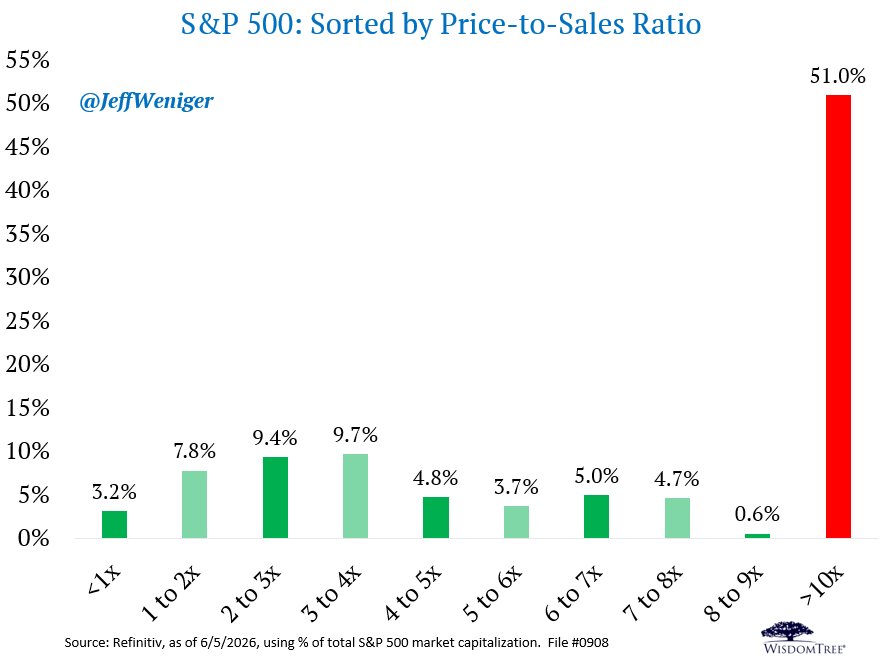

More than half the S&P 500's total value is now in stocks priced above 10x sales. This was once considered an outlandish valuation, as it leaves little room for error. The list includes Nvidia, Apple, GOOG, MSFT, Broadcom, Tesla, Micron, Eli Lilly, AMD, Oracle and 57 more.

🚨 I TOLD YOU THIS WAS COMING!

Absolute bloodbath:

$2,880,000,000,000 wiped out from the US stock market in just 2 HOURS

Let that number sink in.

Two TRILLION dollars. Gone!

In the time it takes to watch a movie.

And if you've been following me, none of this surprises you.

Because I told you that S&P 500 was walking into a trap.

No panic. Just the setup, laid out in plain sight.

Today the trap snapped shut.

So let me remind you WHY it's happening, in 3 forces:

Stacked on top of each other. Every 4 years

1. THE PRESIDENTIAL CYCLE

Year 1-2 is always pain. Tax hikes, budget cuts, "cleaning up the last guy's mess."

We're standing in the pain right now.

2. THE MIDTERM TRAP

15 out of the last 16 midterm years, the market bled from May to October.

A 93.75% hit rate since 1962.

Big money knows it. So they sell in May and hold cash through the summer.

Guess what month we just walked out of.

3. THE FED'S TIMING PROBLEM

The Fed always hikes early, so it has room to cut before re-election.

Translation: midterm year always lands at peak rates.

Exactly when the economy can't take it.

Now stack 2026 on top:

➮ Inflation at a 3-year high

➮ 10Y yield breaking 4.50%

➮ Mortgage rates pushing 7%

This wasn't a forecast.

It was a setup hiding in plain sight, and today it paid out in $2.8 TRILLION of other people's money

The next few days are going to get violent.

But don't worry. That's exactly what I'm here for.

Like it or not, I've called the exact market tops and bottoms for 11 years

My system flags the moment the market shifts from caution to DANGER

You will be warned before it hits, like always.

Not following me will be your #1 mistake of 2026, soon you'll understand why

What is causing the selloff in the semi space today?

🔴 Catalyst #1: SemiAnalysis Report, Nvidia's Vera Rubin Using Less System Memory

The SemiAnalysis article that shook the market is specifically about Nvidia's next-gen Vera Rubin NVL72.

What changed: The system-level DRAM (LPDDR5X) capacity per rack is being configured at ~28 TB, down from the previously expected ~55 TB.

🔴 Catalyst #2: Korean Market Cascade, KOSPI Crashes 5.5%

The SemiAnalysis report + Broadcom's soft guidance combined to create a violent selloff in South Korea:

KOSPI plunged 5.54% to 8,160, the worst single-day drop in months, SK Hynix dropped ~10%, Samsung Electronics fell 6%+

The Korean won hit a 17-year low against the USD, compounding the selloff

🔴 Catalyst #3: Anthropic's "When AI Builds Itself" Report

Published June 4, Anthropic dropped a bombshell report calling for the ability to slow down or pause frontier AI development:

Co-founder Jack Clark described AI development as having a powerful "gas pedal" but no "brake pedal"

They proposed a coordinated global mechanism (involving US and China) to provide the option to slow or pause development.

Net Effect: These three catalysts are converging to create a "question the AI trade" narrative across global markets, memory demand concerns + a leading AI lab calling for a slowdown + hot macro data keeping the Fed hawkish. A potent cocktail for volatility.

$DRAM $MU $SNDK $AAOI $BRUN $SPCX $ASTS $NOK $SIVE

i can't believe this 1 hour talk by the people who control the world's financial system including Ray Dalio, Jamie Dimon & Larry Fink literally told you exactly where the money is going for the next decade:

Today was one of those sessions where every single asset class got hit simultaneously and that combination tells you something specific about what just happened.

The trigger was the May jobs report.

The US economy added 172,000 jobs in May, coming in well above the forecasts that ranged from 80,000 to 105,000.

On the surface that sounds like good news but in this market, it was the worst possible number.

The Federal Reserve has been on hold for months, with markets hoping for rate cuts.

A strong jobs report especially alongside PCE inflation running at 3.8% annually tells the Fed that the economy is not cooling fast enough to justify cuts.

Instead, traders immediately repriced the probability of a rate hike in December from 26% to 43%.

That one shift in rate expectations rippled through every asset class at once.

Stocks sold off because higher rates mean higher borrowing costs for companies and more competition from bonds for investor capital.

The S&P 500 dropped 1.65%, wiping out $1.14 trillion in market value, Nasdaq dropped 2.60%, losing $1.11 trillion, with semiconductor and AI stocks leading the decline after Broadcom left its full year AI chip targets unchanged the day before.

Gold dropped 3.38%, wiping out $1 trillion.

This seems counterintuitive until you understand that higher interest rates make non-yielding assets like gold less attractive, cash and bonds start paying more, so gold loses its relative appeal.

Silver dropped 6.9%, losing $280 billion, and was already under pressure from a separate wave of Chinese investor selling earlier in the week.

Bitcoin dropped 6.31%, wiping out $80 billion, crypto has been trading as a risk-on asset in this cycle, meaning when fear spikes and rates rise, Bitcoin sells off alongside tech stocks rather than acting as a safe haven.

The fact that everything dropped together stocks, gold, silver, and Bitcoin is the key signal here.

This is not a story about any one sector being overvalued or any company reporting bad results.

This is a macro repricing event, where a single piece of economic data forced the entire market to recalibrate its assumptions about where interest rates are going.

When rates rise, the discount rate investors apply to future earnings goes up, which mechanically compresses valuations on every asset that is priced on future cash flows which is effectively everything.

The important context is that this does not change the underlying AI investment thesis, the $7.6 trillion capex buildout, or the fundamental demand for the companies we have been discussing this week.

What it does mean is that the market is entering a more volatile phase where inflation and Fed policy become as important as earnings and revenue growth.

🚨 do you understand what happened to the US stock market today..

A jobs report came in more than double expectations and the entire market panicked - because good news now means the Fed keeps rates high

- $1.75 trillion vanished from US stocks in hours.

- The crypto market cap dropped $130 billion alongside it

- Nasdaq 100 had its worst day since October 2025

- NVIDIA fell 5.84%, Bitcoin 5.99%, Ethereum 12.23%

The economy was too strong - so Wall Street had a breakdown.

Explaining why all assets are down.

When macroeconomic data (like an unexpectedly hot jobs report) catches the market off guard, expectations for interest rates turn hawkish. Treasury yields spike due to US action in Iran, the US Dollar rallies sharply, and mega IPOs are going public; it acts like a giant vacuum cleaner, sucking liquidity out of every single alternative asset class.

This creates a liquidity squeeze.

When the dust settles and forced liquidations stop, the structural fundamentals of gold, equities, and digital assets usually go back to normal.

For people who are worried about the market today, I get it. This stuff is very stressful.

So I put together a chart of all of the times the VIX (the "fear index" of the market) was up over 30% in a day (like today) in the past ten years.

23 out of 25 instances the market was higher one month later. The only two times it wasn't was Feb 2020 when Covid hit the economy in March 2020.

What is the underlying message? When people are afraid, they make bad decisions. Do the opposite.

Attached is a chart summarizing my results.

🚨South Korea's AI-driven stock market bubble is showing its first serious CRACKS:

The KOSPI plunged -5.5% on Friday, with Samsung Electronics falling -6.4% and SK Hynix collapsing -9.9%, as the global AI selloff triggered by Broadcom's disappointing earnings forecast spread from Wall Street into Asia.

Foreign investors sold ~$1.6 billion worth of Korean stocks in a single session, bringing this week's total foreign outflows to more than $10 billion, while the Korean won weakened to its lowest level since March 2009.

Samsung and SK Hynix together account for ~54% of the KOSPI's total market weight, making the entire index structurally vulnerable to any slowdown in AI chip demand.

Meanwhile, the % of KOSPI members hitting 52-week lows has surged to ~31%, the highest since late 2024, confirming that this selloff is broad-based.

Notably, single-stock leveraged ETFs tied to Samsung and SK Hynix are amplifying these moves in both directions, with the 4 most popular single-stock ETFs accounting for 21% of total Korean ETF turnover in their first 5 sessions after launching on May 27.

Is the South Korean AI bubble starting to BURST?

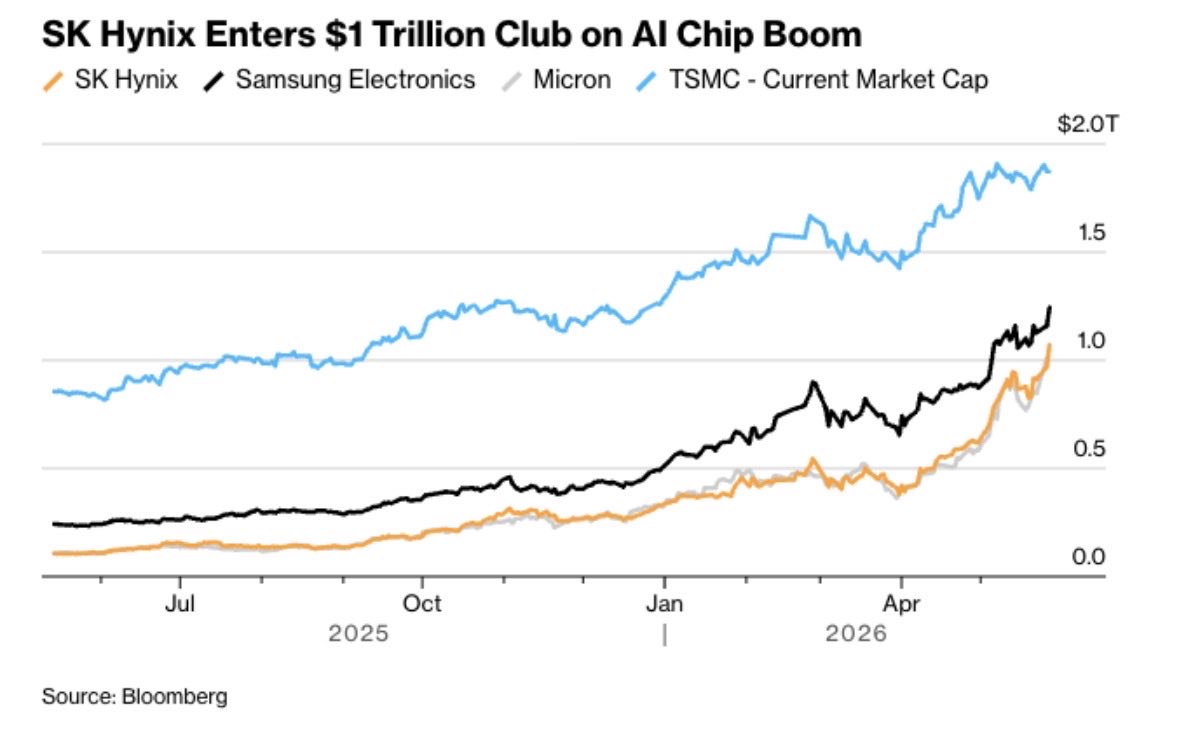

The pace of Micron’s rise to becoming a $1 trillion company is unprecedented. The dot-com boom created millionaires. The aftermath of the 2008 financial crisis minted billionaires. The AI revolution is resulting in trillionaires. https://t.co/0qwUdh7dFG

You can see how unsustainable current US oil exports are here…

Crude stocks are draining, refining runs rates have surpassed seasonal highs, & imports have fallen nearly 500k bpd.

And despite all of that, crude exports reach all time highs, pushing the US nearly to a consistent net exporter using rolling monthly averages.

The numbers don’t lie and the US is exporting crude at very unsustainable levels just to keep things in somewhat of a balance for now. #tankers #oott

🇰🇷 Korea is now the only country after the United States to have 2 companies that are worth over a trillion dollars each as Samsung and SK Hynix join rally 7%, 12% today alone

This country and its people is truly one of the world largest wonder-what an incredible story & country

MSCI EM leadership is shifting fast.

🇨🇳 China’s weight in MSCI EM has fallen from ~43% Oct’20 to ~21% post May’26 review.

AI + semiconductor tailwinds have pushed:

🇹🇼 Taiwan to ~26.5% vs 12.7% in October 2020

🇰🇷 Korea to ~21.5% vs 11.9% in October 2020

🇮🇳 India, after peaking near ~20% in Jul’24, is back to ~11%.

Interestingly, MSCI India vs MSCI EM is now near the lower band of a rising channel in place since 1996 with relative drawdowns deeper than prior cycles.

Source: IIFL Alt Desk

Potential mean reversion setup 🤔

Thoughts from Michael Hartnett, BofA | This Is The Biggest Bubble Since The Railroads

The current AI-driven market rally resembles one of the biggest speculative bubbles in history, comparable to the Nifty Fifty or dot-com era, but investors are unlikely to aggressively sell before two catalysts occur: a major OpenAI/SpaceX-style IPO cycle and a clear Fed policy tightening shock tied to rising CPI from tariffs and inflation.

•AI mega-caps now dominate market concentration, with the “AI bubble” larger than past railroad, Japan, and dot-com bubbles by some metrics.

•Bond yields are the main warning signal: the rise in long-term yields and global cost of capital seen as dangerous for risk assets, especially leveraged consumers, private equity, housing, and emerging markets.

•Several macro stress signals are flashing: weak Asian currencies (KRW, JPY, INR, IDR), widening high-yield spreads, EM outflows, and BofA’s Bull & Bear Indicator hitting a contrarian “sell” level.

•Historically, speculative IPO waves (Alibaba, NTT, Visa, etc.) often marked medium-term market tops rather than immediate crashes.

•Current gains are very narrow (“wealth effect, not wage effect”), while equal-weight consumer stocks remain weak versus the S&P 500.

•Despite near-term bubble concerns, structurally bullish on emerging markets and commodities.

•Preferred post-bubble opportunities would be consumer stocks and smaller AI adopters/disruptors rather than dominant mega-cap AI platforms.

•Geopolitics, energy, AI competition with China, and inflation are increasingly interconnected themes shaping markets.

Zeitgeist quote: “Everyone is now convinced that equities are the best inflation hedge.”

Feedback from recent London trip, main soundbites:

•“we’re long and paranoid,”

•“wants/needs to de-escalate Iran, and stocks pop, yields drop on deal,”

•“if UK gilts find love, everything finds love,”

•“European electorate shifting decisively right, Farage in UK, Le Pen in France, and you watch the AfD in Germany will win Saxony-Anhalt in September, their first state election,”

•“the fear in bonds is nowhere near as strong as greed in equities,”

•“Warsh will be rhetorically hawkish but practically dovish over the summer,”

•“US actions in Venezuela, Ukraine, Iran, Greenland, Cuba should be viewed through single strategic lens competition with China in AI, which can only be won by securing access to critical resources.”

You can't make this up:

On May 22nd, ahead of the market's 3-day closure, President Trump said "Micron is great" and that the company could invest "over $100 billion" in New York.

Today, as markets reopened, Micron's stock, $MU, surged +19%, adding +$150 BILLION in market cap in 1 day.

In just 12 months, the stock's value has gone from $70 billion to a record $1 trillion, adding +$930 billion.

Truly unprecedented.

En un informe de estrategia de Rothschild muy interesante, concluye que el mercado de EEUU se mueve por flujos y no por fundamentales pq las enormes compras de los fondos pasivos obedecen a decisiones sistemáticas de asignación de activos y no al análisis de las compañías 🤔🤔🤔

Leveraged trading in Asia is more popular than ever:

The 2x Leveraged SK Hynix ETF, listed in Hong Kong, has attracted +$1.3 billion in year-to-date inflows.

As a result, total ETF assets under management (AUM) are up to $8.0 billion, the highest on record, making it the world's largest single-stock leveraged ETF by assets.

This fund’s AUM has more than TRIPLED over the last 3 months.

Furthermore, the 2x leveraged Samsung ETF has attracted +$1.3 billion in inflows so far in 2026.

This exceeds the year-to-date inflows of comparable 2x leveraged ETFs tracking Tesla, $TSLA, and Microsoft, $MSFT.

Now, SK Hynix and Samsung are the two largest South Korean stocks, together accounting for nearly 50% of the KOSPI index, which has a total market cap of $4.5 trillion.

Asian retail investors are rushing into leveraged chip stock bets like never before.

🚨Fund managers are piling into stocks at a RECORD PACE:

The share of global fund managers overweight equities jumped +37 percentage points in May, to a net 50% overweight, the largest single-month increase on record.

TAP IMAGE TO SEE FULL INSIGHT👇

https://t.co/EzLukdVPoh

🚨Big Tech is borrowing at a record pace to fund the AI buildout:

Amazon, Alphabet, Meta, and Oracle have collectively issued $159 billion in bonds year-to-date, according to LSEG data.

Amazon leads with ~$57 billion in total issuance, followed by Alphabet at ~$52 billion, while Meta and Oracle have each issued ~$25 billion.

~$50 billion of the total has been raised in non-US dollar currencies, as companies tap European, Japanese, and other foreign debt markets to diversify their funding sources.

US technology companies now account for more than 20% of investment-grade bond supply in the euro, sterling, Canadian dollar, and Swiss franc markets, according to Goldman Sachs.

raising concerns about portfolio concentration among global fixed income investors.

Meta, Alphabet, Microsoft, and Amazon are expected to spend more than $2 TRILLION in CapEx over the next 3 years, meaning the borrowing spree is far from over.

The AI infrastructure is being financed by debt more than ever.

I have a theory why both Japan, Taiwanese, and Korean currencies are so cheap right now.

It's because they are close to China, and considering that China is 88% of East Asia's population and it has a policy of keeping a cheap currency vis the USD forces down the price level of the whole region.

Up to the early 2010s it was still possible for the Japan and Korean price level to deviate drastically from China's because China didn't compete on high tech exports, but now it does.

As the Chinese economy converges to the technological frontier it is forcing the price level of it's developed neighbors to equality but it can keep it's price level much lower than the US's.

This is in some sense nice: currently, Chile, Brazil, China, Japan, Spain, and South Korea are all similar in terms of price level, with PPP varying by about 20-30% relative to the exchange rate.