Suby v3 soon.

Your customer taps Apple Pay or pays by card. You get USDC. Your customer pays in BTC. You receive fiat.

Cards, Apple Pay, Google Pay, stablecoins, crypto and more in. Bank or stablecoins out.

Auto-swap does everything in between.

New app, fully rebuilt.

The gap between cash and crypto just disappeared.

We think crypto competes with banks. In reality, @base is going after Visa, Mastercard, @stripe, and PayPal.

And the numbers are starting to prove them right.

Base isn't positioning itself as "just another Layer 2" anymore. Their bet: become the payment infrastructure that directly competes with the biggest web2 payment rails.

The numbers speak for themselves.

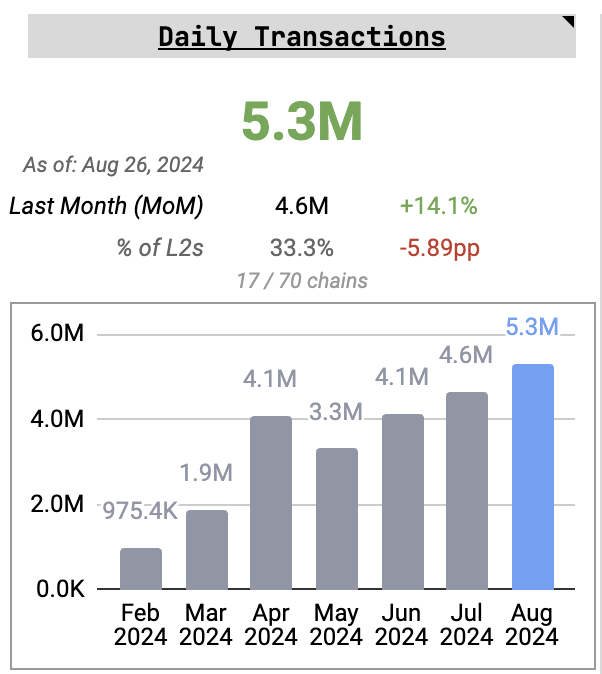

Stablecoins on Base hit ~$5.2B, with USDC at ~90.9%. 12.89M daily transactions at $0.02 median fee. Card networks would charge billions for the same volume at 2.5% interchange.

The honest caveat: that gap holds at settlement. Card rails are priced on wrapped credit, fraud exposure, and reversibility. Strip those out and the question shifts from "cheaper rails" to who carries the risk when things go wrong.

The Coinbase moat

With 110M+ verified users and $250M+ in onchain payments processed in three months, the playbook is clear:

→ Start with institutional B2B payments

→ Onboard merchants (Shopify already accepts USDC via Base)

→ Build a credible alternative to legacy rails

@brian_armstrong puts it bluntly: old way = 3-5 days, 3%+ fees, closed weekends. New way = $33T settled in stablecoins last year, sub-cent fees, 24/7/365.

One nuance: sub-cent fees are network fees, not all-in. Move USD to EUR and you still pay on-ramp, off-ramp, and FX.

The targets are explicit:

- Visa & Mastercard: Visa reported $4.6B annualized stablecoin settlement on its network in Q1 2026.

- Stripe: Coinbase + Nium for USDC payments settled in local fiat across 190+ countries.

- SWIFT & ACH: stablecoin transfer volume eclipsed the ACH network by early 2026.

The real battlefield: agentic commerce

McKinsey & Company projects agent-driven transactions could hit $3-5T by 2030. Visa launched Trusted Agent Protocol. Mastercard has Agent Pay. But those frameworks still sit on rails designed for humans. An AI agent running 1,000 micro-transactions per hour can't operate there.

Base took a step ahead with x402, co-developed with Cloudflare and Anthropic. Settlement in ~200ms, fraction of a cent per transaction. AWS just integrated x402 natively into Amazon Bedrock AgentCore Payments.

Frenemies: competing and partnering at once

Coinbase uses Visa for cards, Stripe for on-ramps, and competes head-on with both on rails. Base is simultaneously a competitor and a partner of the networks it wants to disrupt.

What it means: Web2 rails still own consumer credit, fraud guarantees, and reversibility. But their monopoly on institutional flows, cross-border B2B, and soon agentic commerce is being directly challenged.

Base is betting the next decade of payments won't belong to cards. It will belong to stablecoins on programmable rails, with risk repriced and unbundled rather than wrapped in interchange.

APMs were the first wave. Stablecoin rails might be the second.

PS: I post weekly about payments, stablecoins, and the reality of building a payment startup with @subyhq. Follow for more!

v2 launched one month ago. v2.1 is already a different product.

Not because we changed direction. Because we listened.Every conversation with merchants. Every friction point. Every "this could be better", we took notes and we shipped.

Here's what's in v2.1:

- Onboarding & UX: every step tightened based on real feedback. First impression matters in payments. Ours now reflects that.

- API: same foundation, completely different level. Developers who tested v2 will notice immediately.

- Docs: rebuilt around how developers actually use the product, not how we assumed they would.

- Payin & payout options: significantly wider. More ways in, more ways out.

- Fees: 4-5% overall. No FX fees. No international card surcharge. No hidden costs. What you see is what you pay.

- Payout speed: up to T+0. Your money moves when you need it to.

One month. Same product. 10x sharper. If payments are still a friction point for your business, watch this space.

@EzimmaduC @i_muss@InterestingSTEM Being born somewhere can make you a Christ or a Muslim by identity, but only Allah knows whether you truly belong to that religion. Oth people's faith is none of your business; it is something btw them and Allah. By misrepresenting Islam, you are showing ignorance. Read it first

Just shipped Suby v2

Your processor says 2.9%. Reality is 7-12% after FX, taxes, compliance.

• We built what you actually need:

• Card & crypto → USDC out

• API + Discord/Telegram integrations

• Taxes, fraud, subscriptions handled

Thread with demos 👇

@abilasports futbol izleyicisinin ne kadar cahil olduguna bir kanit resmen, kadin kural ihlali yapiyor. Kosarak tac kullanamazsin. Momentum : kuvvet x hizdir.

@TuncaIchizo Binance long %60'i gecti, ben kari aldim kapadim full nakite gectim. Burdan yukselmesi cok zor cunku usdt dom da destege geldi, hadi azcik bile daha yukselse bu kadar long islemi ile birlikte ustte local bir tepede kitleyecekler. Dusus bekleyecegim. Bu kriz ortaminda +

@ZAMajans O adamı zamanında kendisi seçmiş ve sonucu da kendisine yansıyor. Adam bi anda silah çekse ve kendisine karışanları vursa? kimse yardım etmiyor evet ama her bozuk ortamın özüne bakmak gerekir. Bu adamları seçmemeyi ne zaman ögreneceksiniz kadınlar?