On current grounds (feedstock secured, plant advancing, strong market tailwinds), a fair risked corporate valuation could justify AUD 50–150M market cap in a successful ramp-up scenario (i.e., 2–6x from here) once production starts and a resource is declared.

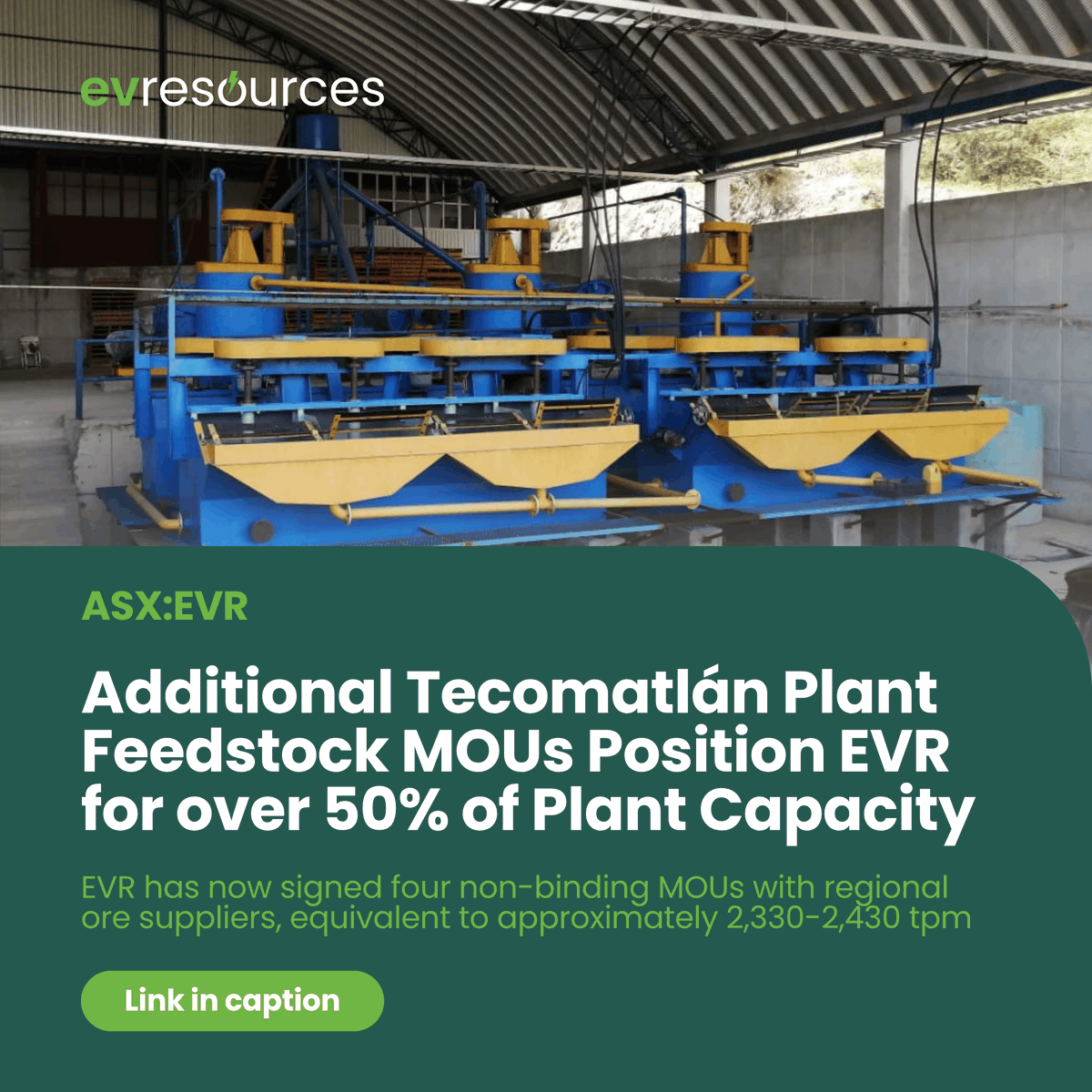

+50% of Tecomatlán Plant capacity secured via 4 feedstock MOUs, a pipeline of ~2,430 tpm high-grade feedstock, a major de-risking milestone as #EVR targets first antimony production in 2H CY26.

Full announcement: https://t.co/JiJjnxrbSK

#ASXnews#UScriticalminerals#USantimony

$CDT is now where $MPK, $WIA, + $TCG were 12–24 months ago.

That’s the kind of growth trajectory Steve and the team want the acquired Nielle discovery to drive.

🚨🇪🇺 EVER GOT A €2,500 RAISE JUST LIKE THAT?

EU bureaucrats just did. 8.5% PAY BUMP while everyone else struggles.

Ursula von der Leyen now gets +€2,500 MONTHLY.

They tell YOU save energy, stay home, don’t drive.

THEY GET RICHER. YOU PAY THE BILL.

2 Weeks Ago we were reassured we had enough fuel due to the Geelong, Victoria Oil Refinery which is one of two remaining refineries.

‘Coincidentally’ today it exploded & it is now engulfed in flames🔥

Also ‘coincidentally’ our biggest fertiliser plant went off line & will take weeks-months to become functional again.

Right in the middle of a Global fuel & fertiliser crisis….

I don’t believe in ‘coincidences’ anymore.