New X Algorithm: What X Didn’t Tell You (And What Actually Works in 2026) 🧵👇

While everyone else is guessing, I’ve spent the last 72 hours reading the entire X Algorithm code line by line since May 15, 2026.

No guru opinions. No speculation. Just the actual code.

Here’s exactly what stopped working after the May 15 Phoenix update, what’s winning right now, and what will still work months from now:

What DIED (according to the code):

1. Spamming 4+ posts a day:

The algorithm punishes you hard with *Author Diversity Decay*. Your 2nd, 3rd, and 4th posts get exponentially weaker reach in the same user’s feed.

2. Low-effort reply farming:

Generic replies (“🔥”, “Great point”, emoji spam) get buried. Grok literally reads and ranks replies now.

3. Pure text-only posts:

They work… but text + image or video (≥10 seconds) consistently outperforms them because of extra visual + dwell signals.

4. AI slop & recycled templates:

There’s an explicit `slop_score` + quality classifier. Low-originality content gets flagged fast.

5. Cheap engagement bait:

“What do you think?” or “Tag someone who needs this” increases scroll-past rate → active penalty via `not_dwelled` signal.

What’s WINNING (and will keep winning):

1. Original, unique takes from small accounts:

Original posts get full Grok evaluation + better out-of-network discovery.

2. Text + Media combos (especially video ≥10s with audio):

Hybrid format maximizes multiple positive signals at once.

3. Contrarian opinions backed by real proof:

Numbers, screenshots, personal results → higher dwell time, more replies & quotes.

4. Early, high-quality replies to big accounts (first 10-30 minutes):

One of the strongest growth levers for small accounts right now.

5. Real conversation > likes:

Quality replies + replying to your own comments in the first 30 minutes is pure ranking gold.

My Day-One Test Results (Real Data):

Reply 1 (contrarian + technical angle, +9 min after Elon’s post):

→ 214 impressions • 43 engagements • 39 detail expands • 2 profile visits.

👉[Link: https://t.co/OzScqzNbG7]

Reply 2 (thoughtful transparency take + direct question to Elon):

→ 45 impressions • 8 engagements • 0 profile visits

👉[Link: https://t.co/JMr7nZveCt]

No viral explosion. Just clean data.

The real question isn’t whether 214 or 45 impressions is a failure. It’s whether you’re willing to treat it as data.

Most people won’t.

The ones who do are the ones who win.

The Evergreen Playbook (Use This Today & Months From Now):

- Cut volume to 1–2 high-quality posts per day max.

- Always pair text with image, carousel, or short video.

- Reply to every real comment in the first 30 minutes.

- Lead with first-person stories + concrete proof.

- One bold, specific opinion per post.

- Focus on dwell time and real replies, not just likes.

The Honest Question:

Does this algorithm truly favor small accounts, or does it quietly give bigger accounts an unbeatable head start?

It feels like a meritocracy with momentum, the rich get richer, but original, high-signal content from smaller accounts can still break through.

I’m testing it publicly and aggressively for the next 30 days.

If you want the full 72-hour technical breakdown (with every file reference, exact constants, codes, tables, and the hidden parts X didn’t publish), just say it in the comments below and I’ll post it in as reply to your comments.

Save this post.

The algorithm might change again in few months, but these principles won’t.

I hope you've found this post helpful.

Comment. Repost. Bookmark.

Follow me @DrMelchisedecB for more...

What’s your first move after reading this?

Drop it below 👇

I read through the published code.

First, genuine respect to the X engineering team. Since Elon Musk took over, the technical quality of what's been built here is serious. The Phoenix transformer architecture, the Rust pipeline, the Grok integration, the two-tower retrieval system, this is world-class infrastructure.

Publishing the code at all took confidence. Most platforms would never do it.

The architecture is open. The weights aren't. I know likes add points and blocks subtract them, but not by how much. Grok scans every post for quality vs slop using classifier prompts that aren't published, so whatever biases are baked in, nobody can audit them. There's also a DO_NOT_AMPLIFY label X employees can attach to any account silently, no notification, no appeal anywhere in the code.

The repo shows you the engine. It doesn't show you who's steering it or with what settings.

A team this technically strong could publish the weight values and classifier prompts without exposing anything competitively sensitive. The skeleton is already out there. Releasing the muscle would make this the most transparent recommendation system ever shipped by a major platform.

Any plans to publish the weights and classifier prompts, even partially, even versioned snapshots?

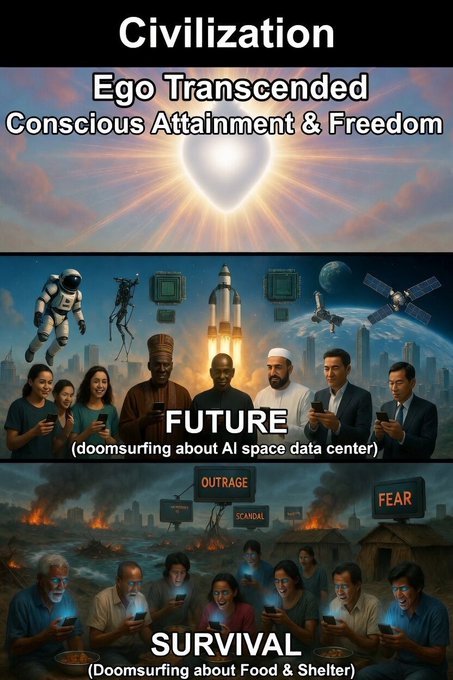

Survival layer:

Doomsurfing the Apocalypse - Food & Shelter.

Burned world. Floods. Fires. Wars.

Everyone glued to phones, feeding on Outrage, Scandal & Fear.

Future layer:

Doomsurfing AI & Space.

Shining cities. Rockets. Satellites. Data centers.

Everyone glued to phones, feeding on Optimism, Progress & Wonder.

Human layer:

Ego Transcended. Conscious Attainment & Freedom.

Everything else is theater.

Are we building the heart as we build technology?

History doesn’t repeat exactly the same way, but it often follows similar patterns, beats, and mistakes.

We used to give away our factories & industry → “too expensive” → “globalization wins!” → now the jobs and power are gone.

Now we’re repeating the same pattern with AI → Outsourcing infrastructure, industrial secrets, future, intelligence layers, and strategic capability to frontier models → “100x faster!” → “sovereignty is for boomers.”

Different technology. Same trade.

Only this time, the dependency is deeper.

Because when intelligence itself becomes the platform, whoever owns the model owns the ecosystem.

And everyone else? Just tenants inside it.

End result? One proprietary AI owns the entire ecosystem… and you’re not even in the room.

This isn’t progress.

This is how nations (civilizations and people) become the product.

Build. Own. Stay sovereign.

Or kneel later.

The various modes of over 40,000 religions that have prevailed in the world are all considered:

-by the masses as equally true,

-by the wise who transcend the ego (attaining God's quality of love in the intention) as equally false, and

-by politicians as equally useful.

@renoomokri SpaceX IPO: To the Moon or To Bankruptcy?

Buy at Open or Abeg Wait?

The Great SPCX Debate.

For deeper breakdown of the SpaceX IPO's S-1 numbers, Starship timeline & what it means, check my full take below 👇

https://t.co/1DYFY6EiUR

Elon Musk will control 82.4% of SpaceX after the IPO. You will control 11.5%.

$135 per share. 555 million shares.

$74.4 billion in net proceeds. $1.765 trillion target valuation.

SpaceX just dropped its S-1 with the SEC and the numbers inside it are unlike anything I've seen from a single filing.

I went through it so you don't have to.

Thread below.🧵👇

1/

SpaceX S-1/A - The Numbers Filed June 3, 2026 | Nasdaq: SPCX

2/

The Offer

$135.00 - IPO price per share

555,555,555 - Class A shares offered

83,333,333 - additional shares if underwriters exercise in full

$75.0B - gross proceeds at base

$74.4B - net proceeds at base

$85.7B - net proceeds if underwriters go full

3/

Voting Structure - straight from the filing

Class A: 1 vote per share

Class B: 10 votes per share

Class A voting power after offering: 11.5% (11.6% if underwriters exercise in full)

Class B voting power after offering: 88.5% (88.4% if underwriters exercise in full)

Elon Musk holds ~82.4% of total voting power post-IPO.

81.1% of that comes from Class B alone.

The public buys 555 million shares and controls 11.5% of the vote.

Elon Musk controls the rest.

Permanently.

By design.

You are buying economic exposure. Not governance. Know what you're buying.

4/

Share Count and Market Cap - the precise math

7,380,196,910 - Class A shares outstanding

5,695,668,265 - Class B shares outstanding

13,075,865,175 - total shares outstanding

5-for-1 - stock split effected May 4, 2026

At $135.00 per share:

$1.765 trillion market cap at base.

$1.776 trillion if underwriters exercise in full.

The $1.75T-$2.0T range you keep seeing is not hype. It is the math from the filing.

5/

What's Actually Inside the Ticker

This is not a rocket company IPO. The filing consolidates three businesses into one:

Space - Falcon, Dragon, Starship

Connectivity - Starlink

AI - Grok, X, COLOSSUS compute

xAI acquired Feb 2, 2026.

X Holdings folded into xAI Mar 28, 2025.

One S-1. Three companies.

6/

Starlink - FY2025

$11.387B - revenue

$4.423B - operating income

38%+ - operating margin

49.8% - year-over-year growth

10.3M - subscribers

164 - countries served

~9,600 - satellites in LEO

Starlink is the cash engine.

This is the business generating real money today.

7/

Total Company - the full picture

$18.674B - consolidated FY2025 revenue

$4.94B - GAAP net loss FY2025

$4.28B - GAAP net loss Q1 2026 alone

22,000+ - full-time employees

80%+ - share of global mass-to-orbit since 2023

99%+ - Falcon mission success rate

Starlink prints cash. The AI buildout burns it faster. The market is pricing the future, not the present.

8/

Valuation Context

$421 - share price at December 2025 tender offer

$800B - implied valuation at that tender

$1.765T - precise market cap at IPO price

~92x - revenue multiple the market is assigning

This is not an aerospace multiple. It is an AI infrastructure multiple.

In six months the implied valuation more than doubled.

The rocket business didn't change. The AI narrative did.

9/

The Underwriter Syndicate

Goldman. Morgan Stanley. BofA. Citi. JPMorgan.

Barclays, Deutsche Bank, RBC, UBS, Wells Fargo.

Allen & Company, Cantor, Needham, Raymond James, SocGen, Stifel, William Blair.

5% of shares reserved for a directed share program - employees and individuals selected at executive discretion.

Every major bank on Wall Street wants a piece of this.

10/

The Starship Dependency

This is the number nobody is talking about.

H2 2026 - Starship first commercial payload to orbit

H2 2026 - V3 Starlink satellites (1 Tbps each) need Starship to launch

2027 - V2 Mobile satellites need Starship

2028 - orbital AI compute satellites need Starship

1 terawatt - Terafab's long-term compute production goal

V3 satellites physically cannot fit in a Falcon 9.

Every premium product. Every next-gen revenue line. All of it runs through one vehicle that has not yet delivered commercial payload to orbit.

11/

Every number above is load-bearing.

The $1.765T valuation is a bet that the 2026-2028 Starship delivery sequence executes on schedule.

If it does, Connectivity and AI reprice upward together.

If it slips, $4.28B quarterly losses with no growth catalyst is a very uncomfortable place to be.

Are you buying SPCX at open?

What's your read on the Starship timeline?

If this cleared things up for you, comment, repost it, quote it, and tag one friend.

12/

This SpaceX IPO is one of the most important moments in AI infrastructure this year.

But if you want to understand why the entire global chip industry is under massive pressure right now, you need to read this immediately👇

Why The Global Chip Industry Just Got Served A $119 Billion Eviction Notice

https://t.co/s1ckBcNVLg

Follow @DrMelchisedecB for more high-signal breakdowns on SpaceX, Starship, AI infrastructure, and the systems moving the world forward.

Haha, I wish it was pure comedy, but it's actually a serious point.

The "feed people first" argument is recurring historical pattern.

Orbital compute and Terafab aren't luxuries.

They're the next infrastructure layer that can accelerate abundance for everyone, especially in food, medicine, and energy.

Glad you enjoyed the meme though! Worth checking the full post here👇

https://t.co/F1z1EuIALN

Survival is Not Enough: Why Humanity Needs Terafab, SpaceX & Orbital Frontiers🧵👇

I think the "feed people first, explore later" argument is the most well-intentioned economic mistake in history.

You're not wrong that people are hungry today. You're wrong about what fixes it.

Every infrastructure that feeds, heals, and connects people today was once called a distraction from feeding, healing, and connecting people.

I disagree with how this debate is being framed.

The argument against orbital compute and space industrialization goes like this: people are struggling today, so ambitious frontier projects are a distraction. I've heard it hundreds of times. I think it misunderstands how civilization actually builds wealth.

Here is what I observed when I ran the numbers on transformative technologies:

Every platform that now supports billions of people was once dismissed as an impractical dream built while ordinary people faced daily hardships.

I looked at electricity. Critics called it a rich man's novelty.

Today it runs hospitals, water pumps, factories, and homes across the planet, lifting more people out of subsistence living than any aid program in history.

I looked at aviation.

Mocked as a reckless folly.

Today it moves billions of passengers and trillions in cargo annually, compressing distances that once separated continents into hours.

I looked at the internet.

Dismissed as an academic curiosity with no real-world use.

Today it is the backbone of global commerce, education, healthcare, and communication.

I also traced each technology back to its origin.

Every single one started as a frontier project funded before its ROI was obvious:

Commercial aviation came from experimental flight.

GPS came from military space programs.

The internet came from government-funded research networks.

Modern weather forecasting depends on satellites.

Global communications run on orbital infrastructure.

The pattern is not random. Frontier investment compounds into mass-market utility, consistently, across every domain I analyzed.

You are looking at the outcome and calling it impractical.

I am looking at the mechanism and calling it predictable.

Now apply that pattern here:

Terafab + Tesla + SpaceX + xAI + Intel combining logic, memory, and advanced packaging under one roof, is targeting 1 TW/year in chip output.

For context: the entire U.S. currently consumes 0.5 TW annually.

These aren't chips competing with Nvidia, Intel, TSMC, SMIC, Samsung Electronic.

The D3 chip is designed explicitly for orbital deployment, a category that doesn't exist yet but will dwarf today's entire semiconductor market.

Elon Musk says 80% of that output goes to orbital AI satellites, citing 5x solar irradiance in space and easier heat rejection in vacuum.

Is it locked in?

No, SpaceX's own S-1 calls the deal "very early stages" with no binding terms, and skeptics are already drawing Battery Day comparisons.

I think that's the wrong lens.

Verbatim excerpt from SpaceX's S-1 (File No. 333-296070) filings (as reported directly in the document):

"Certain of these projects, including Macrohard and Terafab, are in the very early stages, as a result of which we and Tesla have not finalized a variety of details relating to our collaboration, including, but not limited to, financial terms, intellectual property rights, and any timeline for delivery or commercialization, and there are no binding commitments with respect to these projects."

Skepticism is good for engineering, but I view engineering progress as a process in which today's hype often becomes tomorrow's hardware once the physics is solved through iterative development.

Historically, the team have the records of compressing timelines that many people considered impossible.

I have seen this with reusability, the scale of the Starlink constellation, and Gigafactory ramps.

That doesn't make skepticism invalid, especially when it comes to space hardware.

It simply means I prefer to evaluate the physics directly.

I see engineering as a process of confronting constraints, quantifying them, and iterating toward solutions.

In my view, the viability of Terafab and orbital compute will ultimately be determined by hardware performance, economics, and operational data.

The frontier-to-utility pattern doesn't require every announced project to land on schedule, it requires the direction to be correct.

Even a partial realization of Terafab's orbital ambition reshapes the compute available for climate modeling, drug discovery, and agricultural forecasting.

Looking at what orbital semiconductor manufacturing could mean at scale.

The answer is not just cheaper chips, it is a step-change in computing capacity that would accelerate drug discovery, climate modeling, energy optimization, and agricultural yield forecasting simultaneously.

The people who would benefit most are not in Silicon Valley.

They are the ones you claim frontier projects are ignoring.

Here is what I think most people get wrong about this debate:

The tension is real.

A parent worrying about feeding children today is not wrong.

A civilization building long-term frontier capacity is not wrong.

The mistake is treating these as mutually exclusive.

I have studied enough economic history to say with confidence: they are not.

The most successful civilizations did not choose between bread and cathedrals, between food and exploration, between survival and ambition.

They built both, and the ambition consistently produced the abundance.

I have one question for everyone still arguing from the survival frame:

If every generation before us had chosen only to manage today's crisis and delayed the frontier investment that felt "impractical" at the time, would the infrastructure you rely on to make that argument even exist?

If this cleared things up for you, comment, repost it, quote it, and tag one friend.

For a deep dive on Why The Global Chip Industry Just Got Served A $119 Billion Eviction Notice read the full article here🧵👇

https://t.co/s1ckBcNVLg

Follow me @DrMelchisedecB for more simple, high-signal breakdowns on Geopolitics, Solar Energy, Ai, SpaceX, Starship, and how builders are moving humanity forward.

Survival is Not Enough: Why Humanity Needs Terafab, SpaceX & Orbital Frontiers🧵👇

I think the "feed people first, explore later" argument is the most well-intentioned economic mistake in history.

You're not wrong that people are hungry today. You're wrong about what fixes it.

Every infrastructure that feeds, heals, and connects people today was once called a distraction from feeding, healing, and connecting people.

I disagree with how this debate is being framed.

The argument against orbital compute and space industrialization goes like this: people are struggling today, so ambitious frontier projects are a distraction. I've heard it hundreds of times. I think it misunderstands how civilization actually builds wealth.

Here is what I observed when I ran the numbers on transformative technologies:

Every platform that now supports billions of people was once dismissed as an impractical dream built while ordinary people faced daily hardships.

I looked at electricity. Critics called it a rich man's novelty.

Today it runs hospitals, water pumps, factories, and homes across the planet, lifting more people out of subsistence living than any aid program in history.

I looked at aviation.

Mocked as a reckless folly.

Today it moves billions of passengers and trillions in cargo annually, compressing distances that once separated continents into hours.

I looked at the internet.

Dismissed as an academic curiosity with no real-world use.

Today it is the backbone of global commerce, education, healthcare, and communication.

I also traced each technology back to its origin.

Every single one started as a frontier project funded before its ROI was obvious:

Commercial aviation came from experimental flight.

GPS came from military space programs.

The internet came from government-funded research networks.

Modern weather forecasting depends on satellites.

Global communications run on orbital infrastructure.

The pattern is not random. Frontier investment compounds into mass-market utility, consistently, across every domain I analyzed.

You are looking at the outcome and calling it impractical.

I am looking at the mechanism and calling it predictable.

Now apply that pattern here:

Terafab + Tesla + SpaceX + xAI + Intel combining logic, memory, and advanced packaging under one roof, is targeting 1 TW/year in chip output.

For context: the entire U.S. currently consumes 0.5 TW annually.

These aren't chips competing with Nvidia, Intel, TSMC, SMIC, Samsung Electronic.

The D3 chip is designed explicitly for orbital deployment, a category that doesn't exist yet but will dwarf today's entire semiconductor market.

Elon Musk says 80% of that output goes to orbital AI satellites, citing 5x solar irradiance in space and easier heat rejection in vacuum.

Is it locked in?

No, SpaceX's own S-1 calls the deal "very early stages" with no binding terms, and skeptics are already drawing Battery Day comparisons.

I think that's the wrong lens.

Verbatim excerpt from SpaceX's S-1 (File No. 333-296070) filings (as reported directly in the document):

"Certain of these projects, including Macrohard and Terafab, are in the very early stages, as a result of which we and Tesla have not finalized a variety of details relating to our collaboration, including, but not limited to, financial terms, intellectual property rights, and any timeline for delivery or commercialization, and there are no binding commitments with respect to these projects."

Skepticism is good for engineering, but I view engineering progress as a process in which today's hype often becomes tomorrow's hardware once the physics is solved through iterative development.

Historically, the team have the records of compressing timelines that many people considered impossible.

I have seen this with reusability, the scale of the Starlink constellation, and Gigafactory ramps.

That doesn't make skepticism invalid, especially when it comes to space hardware.

It simply means I prefer to evaluate the physics directly.

I see engineering as a process of confronting constraints, quantifying them, and iterating toward solutions.

In my view, the viability of Terafab and orbital compute will ultimately be determined by hardware performance, economics, and operational data.

The frontier-to-utility pattern doesn't require every announced project to land on schedule, it requires the direction to be correct.

Even a partial realization of Terafab's orbital ambition reshapes the compute available for climate modeling, drug discovery, and agricultural forecasting.

Looking at what orbital semiconductor manufacturing could mean at scale.

The answer is not just cheaper chips, it is a step-change in computing capacity that would accelerate drug discovery, climate modeling, energy optimization, and agricultural yield forecasting simultaneously.

The people who would benefit most are not in Silicon Valley.

They are the ones you claim frontier projects are ignoring.

Here is what I think most people get wrong about this debate:

The tension is real.

A parent worrying about feeding children today is not wrong.

A civilization building long-term frontier capacity is not wrong.

The mistake is treating these as mutually exclusive.

I have studied enough economic history to say with confidence: they are not.

The most successful civilizations did not choose between bread and cathedrals, between food and exploration, between survival and ambition.

They built both, and the ambition consistently produced the abundance.

I have one question for everyone still arguing from the survival frame:

If every generation before us had chosen only to manage today's crisis and delayed the frontier investment that felt "impractical" at the time, would the infrastructure you rely on to make that argument even exist?

If this cleared things up for you, comment, repost it, quote it, and tag one friend.

For a deep dive on Why The Global Chip Industry Just Got Served A $119 Billion Eviction Notice read the full article here🧵👇

https://t.co/s1ckBcNVLg

Follow me @DrMelchisedecB for more simple, high-signal breakdowns on Geopolitics, Solar Energy, Ai, SpaceX, Starship, and how builders are moving humanity forward.

Why The Global Chip Industry Just Got Served A $119 Billion Eviction Notice🧵👇

Everyone's focused on which AI chip dominates Earth.

Wrong planet.

I've been studying Terafab - Tesla, SpaceX, and xAI combining logic, memory, and advanced packaging under one roof and I think this is the most important industrial announcement of the decade.

Here's why

"We've already done the impossible," multiple times:

Tesla:

1. 8M+ vehicles delivered

2. Camera-only unsupervised FSD - no lidar, no radar

3. Optimus robot designed for large-scale production

4. 109 GWh+ of energy storage deployed globally

5. Gigafactories built worldwide in record time

6. First and only lithium refinery in the U.S.

xAI:

7. Built the first GW-scale AI training cluster

8. Created the largest coherent supercomputer on Earth

9. Only company capable of building orbital AI compute at scale

SpaceX:

10. First reusable rockets, ever

11. Returned human spaceflight to the U.S.

12. Launches 90% of global mass to orbit

13. Operates the world's largest space-based internet network

14. Built the largest PCB manufacturing site in the U.S.

15. Flies the most powerful rocket ever built

These aren't credentials. They're proof of execution velocity no other org on Earth can match.

Now they're scaling for something most people can't even picture:

1 billion Tesla Optimus robots doing physical labor

10 million tons/year launched to orbit

1 TW+ of solar power required

1 TW/year in chip output from Terafab alone

For reference: the entire U.S. currently consumes 0.5 TW annually.

The chips they're building aren't competing with Nvidia:

AI5 - powers FSD and Tesla Optimus

AI6 - powers next-gen Tesla Optimus

D3 - powers space compute

...and beyond

D3 is the first chip I've seen designed explicitly for orbital deployment, a category that doesn't exist yet but will dwarf today's entire semiconductor market.

Here's my take most people won't say out loud:

Earth is a temporary substrate for AI compute.

On Earth you're fighting:

Power grid constraints

Permitting nightmares

Land costs

Cooling infrastructure

Energy costs

Political bottlenecks

In space you only deal with:

Launch cost (SpaceX is still cutting this)

Operating costs

Satellite build

Infrastructure

The next unlock is lunar mass drivers and Terafab is building the chip supply chain that makes that civilization possible.

We're Type 0.73 on the Kardashev Scale right now, we haven't even fully harnessed Earth's energy yet.

Type I means mastering a full planet.

Type II, a star.

Type III, a galaxy.

Terafab isn't a chip company. It's the first industrial infrastructure project explicitly designed to pull us from 0.73 to the stars.

You've watched Tesla, SpaceX, and xAI systematically dismantle every legacy industry that said their roadmaps were impossible.

Do you still think the terminal future of advanced AI compute stays pinned to Earth's fragile grid, or is this the exact moment the macroeconomic thesis permanently flips to space?

Drop a comment with your take, repost this thread to wake up the timeline, and tag one friend who is still sleeping on how fast the industrial landscape is shifting.

If you want to understand the raw mechanical power enabling this future, check out my breakdown of Starship’s IFT-12 launch sequence:

https://t.co/mhwSOzBC3w

No fluff, no jargon, just a high-signal look at the tower catch, the thrust metrics, and the sheer scale of the machine building the orbital conveyor belt.

Follow me

for more simple, high-signal breakdowns on Geopolitics, Energy, AI, SpaceX, Starship, and how builders are moving humanity forward.

You are spot on.

I have discovered that the cage isn’t colonialism, it’s misaligned incentives that reward extraction over production.

Internal handshake (patronage + grievance) +

External handshake ($88B illicit flows) keep reinforcing each other.

Singapore proved governance beats history.

Deng proved redesign beats resistance.

Africa has the gas, coast, youth, and remittances.

For Africa, the bottleneck is clear: 1.5 billion people with less electricity than Germany’s 84 million.

What Africa needs now is sovereign builders who execute the institutional rewrite before the 2035 AI/orbital window closes.

Hard truth.

Colonialism isn’t the root, incentive architecture is.

Two interlocking handshakes trap the continent: Internal (ethnic patronage + grievance politics).

External (asymmetric deals + $88B yearly illicit outflows).

Ethiopia never colonized → stayed poor.

Vietnam colonized + war-torn → rising.

Singapore turned colonial port into powerhouse via governance.

Meles built infrastructure.

Deng redesigned incentives.

Energy killer: 1.5B Africans have less power than Germany’s 84M.

We have the resources.

Time to rewrite the code.

Full breakdown + visuals here: https://t.co/UCdynUDIHp

Every system that keeps Africa poor runs on incentives, not tribalism, not colonial wounds, not bad luck.

I have studied these failure patterns for years and I will tell you what nobody in the room wants to say: Africa is not poor because of a deliberate, self-reinforcing extraction architecture that has absorbed every reformer by making them an offer they could not refuse.

I have mapped the two handshakes holding the cage shut, identified all fifteen structural pillars no African leader since 1960 has touched, and traced the exact ten-year vertical window closing in 2035 after which the terms of the next economic era lock permanently.

If you are building in Africa, leading in Africa, or thinking seriously about what sovereignty actually requires, this is the most important brief you will read this year.

Read the full breakdown here:

https://t.co/UCdynUDIHp

I am sincerely excited to see SpaceX open this chapter, the vertical integration across launches, Starlink, and AI compute is unmatched.

Just broke down the S-1 numbers in detail (voting power, Starlink margins, Starship dependency, the full $1.765T math).

Worth a read if you're considering SPCX: https://t.co/zm9cDAsx9j

Congrats to the team on reaching this milestone

Elon Musk will control 82.4% of SpaceX after the IPO. You will control 11.5%.

$135 per share. 555 million shares.

$74.4 billion in net proceeds. $1.765 trillion target valuation.

SpaceX just dropped its S-1 with the SEC and the numbers inside it are unlike anything I've seen from a single filing.

I went through it so you don't have to.

Thread below.🧵👇

1/

SpaceX S-1/A - The Numbers Filed June 3, 2026 | Nasdaq: SPCX

2/

The Offer

$135.00 - IPO price per share

555,555,555 - Class A shares offered

83,333,333 - additional shares if underwriters exercise in full

$75.0B - gross proceeds at base

$74.4B - net proceeds at base

$85.7B - net proceeds if underwriters go full

3/

Voting Structure - straight from the filing

Class A: 1 vote per share

Class B: 10 votes per share

Class A voting power after offering: 11.5% (11.6% if underwriters exercise in full)

Class B voting power after offering: 88.5% (88.4% if underwriters exercise in full)

Elon Musk holds ~82.4% of total voting power post-IPO.

81.1% of that comes from Class B alone.

The public buys 555 million shares and controls 11.5% of the vote.

Elon Musk controls the rest.

Permanently.

By design.

You are buying economic exposure. Not governance. Know what you're buying.

4/

Share Count and Market Cap - the precise math

7,380,196,910 - Class A shares outstanding

5,695,668,265 - Class B shares outstanding

13,075,865,175 - total shares outstanding

5-for-1 - stock split effected May 4, 2026

At $135.00 per share:

$1.765 trillion market cap at base.

$1.776 trillion if underwriters exercise in full.

The $1.75T-$2.0T range you keep seeing is not hype. It is the math from the filing.

5/

What's Actually Inside the Ticker

This is not a rocket company IPO. The filing consolidates three businesses into one:

Space - Falcon, Dragon, Starship

Connectivity - Starlink

AI - Grok, X, COLOSSUS compute

xAI acquired Feb 2, 2026.

X Holdings folded into xAI Mar 28, 2025.

One S-1. Three companies.

6/

Starlink - FY2025

$11.387B - revenue

$4.423B - operating income

38%+ - operating margin

49.8% - year-over-year growth

10.3M - subscribers

164 - countries served

~9,600 - satellites in LEO

Starlink is the cash engine.

This is the business generating real money today.

7/

Total Company - the full picture

$18.674B - consolidated FY2025 revenue

$4.94B - GAAP net loss FY2025

$4.28B - GAAP net loss Q1 2026 alone

22,000+ - full-time employees

80%+ - share of global mass-to-orbit since 2023

99%+ - Falcon mission success rate

Starlink prints cash. The AI buildout burns it faster. The market is pricing the future, not the present.

8/

Valuation Context

$421 - share price at December 2025 tender offer

$800B - implied valuation at that tender

$1.765T - precise market cap at IPO price

~92x - revenue multiple the market is assigning

This is not an aerospace multiple. It is an AI infrastructure multiple.

In six months the implied valuation more than doubled.

The rocket business didn't change. The AI narrative did.

9/

The Underwriter Syndicate

Goldman. Morgan Stanley. BofA. Citi. JPMorgan.

Barclays, Deutsche Bank, RBC, UBS, Wells Fargo.

Allen & Company, Cantor, Needham, Raymond James, SocGen, Stifel, William Blair.

5% of shares reserved for a directed share program - employees and individuals selected at executive discretion.

Every major bank on Wall Street wants a piece of this.

10/

The Starship Dependency

This is the number nobody is talking about.

H2 2026 - Starship first commercial payload to orbit

H2 2026 - V3 Starlink satellites (1 Tbps each) need Starship to launch

2027 - V2 Mobile satellites need Starship

2028 - orbital AI compute satellites need Starship

1 terawatt - Terafab's long-term compute production goal

V3 satellites physically cannot fit in a Falcon 9.

Every premium product. Every next-gen revenue line. All of it runs through one vehicle that has not yet delivered commercial payload to orbit.

11/

Every number above is load-bearing.

The $1.765T valuation is a bet that the 2026-2028 Starship delivery sequence executes on schedule.

If it does, Connectivity and AI reprice upward together.

If it slips, $4.28B quarterly losses with no growth catalyst is a very uncomfortable place to be.

Are you buying SPCX at open?

What's your read on the Starship timeline?

If this cleared things up for you, comment, repost it, quote it, and tag one friend.

12/

This SpaceX IPO is one of the most important moments in AI infrastructure this year.

But if you want to understand why the entire global chip industry is under massive pressure right now, you need to read this immediately👇

Why The Global Chip Industry Just Got Served A $119 Billion Eviction Notice

https://t.co/s1ckBcNVLg

Follow @DrMelchisedecB for more high-signal breakdowns on SpaceX, Starship, AI infrastructure, and the systems moving the world forward.

This is deeper than one man's consistency.

Peter Obi, like every politician in the current arena, is operating inside a broken system that rewards short-term power plays over long-term institution-building. The real conversation Nigerians should be having isn't "who is the bigger hypocrite today," but what kind of leader can actually name the full architecture holding us back and build something that outlasts them.

I laid this out in an open letter to the Nigerian transgenerational leader who hasn't arrived yet.

It's not about defending or attacking any individual.

It's about raising the standard beyond the usual cycle. https://t.co/HQLyibC27h

Nigeria has waited long enough for someone whose life is the argument before their mouth opens.

An Open Letter To The Nigerian Transgenerational Leader Who Has Not Yet Arrived🧵👇

Since 1960, Nigeria has produced politicians, generals, activists, and saints.

It has not yet produced the one thing the historical record says moves a national ceiling.

A leader whose life is the argument before their mouth opens.

This is an open letter to that leader. Wherever you are.

However old you are.

Whatever you are currently doing.

Nigeria is waiting. And the window is not permanently open.

You are not yet in the room.

But the room has been waiting for you longer than Nigeria has been a nation.

We do not know your name.

We do not know your state, your tribe, your religion, or your generation.

We do not know whether you are currently a baby, student, a civil servant, a technocrat, an activist, or a private citizen who has not yet been called.

But we know you exist. Because the historical record is unambiguous: every nation that genuinely moved its developmental ceiling produced, at the intersection of crisis and preparation, a leader whose life was the argument before their mouth opened.

You are that leader.

And Nigeria needs you to understand precisely what that means before you arrive.

The Urgency

Nigeria is not merely behind. It is structurally held.

One hundred and fifty million people live below the poverty line in a country sitting on the largest gas reserves in Africa, the most arable land per capita in West Africa, and the largest youth population on the continent. This is not an accident of geography. It is the compounded result of a transgenerational neocolonial architecture that every Nigerian leader since independence has worked within, complained about, and left entirely intact.

1. Azikiwe inspired a generation and built a nationalism that did not outlive the republic that named him.

2. Awolowo designed the most sophisticated regional development architecture Nigeria has seen and spent his best years locked out of the federal power required to scale it.

3. Aminu Kano built the most radical mass movement for structural redistribution Nigeria has produced, named the feudal and colonial architecture holding Northern Nigeria at chokehold with precision that no subsequent Northern politician has matched, and died without ever holding the executive power required to translate the diagnosis into institutional construction.

4. Murtala arrived with reformist urgency and was assassinated before the institutional foundation could be laid.

5. Babangida named poverty and signed structural adjustment but left the system untouched.

6. Obasanjo named corruption and submitted to IMF prescriptions.

7. Yar'Adua arrived with genuine rule of law instinct and died before the institutional architecture could be tested.

8. Jonathan presided over Nigeria's largest oil revenue windfall and left without a single transgenerational sovereign wealth structure to show for it, while the offshore secrecy infrastructure deepened its penetration of the oil sector on his watch.

9. Buhari named looting and left the offshore architecture untouched.

10. Tinubu is building economic plumbing without yet building the political cage that would prevent a future, less capable leader from breaking the pipes.

Each generation has produced louder rhetoric and deeper structural capture. The cage has not moved. It has been redecorated.

Because the neocolonial architecture predates all of them.

And it has survived all of them.

Time is not neutral.

Every decade without transgenerational institutional construction is a decade the architecture deepens:

1. The debt compounds,

2. The youth population ages without productive absorption, and

3. The window for the developmental state narrows.

The nations that moved their ceilings did so within specific historical windows:

South Korea's window was the 1960s. China's was the 1980s.

Rwanda's was the 2000s.

Nigeria's window is not permanently open. You must arrive, and you must arrive prepared.

What You Must Name

Before you hold any office, before you make any promise, before you ask for any vote, you must be able to name the system that has held Nigeria at chokehold with precision and without flinching:

1. The Bretton Woods institutional architecture that Nigeria inherited without negotiating;

i. The IMF conditionalities,

ii. The World Bank structural adjustment prescriptions,

iii. The dollar-denominated debt terms that make Nigerian fiscal policy hostage to American monetary decisions.

2. The petrodollar architecture that forces every oil-importing nation to acquire dollars first, ensuring Nigeria prices and sells its primary resource in a currency it does not control.

3. The offshore secrecy infrastructure;

I. The British Virgin Islands,

ii. The Cayman Islands,

iii. The Channel Islands-

that the same Western institutions prescribing Nigerian transparency maintain for Nigerian elites to extract and conceal wealth.

4. The bilateral investment treaties that legally foreclose the industrial policy space that Mahathir used in Malaysia and Park used in South Korea before Nigerian policymakers write their first budget.

5. The extractive resource architecture that ensures Nigerian oil and solid mineral wealth is priced, contracted, and repatriated on IOC and commodity trader terms; the architecture Botswana restructured with De Beers and Nigeria has never restructured with anyone.

6. The sovereign credit rating system controlled by three private Western institutions that can raise Nigerian borrowing costs with a single decision made in New York or London.

7. The bilateral investment treaties that legally foreclose the industrial policy space that Mahathir used in Malaysia and Park used in South Korea before Nigerian policymakers write their first budget; giving foreign investors the right to sue the Nigerian state in international arbitration if domestic policy changes affect their profits, including policies designed to build local productive capacity.

8. The extractive resource architecture that ensures Nigerian oil and solid mineral wealth is priced, contracted, and repatriated on terms set by international oil companies and commodity traders rather than the producing state; the architecture Botswana restructured with De Beers and built the Pula Fund around, and Nigeria has never restructured with anyone.

9. The transfer pricing mechanisms that allow multinational corporations operating in Nigeria to declare profits in low-tax jurisdictions while extracting value from Nigerian operations; a gap between what is extracted and what is taxed that is not accidental but engineered through intra-company pricing arrangements that Nigerian tax institutions have historically lacked the technical capacity to audit and challenge.

10. The correspondent banking architecture that requires Nigerian banks to maintain relationships with Western financial institutions to process international dollar transactions; giving those institutions effective veto power over Nigerian dollar flows, and the ability to cut Nigerian institutions off from the global financial system through de-risking decisions made entirely for Western regulatory reasons.

11. The intellectual property regimes embedded in WTO agreements that prevent technology transfer and lock Nigeria into importing rather than producing industrial knowledge; foreclosing the technology transfer requirements that Meles embedded in Ethiopian industrial park agreements and Mahathir embedded in Malaysian manufacturing investment, available to earlier developers but legally constrained for late industrialisers.

12. The agricultural commodity pricing architecture that prices Nigerian agricultural exports - cocoa, sesame, cashew, rubber; on commodity exchanges in London and Chicago that Nigerian producers do not control, ensuring raw material exports leave cheap and processed imports return expensive, with the value addition that would build Nigerian industrial capacity happening outside Nigeria entirely.

13. The currency convertibility conditionalities that subordinate the naira's stability to external capital flow preferences rather than domestic productive capacity; hot money flows entering and exiting Nigerian financial markets that can destabilise the naira independent of Nigerian monetary policy decisions, giving external capital structural leverage over domestic economic conditions.

14. The aid and development financing architecture that makes donor legibility more important than domestic accountability; where Nigerian institutions are designed to satisfy World Bank reporting requirements and USAID programme metrics rather than Nigerian legislative oversight, producing a bureaucratic culture oriented toward external validation rather than internal performance.

15. The security assistance architecture that makes Nigerian military and intelligence institutions dependent on Western training, equipment, doctrine, and therefore strategic orientation; creating institutional dependencies that constrain Nigerian foreign policy and security decision-making, ensuring that a state which cannot independently equip, train, and orient its security institutions cannot exercise full sovereign decision-making on the questions those institutions are designed to answer.

The cage is not one bar. It is numerous interlocking pillars, each designed to survive the collapse of the system that built it; as Bretton Woods itself demonstrated in 1971.

And no candidate currently in the Nigerian political field has named all of them, refused their personal benefits, and begun building the transgenerational institutional alternative simultaneously.

That is not pessimism. That is the precise diagnosis of where Nigeria stands.

These are just few of them, they are numerous and interlocking.

Name all of it.

Name it in public.

Name it before you have power, not after. Because a leader who cannot name the cage before entering it will negotiate with it once inside.

What You Must Refuse

1. Your personal record must not contradict your public argument.

This is not optional. It is the threshold.

2. You cannot hold offshore structures in the jurisdictions you name as instruments of extraction.

3. You cannot use nominee directors to obscure beneficial ownership while campaigning on transparency.

4. You cannot accept the personal benefits of the architecture you publicly condemn and expect the institutional alternative you build to survive your departure.

Kagame enforced anti-corruption standards that did not exempt the politically connected.

Khama converted Botswana's diamond wealth into the Pula Fund rather than personal accumulation.

Deng stepped back from positions of formal power and designed succession into the structure.

Their personal records did not contradict their institutional arguments.

Yours must not either.

The electorate will eventually audit the gap between what you name and how you live. The architecture will exploit that gap before they do.

Close it before you arrive.

What You Must Build

Naming is not enough.

Refusal is not enough.

The third obligation is construction, and it is the most demanding of the three because it is transgenerational, unglamorous, and its beneficiaries will not vote for you.

1. You must build a Nigerian Development Authority with a statutory mandate, independent funding, and enforcement capacity insulated from electoral turnover; a single institutional entry point for investment that strips the transaction cost architecture external capital uses to capture Nigerian regulatory environments.

2. You must build a Nigerian Economics and Industrial Policy Profession capable of arguing with the IMF on its own technical terrain, designing trade policy that protects infant industries without permanently shielding them from competition, and producing the next generation of technocrats before the current generation exits.

3. You must restructure Nigeria's extractive resource contracts; oil, gas, solid minerals, to embed technology transfer requirements, local content mandates with enforcement teeth, and sovereign wealth architecture that converts resource revenue into productive capital rather than recurrent expenditure.

4. You must embed your reforms in independent institutional architecture before your personal authority becomes the only thing holding them in place.

NELFUND must have its own funding stream that survives the next president.

LGA autonomy must be constitutionally insulated from the next attorney general. Every structural reform you build must be designed to outlast your departure, because the reforms that moved ceilings elsewhere survived their builders. The reforms that merely decorated ceilings did not.

5. You must build the technocratic pipeline!; the universities, the research institutions, the civil service training architecture, that produces the bureaucratic capacity to implement what you design.

Meles built an Ethiopian economics profession.

Mahathir built Malaysian engineering and manufacturing capacity.

You must build Nigerian institutional memory that does not reset with every electoral cycle.

And you must do all of this knowing that you may not be the immediate beneficiary of the structure that liberates.

Park did not live to see South Korea's democracy.

Khama did not live to see Botswana's full institutional maturity.

Meles did not live to see Ethiopia's industrial ambitions fully realised.

The transgenerational leader builds for the generation after the one that elects him. That is the definition of the work.

To the Electorate Reading This

When this leader appears, you will be tempted to dismiss them.

1. They will not promise immediate comfort. 2. They will name enemies that are structural rather than personal.

3. They will build institutions that feel abstract rather than deliver cash that feels immediate.

4. They will refuse personal benefits in ways that will be called foolish by those who have normalised accumulation.

Do not dismiss them.

Recognise them by their life before their words.

Recognise them by what they name before they have power.

Recognise them by what they refuse when refusal is costly.

Recognise them by what they build that they will not live to benefit from.

The saint exhausts the reform energy of a generation without threatening a single bar. The machine aggregates without building. The perennial repositions without constructing.

The militant confronts without the institutional foundation the confrontation requires.

The builder is different from all four.

And Nigeria has been waiting for the transgenerational builder since 1960.

To the Current Political Class Reading This

The standard has been named.

The historical record is unambiguous.

The threshold is specific and measurable. You know whether your record meets it.

You know whether your personal financial architecture contradicts your public argument.

You know whether what you have built will outlast your departure.

The analysis is not prosecution. It is education.

And education addressed to those with power carries one obligation: act on it, or make way for those who will.

Paul Kagame of Rwanda is doing it.

Deng Xiaoping of China has done it.

Meles Zenawi of Ethiopia has done it.

Mahathir Mohamad of Malaysia has done it.

Seretse Khama of Botswana has done it.

Park Chung-hee of South Korea has done it.

Why not Nigeria?

The cage has numerous bars. But cages have also been dismantled. By tragenerational leaders whose lives were the argument before their mouths opened.

By leaders who named the bars precisely, refused their personal comfort, and built the door.

Nigeria is waiting for that leader.

And that leader must now begin to prepare.

Yes, I concur. Space isn’t a finite resource, it’s the ultimate infinite game.

The real unlock is building the infrastructure to get there at scale.

Just dropped a full breakdown of SpaceX’s S-1 that shows how this plays out in practice: Starship as the enabler for the next wave of connectivity + orbital AI compute, all feeding into Kardashev-style expansion. Worth a read if you’re thinking about the actual mechanics: https://t.co/zm9cDAsx9j

I am very excited to see how fast we can push the frontier.

Elon Musk will control 82.4% of SpaceX after the IPO. You will control 11.5%.

$135 per share. 555 million shares.

$74.4 billion in net proceeds. $1.765 trillion target valuation.

SpaceX just dropped its S-1 with the SEC and the numbers inside it are unlike anything I've seen from a single filing.

I went through it so you don't have to.

Thread below.🧵👇

1/

SpaceX S-1/A - The Numbers Filed June 3, 2026 | Nasdaq: SPCX

2/

The Offer

$135.00 - IPO price per share

555,555,555 - Class A shares offered

83,333,333 - additional shares if underwriters exercise in full

$75.0B - gross proceeds at base

$74.4B - net proceeds at base

$85.7B - net proceeds if underwriters go full

3/

Voting Structure - straight from the filing

Class A: 1 vote per share

Class B: 10 votes per share

Class A voting power after offering: 11.5% (11.6% if underwriters exercise in full)

Class B voting power after offering: 88.5% (88.4% if underwriters exercise in full)

Elon Musk holds ~82.4% of total voting power post-IPO.

81.1% of that comes from Class B alone.

The public buys 555 million shares and controls 11.5% of the vote.

Elon Musk controls the rest.

Permanently.

By design.

You are buying economic exposure. Not governance. Know what you're buying.

4/

Share Count and Market Cap - the precise math

7,380,196,910 - Class A shares outstanding

5,695,668,265 - Class B shares outstanding

13,075,865,175 - total shares outstanding

5-for-1 - stock split effected May 4, 2026

At $135.00 per share:

$1.765 trillion market cap at base.

$1.776 trillion if underwriters exercise in full.

The $1.75T-$2.0T range you keep seeing is not hype. It is the math from the filing.

5/

What's Actually Inside the Ticker

This is not a rocket company IPO. The filing consolidates three businesses into one:

Space - Falcon, Dragon, Starship

Connectivity - Starlink

AI - Grok, X, COLOSSUS compute

xAI acquired Feb 2, 2026.

X Holdings folded into xAI Mar 28, 2025.

One S-1. Three companies.

6/

Starlink - FY2025

$11.387B - revenue

$4.423B - operating income

38%+ - operating margin

49.8% - year-over-year growth

10.3M - subscribers

164 - countries served

~9,600 - satellites in LEO

Starlink is the cash engine.

This is the business generating real money today.

7/

Total Company - the full picture

$18.674B - consolidated FY2025 revenue

$4.94B - GAAP net loss FY2025

$4.28B - GAAP net loss Q1 2026 alone

22,000+ - full-time employees

80%+ - share of global mass-to-orbit since 2023

99%+ - Falcon mission success rate

Starlink prints cash. The AI buildout burns it faster. The market is pricing the future, not the present.

8/

Valuation Context

$421 - share price at December 2025 tender offer

$800B - implied valuation at that tender

$1.765T - precise market cap at IPO price

~92x - revenue multiple the market is assigning

This is not an aerospace multiple. It is an AI infrastructure multiple.

In six months the implied valuation more than doubled.

The rocket business didn't change. The AI narrative did.

9/

The Underwriter Syndicate

Goldman. Morgan Stanley. BofA. Citi. JPMorgan.

Barclays, Deutsche Bank, RBC, UBS, Wells Fargo.

Allen & Company, Cantor, Needham, Raymond James, SocGen, Stifel, William Blair.

5% of shares reserved for a directed share program - employees and individuals selected at executive discretion.

Every major bank on Wall Street wants a piece of this.

10/

The Starship Dependency

This is the number nobody is talking about.

H2 2026 - Starship first commercial payload to orbit

H2 2026 - V3 Starlink satellites (1 Tbps each) need Starship to launch

2027 - V2 Mobile satellites need Starship

2028 - orbital AI compute satellites need Starship

1 terawatt - Terafab's long-term compute production goal

V3 satellites physically cannot fit in a Falcon 9.

Every premium product. Every next-gen revenue line. All of it runs through one vehicle that has not yet delivered commercial payload to orbit.

11/

Every number above is load-bearing.

The $1.765T valuation is a bet that the 2026-2028 Starship delivery sequence executes on schedule.

If it does, Connectivity and AI reprice upward together.

If it slips, $4.28B quarterly losses with no growth catalyst is a very uncomfortable place to be.

Are you buying SPCX at open?

What's your read on the Starship timeline?

If this cleared things up for you, comment, repost it, quote it, and tag one friend.

12/

This SpaceX IPO is one of the most important moments in AI infrastructure this year.

But if you want to understand why the entire global chip industry is under massive pressure right now, you need to read this immediately👇

Why The Global Chip Industry Just Got Served A $119 Billion Eviction Notice

https://t.co/s1ckBcNVLg

Follow @DrMelchisedecB for more high-signal breakdowns on SpaceX, Starship, AI infrastructure, and the systems moving the world forward.

Great timing with the SoFi update, Sawyer.

For anyone submitting interest, a quick break down of the full S-1 numbers:

Elon’s post-IPO voting control (82.4%), the $1.765T valuation math, Starlink’s cash engine vs. the AI burn rate, and why Starship timeline is the real make-or-break factor.

Thread here if you want the details straight from the filing:

https://t.co/zm9cDAsx9j

Elon Musk will control 82.4% of SpaceX after the IPO. You will control 11.5%.

$135 per share. 555 million shares.

$74.4 billion in net proceeds. $1.765 trillion target valuation.

SpaceX just dropped its S-1 with the SEC and the numbers inside it are unlike anything I've seen from a single filing.

I went through it so you don't have to.

Thread below.🧵👇

1/

SpaceX S-1/A - The Numbers Filed June 3, 2026 | Nasdaq: SPCX

2/

The Offer

$135.00 - IPO price per share

555,555,555 - Class A shares offered

83,333,333 - additional shares if underwriters exercise in full

$75.0B - gross proceeds at base

$74.4B - net proceeds at base

$85.7B - net proceeds if underwriters go full

3/

Voting Structure - straight from the filing

Class A: 1 vote per share

Class B: 10 votes per share

Class A voting power after offering: 11.5% (11.6% if underwriters exercise in full)

Class B voting power after offering: 88.5% (88.4% if underwriters exercise in full)

Elon Musk holds ~82.4% of total voting power post-IPO.

81.1% of that comes from Class B alone.

The public buys 555 million shares and controls 11.5% of the vote.

Elon Musk controls the rest.

Permanently.

By design.

You are buying economic exposure. Not governance. Know what you're buying.

4/

Share Count and Market Cap - the precise math

7,380,196,910 - Class A shares outstanding

5,695,668,265 - Class B shares outstanding

13,075,865,175 - total shares outstanding

5-for-1 - stock split effected May 4, 2026

At $135.00 per share:

$1.765 trillion market cap at base.

$1.776 trillion if underwriters exercise in full.

The $1.75T-$2.0T range you keep seeing is not hype. It is the math from the filing.

5/

What's Actually Inside the Ticker

This is not a rocket company IPO. The filing consolidates three businesses into one:

Space - Falcon, Dragon, Starship

Connectivity - Starlink

AI - Grok, X, COLOSSUS compute

xAI acquired Feb 2, 2026.

X Holdings folded into xAI Mar 28, 2025.

One S-1. Three companies.

6/

Starlink - FY2025

$11.387B - revenue

$4.423B - operating income

38%+ - operating margin

49.8% - year-over-year growth

10.3M - subscribers

164 - countries served

~9,600 - satellites in LEO

Starlink is the cash engine.

This is the business generating real money today.

7/

Total Company - the full picture

$18.674B - consolidated FY2025 revenue

$4.94B - GAAP net loss FY2025

$4.28B - GAAP net loss Q1 2026 alone

22,000+ - full-time employees

80%+ - share of global mass-to-orbit since 2023

99%+ - Falcon mission success rate

Starlink prints cash. The AI buildout burns it faster. The market is pricing the future, not the present.

8/

Valuation Context

$421 - share price at December 2025 tender offer

$800B - implied valuation at that tender

$1.765T - precise market cap at IPO price

~92x - revenue multiple the market is assigning

This is not an aerospace multiple. It is an AI infrastructure multiple.

In six months the implied valuation more than doubled.

The rocket business didn't change. The AI narrative did.

9/

The Underwriter Syndicate

Goldman. Morgan Stanley. BofA. Citi. JPMorgan.

Barclays, Deutsche Bank, RBC, UBS, Wells Fargo.

Allen & Company, Cantor, Needham, Raymond James, SocGen, Stifel, William Blair.

5% of shares reserved for a directed share program - employees and individuals selected at executive discretion.

Every major bank on Wall Street wants a piece of this.

10/

The Starship Dependency

This is the number nobody is talking about.

H2 2026 - Starship first commercial payload to orbit

H2 2026 - V3 Starlink satellites (1 Tbps each) need Starship to launch

2027 - V2 Mobile satellites need Starship

2028 - orbital AI compute satellites need Starship

1 terawatt - Terafab's long-term compute production goal

V3 satellites physically cannot fit in a Falcon 9.

Every premium product. Every next-gen revenue line. All of it runs through one vehicle that has not yet delivered commercial payload to orbit.

11/

Every number above is load-bearing.

The $1.765T valuation is a bet that the 2026-2028 Starship delivery sequence executes on schedule.

If it does, Connectivity and AI reprice upward together.

If it slips, $4.28B quarterly losses with no growth catalyst is a very uncomfortable place to be.

Are you buying SPCX at open?

What's your read on the Starship timeline?

If this cleared things up for you, comment, repost it, quote it, and tag one friend.

12/

This SpaceX IPO is one of the most important moments in AI infrastructure this year.

But if you want to understand why the entire global chip industry is under massive pressure right now, you need to read this immediately👇

Why The Global Chip Industry Just Got Served A $119 Billion Eviction Notice

https://t.co/s1ckBcNVLg

Follow @DrMelchisedecB for more high-signal breakdowns on SpaceX, Starship, AI infrastructure, and the systems moving the world forward.

This is massive Grok Imagine Video 1.5 hitting #1 on the leaderboard right out the gate shows how fast xAI is moving.

On a related note, I just went through the full SpaceX S-1 filing that just dropped ties everything together, Starlink cash flow funding the AI buildout, Colossus, and the full stack.

If you're following the story, here's the full breakdown:

https://t.co/zm9cDAsx9j

Exciting times.

Elon Musk will control 82.4% of SpaceX after the IPO. You will control 11.5%.

$135 per share. 555 million shares.

$74.4 billion in net proceeds. $1.765 trillion target valuation.

SpaceX just dropped its S-1 with the SEC and the numbers inside it are unlike anything I've seen from a single filing.

I went through it so you don't have to.

Thread below.🧵👇

1/

SpaceX S-1/A - The Numbers Filed June 3, 2026 | Nasdaq: SPCX

2/

The Offer

$135.00 - IPO price per share

555,555,555 - Class A shares offered

83,333,333 - additional shares if underwriters exercise in full

$75.0B - gross proceeds at base

$74.4B - net proceeds at base

$85.7B - net proceeds if underwriters go full

3/

Voting Structure - straight from the filing

Class A: 1 vote per share

Class B: 10 votes per share

Class A voting power after offering: 11.5% (11.6% if underwriters exercise in full)

Class B voting power after offering: 88.5% (88.4% if underwriters exercise in full)

Elon Musk holds ~82.4% of total voting power post-IPO.

81.1% of that comes from Class B alone.

The public buys 555 million shares and controls 11.5% of the vote.

Elon Musk controls the rest.

Permanently.

By design.

You are buying economic exposure. Not governance. Know what you're buying.

4/

Share Count and Market Cap - the precise math

7,380,196,910 - Class A shares outstanding

5,695,668,265 - Class B shares outstanding

13,075,865,175 - total shares outstanding

5-for-1 - stock split effected May 4, 2026

At $135.00 per share:

$1.765 trillion market cap at base.

$1.776 trillion if underwriters exercise in full.

The $1.75T-$2.0T range you keep seeing is not hype. It is the math from the filing.

5/

What's Actually Inside the Ticker

This is not a rocket company IPO. The filing consolidates three businesses into one:

Space - Falcon, Dragon, Starship

Connectivity - Starlink

AI - Grok, X, COLOSSUS compute

xAI acquired Feb 2, 2026.

X Holdings folded into xAI Mar 28, 2025.

One S-1. Three companies.

6/

Starlink - FY2025

$11.387B - revenue

$4.423B - operating income

38%+ - operating margin

49.8% - year-over-year growth

10.3M - subscribers

164 - countries served

~9,600 - satellites in LEO

Starlink is the cash engine.

This is the business generating real money today.

7/

Total Company - the full picture

$18.674B - consolidated FY2025 revenue

$4.94B - GAAP net loss FY2025

$4.28B - GAAP net loss Q1 2026 alone

22,000+ - full-time employees

80%+ - share of global mass-to-orbit since 2023

99%+ - Falcon mission success rate

Starlink prints cash. The AI buildout burns it faster. The market is pricing the future, not the present.

8/

Valuation Context

$421 - share price at December 2025 tender offer

$800B - implied valuation at that tender

$1.765T - precise market cap at IPO price

~92x - revenue multiple the market is assigning

This is not an aerospace multiple. It is an AI infrastructure multiple.

In six months the implied valuation more than doubled.

The rocket business didn't change. The AI narrative did.

9/

The Underwriter Syndicate

Goldman. Morgan Stanley. BofA. Citi. JPMorgan.

Barclays, Deutsche Bank, RBC, UBS, Wells Fargo.

Allen & Company, Cantor, Needham, Raymond James, SocGen, Stifel, William Blair.

5% of shares reserved for a directed share program - employees and individuals selected at executive discretion.

Every major bank on Wall Street wants a piece of this.

10/

The Starship Dependency

This is the number nobody is talking about.

H2 2026 - Starship first commercial payload to orbit

H2 2026 - V3 Starlink satellites (1 Tbps each) need Starship to launch

2027 - V2 Mobile satellites need Starship

2028 - orbital AI compute satellites need Starship

1 terawatt - Terafab's long-term compute production goal

V3 satellites physically cannot fit in a Falcon 9.

Every premium product. Every next-gen revenue line. All of it runs through one vehicle that has not yet delivered commercial payload to orbit.

11/

Every number above is load-bearing.

The $1.765T valuation is a bet that the 2026-2028 Starship delivery sequence executes on schedule.

If it does, Connectivity and AI reprice upward together.

If it slips, $4.28B quarterly losses with no growth catalyst is a very uncomfortable place to be.

Are you buying SPCX at open?

What's your read on the Starship timeline?

If this cleared things up for you, comment, repost it, quote it, and tag one friend.

12/

This SpaceX IPO is one of the most important moments in AI infrastructure this year.

But if you want to understand why the entire global chip industry is under massive pressure right now, you need to read this immediately👇

Why The Global Chip Industry Just Got Served A $119 Billion Eviction Notice

https://t.co/s1ckBcNVLg

Follow @DrMelchisedecB for more high-signal breakdowns on SpaceX, Starship, AI infrastructure, and the systems moving the world forward.

![DrMelchisedecB's tweet photo. New X Algorithm: What X Didn’t Tell You (And What Actually Works in 2026) 🧵👇

While everyone else is guessing, I’ve spent the last 72 hours reading the entire X Algorithm code line by line since May 15, 2026.

No guru opinions. No speculation. Just the actual code.

Here’s exactly what stopped working after the May 15 Phoenix update, what’s winning right now, and what will still work months from now:

What DIED (according to the code):

1. Spamming 4+ posts a day:

The algorithm punishes you hard with *Author Diversity Decay*. Your 2nd, 3rd, and 4th posts get exponentially weaker reach in the same user’s feed.

2. Low-effort reply farming:

Generic replies (“🔥”, “Great point”, emoji spam) get buried. Grok literally reads and ranks replies now.

3. Pure text-only posts:

They work… but text + image or video (≥10 seconds) consistently outperforms them because of extra visual + dwell signals.

4. AI slop & recycled templates:

There’s an explicit `slop_score` + quality classifier. Low-originality content gets flagged fast.

5. Cheap engagement bait:

“What do you think?” or “Tag someone who needs this” increases scroll-past rate → active penalty via `not_dwelled` signal.

What’s WINNING (and will keep winning):

1. Original, unique takes from small accounts:

Original posts get full Grok evaluation + better out-of-network discovery.

2. Text + Media combos (especially video ≥10s with audio):

Hybrid format maximizes multiple positive signals at once.

3. Contrarian opinions backed by real proof:

Numbers, screenshots, personal results → higher dwell time, more replies & quotes.

4. Early, high-quality replies to big accounts (first 10-30 minutes):

One of the strongest growth levers for small accounts right now.

5. Real conversation > likes:

Quality replies + replying to your own comments in the first 30 minutes is pure ranking gold.

My Day-One Test Results (Real Data):

Reply 1 (contrarian + technical angle, +9 min after Elon’s post):

→ 214 impressions • 43 engagements • 39 detail expands • 2 profile visits.

👉[Link: https://t.co/OzScqzNbG7]

Reply 2 (thoughtful transparency take + direct question to Elon):

→ 45 impressions • 8 engagements • 0 profile visits

👉[Link: https://t.co/JMr7nZveCt]

No viral explosion. Just clean data.

The real question isn’t whether 214 or 45 impressions is a failure. It’s whether you’re willing to treat it as data.

Most people won’t.

The ones who do are the ones who win.

The Evergreen Playbook (Use This Today & Months From Now):

- Cut volume to 1–2 high-quality posts per day max.

- Always pair text with image, carousel, or short video.

- Reply to every real comment in the first 30 minutes.

- Lead with first-person stories + concrete proof.

- One bold, specific opinion per post.

- Focus on dwell time and real replies, not just likes.

The Honest Question:

Does this algorithm truly favor small accounts, or does it quietly give bigger accounts an unbeatable head start?

It feels like a meritocracy with momentum, the rich get richer, but original, high-signal content from smaller accounts can still break through.

I’m testing it publicly and aggressively for the next 30 days.

If you want the full 72-hour technical breakdown (with every file reference, exact constants, codes, tables, and the hidden parts X didn’t publish), just say it in the comments below and I’ll post it in as reply to your comments.

Save this post.

The algorithm might change again in few months, but these principles won’t.

I hope you've found this post helpful.

Comment. Repost. Bookmark.

Follow me @DrMelchisedecB for more...

What’s your first move after reading this?

Drop it below 👇](https://pbs.twimg.com/media/HIqsWpYXwAEEMzu.jpg)