Bill Ackman says Pershing Square made $MSFT “a core holding” after it began building the position in February. He says Microsoft “offers compelling value.”

@oguzerkan Yes, but you can buy Pershing Square Holdings (the old LSE traded vehicle) at 31% discount to NAV. It's an attractive entry vehicle to some of these big names in my opinion.

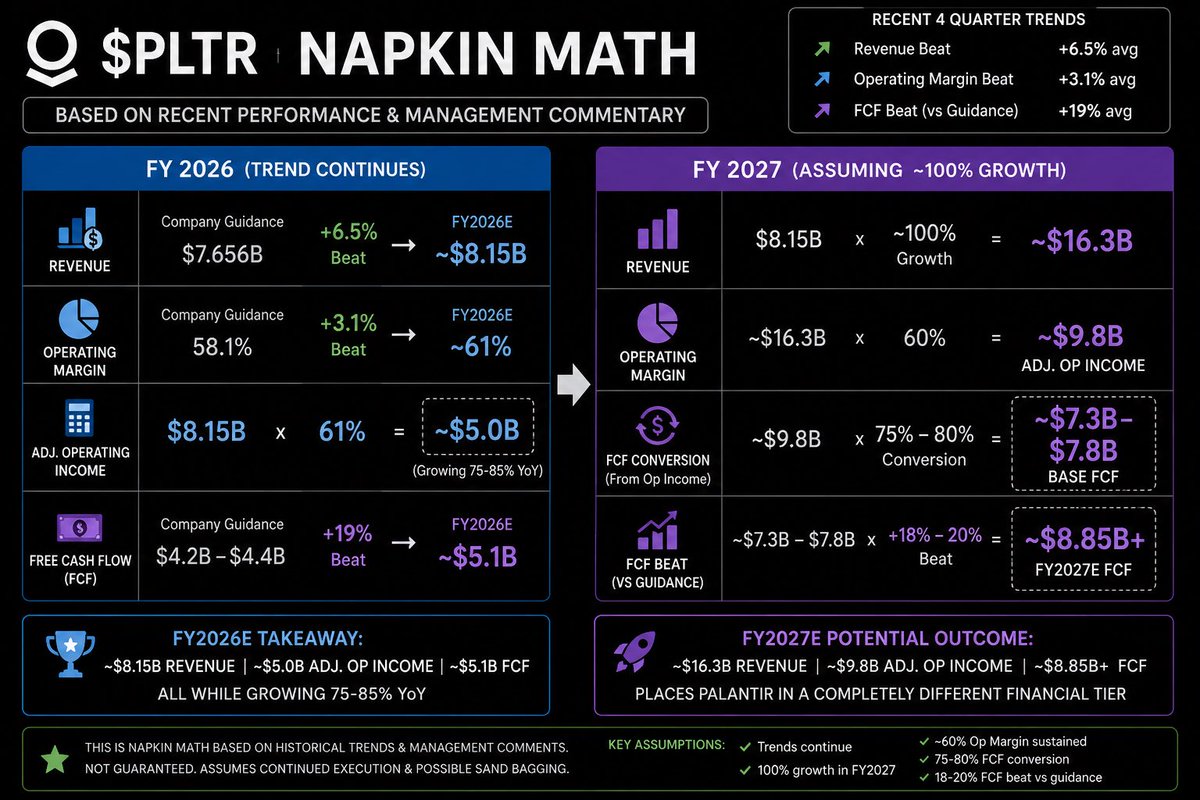

$PLTR

Some quick napkin math…

Over the last 4 quarters, Palantir has beaten revenue expectations by an average of 6.5%

If the trend continues, Palantir’s FY 2026 revenue will be ~$8.15B vs $7.656B (company guidance)

Over the last 4 quarters, Palantir has beaten operating margins by an average of ~3.1%

If the trend continues, Palantir’s FY 2026 operating margins will be ~61% vs 58.1% (company guidance)

$8.15B with 61% operating margins = ~$5B adjusted operating income for a company growing 75-85% YoY…

FCF has also been accelerating…

Over the last 4 quarters, Palantir has beat FCF expectations/guidance by an average of ~19%.

If the trend continues. Palantir’s FY 2026 FCF will be ~$5.1B vs $4.2-$4.4B

Let’s assume Karp’s “100% growth next year” is true (probably sandbagged), that means for 2027 we can expect:

~$16.3B x 60% operating margins ≈$9.8B adj operating income

Assuming 75-80% FCF conversion that means ≈ $7.3 - 7.8B FCF and if we assume the average beat of 18-20% that puts FCF at ≈ $8.85B +

In other words, this puts Palantir in a completely different tier financially and this is based on current historical trends!

Everybody jumps to the conclusion "AI is a bubble", but ignore the fact that underlying demand is rising just as fast as the stocks.

Sure, if the fundamentals break down, the stocks will too. But what if they don't bc demand is actually sustainable? Then we're far from a bubble.

$DUOL report is not bad at all folks.

I see a lot of hate on here, and that’s because sentiment follows share price.

If this same report came out and the stock was up 10% everyone would be bullish on Duolingo.

Bookings and gross margin are the weak spots, but zooming out this company is incredible.

It now has 56.5M people using the platform every single day…

This number was only 52.7M 3 months ago!

monthly active users have climbed up yet again after falling last quarter.

Free cash flow is up ALOT YoY including FCF margins.

They bought back 1% of the company last quarter at bargain prices and plan to continue doing so moving forward with their $400M buyback program.

They’re executing on the teaching front as they’ve stated that words spoken in lessons is up over double YoY (management believes this will improve the user experience and make them a significantly stronger company long term)

I’m more than willing to let this one continue compounding for a few years while everyone thinks the end is near for good ole Duolingo!

$DUOL suffers from tough comps (viral dead Duo campagin and introducing energy)

Besides that, the quarterly numbers were strong

I guess they'll go back to pre-covid growth rates (15-20% annually) starting 4Q26, which is healthy for the business long-term

No reason to panic

At this point it's obvious there's nothing wrong at all with $DUOL

Market reactions are just entirely detached from fundamentals for some reason.

Even Palantir crushed estimates and raised guidance significantly.

Yet, $PLTR is still down -5,5%

Solid earnings by $DUOL

- 56.5M DAUs (up 21%)

- 147.8M FCF (50% margin)

but most importantly:

- 20,500 new course models (using AI to build faster)

- engagement up bc of improved content

Focus on improving and driving engagement

Exactly what long term investors like to see