Options 101: The Foundation

Topics covered:

1.) What is a derivative?

2.) What is an option?

3.) Options example ( airline industry )

4.) Options example ( $BTC )

5.) American vs European options

BTC options positioning remains concentrated across a relatively narrow range of strikes, with negative gamma continuing to cluster below spot, primarily around the $50k-$60k region. Relative to previous sessions, downside exposure has become more localized, while positive gamma has shifted higher and is now concentrated across the $65k-$73k range.

The largest positive gamma concentrations are centered near $65k, $67k, $69k, and $71k, with additional positioning extending toward $75k-$81k. Rather than a single dominant gamma wall, the current profile reflects a sequence of medium sized positive gamma clusters, resulting in a more distributed dealer positioning profile above spot.

The structure continues to be driven primarily by July, August, and September expirations, with comparatively limited front week positioning. Medium term maturities therefore account for the majority of dealer gamma exposure, while longer dated expirations remain relatively lightly positioned.

Overall, the current GEX profile is characterized by concentrated downside gamma below the prevailing trading range and a broad positive gamma corridor extending from the mid $60k into the low $80k region. These strike clusters continue to represent the largest concentrations of dealer positioning and remain the primary areas shaping options market structure.

Important to note that these do not include IBIT data

The market has begun to pull back, and the rally that began in July has turned into a seesaw battle over the past week. Implied volatility (IV) across major maturities has dropped significantly, indicating that the market as a whole expects low volatility.

Looking at the IV trend over the past three months, we can see that a sharp decline in early June briefly drove IV higher. At this stage, IV acts as a “fear index”—the faster the market falls, the higher IV rises; once the market stops falling, IV drops rapidly. This is highly correlated with the level of market panic.

The rising share of put trading volume and persistently low IV are also typical characteristics of a bear market. This situation will not be broken by a single bullish candle. We can say with certainty that now is a good time to sell calls, until two strong bullish candles bring this trend to an end.

July 10 Options Data

23,000 BTC options expired, with a put-call ratio of 0.97, a maximum pain point of $62,000, and a notional value of $1.5 billion.

140,000 ETH options expired, with a put-call ratio of 1.26, a maximum pain point of $1,700, and a notional value of $250 million.

Bitcoin remained range-bound above 60K this week, with relatively calm market conditions. Key options data shows that 7% of options expired this week. The GEX distributions for BTC and ETH were concentrated at 64K and 1,750, respectively, with both showing a significant accumulation of call options. The proportion of large call trades increased notably this week, primarily consisting of selling short-term, shallow out-of-the-money calls, indicating a consensus among institutions that the market lacks upward momentum.

ETH’s Put-Call Ratio reached 1.26 this week, with put options maintaining an extremely high proportion for two consecutive weeks—a relatively unusual phenomenon. Based on the option distribution, this is primarily due to the expiration of deeply out-of-the-money protective positions below $1,500.

U.S. and South Korean stocks have also been correcting recently, and the overall market remains relatively subdued. We are adopting a wait-and-see approach, monitoring the situation for changes.

BTC's 25 delta skew has stabilized across the curve following the sharp repricing observed through June, although downside protection continues to command a premium across all major maturities. Current readings stand at -6.4% (1D), -6.7% (7D), and -7.0% (1M), indicating that front end hedging demand has moderated from recent extremes.

The term structure has become noticeably flatter, with 3M (-6.6%), 6M (-5.6%), and 1Y (-5.3%) skew remaining comparatively close to front end levels. The compression between short and long dated tenors suggests a more balanced distribution of downside premium across the curve than was observed earlier in the quarter.

Puts continue to trade at a premium to calls across all major expirations, although the magnitude of that premium has become more uniform. Relative to previous weeks, downside risk pricing is no longer concentrated exclusively in front end maturities, with medium term expirations accounting for a larger share of overall skew.

The current skew profile reflects a more normalized term structure while maintaining a persistent downside bias in options pricing. Compared with the sharp front end dislocations seen earlier in June, risk pricing is now more evenly distributed across maturities, indicating a less fragmented options market.

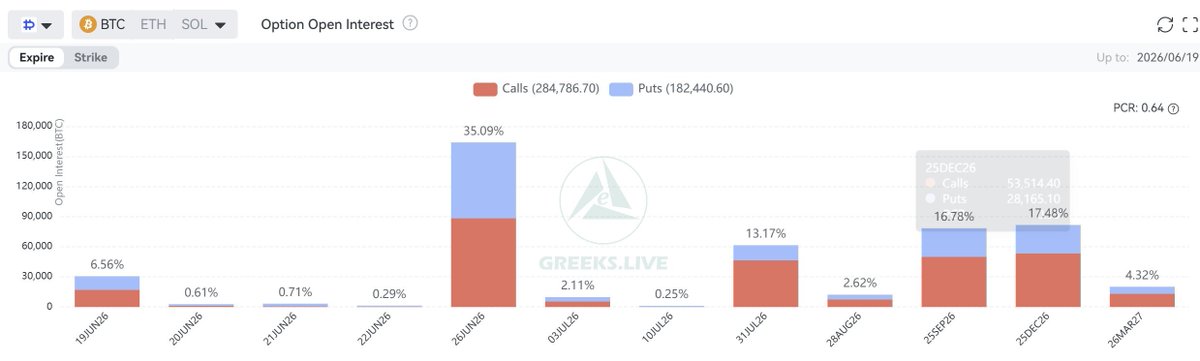

As can be seen from the distribution of open interest, positions across all maturities through the end of this month are very low, totaling only about 15%—a sign of extremely low market activity.

On the other hand, GEX is concentrated in the 60K put and 63K call options, which happen to be the two most recent upper and lower price limits of the trading range. In such an inactive market, prices are likely to follow external markets closely, so it will be particularly important to monitor recent price movements in U.S. stocks and commodities.

BTC options positioning remains concentrated around a relatively narrow range of strikes, with negative gamma continuing to cluster below spot, primarily between $50k and $60k. Relative to previous sessions, downside exposure has become more localized, while positive gamma remains distributed across the mid-$60k to low-$80k region.

The largest positive gamma concentrations are centered around $66k-$72k, with additional positioning extending toward $78k-$82k. Rather than a single dominant gamma wall, the current profile reflects a series of medium-sized positive gamma clusters across higher strikes, resulting in a more gradual distribution of dealer exposure above spot.

The resulting positioning profile continues to be defined by medium-term expirations, with the largest concentrations of dealer gamma exposure centered between the mid-$60k and low-$80k region.

Important to note that these do not include IBIT data

July 3 Options Data

31,000 BTC options expired, with a put-call ratio of 0.7, a maximum pain point of $61,000, and a notional value of $1.9 billion.

135,000 ETH options expired, with a put-call ratio of 1.29, a maximum pain point of $1,650, and a notional value of $230 million.

Bitcoin reclaimed the key psychological level of 60K again this week. From a long-term perspective, the downtrend has not yet ended. Selling pressure from MicroStrategy and ETFs has completely shifted market consensus—the largest buyers have turned into sellers, which is a signal of an accelerating decline in any market transition from bull to bear.

Looking at key options data, over 8% of options expired this week, with BTC GEX concentrated around 60K and ETH GEX concentrated around 1,700. ETH’s Put-Call Ratio reached 1.29 this week, indicating that put options have reached an extremely high proportion, reflecting surging demand for safe-haven assets. Market concerns about another downturn are evident.

The recent focus has been on the U.S. stock market, while the crypto space’s hot topics revolve around the tokenization of U.S. stocks. It will be a long time before the buzz around AI and semiconductors shifts back to crypto. Against this backdrop, the outlook for crypto in Q3 remains bleak.

Selling calls to collect premiums during a bear market is a good way to generate a steady cash flow. Although implied volatility (IV) is relatively low in a bear market, the probability of deep out-of-the-money options being exercised is also very low, so the drawdown from selling calls to collect premiums will be minimal.

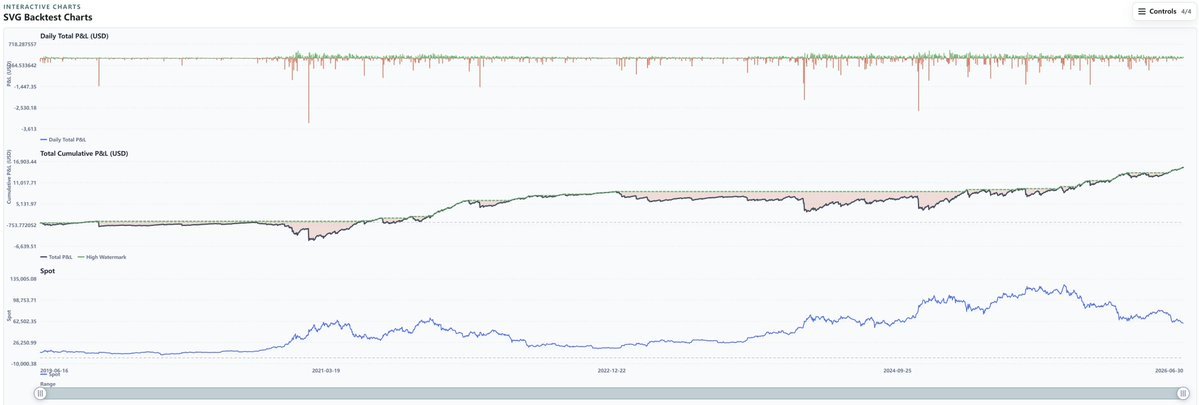

Today, I pulled data from my backtesting system covering the two bull and bear markets since 2019. We can see that:

1) In the late stages of bear markets prior to 2021, selling out-of-the-money call options with a 0.1 Delta for the current week generally resulted in a break-even outcome.

2) During the 2021 bull market, drawdowns occurred during periods of rapid price surges, but thanks to the high IV typical of bull markets, profits were recouped quickly.

3) During the 2022 bear market, this strategy demonstrated exceptionally strong profitability with very low drawdowns.

4) During the slow bull market from 2023 to 2025, this strategy faced its greatest test. Since the bull market rallies during this period were often concentrated within very short time frames, the strategy encountered multiple significant drawdowns. However, thanks to the profits accumulated in 2022, it ultimately maintained a positive return.

5) As the market turned from a bull to a bear market in 2025, this strategy began to replicate the explosive performance seen in 2022.

Looking back at these two bull markets, although there were many differences in market conditions, the overall cyclical nature is evident when observed through the lens of advanced tools like options. As long as this strategy continues to generate profits, the bear market has not yet ended; now is the perfect time to engage in this “sell calls” strategy.

Despite a mild recovery BTC's 25 delta skew remains heavily skewed toward downside protection, with front end maturities continuing to trade near the most negative levels of the quarter. Current readings stand at -11.0% (1D), -11.0% (7D), and -8.0% (1M), highlighting persistent demand for near term downside hedges.

The weakness has broadened across the curve, with 3M (-7.4%) and 6M (-6.3%) skew also trending lower, although longer dated tenors remain materially less negative than the front end. As a result, downside premium continues to be concentrated in short dated expirations while extending further into medium term maturities.

Puts continue to trade at a meaningful premium to calls across all major tenors. The current term structure reflects a sustained preference for downside protection, with the steepest risk premium remaining concentrated in front end options.

Compared with longer dated maturities, short dated skew continues to account for the majority of downside premium embedded in BTC options pricing, indicating that options positioning remains primarily driven by near-term risk management rather than a broad repricing of longer-term expectations.

BTC options positioning has become increasingly concentrated around the low-$60k to low-$70k region. The largest negative gamma exposure remains clustered between $50k and $60k, while positive gamma is distributed primarily across the $62k-$81k range, with the most notable concentrations near $63k, $66k, $69k, $72k, $75k, and $80k.

The current structure is largely driven by July, August, and September expirations, with comparatively limited front-week positioning. Relative to earlier sessions, gamma exposure has become more balanced around spot, while the majority of positive gamma remains concentrated in medium-term maturities.

The distribution of gamma suggests a more gradual transition from negative to positive exposure across the strike curve rather than a single dominant gamma wall. Dealer positioning is therefore spread across multiple higher strikes, while downside gamma remains concentrated below the current trading range.

Important to note that these do not include IBIT data

June 26 Options Data

150,000 BTC options expired, with a put-call ratio of 0.63, a maxpain point of $70,000, and a notional value of $9 billion.

1 million ETH options expired, with a put-call ratio of 0.5, a maxpain point of $2,000, and a notional value of $1.57 billion.

Bitcoin tested the key psychological level of 60K twice this month—once at the beginning and once at the end. Although it briefly rebounded to 67K mid-month, it remains in a clear downtrend. This month, selling pressure from MicroStrategy and ETFs completely shifted market sentiment, turning the largest buyers into sellers—a signal that typically accelerates declines during any market transition from bull to bear. This week marks the quarterly settlement. Compared to previous quarterly settlement volumes, BTC and ETH are at only 70% of the typical quarterly level, indicating a very subdued market.

Looking at key options data, over 30% of options expire this week. The BTC GEX distribution is concentrated around 60K, while the ETH GEX distribution is concentrated around 1,500 and 1,550. As these positions expire, the released margin will impact IV to some extent. However, since the price has once again fallen below 60K this week, demand for bulk puts is strong, Skew’s negative skew has intensified, and market risk aversion is high; IV may decline further once the market stabilizes.

MicroStrategy’s coin sales and the significant discount have dealt a severe blow to market confidence. Capital is flowing heavily into popular AI stocks, and even tech giants like Apple are failing to gain market recognition—the crypto market still has a long way to go before it can turn around.

BTC's 25 delta skew continues to deteriorate across short-dated maturities, with 1D, 7D, and 1M tenors now trading near the most negative levels recorded in recent months. The repricing has been concentrated in the front end of the curve, while longer-dated maturities have remained comparatively stable.

The resulting term structure has become increasingly steep, with downside premium concentrated in near-term expirations. Current readings of -10.7% (1D), -11.3% (7D), and -9.6% (1M) compare with -6.0% (6M) and -5.0% (1Y), highlighting the widening gap between short- and long-dated risk pricing.

Puts continue to command a meaningful premium over calls across all major tenors. The current skew configuration reflects persistent demand for near-term downside protection, while longer-dated options pricing remains comparatively anchored.

BTC options positioning remains concentrated around a limited number of key strikes. Negative gamma exposure is centered between $60k and $64k, while positive gamma is distributed across the $67k-$82k range, with notable concentrations near $67k, $71k, $75k, and $80k

The current structure is primarily driven by June, July, and September expirations, indicating that medium-term maturities continue to account for the majority of dealer gamma exposure. Relative to previous sessions, positive gamma positioning remains broadly distributed across higher strikes, while downside exposure remains concentrated near the low-$60k region.

Important to note that these do not include IBIT data

June 19 Options Data

31,000 BTC options expired, with a put-call ratio of 0.78, a maximum pain point of $65,000, and a notional value of $1.9 billion.

138,000 ETH options expired, with a put-call ratio of 1.03, a maximum pain point of $1,725, and a notional value of $230 million.

Although Bitcoin rebounded to 67K at one point this week, it clearly lacked momentum. The market struggled to absorb institutional selling pressure from MicroStrategy and ETFs, and the price fell below 63K ahead of this week’s expiration. Both BTC and ETH traded below their “maximum pain” levels, fluctuating around those points.

Looking at key options data, 6.5% of options expired this week—lower than last week but roughly in line with the recent average. Next week marks the quarterly settlement, with approximately 15% of positions set to expire. As prices stabilize, GEX is distributed between 60K and 63K, with the majority set to expire this week and next. The margin released at that time will significantly impact IV. Skew remains relatively stable but still shows a negative skew, indicating that the market remains braced for a downturn.

MicroStrategy’s coin sales and the deep discounts on its options have dealt a severe blow to market confidence, making capital inflows even more difficult, and overall market sentiment remains subdued.

The current GEX distribution is consistent with a market structure in which:

The $60,000 strike functions as a critical threshold. A sustained breach below this level would shift dealer hedging flows from stabilizing to directionally reinforcing, increasing the probability of an accelerated move lower.

The $70,000–$82,000 levels acts as a positive gamma range. Within this range, dealer activity is expected to provide a natural dampening effect on volatility, compressing the magnitude of intraday moves absent a material catalyst.

Medium term expiration dominance reduces tail risk from gamma unwinds. The absence of significant front week concentration limits near term pin risk and reduces the likelihood of sharp post expiration repositioning.

We are pleased to announce that the SABR Backtest system is now live in the production environment. This marks a major upgrade to the backtesting system. In the new system, you can flexibly adjust strategy settings, and Gezhi provides seven years of options data dating back to 2019 for your backtesting needs.

This is part of Gezhi’s intelligent upgrade initiative, which involves making advanced internal tools available to the public. In the future, we will also open API functionality and enable direct integration with Vibe Coding—stay tuned.

Try it now at https://t.co/7lON9Ulzoa

June 12 Options Data

35,000 BTC options expired, with a put-call ratio of 0.67, a maximum pain point of $66,000, and a notional value of $2.2 billion.

175,000 ETH options expired, with a put-call ratio of 0.61, a maximum pain point of $1,725, and a notional value of $290 million.

Bitcoin rebounded to $63,000 this week, with both BTC and ETH trading below their “pain points.” However, panic caused by the sharp decline has subsided, and market attention has largely shifted to U.S. stocks.

Looking at key options data, 8% of options expired this week, slightly above the recent average. As prices stabilized, GEX was distributed between $60K and $62K. Skew rebounded significantly compared to last week but remains in negative territory, indicating the market is still bracing for a downturn. Meanwhile, as mentioned last week, the market has not placed large-scale bets on a one-sided crash; as long as prices stabilize, implied volatility (IV) will decline.

Market sentiment is currently subdued. With MicroStrategy having opened the floodgates for selling Bitcoin, the next phase of capital inflows will be even more challenging, and overall market sentiment remains bearish. This week is dominated by bears; the best strategy is not to gamble on a rebound, but to reduce risk exposure.

BTC options positioning has consolidated around a narrow set of strikes. The largest short dealer exposure anchored is at $60k . Collectively, downside exposure is heavily concentrated within the $60k to $62k range.

Above spot, long dealer exposure is distributed more broadly across the $70k to $80k range, with the largest single position at $80k

Overall strike concentration has increased relative to prior sessions. A larger share of total options exposure is now centered around fewer strikes, producing a more defined positioning profile. Liquidity conditions, systematic hedging flows, and realized volatility remain directly linked to these concentrations particularly the $60k to 62k region, which represents the principal risk trigger in the near term.

Important to note that these do not include IBIT data