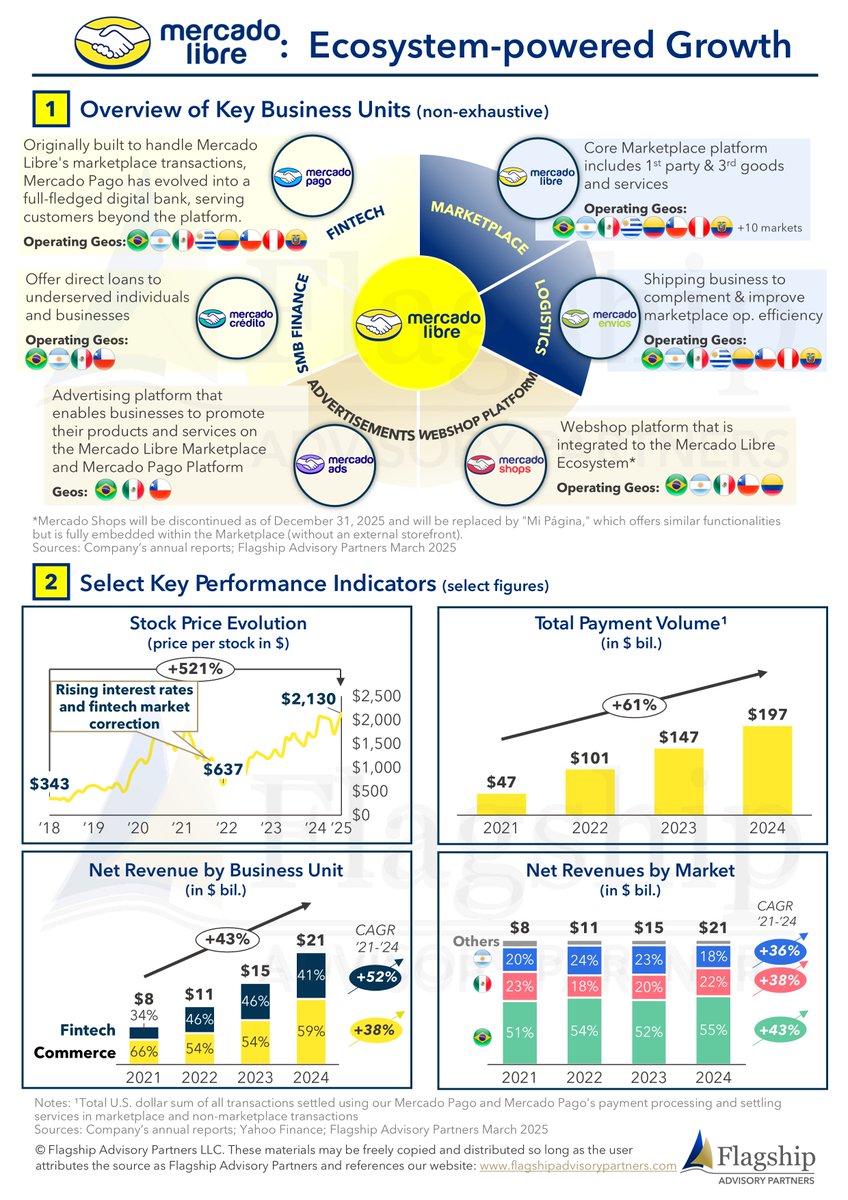

Latam powerhouse @Mercadolibre is a global example of how to successfully integrate fintech with commerce, showing how platform-driven expansion and embedded finance can transform digital businesses: https://t.co/Hd4VLG5Lyq #fintech#payments#latam#Argentina#brazil

#Openbanking enables secure data sharing between banks and third parties, facilitating #payments and info access. Beyond the UK /Europe, we now see other regions at the cusp of open banking adoption, driven by both regulatory and market forces: https://t.co/VWe1srriZ5 #fintech

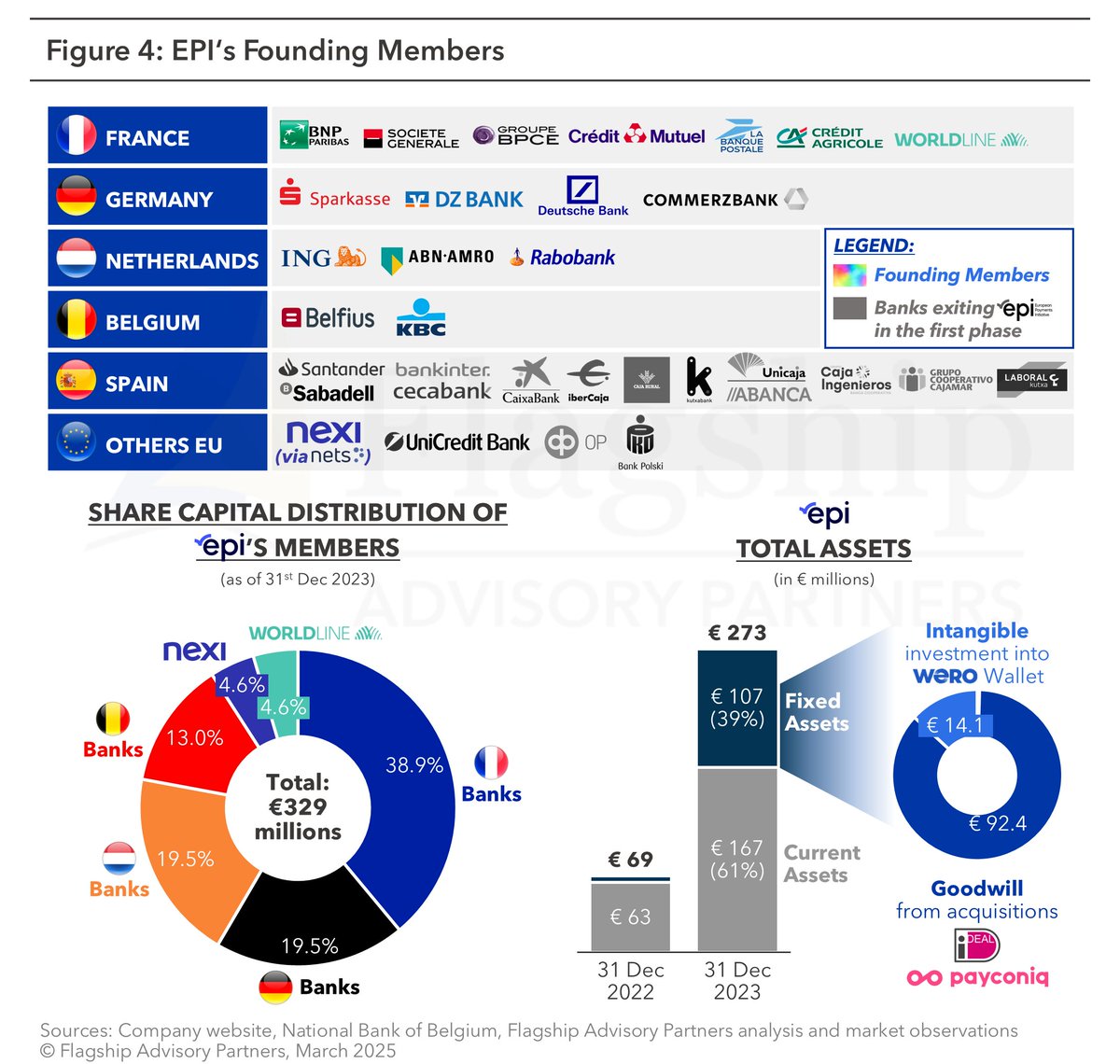

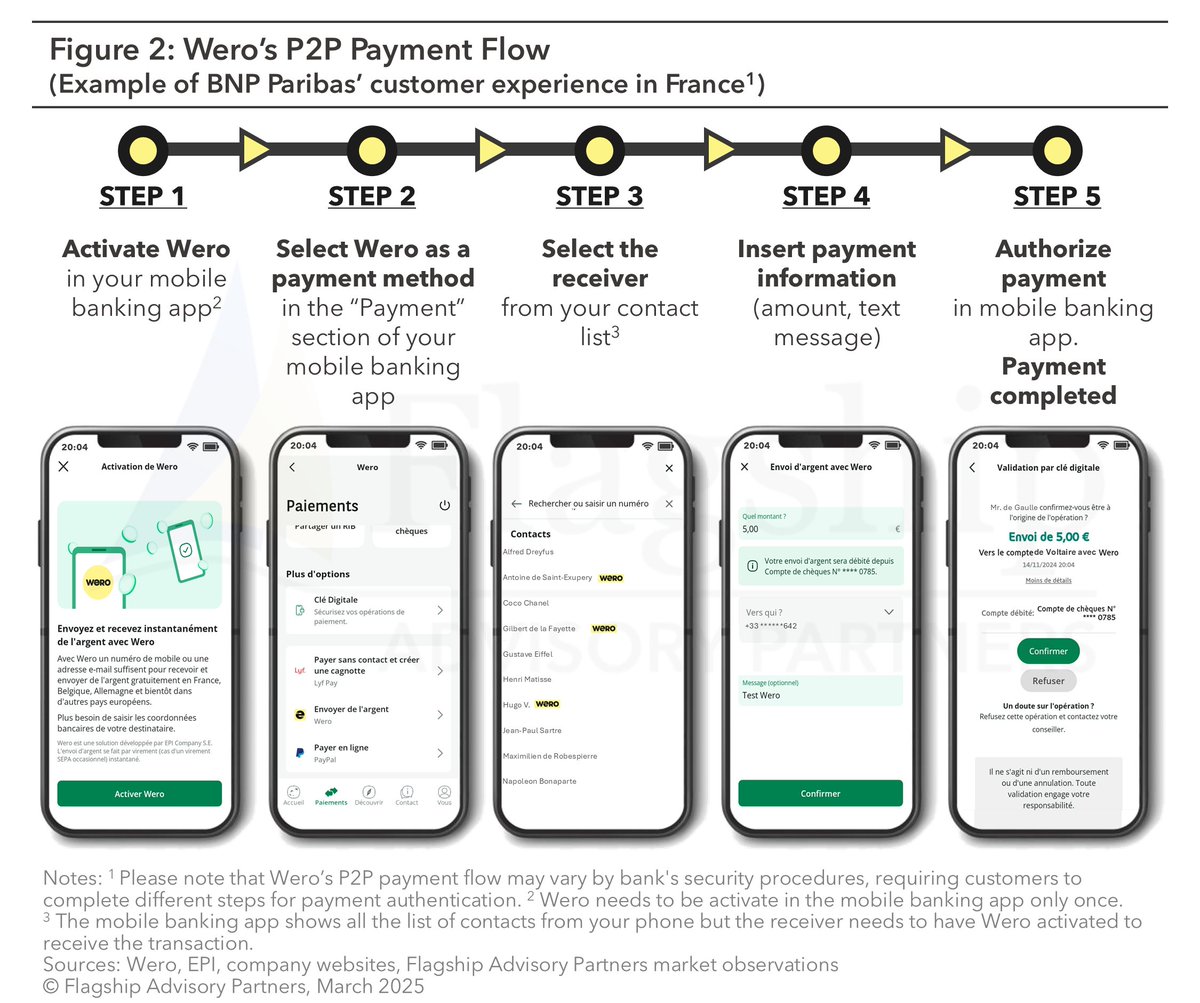

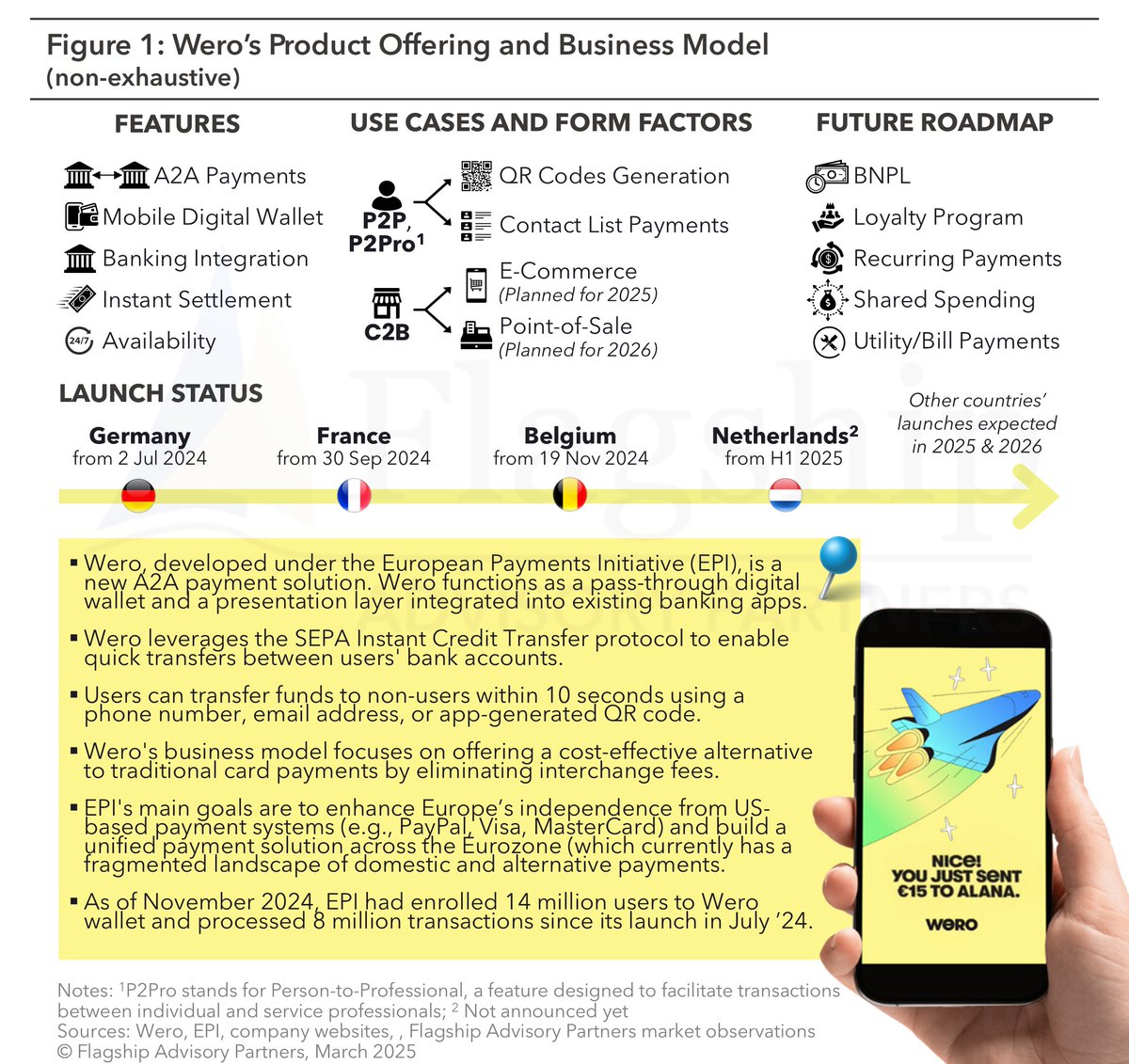

The European Payments Initiative (EPI) has introduced Wero, a Pan-European A2A wallet designed to unify and simplify EU payments for consumers and merchants. Read here: https://t.co/f3D7njsPqS #wero#payments#fintech#EuropeanPaymentsInitiative#fintechnews

@company_epi has introduced Wero a Pan-European A2A wallet designed to unify and simplify EU payments for consumers and merchants

Read more here:https://t.co/f3D7njsPqS

#a2a#digitalwallet#payments#wero

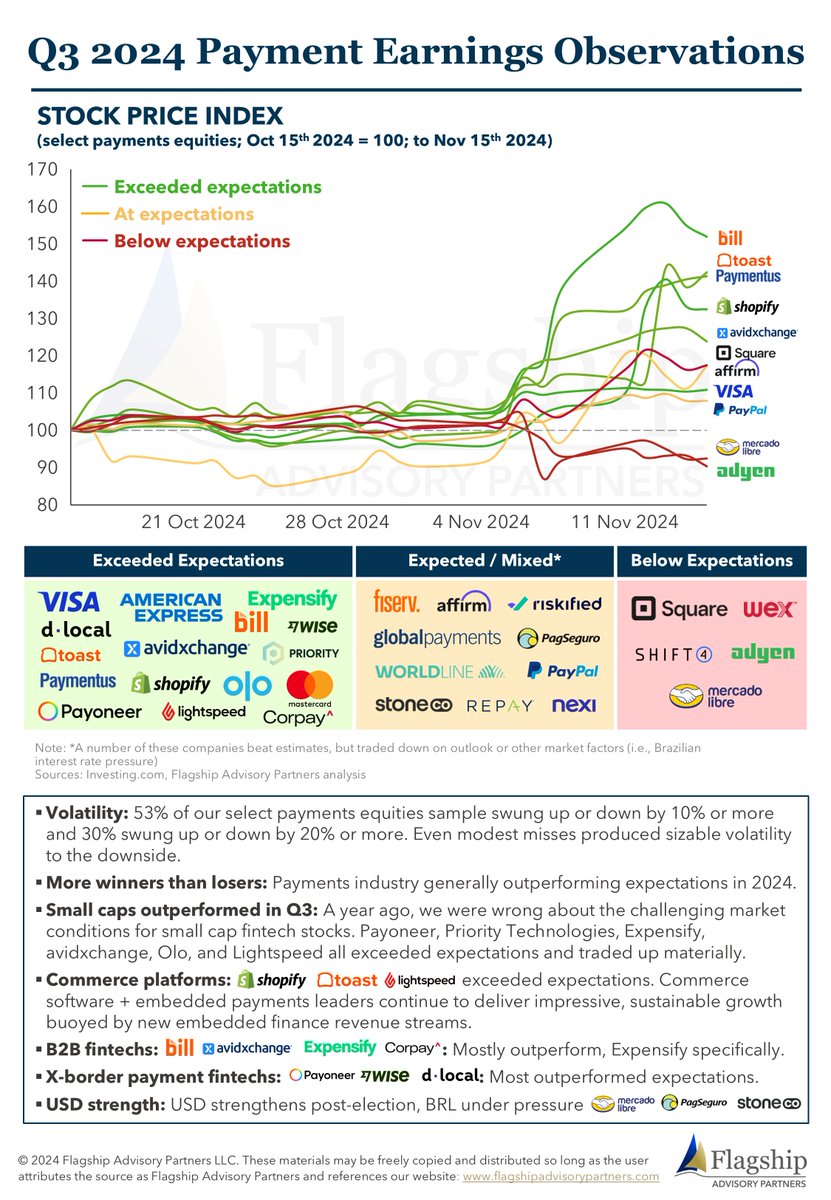

Fintech public equities are rising with the general market in 2024, but performance vs. growth expectations still matters. We examine payment equity price volatility through Q3 earnings season: https://t.co/OJrL06518T #payments#fintech#stockmarket

In collab with Flagship Advisory Partners, @TNSI has released a new report, "A Guide to Payment Orchestration: Navigating In-Person and Online Payment Complexity". Download the full report: https://t.co/mVm8jKIxSr

#paymentorchestration#merchantpayments#Fintech

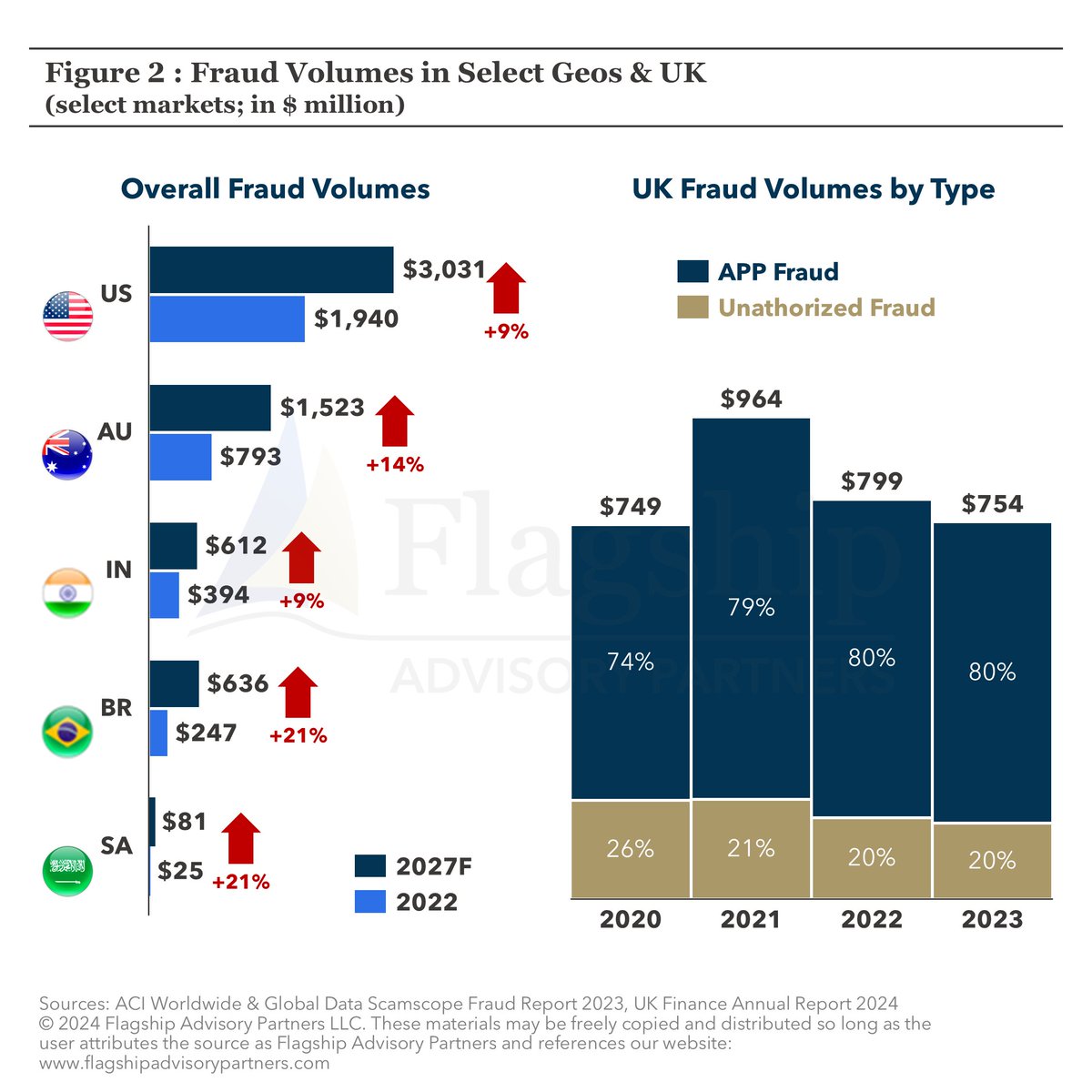

APP fraud is a type of #scam in which victims are tricked into authorizing bank payments to fraudsters. In the UK, APP fraud alone accounts for 80% of all #fraud volumes in 2023: https://t.co/8jSTDh0vqc

#payments#frauddection#scammers

Heading back to the U.S. today after a great week with our @FlagshipAP team in Amsterdam (one of our four global offices). It was a pleasure to be in Amsterdam again (I lived there ten years ago) and see that it continues to offer a unique blend of history, creativity, and technology innovation.

Many payments and fintech trends like the rise of embedded finance, experimentation with digital assets, cash to card conversion, and the (slow) digitization of B2B payments are true around the world, but each market has its own unique characteristics and forces of change. One big event for Europe is the proposed evolution of the Payment Services Directive with PSD3 and the Payment Services Regulation, which will include many new requirements:

• Combat and mitigate payment fraud by requiring merchants and acquirers to share a broader set of data with issuers to combat fraud (data that most issuers probably don’t have the infrastructure to ingest and use properly) and enhancing Strong Customer Authentication rules

• Improve consumer rights, for example by allowing an 8 week “no questions asked” refund period on subscriptions

• Further level the playing field between banks and non-banks by giving non-banks access to all EU payment systems

• Improve the functioning of open banking by, for example, requiring banks to provide customers with a permission dashboard to see and manage which open banking permits they have granted

• Improve the availability of cash in shops and via ATMs by allowing merchants to provide cash services without being regulated

• Further harmonise the EU payment market and strengthen the enforcement of applicable laws by making many of the requirements of PSD2 law across the EU through the PSR

PSD3 and the PSR are not yet finalized but once they are these requirements will likely dominate the attention of European banks and payments companies for the next couple of years.

In the past, major regulatory events in the midst of technology shifts have created white space for disruptive competition: for example, post-financial crisis banking regulation in the early 2010s distracted major US banks and lenders from being able to innovate around the rise of smartphones for several years.

Right now there are big technology shifts happening with generative AI, payments infrastructure (wallets, RTP, etc.), new cloud-based SaaS fintech tools, platformization, and digital assets. European payments companies (and multinational companies operating in Europe, as most do) should be strategic about how they allocate their investment of time and money between regulatory requirements and market-driven innovation.

#payments #fintech

P.s. to everyone in Amsterdam that I wasn’t able to see this time: I’ll be back soon!

The bankruptcy of kevin, once hailed as Lithuania's next unicorn, highlights the challenges of in-store account-to-account payments and the crucial need for robust economic models in the fintech sector 🔗https://t.co/eNkOC03jgc #A2A#payments#Fintech

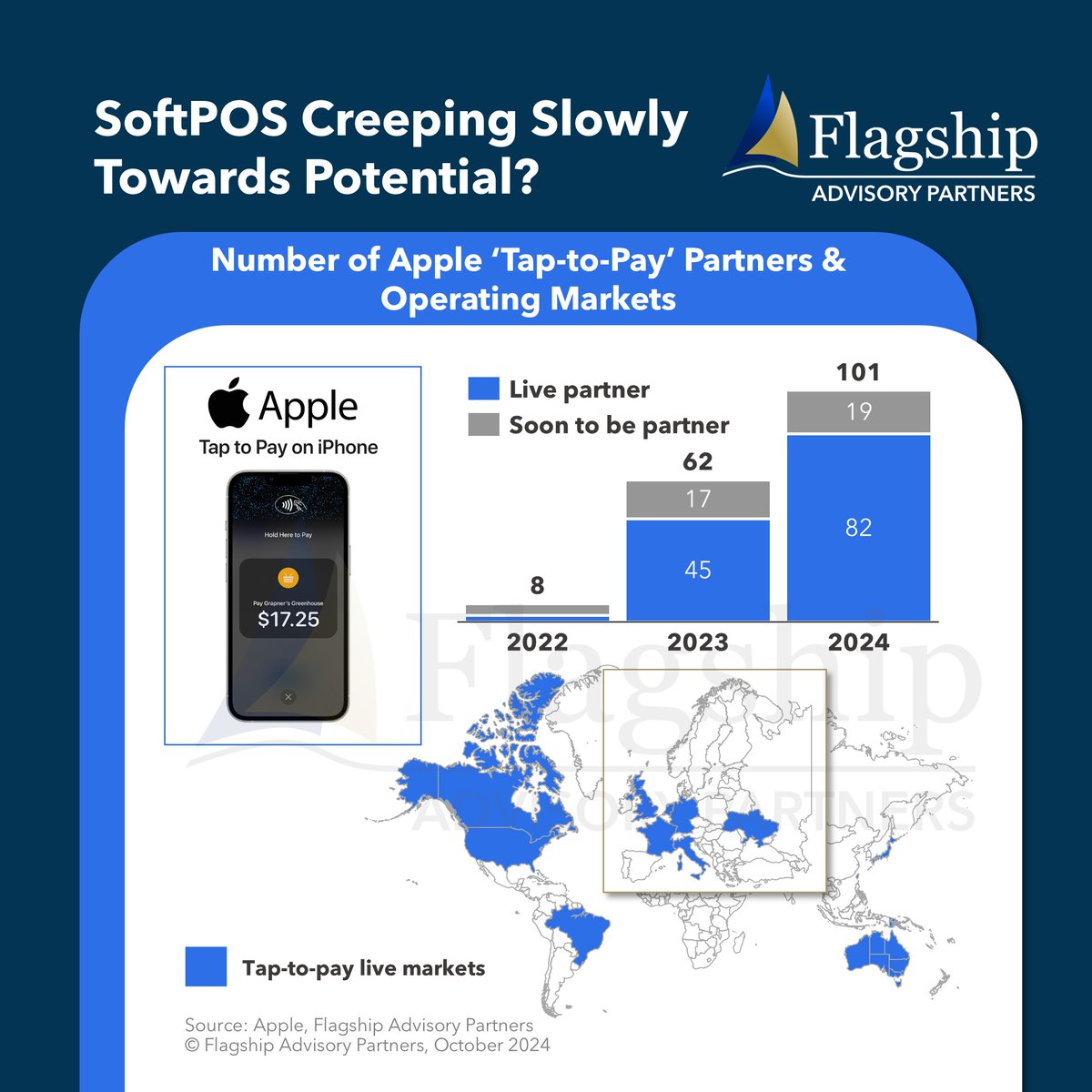

The rollout of Apple’s Tap-to-Pay is an indicator of SoiftPOS’ scaling curve. Apple now has 100+ active or in-flight solution/GTM partners, up 63% from last year (with 3 months remaining in the calendar year) https://t.co/aqHDsn7s95 #apple#taptopay#payments#fintech

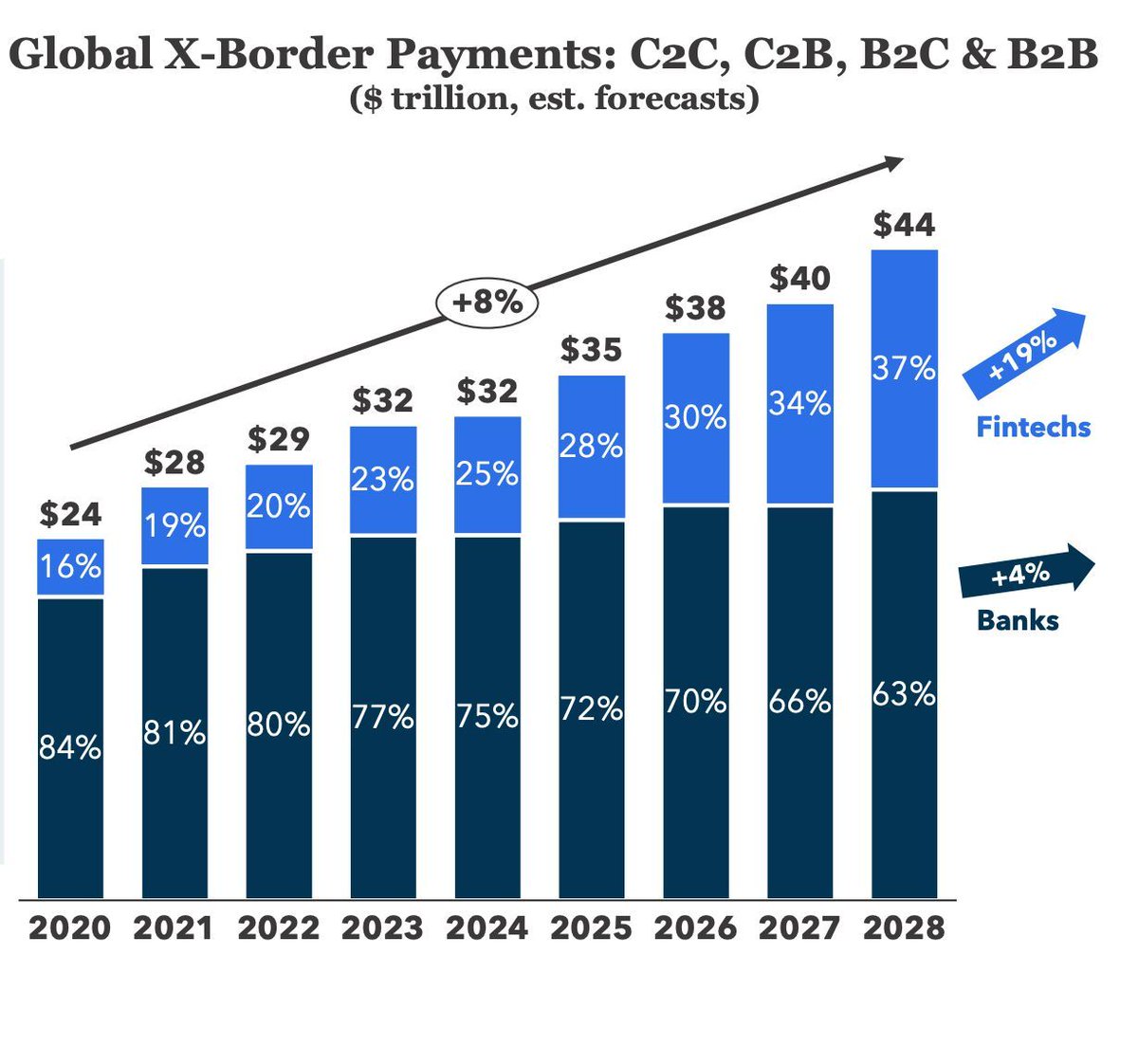

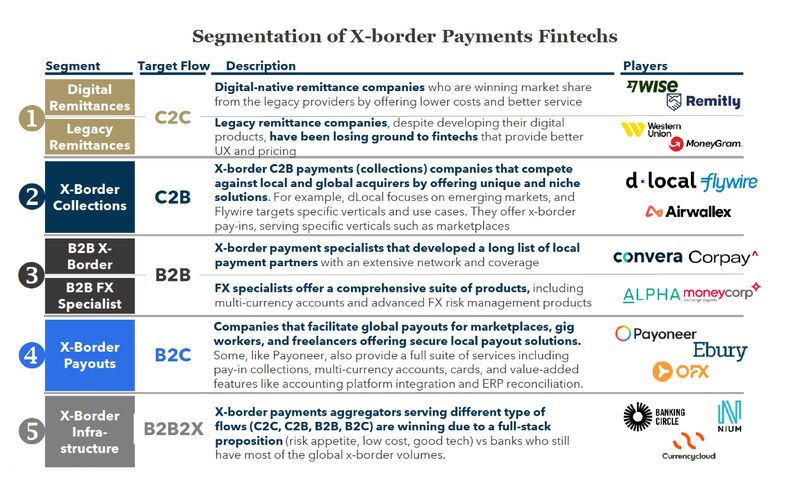

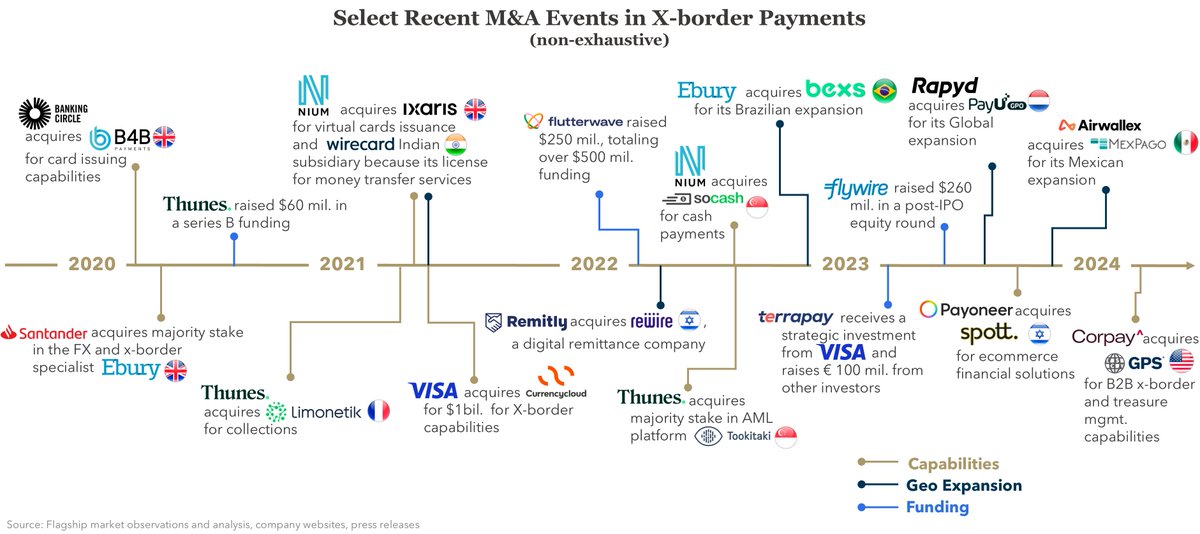

There are strong signs of consolidation evident in the cross-border payments sector. M&A activity in the space has been intense, with several transactions unfolding in recent times https://t.co/rWriSzDyQ2 #crossborder#xborder#payments#fintech#fintechnews

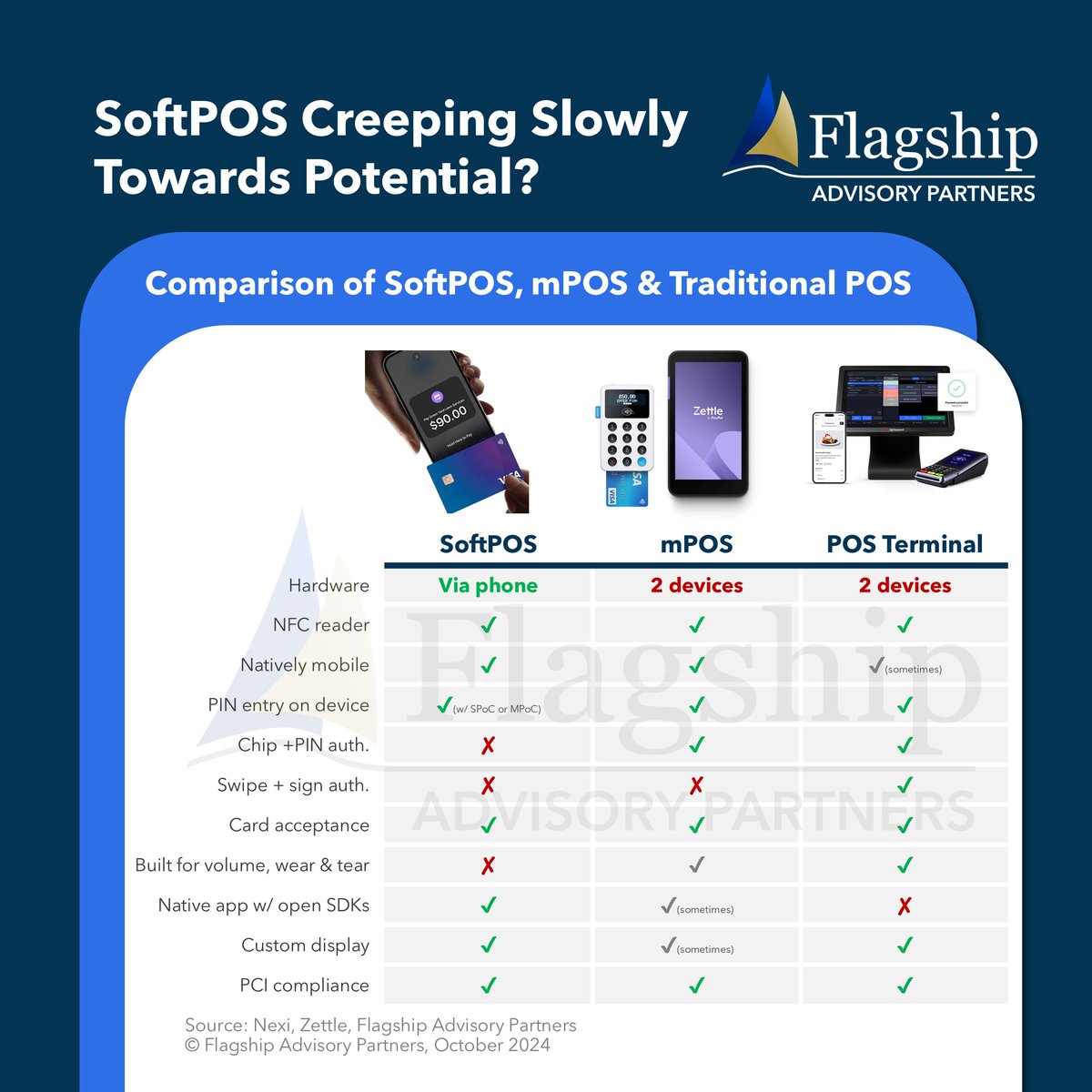

SoftPOS removes the need for a payment device entirely. It relies solely on technology, either native to mobile phones or delivered via a mobile app and corresponding payment host. https://t.co/aqHDsn6Ujx

#payments#softpos#taptopay#fintech#POS#hardware

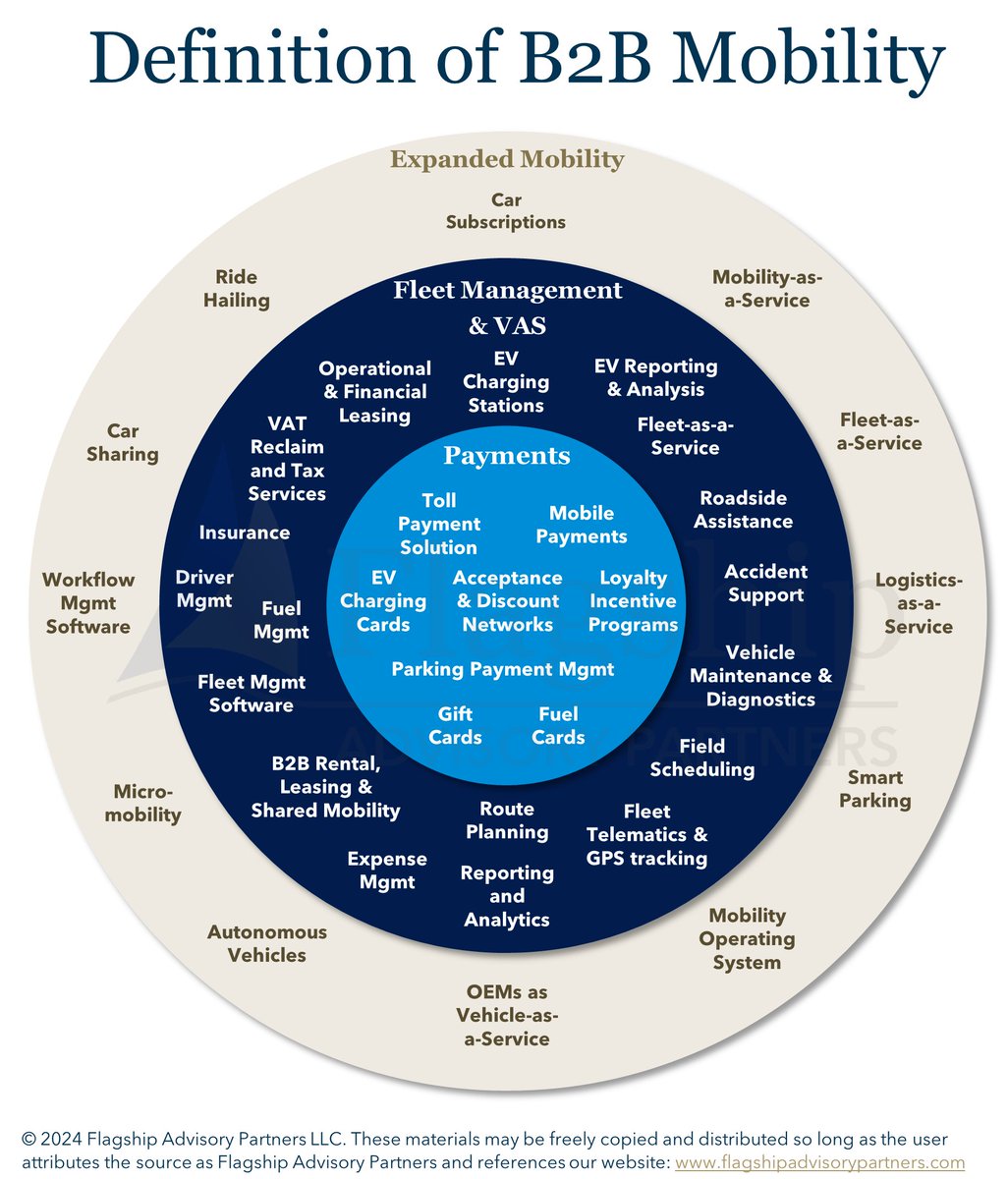

Mobility & fuel payment acceptance tech is a crowded/competitive market that continues to innovate. Industry participants are evolving to solve merchant pain points, with many converging across domains #payments#mobility#B2b#mobility#fuel#EVcharging

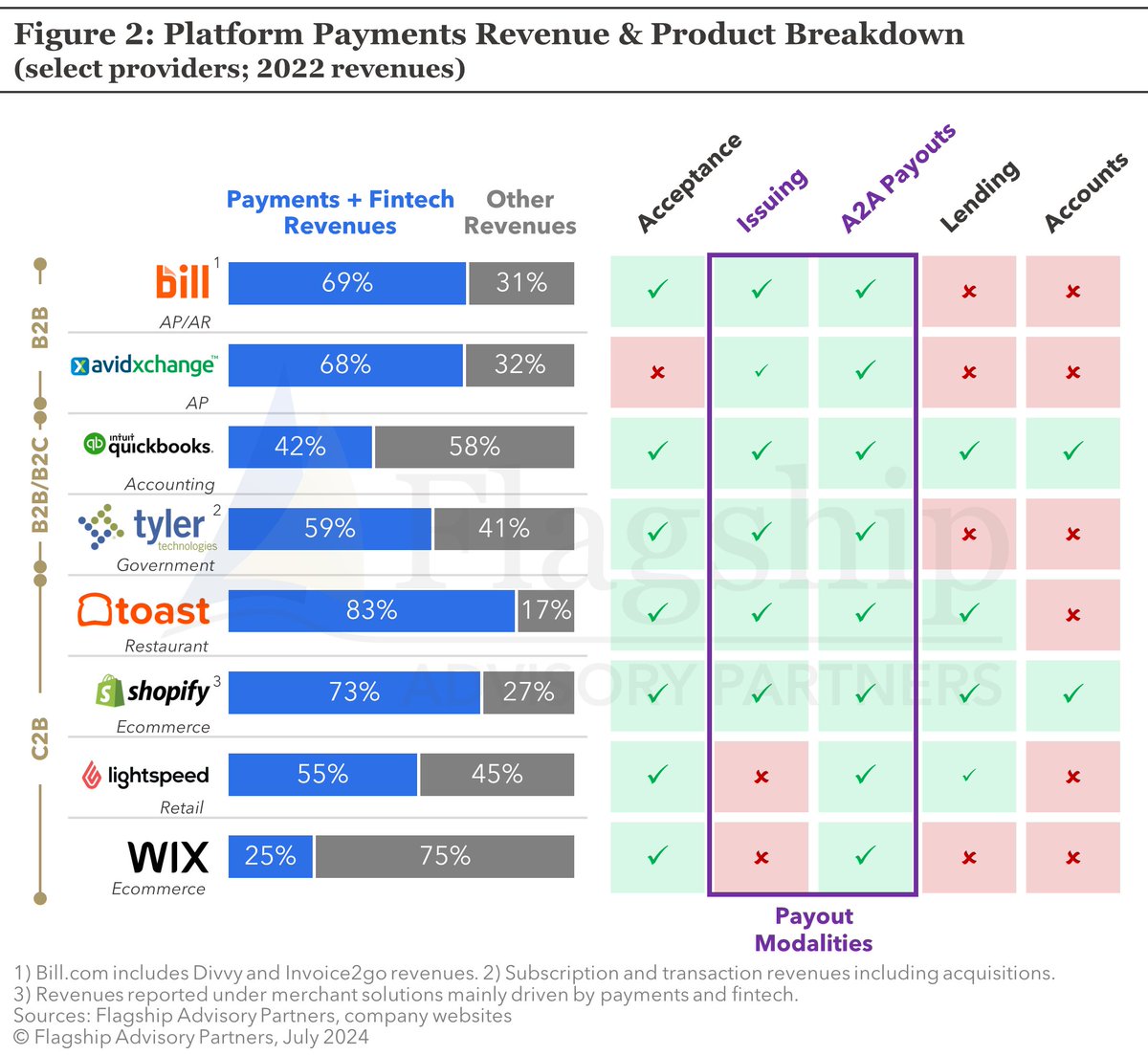

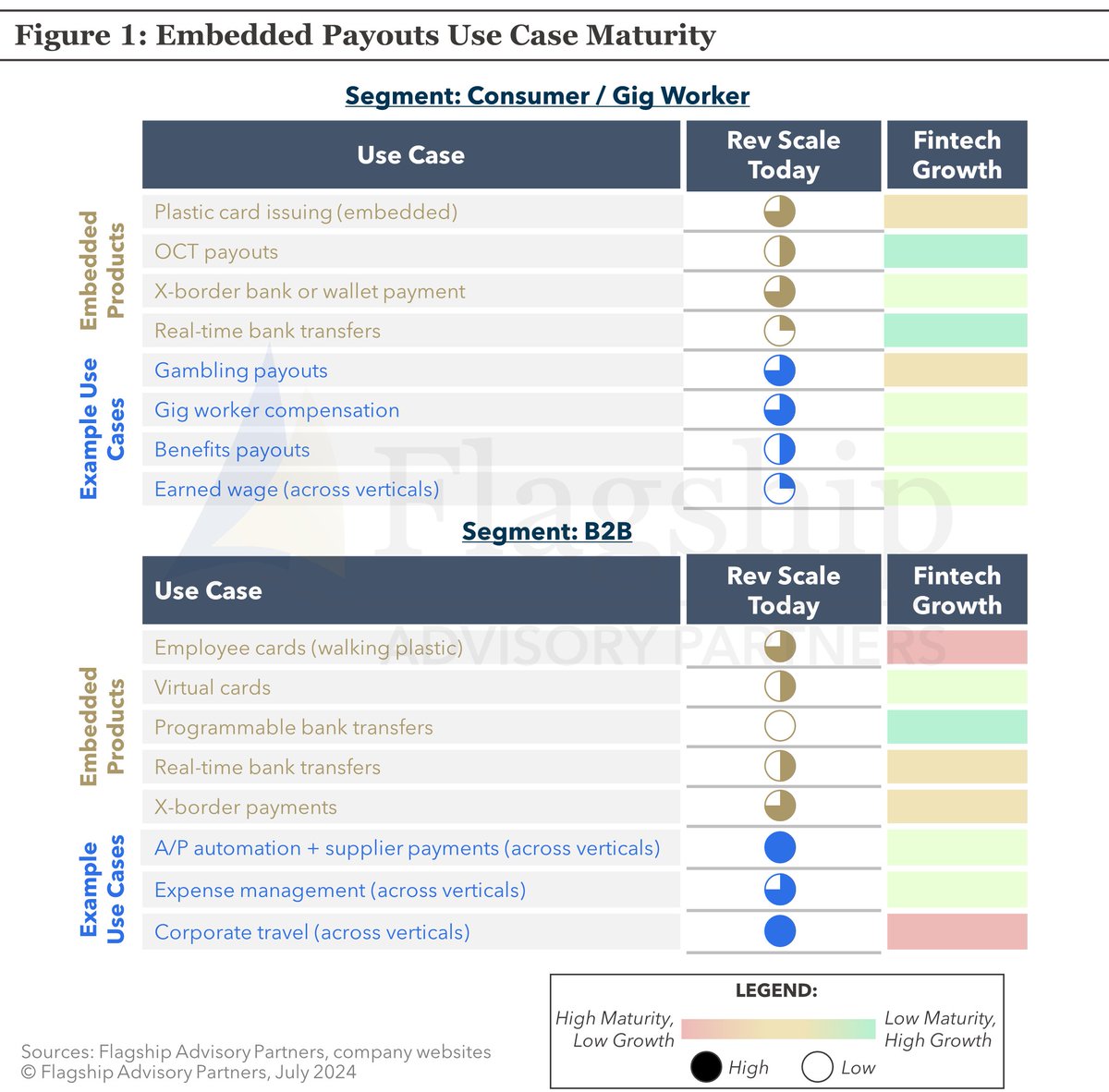

Leading platforms have moved beyond acceptance and have proven the value of other embedded finance product categories with some generating over 50% of revenue from embedded finance: https://t.co/Bu3Sfn5yeP

#payments#saas#embeddedpayments#fintech#payments