So excited to have my very own @substack newsletter! Signing up is free, and this is the only medium where I share my personal portfolio. I’d love it if you would join me on the journey to better investing.

https://t.co/nlxSh4L5gw

By removing used cars, food, energy and housing you are stripping off over 60% of CPI components.

It's like saying Italy sucks if you don't account for weather, cuisine, art and nice people.

there seems to me to be the potential for a sharp correction. If even 1 or 2 homeowners in a neighborhood come into financial difficulty and are forced to sell at lower prices, this has somewhat of a “mark to market” effect on the whole neighborhood. When does the dam break?

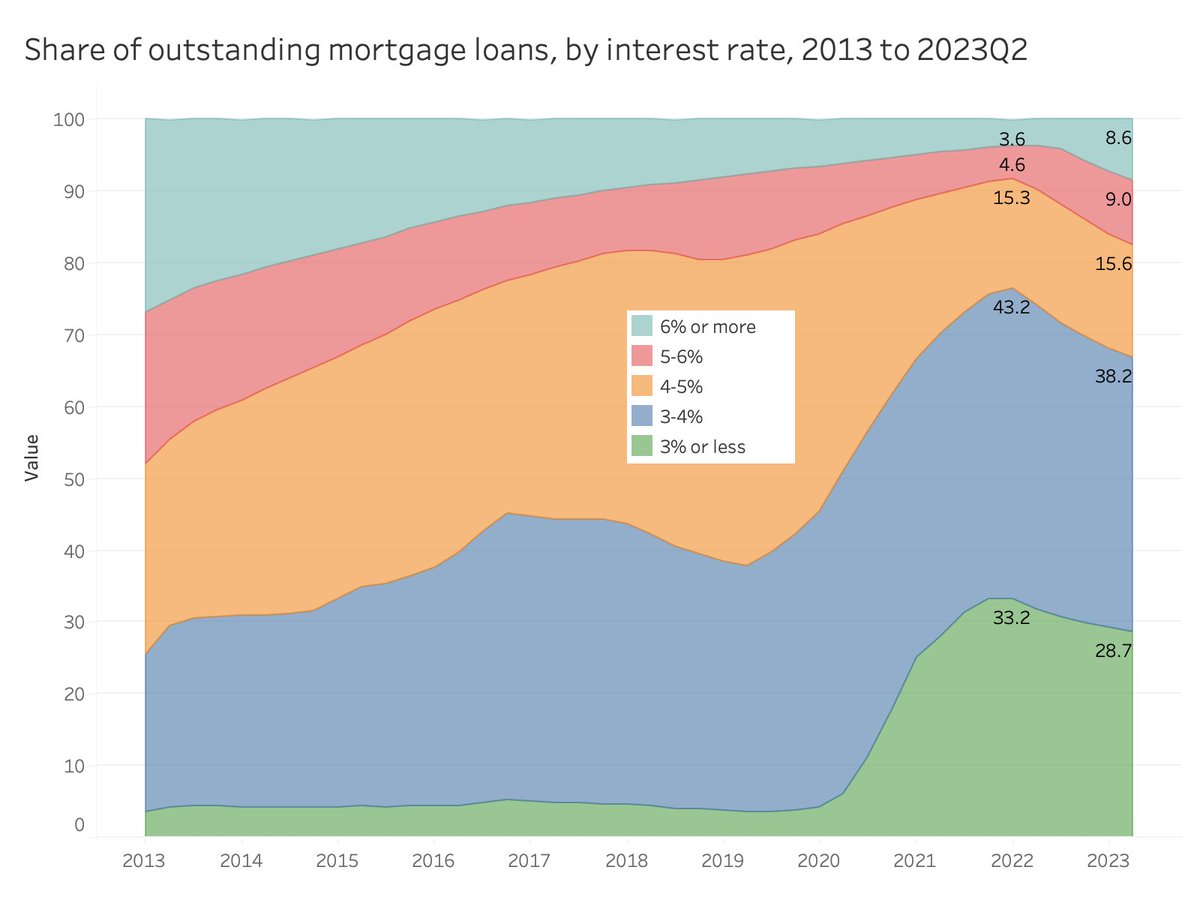

Thank you, @Jeff_Tucke. So I see that, in the past year, roughly 10% of mortgage debt has moved from the sub-4% groupings to the over-5% groupings. Further, that a full 33% is now above 4%. What strikes me is that . . .

Outstanding mortgage debt, by interest rate. Those low interest rates are a nonrenewable natural resource, slowly eroding as the principal gets paid down.

From the National Mortgage Database.

Hang on, though. Is this nominal, or real? Given what inflation has been over this past year, might not a 5.6% “increase” for lower-income consumers simply be the same amount of non-discretionary items? @carlquintanilla

GOLDMAN: “.. Perhaps surprisingly, we find the lower-income consumer is outperforming, with our measure of same-store sales rising 5.6% year-on-year for the 10 retailers whose stores are generally located in lower-income zip codes.”

In recent articles for my @substack newsletter, this is one part of a pattern that keeps me cautious at the moment.

If the consumer is truly so “strong,” it seems counterintuitive to have at least some as desperate as this.

We’ve been here before, in 2007-2009. The commonality? Prices became detached from actual affordability.

During that period, this was accommodated via ARMs, stated-income loans (actual income not verified), and interest-only loans. Looks like we are starting down the same path?

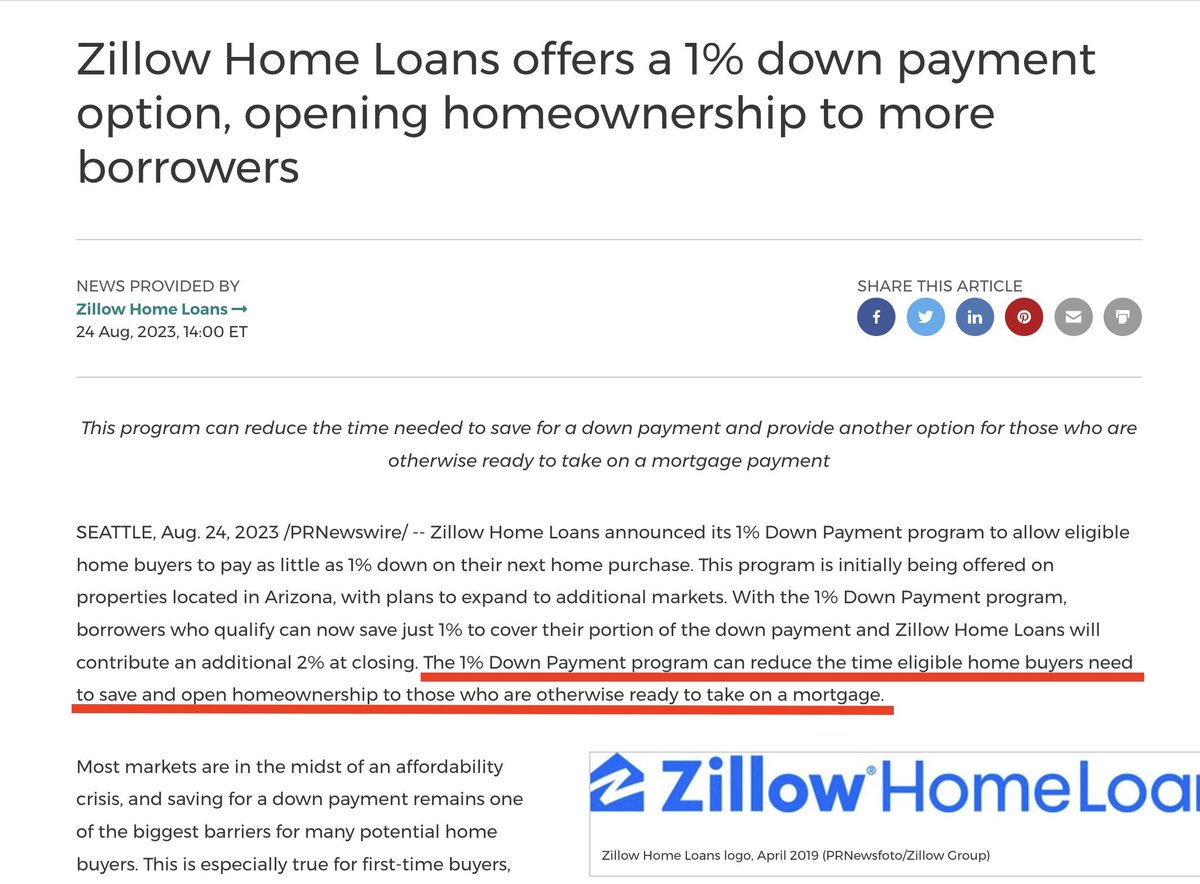

Here's how unaffordable the housing market has become:

Today, Zillow announced that they will begin offering mortgages with 1% down.

Meanwhile, other lenders are now offering 40-year mortgages.

The monthly payment on a $500,000 home with 30-year mortgage and 1% down is $3,500, or $42,000 per YEAR.

This is concerning.

@carlquintanilla@business I just checked, and the Schiller PE ratio was under 20 as the 1990s began. Today? North of 30. Are we sure there is an equivalency here? $SPX

In this article I share the reasons that I feel, as I describe it, that something’s gotta give. Supposedly, the economy and the consumer are... https://t.co/BCsWl0InuJ

@carlquintanilla Is this the same B of A that just reported a 36% increase in 401(k) hardship withdrawals? Can both really be correct? $BAC

https://t.co/FSnx1JzJsW

In my latest article, I feature a recent UBS report on family offices. I identify an area in which many plan to expand allocations, and an ETF to help you do the same.

$VGK @SeekingAlpha

https://t.co/YlKB6nAoqF