For the record.

Canada’s recession is not bad luck, it is a policy choice and the blame sits squarely with Tiff Macklem, not Mark Carney.

By keeping monetary conditions too tight for too long into a tariff‑driven slowdown with inflation already essentially anchored, Macklem has replayed John Crow’s late‑1980s mistake of attacking real estate to prove his anti‑inflation credentials, and in the process turned a manageable adjustment into a made‑in‑Canada recession.

EMBARRASSING

CTV claimed removing all taxes on gasoline would cause inflation to explode 🤯

Because of the increase in demand for gasoline

Pierre Poilievre was SHOCKED

AND I DON’T BLAME HIM

WHAT A TERRIBLE INTERVIEW CTV

@MBjegovic So much noise and panic. I believe most of this is temporary oil prices spiking due to war. You almost wonder if it's intentional to delay deflation before the mid terms.

As Canada’s interest rate–sensitive sectors contract, the Bank of Canada under Tiff Macklem continues to dither. January’s data tell a clear story: headline CPI was flat month-over-month, GDP growth stagnant at 0%, and the economy shed 24,000 jobs. Yet despite this weakness, food inflation surged to 7.3% — including 4.8% for groceries — driven not by an overheating economy but by policy missteps in Ottawa. Even adjusting for last year’s GST holiday base effect, food prices are still rising roughly 6.3%, the highest among G7 nations. The Bank’s refusal to respond appropriately only deepens the damage, compounding the failures of Mark Carney’s misplaced policy legacy. The time to cut rates is now.

And with all due respect to my Canadian friends, whose politics focus obsessively on the United States: your stagnating living standards have nothing to do with Donald Trump or whatever bogeyman the CBC tells you to blame.

The fault lies with your leadership, elected by you.

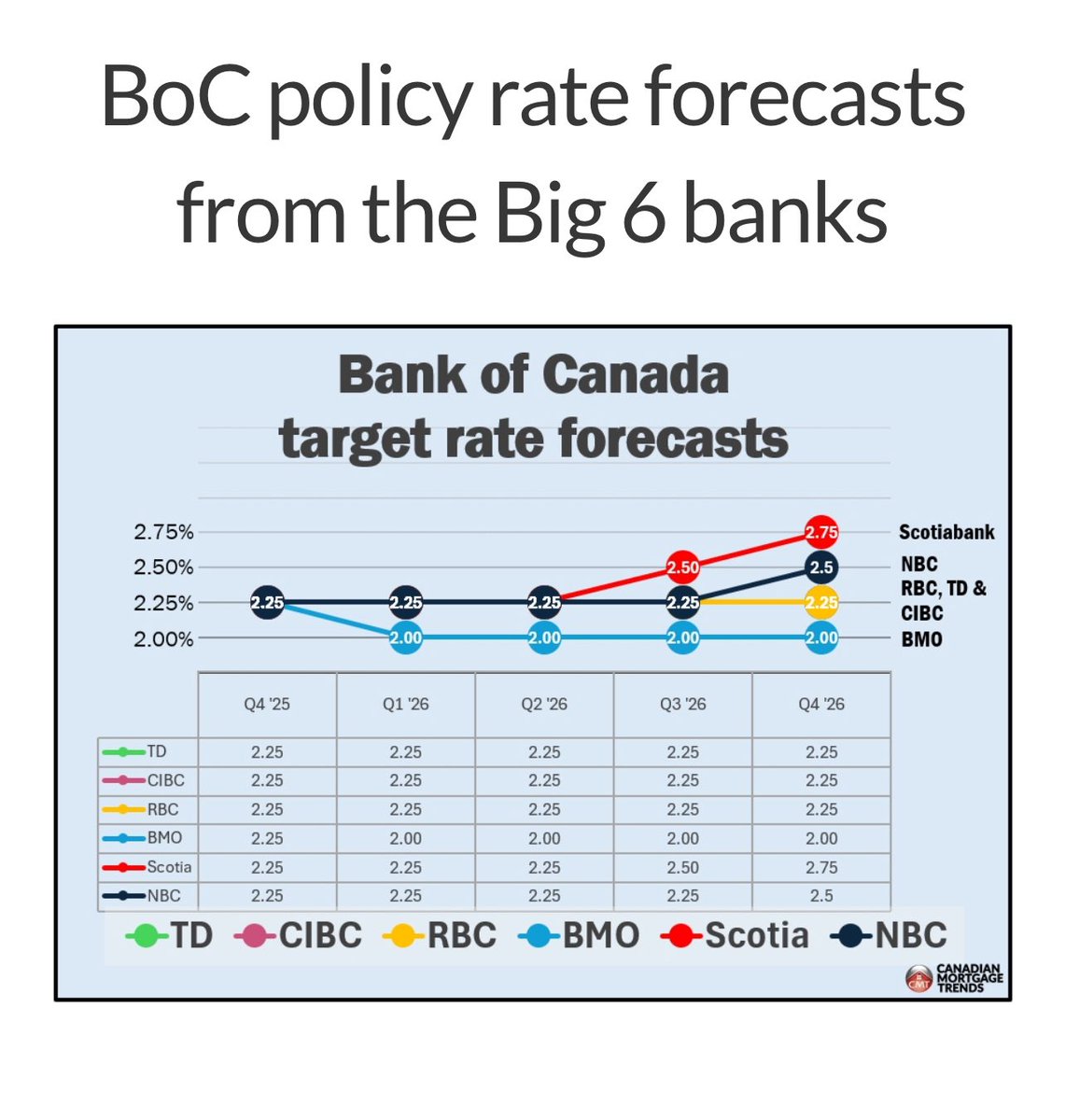

For the record. In Canada r* has significantly declined. Another swing and miss by Mr Macklem.

The neutral rate of interest in Canada has clearly declined in response to shifting trade dynamics and structural changes in the North American economy. Yet the Bank of Canada continues to treat r* as a fixed parameter, ignoring the profound adjustment underway as the economy digests an external rupture. This rigidity reflects flawed policy design and poor communication. Clinging to an outdated estimate of the neutral rate risks overtightening in a disinflationary environment and misjudging the true stance of monetary policy. It is, quite simply, bad policy in action.

https://t.co/EjicoKkXj9

For the record.

Bay Street and BOC economists are catastrophically misreading the crisis unfolding in Canada’s real economy. Their chronic reliance on flawed models and faith in gradualism has left policy utterly out of step with reality: Canadian households and producers are being crushed by recession, with unemployment surging toward 8% in Ontario and Alberta, while manufacturing is gutted by tariff and power cost shocks. Yet the Bay St. consensus still clings to tired forecasts of limited rate cuts and only “subdued” growth, blind to the urgency and depth of structural damage already taking root across the country.

This isn’t just a routine miscalculation, it’s a repeat of the same cognitive failures that led policymakers to wait too long in previous downturns, letting distributive lags compound the harms. With rate cuts taking up to two years to reach full effect, Canada needs to see the overnight rate at 1%, and fast, or risk permanent economic scarring. Bay Street’s and the BOC complacency is not just outdated; it’s actively dangerous in the face of a generational crisis.

https://t.co/2g4Vz6KEqz