@MrtnzAlvrz Tio estas obsesionado con el tema. ITA es una aerolinea enana y ya la han reestructurado bastante, sigue con las pocas rutas profitables que les quedan. Iberia se queda con LHR pero en cambio tiene 100 vuelos internos en España, pick your poison

Although Brunello Cucinelli (the brand) is known for their high quality cashmere and fine tailoring, the man himself is often oddly dressed and appears not to understand how to dress for his body type. His styling choices betray an ignorance of garment cuts, colours, decoration and their meanings, thereby resulting in incongruent looks, like a cook who doesn't know how each ingredient makes or breaks a dish, but throws them in anyway because they taste good individually.

The brand enjoys remarkable positioning due to the army of tailors, designers, stylists, models and brand managers working behind it, thereby giving the impression that its owner is a purveyor of good taste to those whose opinions are easily swayed by authority.

Without the company's standing, the man himself would be seen as a poorly dressed businessman with a sloppy haircut.

As a half Spanish, half Italian. I love both cuisines, but if I'm being forced to choose, Italian food wins by a comfortable margin.

The gap is bigger than most people want to admit.

I am shocked how many Americans buy into such nonsense about Europe, like the idea that there are “no-go zones” in central Paris or Europeans are “too poor” to afford air conditioning.

I wish it was socially acceptable to ask how people afford things, like your house is so nice, you go out to eat 3 times a week, and are always on vacation, are you in debt?

When Ripple came out it was going to be a financial revolution, it was going to change the way we all transacted. Replace SWIFT and all the greedy banks

Over a decade later, what do they have to show far?

Well someone has a $50m car collection to show for..

https://t.co/QGwkEwKBg2 this article describes Vannacci as it was some sort of new Mussolini... in truth he is quite soft-spoken and a little bit of a clown. Anglo-Saxon press always exaggerating the "fascism" risk in latin countries

HF PASS THROUGH FEES intro class

I think JAIN has some of the smartest people in the industry ... Paul is a legend developing talent, their risk team esp my buddy Adam, their main TMT team some real door kickers... I think they are S tier. MLP made a smart decision, esp with the cost synergies you will see below

pass through fees are this opaque area for funds (insiders and outsiders), so this is more about the structure than the fund... JAIN just the example here

FOR FUNDS THERE ARE 3 KEY AREAS TO UNDERSTAND

1. Gross Trading Costs: These are the direct costs of doing business in the market. They are deducted from trading revenue before a PM ever reports a "Gross Return" number. It is the cost of running the portfolio..

*depending on the fund docs, some of these costs may already be embedded in the “gross return” number. Others may sit below the line... if you are an allocator this is critical to understand

**prime broker fees, leverage/financing interest, stock borrow fees (paying to short a stock), execution fees, and exchange clearing costs + many MORE

2. Pass Through Fees: These are the non trading operational costs of building and running the firm itself. They are passed directly down to the investors as an expense drag

*most times include tech, market data, back office talent, and the BIGGEST BUCKET... buying out the deferred bonuses of PMs poached from competitors (see waterfall below)

3. Management Fee: This is a fixed percentage of assets charged by traditional funds to pay for operations and pad the founders' pockets. In a pure pass through fund, this is replaced entirely by the pass through expense layer #2 above

SOME QUICK MATH:

*AUM: $5BN

*Gross Return: 15%

(+) Gross Trading Profits: ~$750M

(-) Pass through Fees: ~$545M

= Pre-Incentive Profit: ~$205M

(-) Performance Incentive (10% blend): ~$20M

= Net Investor Profit: ~$185M (~3.7% net)

Total all in drag = ~$565M (or ~11.3% of AUM)

ILLUSTRATIVE EXAMPLE OF PASS THROUGH + INCENTIVE WATERFALL:

(-) TALENT WAR $240m

(-) TECH & Infrastructure $120m

(-) Data $75m

(-) HQ Overhead $110m

= $545m

(-) Incentive Fee at 10%: $20m

= $565m drag to LPs

*Obv this is me guessing based on what I know...nobody outside the docs knows the exact allocation

These are the buckets LPs are trying to understand

Gross returns tell you about the trading engine

Net returns tell you about the full business model

*I HAVE NOT READ JAIN DOCS... ECONOMICS ALL VARY BY FUND... THIS IS FOR EDUCATION PURPOSES SO YOU CAN UNDERSTAND THE MOVING PIECES... MOST BEST GUESS*

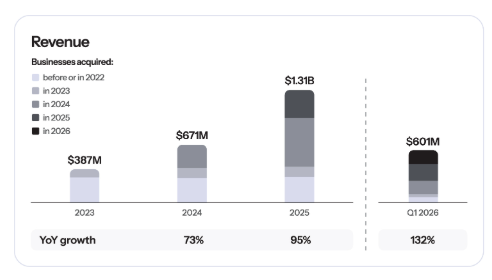

Bending Spoons just filed to go public with the SEC

The Italian startup has snapped up a string of aging apps like Evernote, Eventbrite and AOL over the last few years. It generated $1.3 billion of revenue last year, and $601m in Q1