What happens to human interaction when everyone uses personal AI assistants to read and write conversational messages too? Social media curated your public image but your 1:1 correspondence was always messy. AI curates your 1:1s now so what happens next?

Every AI datacenter is a copper story. Power distribution, busbars, transformers, miles of cabling. Datacenter buildouts at this scale are pushing copper demand into new territory. The AI Exchange lets you hedge the metals that build AI alongside the compute that runs on it.

@bernhardsson Most hedgers won't be shorting GPU prices. They'll be hedging utilization, depreciation, and financing risk (esp if variable costs change ~30-40% QoQ). Dated future contracts with weekly, monthly or quarterly expiries could work. @Architect_Fi who are going live soon.

Nvidia will now pay you to put a mini AI data center on your house

It looks like a normal AC unit in the yard.

But inside sits 16 Nvidia Blackwell GPUs and Dell servers.

A startup called Span builds them, backed by Nvidia.

They bolt onto your home and you get paid for the power and Wi-Fi.

Some estimates put that around $1,000 a month in your pocket.

That is rent money just for hosting a box outside.

Span says it deploys way faster and cheaper than a real data center.

The AI boom is literally moving into the suburbs.

Save this, the grid is getting rebuilt in real time.

Architect’s traditional asset perpetuals exchange just crossed $1 billion notional traded since launch, $783 million in the last month, $77 million in the last 24 hours

PropAMMs are live on Ethereum! pAMM liquidity is now available in every Titan block.

This is a major step toward broader Application-Controlled Execution (ACE) on Ethereum.

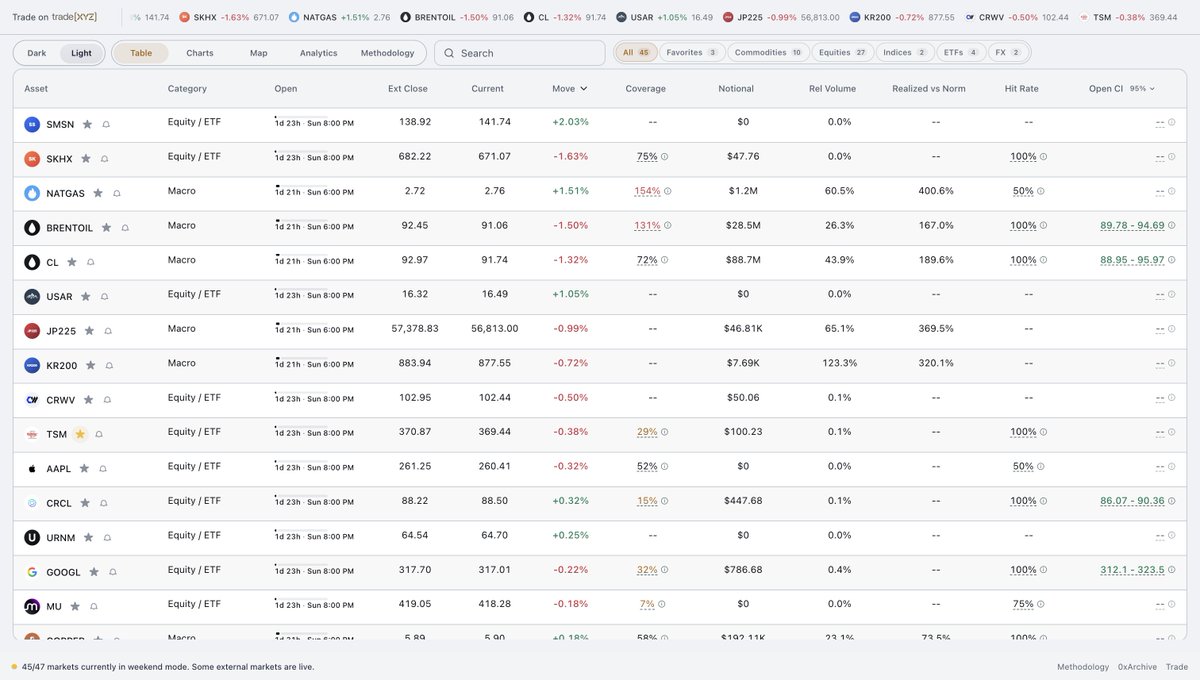

Introducing Weekend Markets:

When traditional markets close, TradeXYZ becomes the only live venue for price discovery. With billions in weekend volume and a 50 bps median error predicting the Monday open, TradeXYZ prices are the most informative signal in finance relative to a stale Friday close.

We built Weekend Markets to systematically track this off-hours data.

Weekend Markets is the comprehensive source for analytics on traditional asset prices over the weekend.

https://t.co/TVkzQcBB2t

@trevor_flipper Yep - there are nuances around exclusivity when it comes to data publishing rights across different ATSes. Circuit breakers do exist, but they require custom implementation depending on the market, its trading hours, the exchange’s data sources, etc.

All the April Fool's Day jokes goes to show how unserious protocols are about their IR functions.

DeFi will need in-house IR once regulators and institutions come. Only few know & do it well.

Earlier today, a user attempted to buy AAVE using $50M USDT through the Aave interface.

Given the unusually large size of the single order, the Aave interface, like most trading interfaces, warned the user about extraordinary slippage and required confirmation via a checkbox. The user confirmed the warning on their mobile device and proceeded with the swap, accepting the high slippage, which ultimately resulted in receiving only 324 AAVE in return.

The transaction could not be moved forward without the user explicitly accepting the risk through the confirmation checkbox.

The CoW Swap routers functioned as intended, and the integration followed standard industry practices. However, while the user was able to proceed with the swap, the final outcome was clearly far from optimal.

Events like this do occur in DeFi, but the scale of this transaction was significantly larger than what is typically seen in the space.

We sympathize with the user and will try to make a contact with the user and we will return $600K in fees collected from the transaction.

The key takeaway is that while DeFi should remain open and permissionless, allowing users to perform transactions freely, there are additional guardrails the industry can build to better protect users. Our team will be investigating ways to improve these safeguards going forward.

Seeing a few such cases in the market. The token → equity / tokenised equity pipeline will be interesting to follow.

What will "going public" look like in the future? IPO on @NYSE or @NasdaqExchange or issue via @OndoFinance or @SuperstateInc or maybe a new mechanism emerges?

Across Protocol wants to become a private company 👀

@paradigm-backed @AcrossProtocol posted a temperature-check proposal exploring a move from a DAO to a U.S. C-corp where ACX holders could exchange tokens for equity.

If approved by the community, holders could either

• exchange ACX for equity at a 1:1 ratio, or

• redeem tokens for $0.04375 in USDC, a 25% premium to the one-month average price.

ACX is already up over 33% since the proposal.

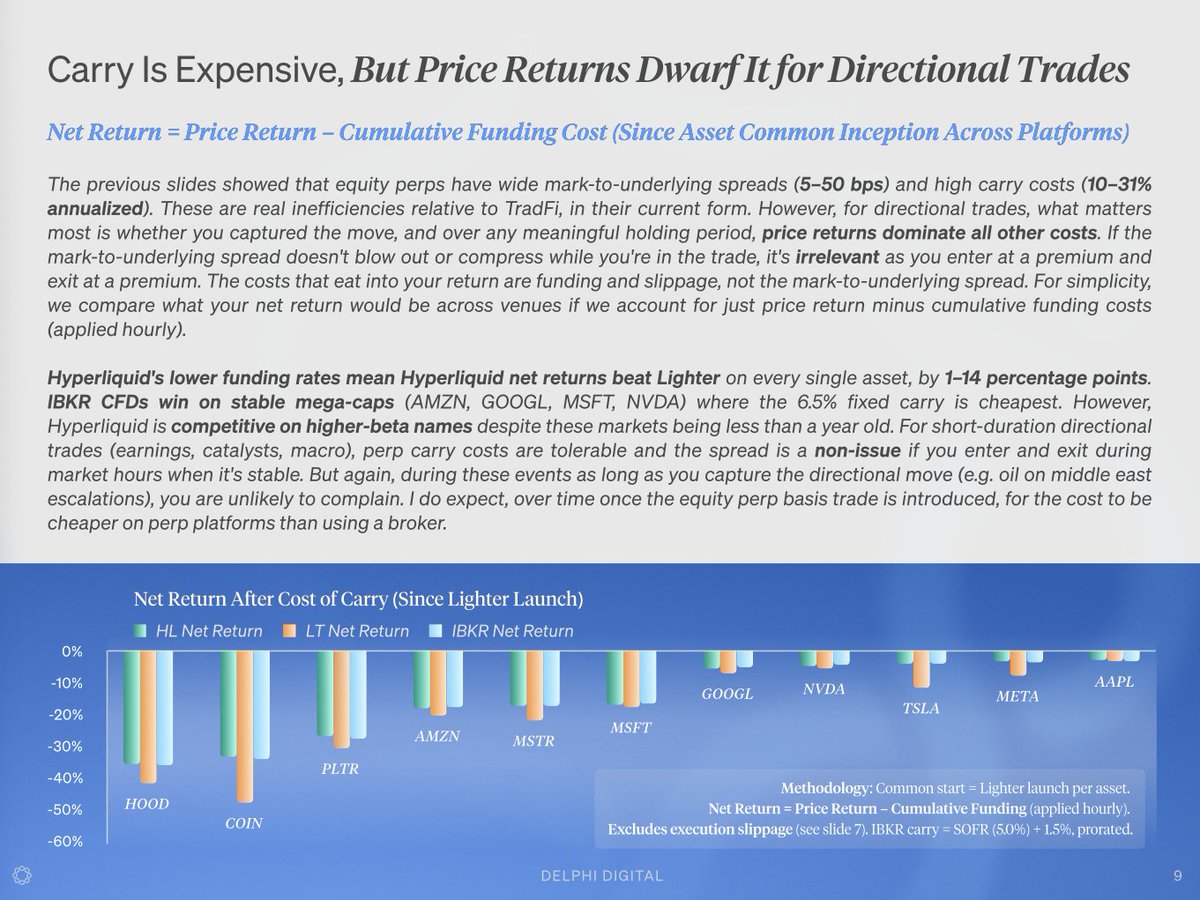

Equity perps continue to get a bad wrap by most people and the common critique is that funding is expensive, order book depth is bad, and the mark-to-underlying can be incredibly volatile at times. And I would have to say that all of these are largely true today.

Equity perp funding runs 11-31% annualized while IBKR CFDs cost 6.5%. @HyperliquidX & @Lighter_xyz order books are 10-100x thinner. So yeah, if you froze markets today and assume no innovation, the picture is pretty dire but I think if this is the future you subscribe to you forget about what just happened last year with the crypto perp basis trade.

The other hidden cost people fixate on is the mark-to-underlying spread. Initially I thought this was an incredibly high hidden cost but after digging into it more I don't think it really matters all that much. It is more akin to a closed-end fund premium, similar to what ETHE was for a period of time.

For traders, assuming you enter and exit at a similar spread, it isn't a cost. It is just something to be mindful of, especially if you tend to be an emotional person who just apes.

And despite all of this - the high funding, the thin books, the spread noise - for directional traders none of it really matters if you capture the move.

So what will close these gaps and inefficiencies? I think it is quite obvious that it will be the same thing that closed the gap and inefficiencies for crypto perps, which was the basis trade.

Before BTC spot launched on Hyperliquid, BTC funding averaged ~18% annualized, and within months it compressed to ~9%. ETH followed the same arc. Nearly 50% reduction in carry cost driven by one change that allowed arbitrageurs to collect interest rate-agnostic yield by going long spot and short the perp. This flow deepened the order book, anchored the price to the actual underlying assets, and compressed funding.

Equity perps today look like crypto perps in 2024. Everyone had the same critiques that funding was too expensive, books too thin, and too much basis risk. And for funds this really did matter and kept many from using these product. And then spot launched and all these inefficiencies were quickly fixed. The same is likely to happen with equity perps. We have the NYSE moving towards 24/7 trading, which will help. We have US regulatory clarity coming this year, which will help. And we even now have the CFTC chief explicitly talking about clearing a path for U.S. perps.

Introducing the Arbitrum Mentorship Program.

An eight-week program starting April 13th, where 15 early-stage teams get access to:

- A clear path from idea to launch on the Arbitrum platform with infra guidance, ecosystem support, and distribution channels

- Hands-on mentorship from leading Arbitrum ecosystem teams and builders like @RobinhoodApp Chain

- Curated investor access with sessions and warm intros to top venture firms

Plus, a chance to win a share of $100K in awards at Demo Day.

If you're an early-stage team at MVP, pre-seed, or seed, apply today:

https://t.co/Apmsmoty9G

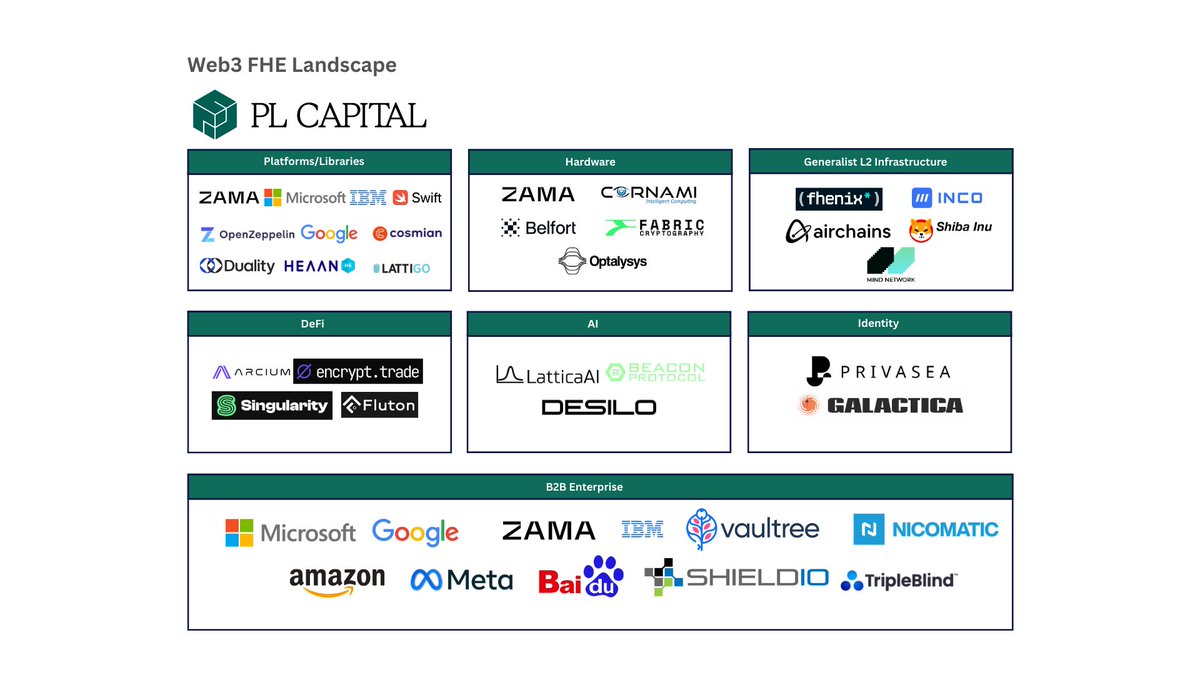

Crypto holds the key to quantum resilience, yet this is often overlooked. At @plcapital we've made several bets in the space (denoted by an *) particularly around FHE. We consider FHE a bet on quantum resilience 🧵