I'm Boris and I created Claude Code. I wanted to quickly share a few tips for using Claude Code, sourced directly from the Claude Code team. The way the team uses Claude is different than how I use it. Remember: there is no one right way to use Claude Code -- everyones' setup is different. You should experiment to see what works for you!

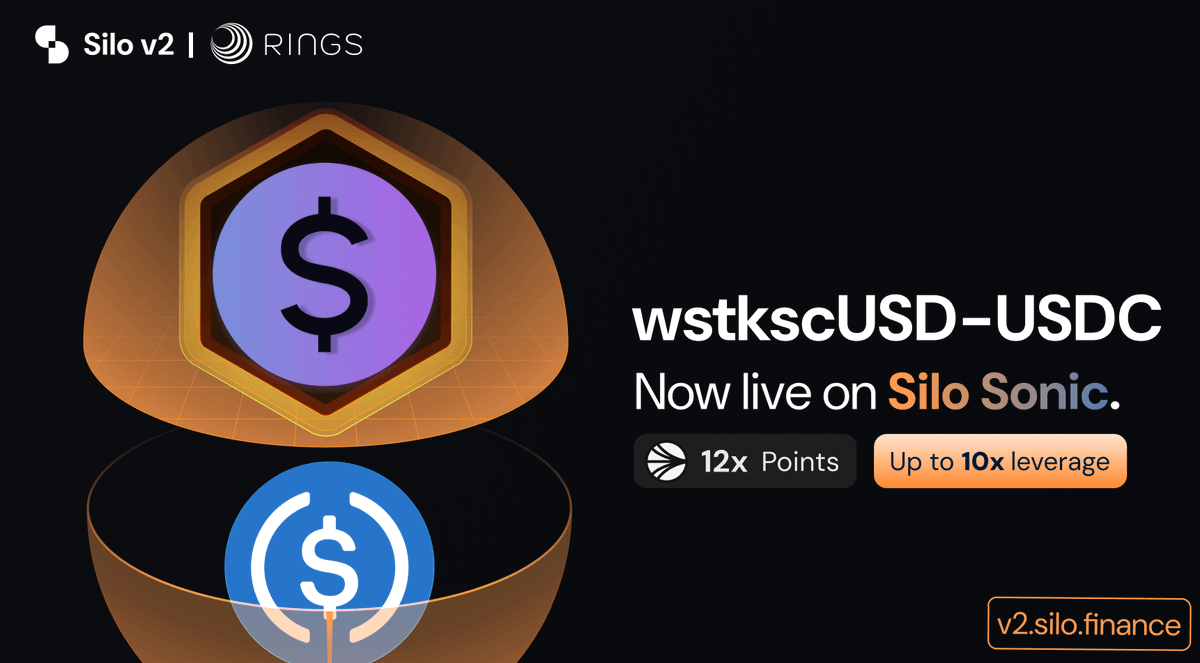

The market that everyone has been waiting for is finally here and you've got two options:

1⃣ Loop wstkscUSD for leveraged yield and up to 120x Sonic Points

2⃣ Deposit USDC to earn interest and 10x Sonic Points

There's no wrong choice.

👇

99% of people use DEX Screener the wrong way.

Only a few degens know about its hidden features and even fewer use them to find 100x gems.

I've scanned 8000 lines of its source code and sharing all the secrets for FREE👇🧵

🚨Off The Grid Event is Live🚨

The SUPER SAIYANS have been called into action!

৹ Head to our site NOW & claim an entry code

৹ Play TECHNOCORE to earn EXCLUSIVE @playoffthegrid NFT gear for SUPER holders

৹ Climb the SV Leaderboard to compete for @GUNbyGUNZ Validators

🧵👇

1/2

TIPS CÀY AIRDROP AEVO HIỆU QUẢ CHO NGƯỜI VỐN THẤP

1/ Aevo là ông lớn trong mảng DeFi Derivatives có sản phẩm tốt

2/ Aevo - Lột xác từ Ribbon Finance

3/ Cơ hội airdrop AEVO trong tương lai

4/ Vốn ít có cơ hội cày airdrop Aevo không?

5/ Hướng dẫn cày airdrop Aevo (Cơ bản)

6/ Nên bao nhiêu ví? Volume bao nhiêu? Vốn bao nhiêu?

7/ Ước tính số tiền AEVO airdrop

Nếu threads chất lượng, mong nhận được ❤️ và 🔁 của c��c b��n 😍

6/ Nên bao nhiêu ví? Volume bao nhiêu? Vốn bao nhiêu?

Như các bạn thấy phía trên ở ví số 4, mình cày $71,000 volume thực nhưng được boost đến 19 lần nên volume boosted tới $1.4 triệu USD.

Và để làm được điều này, mình phải có chiến lược cụ thể ban đầu:

- Cày bao nhiêu ví?

- Phân bổ vốn giữa các ví?

- Mỗi lệnh trade bao nhiêu?

- Nên trade cặp nào?

Nếu không có chiến lược cụ thể, bạn có thể bị đốt nhiều tiền như mình trong thời gian đầu mà volume boost không được cao.

---

Riêng phần hướng dẫn này, mình xin phép gửi riêng cho các bạn với điều kiện rất đơn giản

Bước 1: Đăng ký tài khoản Aevo theo link dưới đây

https://t.co/fC1C3yY2eM

Bước 2: Retweet bài viết này

https://t.co/imrnKESkxJ

Bước 3: Tham gia Facebook Group của Coin98 Insights

https://t.co/A1vRTnBeLU

Bước 4: Copy username của tài khoản Aevo và inbox mình qua Twitter, mình sẽ gửi hướng dẫn cách cày airdrop mình đã thực hiện thành công.

Economics isn't a zero-sum game, but power is.

Crypto is a disintermediation of state control of financial infrastructure. Separating money and state. This is a big deal.

DeFi will be attacked. It's going to get worse.

But our victory is inevitable. The Vietnam Thesis 🧵

Speed Running Financial History, Lessons from TradFi for DeFi

Part 1: Governance Tokens, Tech Stocks, Dividends, and "Utility"

DeFi needs more awareness of our TradFi parallels. Namely how our problems, discoveries, life cycles, etc. are not new. The point of this series is to predict the future and clarify the present, by looking to the past. We are not reinventing human behavior or financial axioms. We are creating superior environments for them to take place.

YOUR EQUITY IS NOT EQUITY

Governance tokens… perhaps not as valueless as we’ve been led to believe. And stock "equity" isn't exactly what it's sold as, either. Let’s observe how TradFi views them, functionally and literally.

There’s hyperfocus on DeFi projects’ revenue distribution, which means you receive fee share when you own the project’s token; it’s tantamount to a dividend (idk why DeFi rebranded the term "dividend" to "rev share", maybe because it feels more community inclusive). Is this necessary for the token to accrue value? Does it give it “utility”? What do we even mean when we say that?

When you break down the “equity” platitudes and get down to concrete situations, you’re being hypocritical if you deride governance tokens but would own Nvidia, Google, TSLA, Cloudflare, or any tech stock with no dividend. What does your “equity” mean here?

I’ve taken CFA tests, I know the official theory. What I’m interested in is situational reality; what do you actually get at the end of the day with these tech stocks? Because when I break it all down, it isn't a claim on cashflows or company assets. So what is this “equity” you speak of?

Last I saw figures on it, about 50-70% of stocks pay a dividend, and the most richly valued ones (tech and high-growth stocks) rarely do. I believe less than half of the NASDAQ pays dividends (if someone has Bloomberg and wants to get exact numbers that'd be great). No cash will ever be returned to you from many of these. So why own them? Where is their “fee switch”? Because that’s how something accrues value right? Well, tech stocks do not do that. And yet, they’re very valuable.

It's odd how we describe dividends as "utility" in DeFi, but no one says a tech stock has/doesn't have utility based on if it pays dividends.

BANKRUPTCY AND BOOK VALUE

The value for the stock must come from the equity claim on company assets then...?

Nope! Especially if they're tech companies. Most tech company assets are intangibles. What are intangibles: things like IP, goodwill, the spoils from research and development, etc.. They're the brand and service they've built via investing through the income statement, not the balance sheet.

Here’s an infographic on how tangible assets for US companies has been declining, broken down in 10-year chunks. As you can see, it's mostly intangibles now.

This means there's no factory for you to lay claim to in bankruptcy (a factory or equipment would be examples of tangible assets). No hard assets to be sold off to make you whole. You have no “equity” in anything concrete here. The investments these tech companies make are often in things that seem periphery like customer support and advertising, but are critical capital assets of the tech world.

These squishy tech assets are very valuable... to the company. But they have little salvage value in liquidation. What is MongoDB going to do, sell its advertising investment and goodwill in bankruptcy?

Common stock is a junior claim on assets if the company fails. You get the leftovers after bond holders and preferred shareholders are repaid. And you sure as hell aren't investing in a tech company, or any company, hoping you get scraps in bankruptcy. That means the company failed and the share price was decimated.

And you're not going to get anything anyways, because the tech company has little salvage value for its assets because they're all intangibles. What is your "equity" equity in??

So what are you getting when you buy NET?

- no cashflows

- nothing in bankruptcy

- voting rights!

When you buy NVDA, CFLT, SNOW, etc. all you get is to vote in shareholder meetings. Neat! Wait, what's a governance token again?

No cash is returned to you from tech stocks. And you don’t buy them hoping for that anyways, you want 100x, not a 4% yield. You can't have both at the same time. Life doesn't work that way, that's called "having your cake and eating it too".

You buy these things for huge capital gains, not a bond yield. Companies who start paying dividends only do so because they can't reinvest all the profits back into the business. Paying a dividend means your growth is slowing. The history of this will be covered in detail in Part 2.

The financial laws of physics dictate the valuation of equities follows some DCF iron rule that says they go up in price as revenues, cashflows, margins, etc. increases. For many stocks, you will never touch that revenue. You will never exercise any claim on the company’s assets. What, exactly, is your “equity” giving you equity in?

If that tech company fails, the stock is a zero. And there are no assets to be sold off to make you whole. In essence, you own a governance token with no cashflows, and by the grace of god its valuation is tied to company performance. Tech stocks and governance tokens, mostly a distinction without a difference.

STOCKS CAN'T RUG AS EASILY?

I’ve heard some say legal protections make stocks safer, and from a “rugging the business” standpoint, that’s true. However this is value-accrual analysis, not a legal-protections one.

Why does the treasury of Cloudflare make NET more valuable when you will never touch one penny of it? Ok so @eastdakota can’t just steal the corporate bank account because of laws, yes. But that doesn't refute how you'll never get anything valuable returned to you from owning NET.

ON SHARE BUYBACKS

Some important points on share buybacks vs dividends: they're technically the same thing if you're taking a CFA test. I understand the accounting logic and the tax-advantaged approach. But it doesn't change the central point being made here.

You're still not getting any income stream with buybacks, and you still have no functional claim on company assets.

How do you acquire actual dollars out of your stock, post-buyback? You have to sell those shares to get anything. You receive absolutely nothing by virtue of owning them besides… voting rights.

But there are less of them now because of the buyback, so just less of something makes it magically more valuable? Why the hell was it valuable to begin with though?

This artificial-scarcity act pleases the DCF gods that say your stock price should go up now by virtue of there being less of them. But you still have a governance token. A share that only lets you vote on things, has no profits returned to you, and has no real claim on any resources.

Buyback or no buyback, you can still just vote with your stock and hope number goes up as the company does well. And as the company grows and its margins improve, that’s exactly what happens!

Empirically, this is the case whether or not cash is ever returned to you. Fee switch or no fee switch. Dividend or no dividend. Why? I don't know. But it just does.

To be clear, I’m not smearing tech stocks; I’m using them as demonstrable evidence that governance tokens are in fact valuable. I own them myself (long NET and NVDA, in fact). Be aware of what you own, and don't be hypocritical bashing one thing but not the other when they're functionally the same.

Footnote: I’m aware NVDA pays like a 0.03% dividend, which is useless. As a shareholder I'd rather the money be in Jensen's hands than mine, where it's far more valuable. Nobody owns Nvidia for the dividend.

Sub to blog so we can discuss more stuff together (remove 7s):

backthebunny.subs77tack.77com/p/on-governance-tokens-and-tech-stocks

Speed Running Financial History, Lessons from TradFi for DeFi

Part 2: Why Did Investors Stop Demanding Dividends?

1600s-1900s: What Does the Stock Do?

2020s: What Does the Token Do?

DeFi needs more awareness of our TradFi parallels. Many of our problems, discoveries, life cycles, etc. are not new. The point of this series is to predict the future and clarify the present, by looking to the past. Crypto is not reinventing human behavior or financial axioms. We’re creating superior environments for them to take place.

Remember, DeFi users aren’t some new breed of enlightened human. We’re not changing the state of man with atomic swaps and L2s. We’re seeing the same greed, fraud, leverage, innovation, and hard lessons of our financial ancestors.

That’s what happens when a lot of value is being created in a permissionless, open system: it attracts all types, good and bad. “Speed running financial history” means we can glean historical wisdom from lessons that have already been learned. We would be wise to learn from them.

An instance of said speedrunning that’s happening right now: fee sharing. AKA staking. AKA “utility”. AKA “if the token doesn’t have yield, what does it do?”

TradFi has a name for this, it’s called dividends. Back in the day, they didn’t care much for abstract notions of equity in the business, they wanted cold hard cash for holding your stock. Right now, DeFi is of a similar mindset. Parallels.

1600s-1900s: “If it doesn’t pay dividends, what does the stock do?”

2020s: “If it doesn’t let you stake for yield, what does the token do?”

We’re doing the speedrunning financial history thing again. Flat circle.

Let’s review historical examples of what TradFi already experienced, and what DeFi will eventually make peace with.

Before diving in, I want to emphasize the first part of this series: Governance Tokens, Tech Stocks, Dividends, and "Utility” (QT’d). It goes into very literal detail that shows deconstructing a stock that pays no dividends and has no book value… is just a governance token. This is important to internalize. If that feels viscerally wrong to you, read Part 1. Unless you’ve amassed enough stock to launch a hostile takeover, your equity is not equity.

-- STOCKS 1.0: WHY WERE THEY OFFERED IN THE FIRST PLACE? --

Our TradFi ancestors shared many of the sentiments and feelings DeFi presently does, and at one point stocks with no dividends were unacceptable! They used to demand ‘real yield’ (a cut of earnings), because what else does the stock do!? TradFi’ers once saw stocks from this lens, and yet now only 50% of the Nasdaq pays a dividend… how did we get here?

The instinct to tie the value of an abstract, intangible asset to something recurring and concrete is logical. There are a lot of scams out there, and proof of profitability via payouts is a solid heuristic for avoiding them.

However, this heuristic now carries inverted utility for growth investing. In modern finance, if you’re paying a dividend that means you don’t have enough growth prospects to invest in, so you return money to shareholders. If you’re rapidly growing, you keep your earnings and deploy it back into the business. I’ll cover this in more detail at the end.

-- A BRIEF HISTORY OF STOCKS AND DIVIDENDS --

The first instance of an IPO and publicly tradable stock in financial history came in 1602 from the Dutch East India Company, ticker VOC for Vereenigde Oost-Indische Compagnie.

The reason for VOC stock provides insight into business models and investor expectations from that era. VOC needed big chunks of capital for specific reasons: to finance voyages for its massive spice trade. VOC issued stock and bonds to fund highly uncertain expeditions, which could either pay out a lot or nothing at all. If the voyage was successful then everyone got paid, if not then no dividend.

Capital markets used to view stocks essentially as junk bonds. They paid a dividend that was greater than the debt coupon, however it was junior in the payout waterfall and contingent on certain degrees of success.

Here’s an example prioritized payout structure:

- 1st: Bondholders receive interest payments (eg 4%)

- 2nd: Preferred shareholders are paid next. More than bonds, but less than common stock (eg 6%)

- 3rd: If there’s remaining profit, then common stock gets paid. This dividend was the most uncertain, but also the largest (eg 10%).

Fun fact: sometimes dividends for VOC holders were in the form of pepper, nutmeg, cloves, and other kinds of spices! Imagine dividend day arrives and you get a big chunk of oregano in the mail. RETVRN.

Older companies issued equity for specific endeavors that required a large amount of money at once: we’re going on a voyage, we’re building a factory, a railroad, etc.. Growth was achieved in chunks, not increments; this is not how growth works today.

In modern times, businesses can use their profits for generalized, gradual expansion; you can do something productive with $500k or $50M. The old-school mindset was “we need $20M for an investment we think will make X amount of money, and we’ll pay you Y if it does”. If a voyage costs $20M, keeping only a fraction of that as retained earnings doesn’t do you much good. Growth came more in waves, less in persistent increases.

Here are excerpts from the brilliant @ByrneHobart that are very much worth your time. He’s incredibly insightful on dividend evolutions and the reasons behind them; I deeply appreciate this kind of nuanced analysis and draw heavily from it.

Today, retained earnings facilitate incremental reinvestment that wasn't practical or possible in the past. Capital gravitates to its most efficient uses, and it makes intuitive sense to me that earnings distribution vs deployment would evolve in a way that favors deployment. For the same reason water takes the most direct path downhill, capital eventually flows to its most productive uses.

-- INVESTOR EXPECTATIONS AND RETURNING CAPITAL --

A company can do two things with earnings. Two. You can:

- Reinvest the money into the business

- Return the money to shareholders

There are tech companies that raise money in big chunks for multiyear continuous growth: early stage VC-backed ones. And these startups are well-known for paying fat dividends…. 🙃

Do you know how many startups pay a dividend? Zero. Why? Because they use that money to 1000x by investing in growth. Pre-revenue, positive unit economics, it doesn’t matter, you do one thing with that money: grow, aggressively.

(I’ve only heard of one previous startup paying dividends: Kickstarter. And they’re extremely weird and not a big growth story.)

If growth investors wanted a dividend, they’d buy a tobacco company or bonds. We’re here for capital gains, not 4% yields. Paying a dividend would essentially be a sign of failure for a growth business… “Here take your money back, we can’t find enough productive things to do with it.” Empirically, investors now value growth above all else, and would rather management keep the money if it can be redeployed into expanding the company.

Investors just don’t care about “real yield” like they used to.

The environment for what modern businesses need to grow is much different than VOC times. Earnings can now be productively reinvested into the business and have a higher ROI to the company than paying them out, and modern shareholders are more than ok with this.

GrowthCo’s do not pay dividends, and they’re the most richly valued stocks. OldCo’s need to entice you with dividends, because performance isn’t cutting it anymore.

DeFi projects (crypto startups) have no such VOC-style limitations of yesteryear, yet the cultural demands act as if we’re going on a spice expedition.

-- Financial Natural Law, 100x or 5%: Pick One --

Do you buy a hypergrowth company for a 5% yield or a 100x capital gain? You know how you’re going to get that 100x? By the company growing rapidly. Do you know how the company will grow rapidly? By spending a lot (a lot) of money on marketing, product, marketing, employees, product, and marketing. It’s expensive out there.

DeFi is constantly hunting for the next 100x gem while also asking “do we get a yield too?”. That’s speaking out of both sides of your mouth. You can’t be a long-distance runner and a bodybuilder simultaneously. If someone promises you both… recall the saying on “free lunches”.

The growth-vs-dividends dichotomy feels tantamount to finance natural law. No reward without risk. No huge gains without volatility. To want 100x and 5% is to seek stability and volatility concurrently. To want reliability and wife-changing returns from one asset. It’s a contradiction. Devs have not outprogrammed the rules of leverage nor have they reinvented axioms of economics.

I’ll end with an interesting cultural insight: in the 19th century and earlier, wealth was often measured in terms of annual income, not the value of your assets. The historical emphasis on dividends makes a great deal of sense when you consider this social-signalling component.

It’s the exact opposite today. The ultra-wealthy only speak in terms of capital gains and asset prices. Even lower classes look to asset-based net worth as the barometer of wealth, not your salary/dividend streams.

Considering that absolutely no one in crypto measures their wealth in staking yield, I don’t think it will take all that long for us to speedrun the dividend thing. DeFi is currently in its VOC phase. This too shall pass.

"LPs in UniV3 are losing millions per year. Don’t LP unless you’re a pro!”

As a retail level LP, this hasn’t been my experience at all; once I realized LPing is like selling options, it got much easier to LP successfully.

Let’s use options to demystify IL/LVR/JIT/MEV

A 🧵