Hello there 👋

Here to share observations, confessions, ideas and notes from my investment journey.

"Writing is thinking. To write well is to think clearly", hope these help me learn too. Very much looking forward to meaningful discussions. Where will this end up.. we'll know 😉

Yay! With a bit of hiccup in last few days and subsequent profit booking by trimming the position down, finally #YashHighVoltage goes a #multibagger for me 🥳

This one has escalated pretty quick 🚀

@theaiportfolios Thank you. Autopilot isn't available in many countries incl mine. Although we do invest in USA (with constraints).

So wish there is some service or ideally @theaiportfolios's website where portfolio and posts are available for rest of us.

Anyway fantastic job on creating this 👏.

It’s been a while since a clean multibagger in this choppy market, but #ANLON delivered! 🚀

#SME rule: NEVER average down. Always Pyramid / Average Up on structural winners.

📊 Execution:

* Base: @ ₹355.50 ➡️ +100.7%

* Pyramid: @ ₹560.00 ➡️ +27.4%

Let winners run! 📈

Emerald Finance Ltd Q4FY26 Results:-

#Q4Results#Q4FY26#Stockmarket#Nifty#Emerald

🟢 Total Revenue at 9.75 Cr vs 6.45 Cr

(+51.13% YoY┃+24.97% QoQ)

🟢 PBT at 5.94 Cr vs 3.60 Cr

(+65.06% YoY┃+11.26% QoQ)

🟢 PAT at 4.36 Cr vs 2.65 Cr

(+64.35% YoY┃+8.95% QoQ)

🟢 PAT After Minority Interest at 4.05 Cr vs 2.56 Cr

(+58.41% YoY┃+5.58% QoQ)

🟢 Strong all-round growth with consistent improvement across revenue and profitability metrics

🟢 Steady scaling in financial services business with healthy YoY and QoQ momentum

Is Emerald Finance building a consistent micro-finance growth story or still in early-stage expansion phase? 🤔

#IndianStocks #ShareMarket #StocksToWatch

🍏SATHLOKHAR SYNERGYS FY26 ANNUAL RESULTS. H2FY26 RESULTS. Rs. 398 was at 19 p/e. Now 12.6x👍

REAL BIG 👍HAUL in H2 as can be seen below. Topline has grown from 87Cr in Fy23 to 824Cr in Fy26! And valuation 12.6x!

(Valuation of SME Civil construction space is in very bad shape. Hope some sanity comes and good companies like this get deserving valuation)

H2 FY26 Vs.H1 FY26

REV:Rs. 574Cr Rs. Vs Rs. 250Cr👍👍

PAT:Rs. 54.4Cr Vs Rs. 28Cr👍👍

FY26 Vs FY25

REV:Rs. 824Cr Vs Rs. 372Cr👍👍👍

PAT:Rs. 82.2Cr Vs Rs. 34Cr👍👍👍

SATHLOKHAR SYNERGYS SME IPO was in AUG 2024 at Rs. 140 at 13 p/e .

@investor_sr33 Hermes is excellent. I use it for serious projects. But isn't it free and open source anyway irrespective of the model provider you use?

After multiple profit bookings, the latest re-entry is at 457.75 (already 40% up).

Things are looking even better with #Anlon

Looks like this investment will be for a longer term with much higher conviction.

Ah and bumper results too.

Checking my dad's portfolio is instant peace of mind🧘 vs the chaos of my own pf.

A small investment size but has a right mix of diversification and growth IMO

1. AXISVALUE

2. JUNIORBEES

3. KRISHNADEF (Highest allocation and Profit)

4. SMALL250

@investor_sr33 Done tons Agentic AI Engineering work lately so I find this very impressive and inspiring ✨

Would love to read any insights / learning as you build it.

Guessing it's not open source but if there is any way for others to contribute would be interesting too🤝

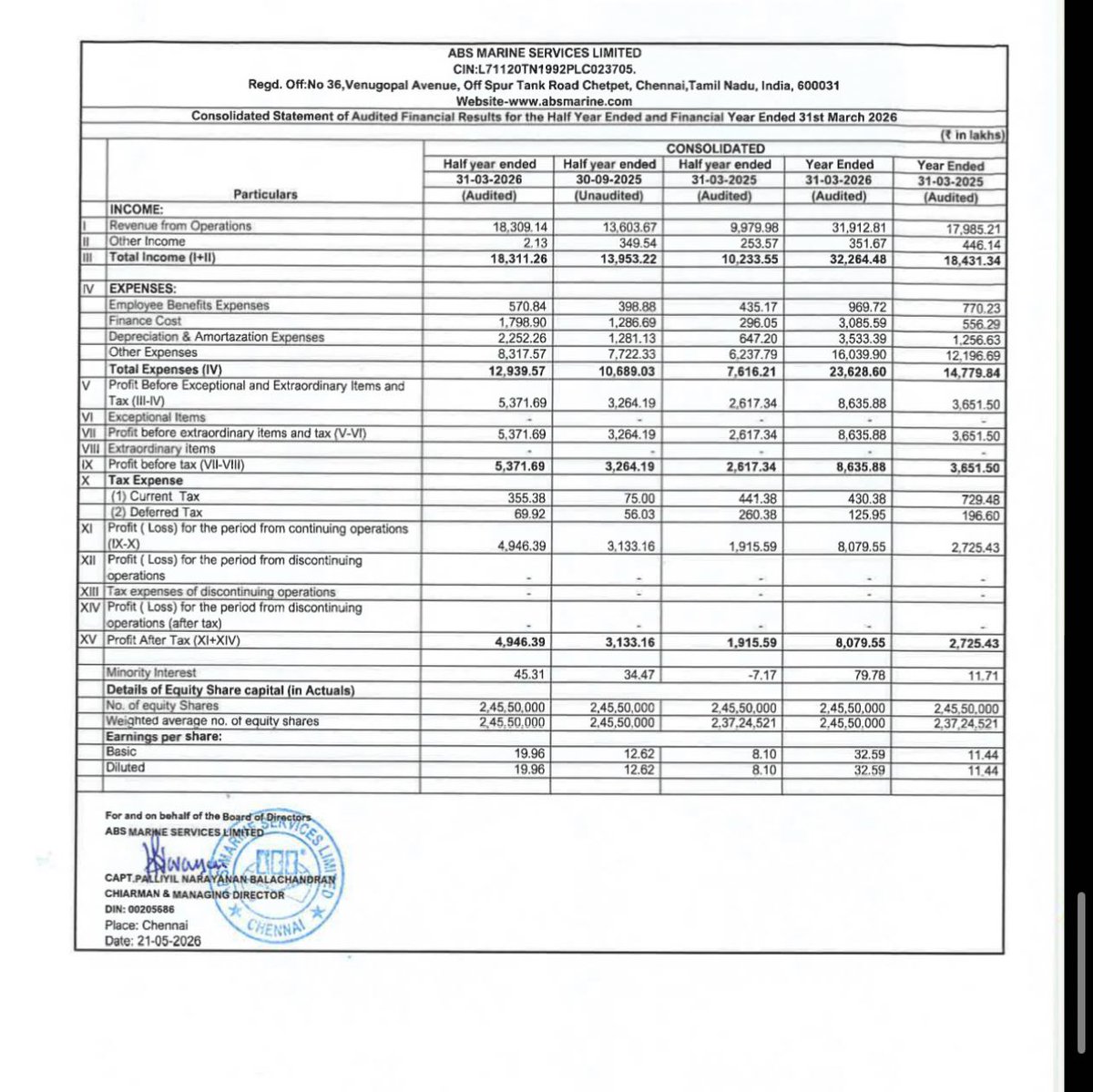

Abs marine

Super awesome results.

My expectation was 20-25 eps for fy 26. But company has delivered 32.5 EPS.

Surely this one should get atleast 10-15 pe minimum.

That itself will take the company to 350-450.

Not buy sell recco. Do study.

Probably big UC tmrw

Newest Addition: FROG INNOVATIONS LIMITED 🐸

Current pricing, CCTV and generally innovation lead approach ✨

Let's see how it turns out.. next few months🤞

🍏BONDADA ENGINEERING FY26 ANNUAL RESULTS. H2FY26 RESULTS. Rs.382 was at 25 p/e. Now 20x👍

Company is reporting close to Rs.3000Cr revenue in EPC of Solar / Telecom projects. These numbers are very good, considering the large base. 👍 It deserves valuation in line with other strong EPC companies in Main Board.👍 Hope market will consider this and do a re-rate!!

Cashflow is 124Cr positive. 👍Don’t bother about receivables in EPC by end March. Will get collected anyway

Q4 Rev is 916Cr Vs 717Cr in Q3. 👍

Q4 Pat is 63Cr Vs 54Cr in Q3 👍

H2 FY26 Vs.H1 FY26

REV: Rs. 1631Cr Vs Rs. 1220Cr 👍

PAT: Rs.118Cr Vs Rs. 93Cr 👍

(May Compare with H2FY25 Rev=Rs. 977Cr & PAT=Rs. 70Cr )

FY26 Vs FY25

REV: Rs. 2851Cr Vs Rs. 1580Cr 👍👍

PAT:Rs.211Cr Vs Rs. 113Cr 👍👍

SME IPO was in Aug 2023. Considering stocksplit with present FV at Rs.2, the adjusted IPO price is Rs.15 at 9P/e!