Fable eats your Claude Code usage limits in hours - here's how I'm getting around it:

1. Use Fable for planning and to write out your planning doc to disk. I like to use Compound Engineering brainstorm/plan: https://t.co/PC4JUpuPUL

2. In your brainstorming/planning, clear your session (/clear in CC) and do handoffs at appropriate intermediate stages. Install this /handoff skill to automate it: https://t.co/ZyGgjGzazI

3. Install the Codex plugin for Claude Code: https://t.co/TqmkWuPOQ6

4. Either use /ce-work-beta through Compound Engineering (in a new session after doing /handoff), or just tell Fable to delegate work to Codex to save on tokens.

The general principle - use the expensive/better model to decide what to do, and use the cheaper model to do it - is a common technique in agentic deevlopment.

📢 Call for papers! SITE 2026 Session 15: "Causes & Consequences of Misallocation" at Stanford GSB, Aug 31–Sep 1. Theory + empirics welcome.

Deadline: June 15 Submit: https://t.co/d5YRxEyLzl

w/ @TheMichaelBlank@PeteKlenow@sarapfmoreira

1/ Economists: I’ve launched a small project to make AI coding tools actually useful for your day‑to‑day work.

Awesome Econ AI Stuff – a growing collection of reusable AI “skills” for Claude Code, Cursor and Gemini CLI, tailored to empirical + theoretical economics. https://t.co/IdLIprWnr9

📢 News for researchers: Would you like to analyse the housing market in Spain? Thanks to our collaboration with @Registrador_es, you can now carry out your research project at #BELab using #microdata from the Property Registry Statistics (PROP), which contain information on individual property sales and mortgage transactions by municipality. https://t.co/MxuoCbPByx #bdeResearch

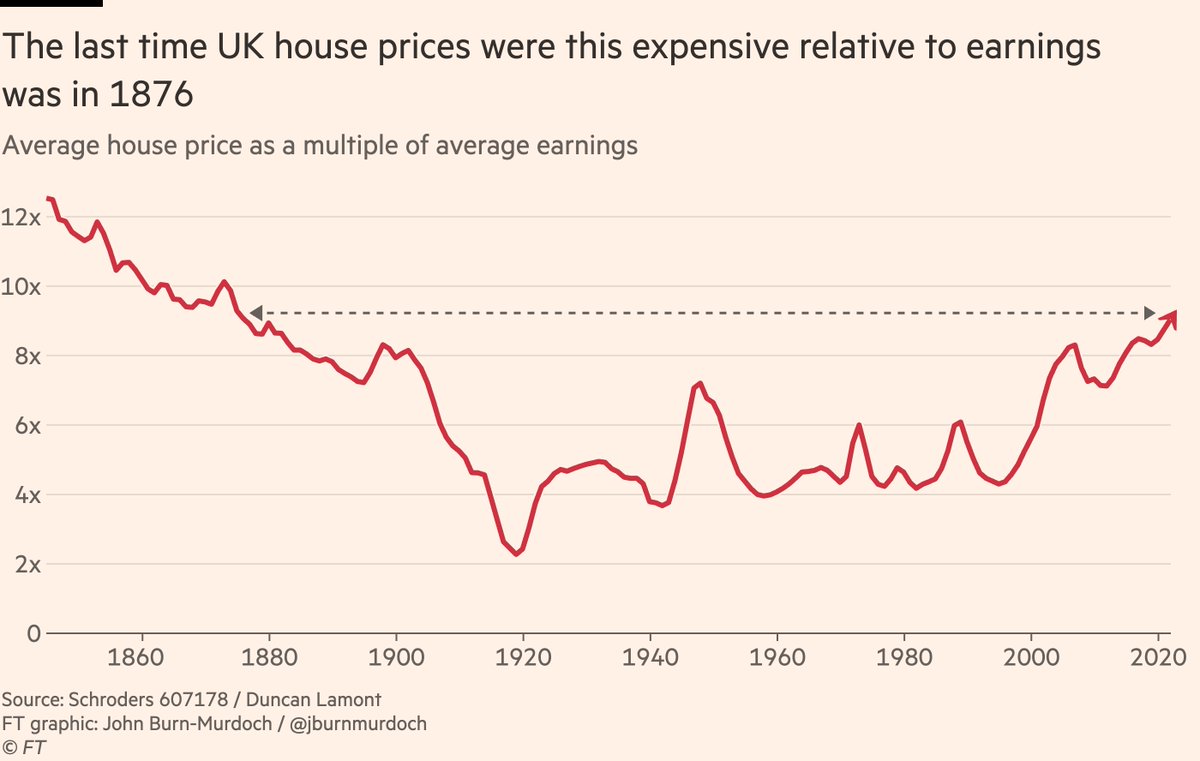

NEW: we don’t reflect enough on how severe the housing crisis is, and how it has completely broken the promise society made to young adults.

The situation is especially severe in the UK, where the last time house prices were this unaffordable was in ... 1876.

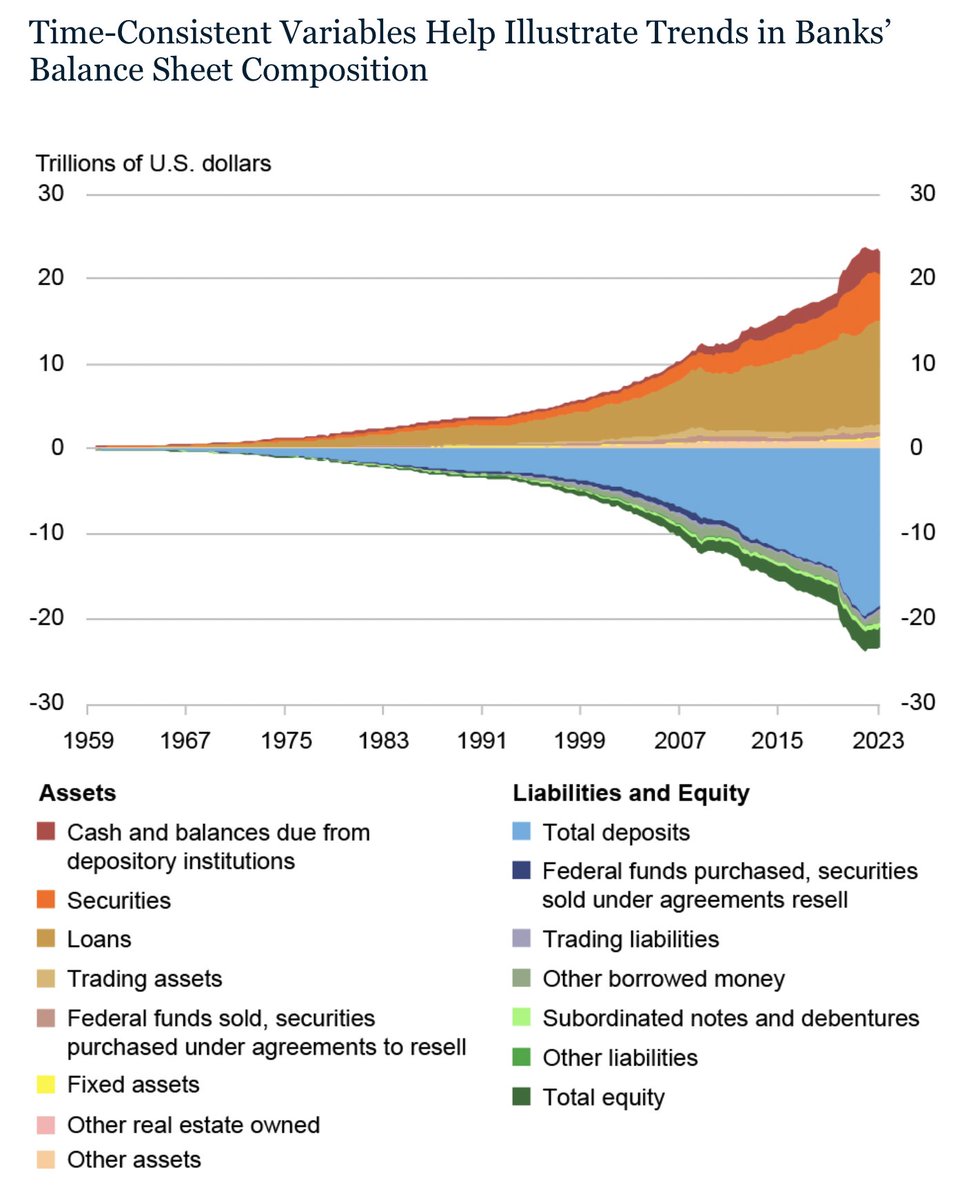

🚨New dataset🚨

Time-consistent balance sheets and income statements for commercial banks in the United States from *1959* to 2025.

https://t.co/OJXCtV7HVK

1/

Banco de España organizes the 1st Workshop on Financial Intermediation on 7 May 2026. Each accepted paper will have a discussant and Prof. Rajkamal Iyer will deliver a keynote speech. Deadline for submission: 2 February 2026. Call for papers: https://t.co/mfeniLN7a2 #bdeResearch

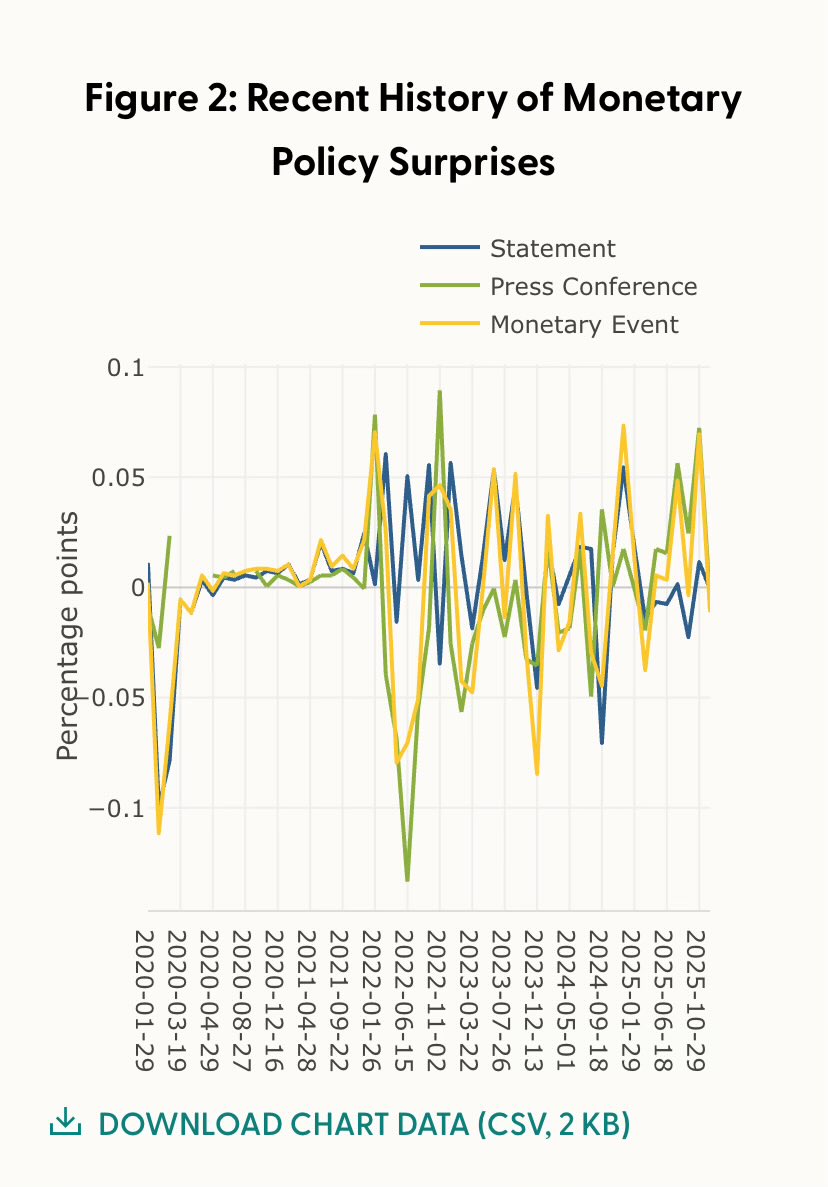

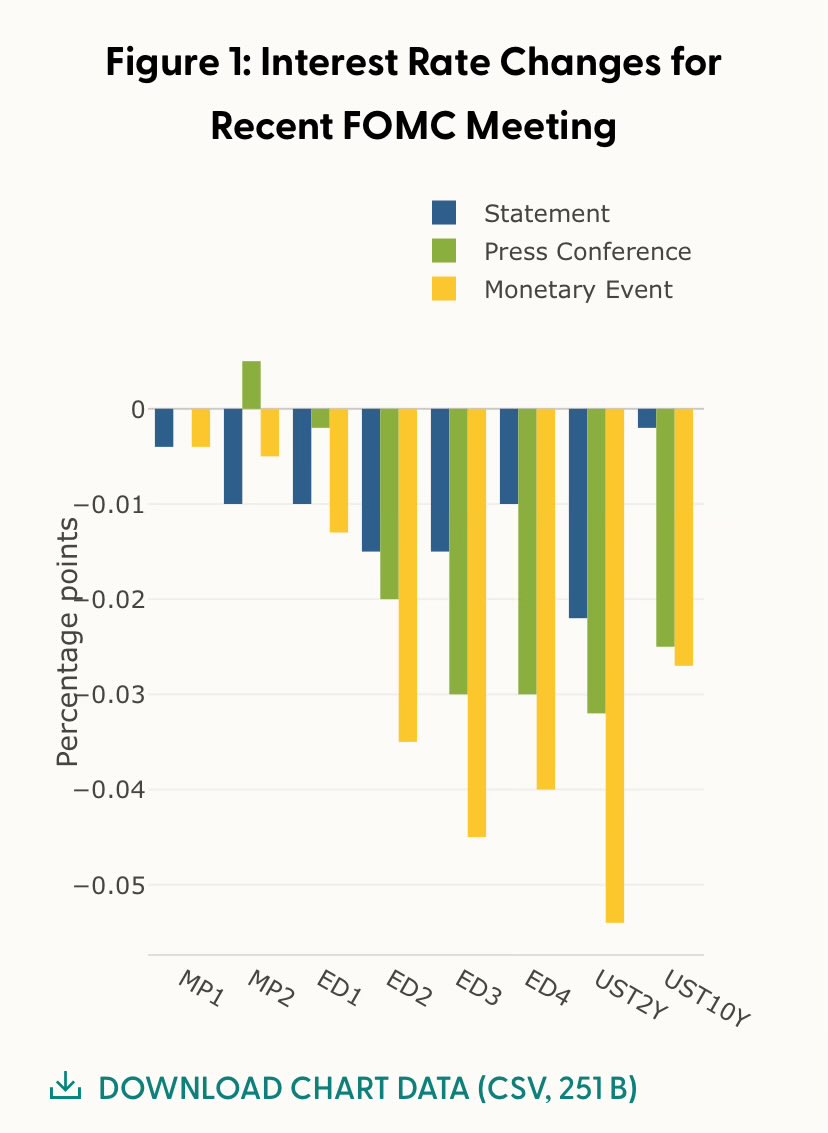

‼️💥 The USMPD is now out 💥‼️

High-frequency monetary policy surprises for all official FOMC comms

👇

https://t.co/2iRXTHDcMD

🔸 Since 1994

🔸 Regularly updated

🔸 FREE!

Paper 👉 https://t.co/iaCd5RK6Wr

w\ @migacosta A. Ajello @michaelbauer_hh & F. Loria

#EconTwitter

📢#CallforPapers - European Summer Symposium in Financial Markets 2026 - Banking and Corporate Finance

ESSFM 2026 will take place in Gerzensee from 27-31 July and is organised by Zhiguo He @Stanford.

Submit a paper or express interest in attending by 15 February.

https://t.co/irvbtEgL4s

1) 📈Hoy publicamos en @elDiarioes una historia que revela cómo 2,5 millones de migrantes no europeos que llegaron en el último boom han acabado en los barrios más pobres del país.

España es hoy más diversa que nunca… pero también más segregada 📊

Submissions are now open for the 19th Meeting of the Portuguese Economic Journal, a super fun conference

When? 3-5 July, 2026, right after the SED!

Where? Aveiro, the Venice of Portugal!

Keynote speakers: S. Bonhomme, @M_De_Nardi, M. Tertilt

More info: https://t.co/AjpaqX2tAV

Hey #EconTwitter I am on the #EconJobMarket this year and I study causal inference in macroeconomics.

My Job Market Paper introduces a novel methodology to study how shocks affect the whole distribution of economic outcomes.

🧵 below

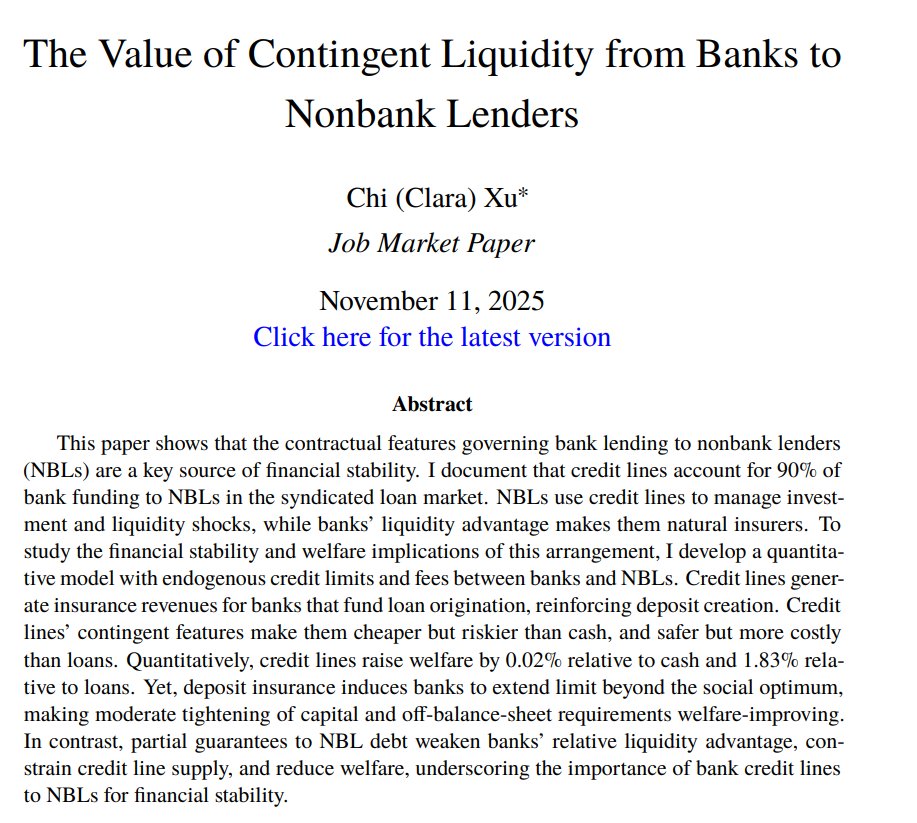

I have an excellent student Clara Xu on the market this year, whose JMP analyzes how nonbank lenders finance themselves with credit lines from banks. After documenting how empirically common this relationship is, she shows in a GE/macro model that it is welfare improving.

My excellent student Luigi Falasconi @Luigi_Fala is on the PhD job market. His JMP shows that investors' beliefs that banks are less likely to be bailed out after 2008 raised their borrowing costs. This higher borrowing cost made banks less able to provide risky loans.

I’m excited to share my JMP: “The Granular Drag on Growth”

Key insight: firm granularity can dampen the reallocation engine that drives productivity growth.

Want to know more? Read the thread below or download the paper ⬇️

https://t.co/Nj3PuRAqxG

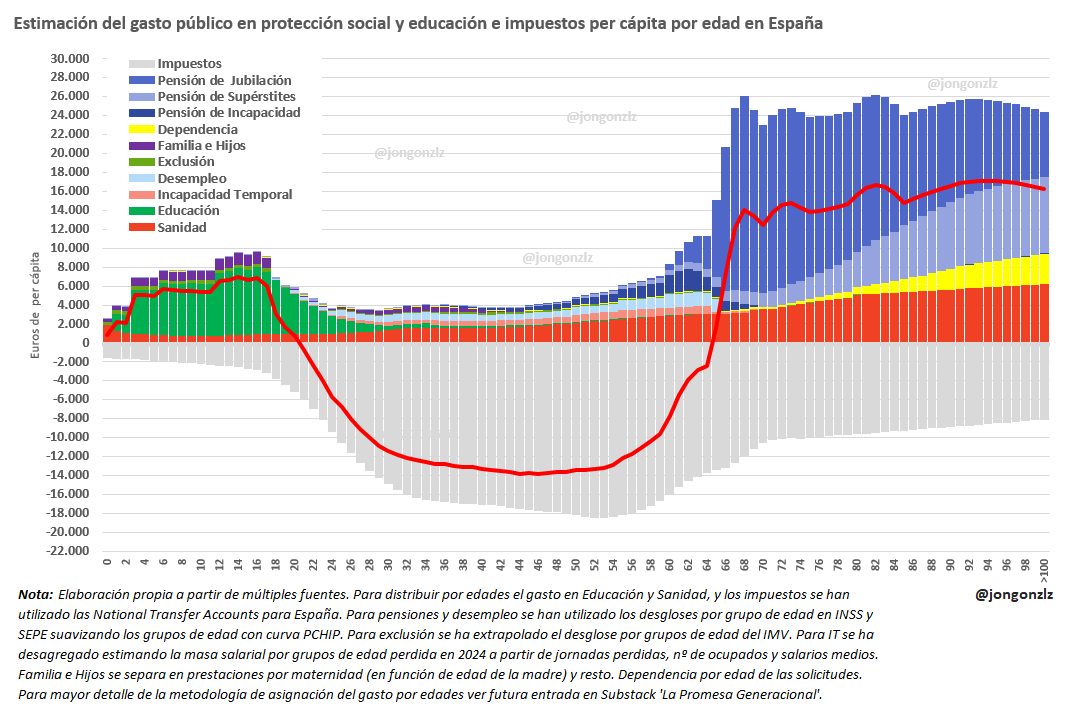

A coauthor of mine, @Jongonzlz, just computed age-indexed per-capita social spending and taxes for Spain. The figure below shows the results (any LLM can translate the axes if needed).

Why should you care? Because the broad patterns apply to most Western countries.

This is a quick calculation, and some details could be refined, but the main ideas are clear:

1️⃣ Above zero on the x-axis you see per-capita social spending: pensions, disability, survivor benefits, etc.

2️⃣ Below zero you have per-capita taxes.

3️⃣ The red line is the difference. It highlights the large transfers from people in their 30s–60s toward older and younger groups, a natural feature of pay-as-you-go systems like Spain’s.

4️⃣ The red line is not the net fiscal position of an individual: you must add other public spending (defense, police, general administration, etc.).

5️⃣ Discounting the red line at a 2% real interest rate (roughly in line with long-run debt-financing costs), the government’s net present value for the average individual is around €60,702.

6️⃣ Adding each person’s per-capita share of the rest of government spending yields a net present value of about €–21,375. This is one way to illustrate the long-run pressure on the welfare state.

7️⃣ This average figure naturally reflects a wide distribution: individuals with different educational backgrounds, skills, and earning trajectories contribute very differently over their lifetimes. Some have strongly positive fiscal contributions; others have lower or negative ones. This is normal in any redistributive welfare state.

If we want to think seriously about the future of the welfare state, we need some basic facts:

1️⃣ Who pays into the system and who receives from it.

2️⃣ How net transfers evolve over the life cycle.

3️⃣ Whether this pattern is the one we want.

4️⃣ Whether this pattern is sustainable.

These fiscal patterns also matter for thinking about how demographic change interacts with the sustainability of the system.

People may differ in their answers to 1️⃣–4️⃣, but it helps to start with the data.

The original post:

https://t.co/8pHK0sWrlw

🚨 𝐉𝐨𝐛 𝐌𝐚𝐫𝐤𝐞𝐭 𝐏𝐚𝐩𝐞𝐫 🚨

"Financial Regulation, Pension Investment, and Economic Growth"

I ask: How does regulation that limits risk-taking in the financial sector affect economic growth?

Link: https://t.co/gashy5X4tI (1/16)