiday spending which LIFTS the retail side

• AWS capex concerns ease as enterprises stop deferring cloud spend

• not exciting, but at least it stops bleeding

5. $GOOGL (+1.8%) - barely positive

• SMB ad budgets start to RECOVER post-midterm but it's slow

• regulatory headlines tend to FADE after elections

• gets back to flat but don't expect fireworks

6. $META (-6.6%) - the second-half disappointment

• despite strong digital ad trends, META tends to GIVE BACK gains in H2

• earnings volatility keeps Wall Street nervous — one miss and it gets PUNISHED

• the wild swings that help in H1 work AGAINST it when sentiment shifts

7. $TSLA (-11.0%) - the worst of the group

• big-ticket consumer discretionary SUFFERS as midterm anxiety lingers

• Tesla trades on SENTIMENT more than fundamentals

• historically the one to AVOID in the second half of midterm years

The takeaway heading into the second half of 2026:

$AAPL and $NVDA are the clear WINNERS - both averaging double-digit gains from July through December.

If you're heavy in $META or $TSLA, consider OFFSETTING potential weakness with stocks in healthcare, industrials, and financials.

They will do MUCH better in 2027.

High SaaS multiples are in the past. A permanent rerating has occurred. The high multiples we once had, are in the past.

That does not mean you should ignore them. There is still quality, there is still growth.

I believe having exposure to some of these 10 SaaS companies won't hurt.

Which one is your favorite?

1. $NOW - ServiceNow

“Liberated,” they said.

Bakhmut today shows what that word really means.

A city of 70,000 people, reduced to rubble after more than two years under “russkiy mir.”

Only ruins where a city once stood.

And the silence around it says as much as the destruction itself.

This is a message to the peoples and regions of Russia

You have the right to self-determination and to rise up for freedom and independence from Moscow.

Only you can decide your own fate!

Together, we can cut Moscow off from the riches of Komi, Ingria, Karelia, the Caucasus, the Kuban, the Volga Region, the Urals, Siberia, and the Far East.

Let's defeat the empire together!

Join us!

https://t.co/JXgaDD6928

https://t.co/V0Of6ztgl3

https://t.co/oe2AH4iSto

https://t.co/Vi2ctUa5Wp

https://t.co/k5v1V7Mrzx

https://t.co/zIgXMSfPLD

Lest we forget.

On June 27, 2022, russia struck the Amstor Shopping Center in Kremenchuk while it was full of civilians.

22 people were killed. Over 50 injured.

And it didn’t stop there — because the world moved on.

Probably something everyone should consider doing is increase their exposure to non-AI, low valuation, and wide MOAT companies.

You don't want to have a lot of exposure to high beta names that can risk selling off quickly - 20%, 30%, or even more in just days.

I talked about American Express 2+ weeks ago, and Visa and Mastercard. They are still dirt cheap, high ROIC companies and not going away anytime soon. A lot of stablecoin fear has knocked them to multi-year lows.

Probably worth investigating these companies if you haven't already.

The ATGs in Credit Card Processing

Why am I a believer in these 3 credit card companies?

Highlights:

> Crypto can’t replace credit cards; consumers desire “friction” in transactions.

> American Express is tailored towards an affluent group of people compared to Visa and Mastercard. Think of Toyota/Honda compared to Ferrari.

> Mastercard and Visa are a duopoly; 90% of the market share in the U.S.

> Mastercard has seen the fastest growth in total cards of 232% over 13 years.

> American Express perks and rewards allow for higher APR and transaction fee.

> Visa and Mastercard are an open-loop system while American Express is closed-loop; vertically integrated.

> Risk of international protectionism and credit risk exists in current market.

> All 3 companies present high switching costs for 3 parties: merchants, bank, and consumer.

> Mastercard has the highest ROIC, in the 40s for the past half decade.

> Average PT of $372.50 for $V, $575 for $MA, and $390 for $AXP

Check it out 👇

https://t.co/MB4uqwSEyY

New High Conviction Buy: $INSM

Market Cap: $22.4B

Portfolio Allocation: 5%

Current Price: $103

Average Analyst Price Target: $215

Insmed ( $INSM ) is one of those rare situations where Wall Street seems to be focused on the next quarter, while some of the smartest biotech investors are looking several years ahead. We have seen similar pattern in all our recent wining picks.

The company develops medicines for serious lung diseases with few effective treatment options. Its lead product, Brinsupri, was recently launched for patients with bronchiectasis suffering from recurrent lung infections.

Earlier this year, the stock fell nearly 50% after the initial launch failed to meet the market’s extremely high expectations. Investors had expected an explosive rollout, but early prescription growth came in slower than hoped, leading many to question whether the launch was falling apart.

So far, that doesn’t appear to be the case.

Prescription trends have continued to improve, physicians remain optimistic, and several recent reports from JPMorgan, UBS and other research firms support our view that the market became overly focused on the first few months of prescriptions while missing the much bigger story. They also believe Brinsupri still has the potential to become a multi-billion-dollar drug as physician adoption expands and reimbursement improves over time.

From a technical standpoint, the stock also appears to have found a bottom after the 50% decline, with selling pressure easing while the underlying business continues to execute.

That alone would make Insmed interesting. But the pipeline may be even more valuable.

The company’s inhaled treprostinil program for pulmonary arterial hypertension (PAH) could become another major growth driver, with important clinical data expected in 2026. If successful, Insmed would evolve from a one-product company into a diversified rare disease leader with multiple blockbuster opportunities.

Wall Street still sees substantial upside. Average analyst price targets remain well above today’s share price, with many analysts believing the recent selloff reflects timing rather than a deterioration in the long-term opportunity.

Perhaps the most interesting signal, however, comes from who owns the stock.

This isn’t a company being accumulated by generalist momentum funds. It is owned by some of the most respected healthcare investors in the world.

RTW Investments: 7.9% of its portfolio.

Baker Bros. Advisors: 7.0%.

Stanley Druckenmiller: 6.4%.

And perhaps most impressively, Darwin Global Management, one of biotech’s premier specialist hedge funds, has made Insmed roughly 68% of its disclosed public equity portfolio.

That level of concentration is almost unheard of. Specialist biotech investors spend years building relationships with physicians, researchers and management teams. While no investor is always right, seeing multiple world-class healthcare investors independently build such meaningful positions deserves attention.

The investment case ultimately comes down to one question.

If Brinsupri continues executing as prescription trends suggest, and the PAH program delivers positive clinical data next year, today’s valuation could look surprisingly inexpensive in hindsight.

The market is pricing execution risk.

The specialists appear to believe the market is underestimating the probability of success.

That’s exactly the kind of disconnect that often creates the best long-term investment opportunities.

Brokers research attached below.

Прямо сейчас россияне бьют авиабомбами по украинской Дружковке.

По жилым домам.

В городе живут более 6 000 человек. Это должен видеть мир.

Россия государство террорист.

@dutchman050@johannesmkx The men here will keep those freaks in line or scare them out of the nation. We don't fuck around over here like the cowards in Europe

To anyone who takes russia's side and says they are "liberating russian speakers"

Look, just look, THIS is what russian liberation looks like, THIS is the ruskie mir (russian world)

All they know is death.

June 2026 is DOWN -3.90%.

Since 2005, there have been 12 times where JUNE closed red.

10 out of 12 times, July was GREEN.

That's an 83% win rate.

The LAST 3 times June dropped more than -3%:

• 2022: June -7.90% → July +8.07%

• 2010: June -4.01% → July +7.31%

• 2009: June -2.98% → July +7.02%

Average JULY bounce after a big June selloff: +7.47%.

2026 is also a MIDTERM election year.

July in midterm years SINCE 2006:

• 2006: +0.04%

• 2010: +7.31%

• 2018: +3.48%

• 2022: +8.07%

Win rate: 80%. Average: +3.38%.

The last midterm July?

SPY ripped +8% in a SINGLE month.

History doesn't guarantee anything.

But when 83% of the data points in the same direction, make sure you PAY attention.

A man who sleeps with 1000 women is admired because he did something hard that very few men can do. Many guys can’t even get 1 girl.

A woman who sleeps with just 1 man her whole life is admired because it’s hard. Temptation comes at her from every direction as soon as she hits puberty, and she was strong enough to resist and stay pure for her future husband.

In both cases, doing what’s hard is admired because it’s rare. Any woman can sleep with a hundred guys. It’s easy. No effort required. So a woman doing the same shouldn’t be applauded. She is rightfully shamed as a slut

Забайкальский край в топе по количеству террористов которые едут в Украину убивать, пытать, насиловать и грабить людей.

У террористов не должно быть нефти

My dear followers.

Get READY for July, SURVIVE September, and ride the October-November move for 2026.

Here's how every sector PERFORMS month by month during MID-TERMS and what it means heading into July.

July:

- the BROADEST strength of the entire back half

- every single sector finishes POSITIVE

- tech, energy, and consumer discretionary lead with +4% moves

August:

- the rally STALLS

- half the sectors turn NEGATIVE

- biotech $XBI is the standout at +4.52% while energy $XLE and materials $XLB fade

September:

- this is the month to be CAREFUL

- nearly every sector DIPS

- utilities $XLU and real estate $XLRE get hit hardest

- if you're adding exposure, this is where you WAIT

October:

- the TURN

- STRENGTH comes back almost everywhere

- staples $XLP LEAD at +3.91%, but even the LAGGARDS catch a bid.

- this is historically where the midterm LOW gets put in.

November:

- CONTINUATION

- materials $XLB rip +4.57%. industrials $XLI +3.79%. the cyclicals take over

December:

- profit-taking

- almost every sector gives BACK

- tech DROPS -3.45%, energy -3.01%

- the back half rally takes a BREATHER before the post-midterm year kicks in

A lot of traders have setups. But they do NOT know the timing cycles.

I will always make sure you're STEPS ahead of everyone else.