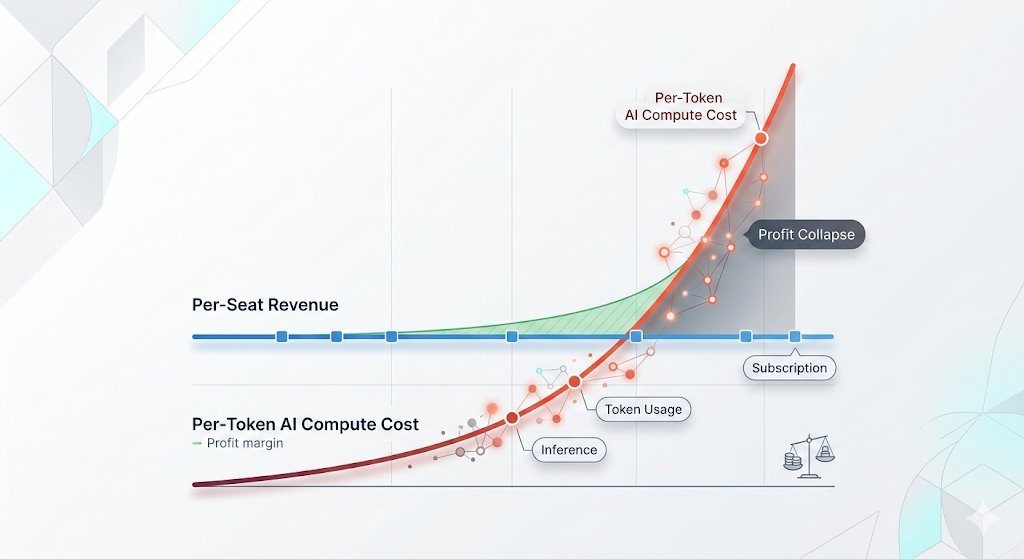

🦔Fortune published a piece this afternoon connecting Microsoft and Uber's AI cost overruns to token economics, with a headline that lands hard: "Microsoft reports are exposing AI's real cost problem: Using the tech is more expensive than paying human employees." Underneath those headlines, the unit economics tell the story. OpenAI is projected to lose $14 billion in 2026, spending roughly $2 for every dollar of revenue it brings in. Anthropic is in a similar position with break-even not projected until 2028. GPU rental prices for Nvidia's newest Blackwell chips jumped 48% in just two months. OpenAI's response was to close a $122 billion private funding round at an $852 billion valuation, the largest in history.

My Take

The token pricing story is really an IPO timing story. OpenAI, Anthropic, and xAI all need to go public in the next 18 to 24 months because the private market cannot keep absorbing burn rates like these indefinitely. Public markets do not accept "we will figure it out" as a line item on an S-1, they require disclosed unit economics with a credible path to profitability and a date attached. That deadline is why the price increases are happening now rather than next year. The labs need to show declining loss curves before the filings hit, and that means enterprise customers have to start covering more of the actual cost regardless of whether the productivity math holds on their end.

Every token bought over the last two years was effectively subsidized below cost by venture capital and hyperscaler cross-subsidies, and that subsidy has a hard deadline. Uber publicly admitted burning through its entire 2026 AI budget in four months, and CFOs at major enterprises are starting to flag the same pressure. The labs cannot keep losing $2 per dollar of revenue once they file public statements, so the cost transfer to customers accelerates from here. For investors, the question is not whether these companies are valuable. They clearly are. The question is who absorbs the difference between what enterprises can budget and what the models actually consume between now and 2028, and right now the answer is the hyperscalers funding the buildout. That is why I have been watching Microsoft and Amazon capex commentary more closely than the lab announcements themselves.

Hedgie🤗

Link: https://t.co/S2oIgUSijV

🦔Microsoft canceled its internal Claude Code licenses this week after token-based billing made the cost untenable, even for a company with effectively infinite cloud resources. Uber's CTO sent an internal memo warning the company burned through its entire 2026 AI budget in just four months. American AI software prices have jumped 20% to 37%, and GitHub (owned by Microsoft) is dropping flat-rate plans for usage-based billing across its products.

My Take

The AI subsidy era is ending in real time. The same company that put $13 billion into OpenAI and built the Azure infrastructure powering most of Anthropic's compute just looked at the bill from a competitor's coding tool and decided it was not worth paying. That is not a productivity failure on Anthropic's end. Token-based pricing is forcing every enterprise customer to confront the actual cost of running these models at scale, and the number turns out to be far higher than the flat-rate experiments suggested.

This ties directly to my Gemini Flash post yesterday. Anthropic, OpenAI, and Google all raised effective prices in the last six months. Enterprises that built workflows assuming AI costs would keep falling are now watching annual budgets evaporate in months. Two outcomes look likely from here. Either enterprises scale back AI usage to fit budgets, which slows the revenue ramp the labs need to justify their valuations ahead of IPOs, or the labs cut prices and absorb the losses, which makes the unit economics worse at exactly the wrong moment. Both paths land in the same place, the numbers stop working, and somebody has to take the writedown.

Hedgie🤗

OpenAI has been tracking very high demand on both the consumer and enterprise front and we strongly disagree with the notion that growth is weakening. We would be buyers of AI driven tech stocks this am and in particular Oracle on this way overreaction to this WSJ report.🎯🏆🐂

Exclusive: OpenAI recently missed its own targets for new users and revenue, stumbles that have raised concern among some company leaders about whether it will be able to support its spending on data centers https://t.co/rVSpL0KJkc

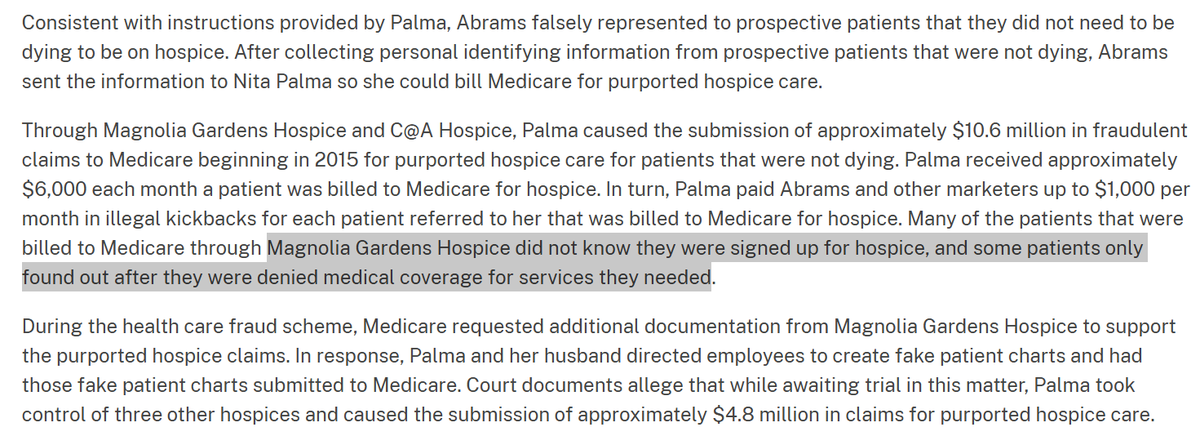

Quite the detail in this hospice fraud case.

Woman in her 70s operates multiple crooked hospice agencies *while on bail awaiting trial for previous hospice fraud.*🤯

Can they just hire fraud experts to deal with this issue? Admit you're over your head and do it right.

...

Also, when is the moratorium on new hospice numbers taking effect?

Look out for unintended consequences, when it comes to CMS you have to.

But, generally speaking, this is an acknowledgment that internal policies relating to issuance and management of enrolled suppliers is not where it needs to be and they, CMS, need to fix.

“There’s no cost of goods sold, there’s no inventory, there’s no payroll,” he said. “No one works in the place – it’s empty – but they generate millions of dollars of fake bills.”

🔨 nailed it...finally addressing at root cause, supplier #s issued by CMS

https://t.co/mAaqSENAQ2