Jay|Founder @econblox

🎓 Harvard MBA | 40-yr CEO & PEng | 🫡 Vet

📚 Author of 6 books on business economics

🤖 Built the AI advisor I always wished I'd had👇

@AGHuff Any operator hiring for results doesn't care much about credentials.

They care about whether you can do the job.

Participation trophies don't make the shortlist.

On Black Monday, October 19, 1987, automated trading algorithms helped wipe 20.4% off the S&P 500 in a single session.

The computers did exactly what they were programmed to do.

Nobody had thought through what happened when they all did it simultaneously.

That's not a computer failure. That's a judgment failure.

The S&P 500 rebounded 5.3% the very next day and 9.1% the day after.

Investors who didn't panic kept both recoveries - and everything that followed.

That's the decision Econblox is built to support - not the automation, the judgment.

@girdley TopGolf's real business wasn't golf. It was giving non-golfers a reason to show up.

The Jolliffe brothers figured that out only after closing their first location.

Sometimes the market tells you what it actually wants - if you're still in the game to hear it.

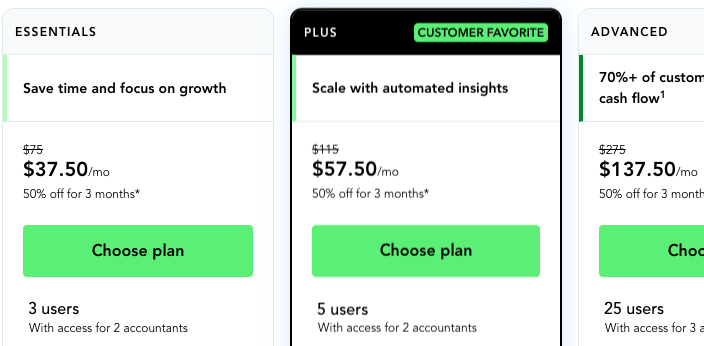

Legacy software is quietly taxing your P&L.

A few examples operators rarely question:

- QuickBooks: $75–$115/user/month for transaction recording

- Generic CRM: $50–$150/user/month for contact management half your team ignores

- Project management tools: $25–$50/user/month to replicate a whiteboard and a spreadsheet

The software isn't the real problem.

The real problem is that none of it helps you make a better decision. It just documents what already happened.

That's the gap Econblox fills - not another workflow tool, but the part where you figure out what to do next.

QuickBooks charges $75–$115 per month to do basic transaction recording.

I just exported 12 months of raw bank transaction data and ran it through an AI tool.

Full accounting reports and tax records. Done in minutes.

Legacy accounting software isn't solving a hard problem anymore. It's collecting rent on a workflow that no longer needs it.

The business operators I work with at Econblox aren't asking whether AI can replace existing systems. They're asking why they waited.

#SmallBusiness

The current debate over Nvidia’s valuation and customer concentration reminds me of a legendary financial history lesson: the collapse of Stirling Homex Corporation.

In the early 1970s, Stirling Homex aggressively booked revenue the millisecond a modular housing unit rolled off the assembly line—even though the SEC later revealed they had no secured contracts or ready installation sites. They mistook a manic, short-term production push for permanent economic demand.

While Nvidia does not have a "phantom revenue" problem, the structural demand distortion looks eerily similar.

In their April 2026 10-Q, just 3 hyper-scaler customers accounted for 63% of Nvidia's entire accounts receivable https://t.co/dI8lkhhBG9. Are these tech titans buying chips based on permanent consumer demand, or are they just burning billions to out-benchmark each other on AI leaderboards?

History shows that treating a short-term, competitive infrastructure race as permanent demand can easily lead to a brutal cash flow catch-up:

The Telecom Fiber Glut (1990s): Built on the illusion of permanent growth, telecom giants laid over $500 billion in fiber infrastructure, only to discover later that only 3% of the laid fiber optics was needed to meet consumer demand.

The Radio Boom (1920s): RCA became the ultimate glamour stock as infrastructure surged, skyrocketing from under $5 to an astronomical peak of over $540 before the 1929 crash wiped out 98% of its value..

Exceptions exist—like Tesla building out its early Gigafactory and Supercharger runway—but treating a frantic corporate race to build capacity as if it is permanent consumer demand carries historically high risks.

#NVDA #FinTwit #Macro

Thoughts on this, @JavierBlas@KobeissiLetter?

Striking look at global diesel dynamics. What stands out to me is the massive lag in 2025—stockpiles were sliding to multi-decade lows, yet futures prices remained entirely flat.

Historical EIA Data https://t.co/IRNKQpcSx4 shows U.S. national average diesel flatlined around $3.50/gallon for nearly all of 2025, completely ignoring the structural drain on inventories.

It wasn't until the Hormuz closure forced a reality check in 2026 that the lack of a supply cushion sent prices vertical, exploding over 53% to $5.52/gallon by May.

Was the market pricing in weak global industrial demand throughout 2025, or was it simply a classic case of mispricing the risk of a structural supply shock until it was too late?

Thoughts on this lag, @JavierBlas@KobeissiLetter?

The @michaeljburry / @BullTheoryio thesis reminds me of the famous Harvard Business School case study on Stirling Homex Corporation.

Stirling Homex juiced its paper numbers by booking sales the moment modular homes left the factory assembly line—even though there were no ready installation sites or approved funding. It created a massive illusion of permanent demand.

While Nvidia doesn't have a "phantom revenue" fraud issue, Burry is spot on to question if NVDA's current valuation is built on permanent demand, or just a temporary, hyper-competitive infrastructure race among a handful of tech titans.