⚡️Stablecoins are being absorbed into the legacy payments empire before they fully escape it.

That is the whole move.

Visa and Mastercard can see the threat clearly.

Stablecoins attack the deepest part of their model: settlement friction, cross-border fees, merchant fees, card-network dependency, and the need for banks/payment processors to sit between buyer and seller.

Stripe sees the opportunity from the merchant/software side. Coinbase sees the bridge from crypto custody/liquidity into mainstream dollar payments.

Put those together and the shape is obvious: the incumbents are trying to own the stablecoin transition rather than get routed around by it.

This is regulated dollar infrastructure.

The people replying “this is centralized” are right, but they are missing the bigger point. Of course it is centralized. That is why it can scale into mainstream commerce. The mass market does not want seed phrases, bridge risk, fragmented liquidity, or ideological purity. Merchants want lower fees, faster settlement, fewer chargebacks, cleaner APIs, global reach, and accounting that works. Enterprises want compliance. Regulators want visibility. Networks want control.

This is the institutional stablecoin phase.

Stablecoins started as crypto-native liquidity instruments. Then they became offshore dollar rails. Now they are being pulled into the core payments stack. That means the next phase is not just “crypto adoption.” It is dollar settlement moving onto programmable rails under corporate and regulatory control.

The float question is the real money.

Who holds the reserves? Who earns the yield? Who controls redemption? Who owns the customer relationship? Who sees transaction data? Who sets compliance rules? Who can freeze, reverse, blacklist, or censor flows? That is where the power sits.

If Visa, Mastercard, Stripe, and Coinbase coordinate around a stablecoin platform, they are not launching a toy. They are positioning around the future settlement layer for internet commerce. The token itself may be boring. The control surface is not.

This is also a shot at banks. Banks have lived off deposits, payment rails, card relationships, settlement friction, and regulatory enclosure. Stablecoins threaten to peel away part of the transaction layer. The banks will not disappear, but their monopoly over money movement gets squeezed if stablecoin settlement becomes native to merchant platforms and wallets.

The big risk for card networks is cannibalization. The big opportunity is control. If they wait, stablecoins compress them. If they lead, they can turn stablecoins into another network layer and preserve relevance.

For Coinbase, this is structurally bullish. It places them closer to the regulated interface between crypto liquidity and mainstream commerce. Coinbase does not need every user to become a crypto trader. The bigger game is becoming infrastructure for onchain dollars, custody, compliance, wallets, conversion, and settlement.

For Bitcoin, this is indirectly bullish in the long arc because it further normalizes crypto rails as real financial infrastructure. But it also reinforces the split: Bitcoin remains neutral collateral, while stablecoins become regulated transactional dollars. Different roles. Bitcoin is exit. Stablecoins are upgraded dollar plumbing.

The clean truth:

This is the payment giants conceding that stablecoins are real while trying to make sure the revolution settles through them.

That is the phase shift.

Stablecoins are no longer fringe crypto instruments.

They are becoming the programmable settlement layer the incumbents now have to capture, defend, monetize, and regulate.

BREAKING: The first Federal National Mortgage Association-backed mortgage using Bitcoin in the US just closed using Coinbase 🇺🇸

The homebuyer said: “We closed on our home and my Bitcoin stayed intact. We didn’t have to liquidate, didn’t have to time the market” 🙌

@jakluge Bitcoin is an asset with a verifiable limited supply of 21 million, in a world where dollars are printed to infinity.

Not holding bitcoin is speculative: You'd gamble that governments will stop printing money.

When you study other things that have come back from 50% drawdowns multiple times, you realize it's all the best stocks on planet earth. It's Amazon, it's Microsoft, it's Berkshire. Only stud things come back 3 or 4 times & that's why I gave it respect.

@EricBalchunas on Bitcoin

@KingKong9888 Incorrect. They did not and cannot seize Bitcoin. However, you are correct, crypto and stable coins are at risk. Be sure to make the distinction.

BREAKING: Iran has launched "Hormuz Safe," a Bitcoin-backed insurance service for shipping companies that want to transit the Strait of Hormuz.

Details include:

1. The Iranian government says it could generate more than $10 billion in revenue from the program

2. The service will be for "Iranian shipping companies and cargo owners"

3. "The shipment will be covered from the moment of confirmation and signed receipt will be given to the owner," Iran says

4. It is unclear if this insurance service will be charged in addition to tolls, which have been as much as $2 million per ship

Iran says an official website with more information is "coming soon."

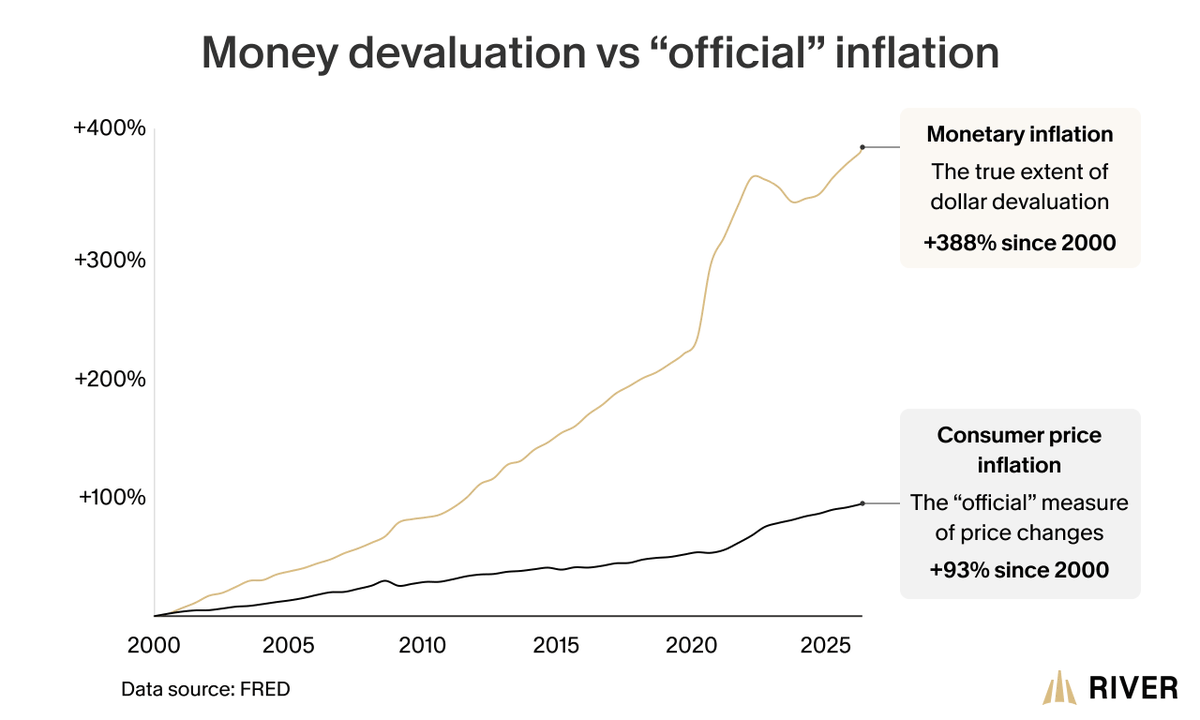

Ribeye inflation index has a big print. New price $37.99/lb. 17% inflation annualized from October. 18.5% annualized since last June. 90% cumulative since 2020. 11.0% compounded annually over 6+ years. Same ribeye, same store. High rates? Don't care. Bitcoin is the only way out!

You can’t explain Bitcoin to someone who doesn’t understand money in the first place.

No awareness of the problem = zero appreciation for the solution.

That’s why most people dismiss bitcoin.

MILES SUTER: “Bitcoin is the only truly censorship resistant money that there is right now.”

“If we don’t preserve peer-to-peer digital cash right now, it’s a right we’re going to lose forever.”

“It’s a really important thing for human freedom in the long run.”

JUST IN: Fast food giant Steak 'n Shake announces "when we use bitcoin, we save 50% on processing fees vs a traditional credit card user." 👀

"If every credit card user used bitcoin, we would save roughly $6 million annually. Which is huge" 🙌

Freezing $344 million in "crypto" is easy.

Freezing $344 million in Bitcoin is impossible.

You have to wonder what nations are looking at this and thinking...

1) Holding US Treasuries will get me sanctioned

2) Holding stablecoins will get me sanctioned

3) What about Bitcoin?