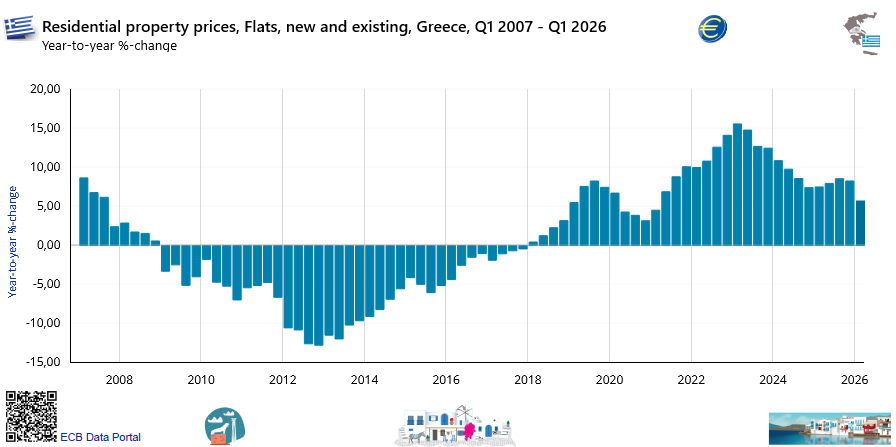

Η αγορά ακινήτων στην Ελλάδα το πρώτο τρίμηνο του 2026 χαρακτηρίζεται από συνεχιζόμενη ανοδική πορεία των τιμών, με επιβράδυνση του ρυθμού αύξησης σε σχέση με τα προηγούμεν�� χρόνια, καθώς σύμφωνα με τα στοιχεία της Τράπεζας της Ελλάδος για το α’ τρίμηνο 2026 οι τιμές των διαμερισμάτων αυξήθηκαν κατά 5,7% σε ετήσια βάση (νέα +6,0%, παλαιά +5,5%), με την Αθήνα στο +5,2%, τη Θεσσαλονίκη στο +6,4% και τις λοιπές περιοχές στο +6,9%, ενώ το 2025 είχε καταγραφεί μέσος ρυθμός περίπου 7,8%, συνεχίζοντας την ανάκαμψη από την κρίση χρέους που είχε οδηγήσει σε πτώση τιμών κατά 40%+ την περίοδο 2009-2017.

Η αγορά δείχνει σημάδια κόπωσης, με το Q1 2026 να καταγράφει μόλις +0,63% τριμηνιαία (Q/Q) αύξηση — τη χαμηλότερη από το 2020 — ενώ η δυναμική μετατοπίζεται εκτός πρωτεύουσας και η συνολική στεγαστική κρίση βαθαίνει.

Σε ��υτό το πλαίσιο, η αγορά παραμένει ιδιαίτερα illiquid με πολύ χαμηλό αριθμό συναλλαγών, η προσφορά περιορίζεται από την υποτονική οικοδομική δραστηριότητα (άδειες δόμησης μόλις στο 38% του 2007), τις ελλείψεις εργατικού δυναμικού στον κατασκευαστικό κλάδο, το υψηλό κόστος υλικών, το μεγάλο απόθεμα παλαιών και κενών κατοικιών (12% σύμφωνα με την απογραφή 2021), καθώς και τον ανταγωνισμό από τις βραχυχρόνιες μισθώσεις, ενώ η ζήτηση παραμένει ισχυρή τόσο από εσωτερικούς όσο και από ξένους επενδυτές (παρότι η τελευταία έχει περιοριστεί).

Ως αποτέλεσμα, η προσιτότητα τ��ς στέγασης έχει επιδεινωθεί δραματικά, με τους Έλληνες να δαπανούν κατά μέσο όρο 35,5% του διαθέσιμου εισοδήματός τους για στέγαση (ΕΕ 19,2%), το 28,9% του πλη��υσμού να υπερβαίνει το 40% του εισοδήματος σε στεγαστικά έξοδα, και τα χαμηλά εισοδήματα να ξεπερνούν το 60%, ενώ ιδιαίτερα πιεσμένη είναι η κατάσταση για νέους, και ευάλωτες ομάδες.

Συνολικά, η αγορά παραμένει θετική για ιδιοκτήτες και επενδυτές, αλλά εξαιρετικά προκλητική για νέους αγοραστές και ενοικιαστές, με την άνοδο των τιμών να αναμένεται να συνεχιστεί με πιο ήπιους ρυθμούς τα επόμενα χρόνια, εφόσον δεν υπάρξει σημαντική αύξηση της στεγαστικής προσφοράς.

Δείκτες Τιμών Οικιστικών Ακινήτων — Α΄ Τρίμηνο 2026.

Το Q1 2026 ο τριμηνιαίος ρυθμός μεταβολής (Q/Q) διαμορφώθηκε σε +0,63%, το χαμηλότερο επίπεδο από το Q4 2020 (-0,19%).

Δεν έγινε αρνητικός, αλλά η επιβράδυνση είναι εμφανής: από +3,07% στο Q1 2025 σε +0,63% στο Q1 2026, δηλαδή μόλις το ένα πέμπτο του ρυθμού ένα χρόνο πριν.

Ο ετήσιος ρυθμός (+5,7%) οφείλεται κυρίως σε base effect από το ισχυρό Q1 2025, όχι σε νέα ανοδική ώθηση.

Το momentum έχει καθαρά επιβραδυνθεί.

Σε γεωγραφικό επίπεδο, οι λοιπές περιοχές ανήλθαν για πρώτη φορά στην κορυφή της κατάταξης με ετήσια αύξηση +6,9%, όχι λόγω επιτάχυνσης της δικής τους δυναμικής, αλλά λόγω της μεγαλύτερης επιβράδυνσης των υπόλοιπων κατηγοριών — ιδίως των άλλων μεγάλων πόλεων (-4,8 ποσοστιαίες μονάδες) και της Θεσσαλονίκης (-3,3 π.μ.) σε σχέση με το 2025.

Η Αθήνα καταγράφει τον χαμηλότερο ετήσιο ρυθμό αύξησης (+5,2%), γεγονός που υποδηλώνει ότι η αγορά της έχει ήδη απορροφήσει μεγάλο μέρος της ανόδου της περιόδου 2018–2023, ενώ οι υπόλοιπες περιοχές εξακολουθούν να συγκλίνουν από χαμηλότερη βάση.

Για την κατασκευή των δεικτών της Τράπεζας της Ελλάδος σχετικά με τις τιμές στην αγορά οικιστικών ακινήτων χρησιμοποιούνται τα αναλυτικά στοιχεία, τα οποία συγκεντρώνει το Τμήμα Ανάλυσης Αγοράς Ακινήτων, από όλα τα πιστωτικά ιδρύματα που δραστηριοποιούνται στην Ελλάδα.

Τα στοιχεία αυτά περιλαμβάνουν τις εκτιμήσεις των τραπεζών για την τρέχουσα εμπορική αξία των οικιστικών ακιν��των, καθώς και πληροφορίες για τα ποιοτικά χαρακτηριστικά τους.

Ο αριθμός των εκτιμήσεων που έχουν ήδη αναγγελθεί στην Τράπεζα της Ελλάδος (με περίοδο αναφοράς έως το τέλος Μαρτίου του 2026) ανήλθε συνολικά σε 964,3 χιλιάδες (65,3% διαμερίσματα, 18,4% μονοκατοικίες, 6,3% μεζονέτες, 6,0% οικόπεδα και 4,0% λοιπά ακίνητα).

#Greece: #HousePrices: Indices of residential property prices: Q1 2026: BoG

Ιn the Q1 of 2026, the annual rate of change in apartment prices for the entire country stood at 5.7%.

Broken down by age of property, the annual rate of change in prices of new apartments was 6% and of old apartments 5.5%.

Broken down by region, the annual rate of change in prices of apartments was 5.2% in Athens, 6.4% in Thessaloniki, 5.4% in other cities and 6.9% in other areas of Greece.

Ισχυρή Ανάκαμψη & Νέα Ιστορικά Υψη (2019–2025).

Η ανάκαμψη των τιμών των νεόδμητων κατοικιών επιταχύνθηκε απότομα, ιδίως μετά το 2020.

Και η #Αθήνα και η #Θεσσαλονικη ξεπέρασαν το επίπεδο του 2007 και στη συνέχεια τα ιστορικά υψηλά του 2008. #ακίνητα

Residential Property Price Index (RPPI) for new flats in Greater #Athens, and #Thessaloniki (Q1 2006 - Q4 2025)

#HousePrices

The residential property price index for new flats in Greece’s two largest cities shows a strong bull market after a prolonged crisis.

Both Greater Athens and Thessaloniki have reached new all-time highs, significantly above pre-2008 crisis levels.

Athens vs Thessaloniki

The two markets have moved very closely together over the 20-year period.

Thessaloniki showed slightly higher volatility (stronger peak in 2008–09 and marginally stronger recent gains).

In 2025, both cities have converged again and are performing almost identically at record levels.

Market Interpretation:

The Greek new residential property market has fully recovered from the debt crisis and entered a sustained boom phase.

The recovery that started around 2018 has been particularly robust since 2021, with prices rising sharply in both major urban centres.

Current Market Status (2025):

Strong Uptrend.

All-time high prices.

Robust demand for new flats in both Athens and Thessaloniki.

Τιμές κατοικιών, #ενοίκια και εξέλιξη της αναλογίας τιμής προς εισόδημα σε 6 χώρες ης Νότιας Ευρώπης (#Ελλάδα, Ιταλία, Ισπανία, Πορτογαλία, Κροατία, Κύπρος) και στην #ΕΕ από το 2005 στο 2025.

House prices, rents and price-to-income evolution in 6 Southern European countries and EU27 since 2005.

#Mediterranean#Housing#Greece

Many countries show house prices and rents outpacing incomes and EU averages post-2010s recovery, linked to tourism, migration, low construction, and foreign investment.

This fuels affordability concerns, urban-rural divides, and labor mobility issues.

The Commission highlights needs for increased housing supply, social/affordable stock, permitting reforms, and energy renovations.

Spain and Portugal face the most severe affordability crises, with soaring house prices, rents, and price-to-income ratios, driven by tourism, foreign demand, and limited social housing stock.

Greece and Cyprus show mixed trends: Greece has high affordability pressure in cities, while Cyprus remains relatively affordable.

Italy is an outlier with declining house prices and rents, improving affordability.

Croatia has seen explosive house price growth, but low overburden rates due to high homeownership.

Στις 9 Ιουνίου του 2026, η ΤτΕ ανακοινώνει τους δείκτες τιμών κατοικιών για το α΄ τρίμηνο 2026.

Θα συνεχιστεί η επιβράδυνση του τριμηνιαίου ρυθμού — ή θα δούμε για πρώτη φορά από το 2017 αρνητικό Q/Q; Θα συνεχίσουν οι άλλες πόλεις να ξεπερνούν την Αθήνα και τη Θεσσαλονίκη σε ρυθμό ανόδου;

Η #Ελλάδα βρίσκεται στο 19% (κάτω από τον μέσο όρο της #ΕΕ-27 που είναι 23% ) που εξηγείτ��ι από την πολύ αργή ηλικία αποχώρησης από το γονεϊκό σπίτι (30,7 χρόνια), η οποία μπορεί να καταστέλλει την ανησυχία για #στέγαση μεταξύ εκείνων που ζουν ακόμα με την οικογένειά τους.

Share of young people (16–30) for whom housing affordability is the biggest worry, by country, 2025.

#EU#Greece#HousingCrisis

EU-27 Average: 23% of young Europeans consider housing affordability to be their primary concern.

Greece at 19% — below the EU-27 average of 23% — is similarly explained by the very late age of leaving the parental home (30.7 years), which may suppress expressed housing worry among those still living with family.

The "Middle" Cluster: A massive block of 13 countries sits right around the average mark, hovering tightly between 23% and 26%.

High-Concern Zone: Major economies and notable housing markets like Germany (30%), Spain (28%), and the Netherlands (32%) all sit comfortably above the EU average, showing heightened anxiety among their youth

According to the Flash Eurobarometer, when thinking about their future, young Europeans are most worried about the cost of living and peace and global stability. Nearly four out of ten young Europeans believe the EU should invest more in affordable housing and cost-of-living support.

Η #ΕΕ χρειάζεται 7,14 εκατομμύρια επιπλέον κατοικίες μέχρι το 2035.

Αύξηση της κατασκευαστικής δραστηριότητας:

Η Ευρώπη πρέπει να κατασκευάζει περίπου 650.000 επιπλέον κατοικίες ετησίως, πέρα από τις ~1,6 εκατομμύρια που ��ατασκευάζονται ήδη κάθε χρόνο.

#ΣτεγαστικήΚρίση

#EU#Housing: Investment needs per NUTS3 region in % of the 2024 national dwelling stock.

For every NUTS‑3 region in the EU, how large the projected housing investment need (2025–2035).

Additional housing units needed (2025-2035) divided by the national dwelling stock in 2024.

No data for CZ, EL, HR, RO, SI, SK.

The Dwelling Shortfall: The EU requires 7.14 million additional dwelling units by 2035.

The Construction Increase: Europe needs to build roughly 650,000 additional units per year on top of the ~1.6 million units currently built annually.

The Monetary Value: Closing this gap translates to a required total investment of €1.68 trillion by 2035 (approximately €150 billion per year when evaluated at 2024 price levels).

Διανυκτερεύσεις σε τουριστικά καταλύματα κατά περιοχή NUTS 3 (2023).

Ο τουρισμός στην #Ελλάδα είναι υψηλά συγκεντρωμένος στα νησιά στις παραθαλάσσιες περιοχές και στην Αττική, με περιοχές όπως οι #Κυκλάδες και τα #Δωδεκάνησα να ηγούνται στις τουριστικές διανυκτερεύσεις.

Η Goldman Sachs λάνσαρε ένα tokenized real estate fund — αμοιβαίο κεφάλαιο επενδύσεων σε ακίνητα με ψηφιακή έκδοση κατακερματισμένων μεριδίων (fractional) επί blockchain.

Το fund είναι Ευρωπαϊκό / EEA-focused, λειτουργεί υπό το πλαίσιο της οδηγίας AIFMD με έδρα στο Λουξεμβούργο, και απευθύνεται σε θεσμικούς επενδυτές σε όλη την Ευρώπη — χωρίς καμία πρόβλεψη για λιανική πρόσβαση ή διανομή εκτός ΕΕ/ΕΟΧ.

Πρόκειται, για ένα ισχυρό σήμα αναγνώρισης της αγοράς tokenized ακινήτων: όταν η Goldman Sachs επιλέγει να δ��μήσει ένα real estate fund blockchain-native εντός Ευρωπαϊκού ρυθμιστικού πλαισίου, δεν πρόκειται για πείραμα — αλλά για επικύρωση ότι το tokenization ακινήτων ωριμάζει ως θεσμικό εργαλείο κατανομής κεφαλαίου σε επίπεδο ΕΕ.

Εκτιμήσεις για την ετήσια υπερ/υπο-εκτίμηση των τιμών κατοικιών στην Ελλάδα (2007-2025).

Οι τιμές αυξήθηκαν +7,8% το 2025, με ενδείξεις υπερτίμησης ~18% σύμφωνα με την Ευρωπαϊκή Επιτροπή.

Η ΕΚΤ προβλέπει για το 2025 ευρύ εύρος (μέγιστο +26,0%, ελάχιστο -15,3%), με spread 41,3pp

Estimates of the annual over/undervaluation of residential property prices in #Greece (new and existing dwellings), 2007–2025

#Houseprices started to pick up in 2018 with the economy's gradual recovery, and grew by 13.9% in 2023.

The growth rate has moderated since then, still remaining high, averaging at 7.8% in 2025, and showing signs of overvaluation, of around 18% in 2025 (based on the standard European Commission methodology, not ECB's).

Greece is among EU countries showing notable overvaluation signals in maximum/average metrics in 2025, alongside strong recent price growth.

Greece shows: Strong price and rent growth, Structural supply shortages, High foreign investment, Mixed valuation signals, Rising affordability pressures.

But no evidence of a credit‑driven bubble.

The market remains in a structural growth phase post-crisis recovery, but with cooling momentum and increasing policy/regulatory attention on affordability and overvaluation risks.

The 41.3pp spread in 2025 between maximum 26.0% and minimum -15.3% reflects high uncertainty.

BOG’s Financial Stability Reviews often flag this divergence — model-based methods tend to show undervaluation for Greece while price-to-rent/income show overvaluation.

The #AI IPOs are coming.

Τι θα στοιχίσει αυτό στο Σαν Φρανσίσκο;

https://t.co/D4pdh5b58g

Δισεκατομμύρια δολάρια πρόκειται να πλημμυρίσουν την πόλη σχεδόν ταυτόχρονα.

Ήδη όμως βλέπουν την τρέλα (ή την φούσκα) στα ακίνητα τους:

• Ένα σπίτι βγήκε στην αγορά με ζητούμενη τιμή στα 6.000.000$ και πουλήθηκε 9.000.000$ (+3 εκατ.$, 150% του asking price) σε μόλις 11 ημέρες, και όλα σε μετρητά.

https://t.co/BqCF9oMEKQ

• Άλλο ένα σπίτι βγήκε στην αγορά με ζητούμενη τιμή στα 7.950.000$ και πουλήθηκε 15.000.000 $ (+7.050.000$, σχεδόν διπλάσια τιμή).

https://t.co/GDHRzawgRu

Τα lock-up periods μετά από IPO — συνήθως 6 μήνες — σημαίνουν ότι οι employees δεν μπορούν να πουλήσουν μετοχές αμέσως.

Μήπως γι' αυτό υπ��ρχουν ήδη πωλητές που ζητάνε την άξια του σπιτιού σε μετοχές OpenAI ή Anthropic αντί για δολάρια;

Όσοι δεν πρόλαβαν τα tender offers είναι πλούσιοι στα χαρτιά αλλά χωρίς ρευστό, οπότε κάνουν barter με το μόνο που έχουν: private equity.

Το φαινόμενο AI

Ιδρυτές, στελέχη και early employees από OpenAI, Anthropic και άλλες AI εταιρείες φέρνουν τεράστιες ποσότητες μετρητών και μετοχών.

Πληρώνουν cash και σαρώνουν τα καλύτερα σπίτια στην πόλη του Σαν Φραν και όχι μόνον.

Η πραγματικότητα:

Δεν πρόκειται για επαύλεις με πισίνες και μεγάλους κήπους.

Είναι κανονικά πολυτελή σπίτια μέσα στην πόλη.

Κι όμως πωλούνται σε εντελώς εξωφρενικές τιμές.

Πρόβλεψη:

Πολλά από τα σπίτια που αγοράζονται τώρα σε εξωφρενικές τιμές στο Σαν Φρανσίσκο θα μεταπωληθούν ως το τέλος του 2026 σε ακόμα εξωφρενικότερες τιμές, όταν μπει το φρέσκο χρήμα από τα AI IPOs.

Πιθανή φούσκα σε εξέλιξη;

Υπάρχει πιθανότητα κάποια από αυτά τα κεφάλαια να μεταφερθούν σε ακίνητα στην Ευρώπη;

Το 2025 το 26,4% των Ελλήνων επιβαρύνεται υπερβολικ�� από στεγαστικό κόστος (3+ φορές πάνω από τον μέσο όρο ΕΕ 8,2%).

Οι Έλληνες δαπανούν κατά μέσο όρο 35,5% του εισοδήματός τους για στέγαση (στην ΕΕ: 19,2%).

#Ελλάδα #Ακίνητα #Ενοίκιο

Housing Cost Overburden Rate at NUTS2 regional level in Greece for 2025: EC

#Greece's overall #HousingCost overburden rate is 26.4% of the total population — more than three times the EU27 average of 8.2%.

28.9% of Greeks live in households where housing costs exceed 40% of disposable income (vs. 8.2% in the EU).

Greeks spent on average 35.5% of available household income on housing (vs. 19.2% in the EU).

Most Affected Groups:

Market-rate tenants: 37.4% face overburden (vs. EU average of 19.2%)

Owners with mortgages: 20.9% (vs. EU average of 5%)

Single households: ~65.1% face overburden

Single-parent households: ~65.8%

Low-income households: 62.8% of income spent on housing (vs. 26.9% EU)

At-risk-of-poverty population: 88.9% face housing cost overburden

Young people (aged 20–29): 31.1% in 2024 (vs. 11% EU)

Non-EU citizens: 38% face overburden (vs. 16.3% EU)

Persons with disabilities: 33% of their households spend >40% of income on housing (vs. 10.4% EU)

Structural Causes Cited:

No regulated rental prices

Social housing provision stopped in the early 2010s

House price-to-income ratio grew 13% in the last decade

House price increases among the sharpest in the EU

Tourism pressure driving up rental costs in coastal and island areas

Overcrowding at 27% (vs. 16.9% EU)

Οι τιμές των κατοικιών στην #Ελλάδα αυξάνονται έντονα από το 2019, λόγω υψηλής ζήτησης από Έλληνες και ξένους μέσω Golden Visa και περιορισμένης προσφοράς.

Τ��υτόχρονα, η αύξηση τιμών και ενοικίων ξεπερνά την αύξηση των εισοδημάτων, κάνοντας τη στέγαση πολύ πιο δύσκολη. #ακίνητα

#Houseprices have been rising at a high pace since 2019, driven by strong demand and subdued construction activity.

Domestic demand picked up in the post-pandemic period and has remained strong.

Foreign demand – which has been incentivised by the golden visa programme and investment opportunities in tourism – moderated somewhat in 2025.

Housing supply is constrained by years of sluggish housing investment which remains low by EU comparison despite the recent uptick in construction activity.

House price and rent increases surpassed income growth, hence housing affordability has deteriorated, affecting a large part of the Greek population.

Delays in the judicial liquidation of collateral also exacerbate the housing affordability crisis, as many vacant residences are tied up in processes related to debt enforcement.

Στην #Ελλάδα το 2025 οι τιμές των κατοικιών αυξήθηκαν 7,8% (από 9,1% το 2024), με υπερτίμηση ~18%

Το ratio τιμών/εισοδημάτων χειροτέρευσε σημαντικά, ενώ τα ενοίκια αυξήθηκαν 10%

Οι Έλληνες δαπανούν 35,5% του εισοδήματός τους για στέγαση , με πολύ χαμηλή προσφορά νέων κατοικιών

#HousePrices, #Rents & Price-to-Income Ratio Greece vs EU27, 2005–2025 and House Supply Indicators in 2005–2025: #Greece

Greek Housing Market: 2025

In 2025, house prices grew by 7.8% (down from 9.1% in 2024), but still showed signs of overvaluation of around ~18%, based on the standard European Commission methodology.

House prices grew at 13.9% in 2023, moderating to 7.8% in 2025.

As household income growth has lagged behind price increases, the house-price-to-income ratio has increased rapidly since 2021, pointing to deteriorating affordability.

Rental prices (including existing and new rental contracts) have also accelerated, growing by 10.0% in 2025, increasing rental affordability pressures.

Greece's trends diverge significantly from the EU27 average, especially in recent years.

Residential building permits remain far below pre-crisis levels — only 38% of 2007 levels in 2025.

Investment in dwellings recovered somewhat to 3.1% of GDP in 2025, but remains well below the EU average of 5.0%.

Producer prices for residential buildings have risen significantly.

Supply remains constrained despite strong demand, contributing to price pressures.

A large share of the housing stock is old, vacant, or tied up in legal issues.

Housing affordability is a major challenge: in 2024, Greeks spent on average 35.5% of available household income on housing costs (vs 19.2% in the EU), and a substantial 28.9% of the population lived in households where housing costs exceeded their means — more than three times the EU average of 8.2%.

Low-income households spent more than 60% of their income on housing. Greece has the highest share in the EU.

A surge of foreign buyers since 2022, partly driven by the golden visa programme and investment opportunities in tourism and short-term rentals, pushed prices up further — though foreign demand started to contract in 2025 due to changes in regulations.

Building permits in 2025 were still only 38% of 2007 levels, dwelling investment (3.1% of GDP) was well below the EU average (5.0%), and a large share of the existing stock is old, vacant, or uninhabitable.

#Ελλάδα: Το κόστος στέγασης αυξάνεται γρήγορα, ενώ η προσφορά κατοικιών είναι περιορισμένη. Η ανακαίνιση άδειων ακινήτων, η ενθάρρυνση μακροχρόνιων μισθώσεων και ανακαινίσεις για ενεργειακή φτώχεια μπορούν να μειώσουν τις πιέσεις.

#ΣτεγαστικήΚρίση

#Greece: EC: Housing costs are increasing at a fast pace, while the supply of dwellings is limited. Renovating and making empty properties liveable, incentivising long-term rentals, and tackling energy poverty via energy efficiency renovations could ease pressures. #HousingCrisis

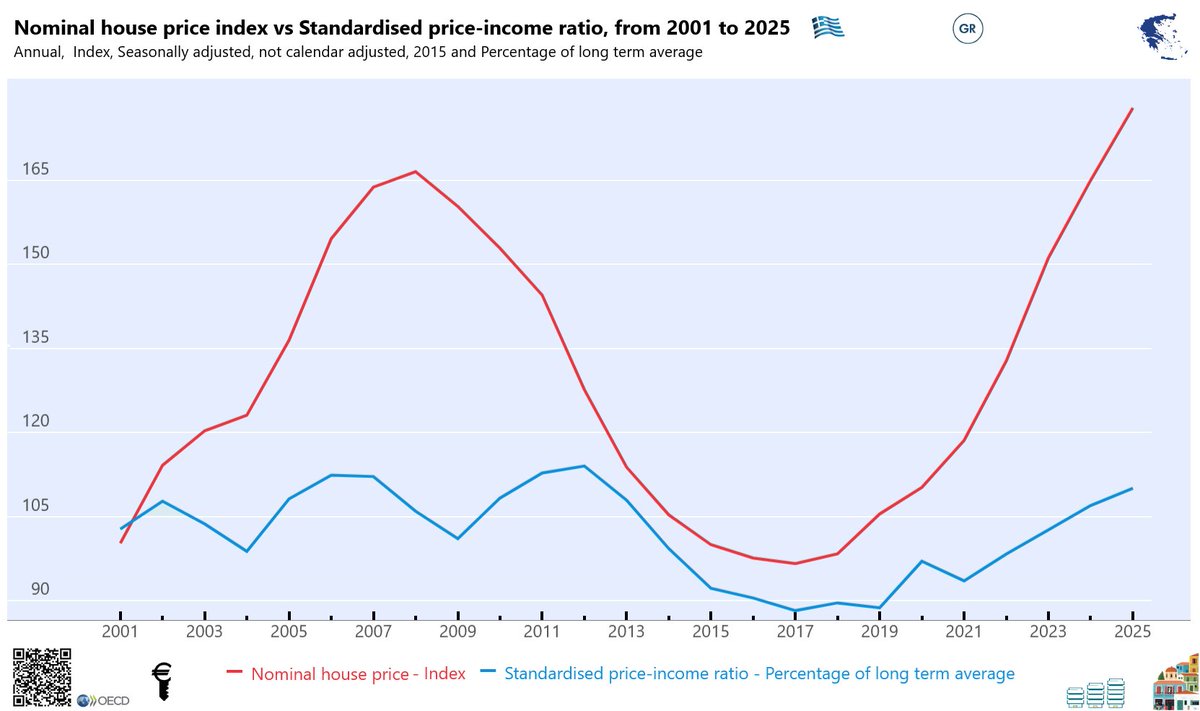

Στην #Ελλάδα, οι τιμές κατοικιών αυξάνονται ταχύτερα από τα εισοδήματα.

Ο τυποποιημένος δείκτης τιμής-εισοδήματος ξεπέρασε το 105 το 2025, δείχνοντας ότι η στέγαση επέστρεψε σε «μη προσιτή» ζώνη.

Ισχυρή άνοδος τιμών, πληθωρισμός ενοικίων και πιέσεις προσφοράς, όχι όμως φούσκα.

#Greece: Nominal house price index vs Standardised price-income ratio, from 2001 to 2025

Greek #HousePrices have grown faster than household incomes relative to the historical norm.

Greece’s #HousingMarket shows strong price growth, persistent rental inflation, and tightening supply, with all major institutions (ECB, Eurostat, OECD, IMF, BIS, BoG) confirming rising valuation pressures but no credit‑driven bubble.

Greece has shown stronger house price growth than the euro area average in recent years, though growth moderated in 2025.

The Affordability Squeeze: Because nominal residential real estate values shot up by double digits annually while domestic disposable income recovered at a much more rigid, slower pace, the gap between the two expanded exponentially.

The standardised price-income ratio (blue line) climbing back past 105 by 2025 indicates that housing has officially crossed back into ‘unaffordable’ territory relative to long-term historical norms

Η #ΕΕ χρειάζεται 7,14 εκ. επιπλέον κατοικίες μέχρι το 2035 για να καλύψει το κενό ζήτησης-προσφοράς.

Από το 2010-2024 υπήρξε έλλειψη 4,57 εκ. λόγω ανεπαρκούς κατασκευής.

Το ετήσιο έλλειμμα φ��άνει ~650.000 κατοικίες.

Χωρίς στοιχεία για την #Ελλάδα

#EU: #Housing investment needs per NUTS‑3 region, measured as the absolute number of additional dwellings required to close the gap between household demand and housing supply up to 2035.

For CZ, EL, HR, RO, SI, SK= NO data

Insufficient construction 2010-2024 in regions with dwelling shortfall: 4.57 million units

Demographic change 2025-2035: 5.09 million units total, 4.77 million in regions with expected

shortfall

Replacement/amortisation need: 3.55 million units total, 0.75 million in regions with shortfall

Expected construction 2025-2035: 17.06 million units total, 2.95 million in regions with shortfall

EU total: Housing construction gap 2025-2035 = 7.14 million dwelling units, or ∼650,000 units/year additional to current build rates.

The framework determines that the absolute housing construction gap across the EU between 2025 and 2035 stands at 7.14 million additional dwelling units.