This is not a robotics thesis. It is a funnel.

Slick video, charismatic marketer, “why I bet my career on robotics.” He works for $BOT. RoboStrategy, the closed-end vehicle Andrew Kang now runs and openly brands the “MicroStrategy of robotics.”

Same playbook: a committed equity facility that only works if the share price stays bid and retail keeps showing up to absorb the issuance. The content is the top of the funnel. You are the liquidity.

We traded millions of dollars of converts on the real robotics names in the late 2010s, mostly within a convertible arbitrage mandate, not fundamental stock-picking. Which is exactly why we can point at the honest alternatives here, the ones nobody is cutting a hype video for, because there is no salesman making big bucks dumping them on you.

If you want robotics exposure, the honest version is already listed in Tokyo. FANUC (6954), 20%+ operating margins through full vertical integration. Keyence (6861), asset-light, ROE most software firms would kill for. Yaskawa (6506), the servo muscle behind half the world’s arms. The Japanese Big Five ship 40%+ of global industrial robots. These are priced for competence, audited for decades, and you can size them without praying a NAV premium holds. Dull. Real. Yours at a clearing price.

And if you actually want the convexity, the asymmetric leg, it is one layer down in the actuation supply chain, not in a closed-end fund. Harmonic Drive Systems (6324), Nabtesco (6268), the strain-wave reducer makers. A humanoid needs roughly 20 harmonic drives per unit, which makes precision reducer supply the binding constraint on the entire scaling story. That is where the torque is. That is also where you get your face removed if the shipment curve disappoints. Omdia has 2025 humanoid shipments up ~480% to ~13,000 units, real growth, and a rounding error against the valuations now leaning on it.

So here is the actual choice. You can own the cash-generating incumbents directly, at a price, with no wrapper skimming you. You can own the actuation convexity directly, eyes open, and underwrite the humanoid curve yourself. Or you can buy a single ticker at a premium to its own book, structured so the manager can print on your ‘enthusiasm’, and call that a career bet.

Robotics is real. The compounding is real. The funnel is also real, and it is looking for your money.

The edge was never finding the names. The edge is knowing who is selling, and to whom.

We’ve just raised $175M, in a round co-led by @paradigm, @a16zcrypto, and @RibbitCapital, the largest raise DeFi has ever seen.

Credit is the bedrock of our civilization, but the infrastructure underneath is fragmented, extractive, and closed to most of the world. That is what @Morpho is here to change.

Morpho is building the open credit network for the world. The global credit market is $ 200T. We are building the infrastructure layer that will move it onchain, and every institution, fintech, and bank that wants to participate in the next era of finance will connect to this network.

After four years of being heads down building Morpho, we now count more than $11B in deposits and integrations with leading financial institutions including @Coinbase, @Binance, @FireblocksHQ, @SG_Forge, @krakenfx, @Bitwise, and dozens of others building on Morpho to offer better products to their users. But this is just the beginning.

This raise will allow us to accelerate: activating the global credit network at scale, building the go-to-market engine to match our ambition, and bringing more institutions onto the network faster.

Having any kind of onchain strategy in this era will mean going through Morpho at some point. Reach out and let's talk. And if you want to help build the open credit network for the world, we have plenty of open roles.

Let’s fly 🦋

I cringe when I hear “I missed [X]”

Companies that achieve high market caps get there for good reasons that usually allow them to continue to compound growth. Past success is one of the best indicators of future success. Better leadership/teams = Better decisions/execution. Winners develop moats around talent, economies of scale, network effects, brand, regulation, IP, etc

Winners win

this clip is like the ideal mental state the powerful algorithm want us to be in

cat has mentioned this before, an ideal algorithm, for maximum shareholder profits, is an algorithm that makes everything else other than itself, such as going outside, seem boring, or even scary

i have different interpretation that fits the data in the article. the authors found it takes 2 blocks before hyperliquid fills have price information (~700ms) but hyperliquid provides other price information: the orderbook/best-bid/offer and gossip

if best bid/offer rather than fills is the metric for discovering prices, hyperliquid discovers prices every block

we can fill into (1) arbitragers who are trying to pick off stale quotes and (2) non-arbitragers who are willing to execute against the latest quote

hyperliquid batches transaction into blocks, prioritizes cancels/ALO then emits execution results (fills). whereas lighter adds 300ms to all taker orders and executes trades continuously

on hyperliquid, the arbitrage fill signal would be strongest at the first block, and fall off in later blocks

vs lighter, where any signal from arbitragers picking off stale quotes would be at least 300ms after binance and fills from 0-300ms would be dominated by non-arbitrage (2)

if we filtered out arbitrage transactions, i think we would find hyperliquid non-arbitrage fills do discover prices

and hyperliquid gossip should allow latency sensitive users to discover new prices even before transactions are committed

we could view the arrakis article as a measurement of stale quote arbitrage on hyperliquid

the natural followup question would be, does lighter have less stale quote arbitrage?

it wouldn't surprise me if lighter has less arbitrage because they continuously execute trades which minimizes jitter

the reason for this could be that hyperliquid executes and prioritizes cancels in blocks: even with cancel priority, if the price moves close to block a boundary an arbitrager can still land first, especially with write priority

the counter-factual would be we see a spike of lighter correlation to binance at 300ms which i dont see in the article

In 2022 Luna was offering 20% yields on $14b

They collapsed with about 40 days of runway left in May 2022

This post was made when they had about $400m in reserves left

$STRC is offering 11.5% on $15.5b

They have about 6 months of runway left

MSTR currently has about $871m in reserves left

History doesn't repeat, but it sure as hell rhymes

Saylor’s sell of 32 BTC yesterday is percolating through today with STRC depegging down to 96s. It is becoming more and more likely that STRC will not pull to par this month.

Saylor has backed himself into a corner. The sequencing of his actions has been, to say the least, incredibly suboptimal. He first established a ~22 month div reserve, only to deplete a quarter of it with further issuance. Note that he could've issued STRC responsibly, setting aside 1-2yrs of divs as he sold. Instead he aped the full raise qty into BTC. He then used another 2/3 of it to buyback converts, which were not even due this year or next, with no communication around topping the reserve back up.

The only "out" for his actions was that he was going to use this month's STRC issuance to replenish reserves, but that would be highly inconsistent with his previous behaviour.

Something needs to give here, whether it's the common, the prefs, or BTC. The longer run optimal choice for him is to give up on the prefs but I am not convinced he'll go that route just yet, hence the selloff in coins today.

STRC alone is 1.2bn of annual div obligations. While he could sell 1 large clip of BTC down to 60k and fund it for a year, if he believes he will get minimal issuance out of it for the next 1-2 years, then why would he bother? By the time the next bull market rolls around in, say, 3 years, the market will have forgotten and forgiven the transgression of a dividend pause.

Funding the reserve is only worth it to inspire confidence in the product insofar as his ability to extract dollars out of it, and it's clear the market thinks he's tapped now.

I think there's a >50% chance we see sub 60-70 in the product by September.

Case one: Strategy (Nasdaq: MSTR).

In August 2020, Strategy began buying Bitcoin. BTC value per diluted share: ~$2.34.

Today, BTC value per share: $164.71

Net of Credit/Preferred Shares: $129.53

That’s ~55× in 5.7 years.

Important note:

Strategy's average Bitcoin buying price is roughly $75,500. Bitcoin today is roughly $77,000.

They've made marginal returns on holding Bitcoin itself, yet net BTC value per share grew ~55×.

To deconstruct MSTR’s NAV/Share returns:

~3% came from Bitcoin price going up.

~97% came from MSTR issuing shares above NAV (proceeds were then used to buy more BTC).

If Bitcoin dropped 50% to ~$38,500, Strategy would face a large loss on their BTC NAV. Net BTC value per share would be ~$27.7, ~12x greater than the original BTC NAV per share. The company would have lost money on its investments, but retained returns from accretive share issuance.

In the scenario that Bitcoin doubled, the net BTC value per share would rise to $294.24. In this scenario, the company would have achieved substantial returns from both its investments and also accretive share issuance.

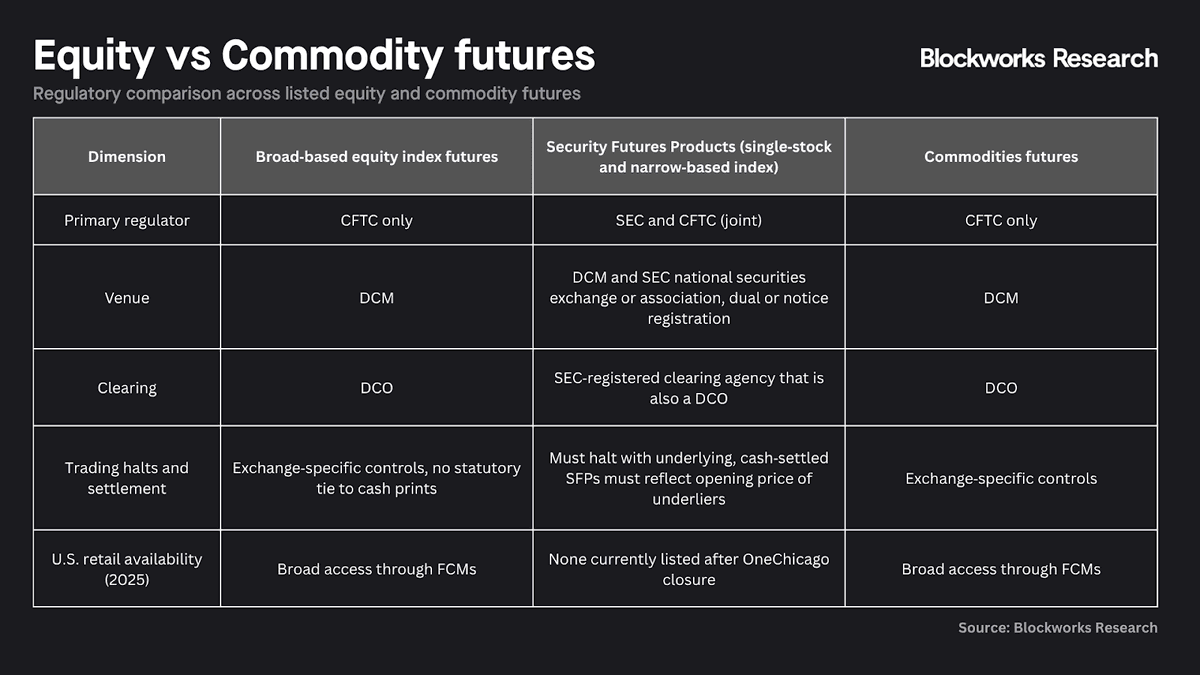

Perpetuals have no expiry and never physically deliver. In the U.S., that pushed them into the futures framework: DCM execution, DCO clearing, FCM intermediation, and CCP-style margining.

To be compliant, U.S. perps had to take two steps back to fit this legacy system. For example, instead of simply listing a crypto-native perp, Coinbase Derivatives acquired a DCM, worked through Nodal Clear, and structured its product as a five-year, cash-settled futures contract, with funding handled through clearinghouse cash adjustments.

This framework therefore created a lot of complexity:

-Exchanges can’t list any asset they want. They need to be a DCM, acquire a DCM, or list through one.

-Expiries, funding, and settlement mechanics need to be adjusted to fit legacy infrastructure.

Importantly, it structurally prevents brokers from using exchanges like Hyperliquid that do not meet the legacy criteria of a DCM.

While this new order does not remove those complexities, it does allow a true no-expiry BTC perp instead of the five-year expiry workaround.

Still, it points to the CFTC genuinely being willing to innovate and make perps fit into existing frameworks. Over time, hopefully that framework expands to also include crypto-native exchange layers like Hyperliquid as true market layers.

Today we reduced headcount by 22%. The business is the strongest it's ever been. So I think it's important to be direct about what I'm seeing and why.

First, I made this decision and I own it. I did it because the way to operate at the highest level of productivity is changing, and to win the future, ClickUp needs to change with it.

Second, this wasn't about cutting costs. Most savings from this change will flow directly back into the people who stay. We'll be introducing million-dollar salary bands. If you create outsized impact using AI, you'll be paid outside of traditional bands.

Most importantly, I have the deepest gratitude for those affected. We're doing this from a position of strength specifically so we can take care of people properly. Everyone affected receives a package aimed at honoring their contributions and easing the transition.

I only see two options: wait for this to play out gradually in the market or be honest about what I'm seeing and act proactively.

THE 100X ORGANIZATION

The primary change is that we're restructuring around what I call 100x org. The goal is 100x output. The roles required to build at the highest level are fundamentally different than they were a year ago.

Incremental improvements to existing systems won't get us there. We need new ones. That means creating enough disruption to rebuild rather than iterate on what's already broken.

The common narrative is that AI makes everyone more productive. It doesn't. Many of the workflows of today, if left unchanged, create bottlenecks in AI systems.

These roles will evolve. But waiting for that to happen naturally means falling behind now.

The 100x org is actually heavily dependent on people - infinitely more than today. This is only possible with 10x people that have embraced and adopted new ways of working.

THE BUILDERS, AGENT MANAGERS, AND FRONT-LINERS

— THE BUILDERS: 10X ENGINEERS

I don't think most companies have internalized what's actually happening with AI in engineering. The common narrative is that AI makes all engineers more productive. That may be true in isolation, but at an organization level - that is the farthest thing from reality.

Here's what we've validated recently at ClickUp: the great engineers, the ones who can orchestrate, architect, and review, are becoming 100x engineers. They're not writing code. They're directing agents that write code. The skill is judgment.

AI makes the best engineers wildly more productive, and everyone else using AI slows these engineers down.

Think about it - the bottlenecks are (1) orchestration - telling AI what to do, and (2) reviewing - what AI did. Everything is leapfrogged and no longer needed.

So who do you want orchestrating and reviewing code?

And how do you want your best engineers to spend their time?

If your best engineers are spending time reviewing other people's code, then this is inherently an inefficient bottleneck. These engineers can review their agent's code much faster than reviewing human code.

The new world is about enabling your 10x engineers to become 100x.

The wrong strategy is to push every engineer to use infinite tokens. Companies doing this are celebrating 500% more pull requests. But customer outcomes don't match the volume of code being generated.

I call this the great reckoning of AI coding, and every company will face this soon if not already.

More code is just another bottleneck to the best engineers, and ultimately to your company's impact as well.

— THE BUILDERS: 10X PRODUCT MANAGERS

Product management and design roles are merging.

Designers that have customer focus, become more like product managers.

And product managers that have intuition for UX become more like designers.

The bottleneck of user research is gone. It takes us just one mention of an agent to kickoff research and analyze results.

The bottleneck of product <> design iteration is also gone. The product builder iterates on their own, along with agents and skills that ensure alignment with quality and strategy.

Also controversial today - I believe that the wrong strategy is to have your PMs shipping code - that just introduces another bottleneck that the best engineers will waste their time on.

To be clear, PMs should be coding but they should do this in a playground to iterate, validate, and scope. That code should not go to production.

Everything outside of managing systems, orchestrating AI, and reviewing output becomes a bottleneck.

That's why the other roles that are critical along with these are the systems managers (to reduce bottlenecks) along with a bottleneck you can't replace - customer meeting time.

— THE SYSTEM MANAGERS

Ironically, the people that automate their jobs with AI will always have a job. They become owners of the AI systems - agent managers. We have many examples of these people at ClickUp.

The underlying systems in which we operate are absolutely critical to get right. I think most companies are delusional to think they can iterate on existing systems and compete in this new world.

You must create enough disruption so that old systems are deprecated entirely. If there's any definition for 'AI native' that's what it is.

— THE FRONT-LINERS

In a world that will become saturated with AI communication, the human touch will matter more than anything to customers.

This is a bottleneck that you shouldn't replace - even when agents are high enough quality to do video meetings.

One-on-one meeting time with customers is something that shouldn't be automated. The systems around the meetings should be - so that front-liners spend nearly 100% of their time with customers.

REWARDING 100X IMPACT

In a world where companies are able to do so much more with less, where does that excess money go?

In our case, much of the savings in this new operating model will flow directly back to those that enabled it.

We must reward people that create productivity accordingly. This aligns incentives on both sides. Plus, in a world where your best people create 100x impact, you can't afford to lose them.

You should aim to retain these employees for decades. The context they have and their ability to efficiently orchestrate and review will be nearly impossible to replace.

Compensation bands of today should be thrown out the door. We're introducing $1 million cash/year salary bands with a path available to nearly everyone in the company if they produce 100x impact by creating or managing AI systems.

THE FUTURE

Nearly every company will make changes like these. The ones that do it proactively will define what comes next.

The future is not fewer people. It's different work, new roles, and better rewards for those who embrace it. We're already seeing entirely new roles emerge, like Agent Managers, that didn't exist a year ago.

ClickUp is positioning to lead this shift, not just internally, but for our customers too. I've never been more certain about where we're headed.

Three years ago today, on May 20th, 2023, I started compiling CitriniResearch’s first thematic primer “Artificial Intelligence: Global Equity Beneficiaries”.

The thesis was simple - if a bit controversial back then - AI compute demand would go beyond lifting just Nvidia, the massive scaling of data center infrastructure would mean that valuations in most of the semiconductor sector (at the time reflecting COVID supply gluts & recession fears) were far too low.

When I wrote this, SMH was still in a 30% drawdown from its 2021 highs. Because it would be far too difficult to predict what AI looked like in 5 years, I decided the best risk reward was in the beneficiaries of AI Capex spending - Phase 1, or the “global data center hyperscaling”, was the bottleneck for everything else.

The best risk reward was indeed in the data center infrastructure, and I got most of that right (as expected, the further in the future predictions were shakier). It makes me extremely proud to go back and read this piece - the mark of truly good work is that it is enduring. A subscriber could have gone and re-read this at any point in the past three years and found solid ideas.

It’s free to go back and read it, keep in mind this was published in May 2023.

It calls for outperformance in GPUs, Memory, Optical Interconnects, Semicap, Power Density, Cooling, Memory Testing and more. All 1-2 years before most of the trades became consensus. Nearly everything that we said would outperform in the first phase of the AI trade has done so, to a massive degree.

Some of the best performers out of the names that were highlighted in this piece:

Applied Optoelectronics +6850%

SK Hynix +1800%

Vertiv +1450%

Hanmi Semi +1435%

CRDO +1160%

My original goal was to publish just three thematic primers on the trends I thought would define the decade: AI, peptides and government spending.

However, those themes required more coverage. The AI trade evolved, the fiscal trade became more important than ever. Three years later, I’ve parlayed the early success of our work to build CitriniResearch and its team of analysts to produce the kind of equity research I would want to read.

https://t.co/pVv4ifWsmj

Who remembers Morpho Optimiser?

Here's how you'd build a better one on Euler today. 👇

And create an interest rate swap market on top.

What does an Optimiser do?

On most lending protocols there's a spread between the lend and borrow rate. It emerges primarily because of the target 90% utilisation rate, which leaves breathing room for lenders to withdraw, and partly because of the protocol fee on borrower interest (typically 10% if the fee switch is on).

Borrowers pay 5%.

Lenders earn 0.9 * (1 - 10%) * 5% = 4.05%.

An Optimiser matches lenders and borrowers peer-to-peer somewhere in the middle where possible, and reverts to the variable rate pool when not.

Borrowers pay 4.5% (10% cheaper).

Lenders earn 4.5% (11% more yield).

Both are strictly better off if they can lend and borrow peer-to-peer.

Extra yield

It can get even better for borrowers on Euler than on a vanilla Morpho market.

The collateral they deposit sits in an Euler vault rather than idle, and can earn yield via cross-collateralisation when there's demand to borrow it.

For example, a borrower posting WETH as collateral for a USDC loan can have that WETH lent out to wstETH holders looping to capture LST yield. The WETH interest then offsets the cost of the USDC loan.

If that yield runs at even 1%, the effective borrow cost drops to 3.5%, a 30% reduction over regular Morpho market borrowing. 🤯

How to build

So how do you build this on Euler today?

Lenders deposit USDC into an Euler Earn vault. The Earn vault has two strategies: Morpho USDC/WETH (variable rate), and an Euler USDC/WETH P2P vault.

We'll call the P2P vault's shares eUSDC-P2P.

When a borrower takes out a new loan they always borrow from the P2P vault, which pulls deposits just-in-time from the Morpho market.

Similarly, when lenders withdraw, liquidity is preferentially pulled from the Morpho market.

The P2P vault gets its rate (call this the matched rate) by reading the IRM on the Morpho market and splitting the spread between lenders and borrowers.

It can do this because it's designed to be 100% utilised at all times. Effectively a pool of P2P loans. When a borrower repays, the excess deposits are pushed back into the Morpho market.

Parasitic?

The Optimiser and its host have a parasitic relationship. A rational lender or borrower should always migrate to the Optimiser, all else equal including risk. The host becomes wholesale backstop liquidity while the Optimiser captures the prime matched flow. Its economics degrade and the pool drifts towards full utilisation, where it becomes structurally fragile.

Morpho Optimiser was originally built on top of Aave's monolithic pool. Morpho's own isolated markets are now liquid enough to be vulnerable to the same dynamic. I say vulnerable, because parasites can kill their host given a long enough time frame.

When Morpho first built on Aave, the Aave team were delighted they had a new integration. They didn't realise Morpho Optimiser was silently hurting them. Every matched borrower was a borrower whose interest no longer flowed into Aave's pool. Utilisation drifted up, rates got more volatile, and Aave was carrying the tail risk while Morpho Optimiser took the benefits.

It's a vulnerability all variable rate pool models share.

The fix: a secondary market for pool exits

The solution, in my opinion, is liquid secondary markets for pools. You need an interest rate swap market, so people can exit a variable rate pool via a swap instead of a withdrawal, just like exiting a bond early.

Fortunately you can build this on Euler too, thanks to a feature that allows any ERC-4626 compatible vault on Euler to be accepted as collateral for any other.

Introduce a new Euler variable vault, call it eUSDC-variable, that cross-collateralises the P2P vault. You can deposit eUSDC-P2P shares and borrow USDC from eUSDC-variable, or vice versa. Since the underlying asset is identical (USDC on both sides, with eUSDC-P2P just being a yield-bearing USDC claim), the LTV can be set extremely high. 95% is realistic.

The main difference is duration risk: matched and variable rates can diverge, so the share values drift apart.

Two things become possible.

First, anyone stuck in the P2P pool can borrow themselves out without waiting for a withdrawal. They deposit eUSDC-P2P as collateral, which earns the matched rate, and borrow USDC from eUSDC-variable, which pays the variable rate. Net carry per second is matched minus variable. They've swapped an illiquid matched position for a liquid variable one, paying only the spread.

Second, anyone with a view on the spread can take a highly leveraged position on it, going long or short, by swapping into and out of the two pools on leverage. You're trading the interest rate market directly.

Pretty neat, huh?

I left Euler back in January and my understanding is that the Euler team have plenty to be getting on with right now, so I don't expect this to be built by them any time soon.

But if anyone fancies giving it a go, I have a vibe-coded prototype ready to share.

Matched vault, custom IRM, EVC borrow router. About 30 lines of actually novel code on top of existing Euler and Morpho infrastructure.

DM me if you want a look.

The original Morpho Optimiser is what put Morpho on the map. No reason a successor couldn't do the same for someone else.

People keep confusing a bubble with “stocks go up and get overvalued”. A bubble is when when a prevailing trend and a prevailing misconception about that trend interact reflexively, each reinforcing the other until the gap between perception and reality becomes unsustainable.

A bubble is not when everyone realizes that right now every iota of AI demand eventually, at some point upstream, must move through memory OEMs. Nor is it when estimates continue rising because things are better than expected. And it’s not just when stocks trade expensive to historical valuations.

The reason behind the moves in the AI infrastructure layer so far have been simply that we don’t have enough. They’ve been driven by the fundamental reality more than the perception of the future. It’s why the bulk of the most bullish parts of this cycle have been lumpy and centered around earnings season when companies uniformly come out and confirm there’s still not enough. In the bubble, the reality is driven by the market - not the other way around.

Everyone keeps saying “people are gonna freak out if it’s not a bubble!”. I think that’s silly, we have a transformative new technology that needs crazy capital to fuel it coming to fruition, that has and always will result in a bubble as long as we have financial markets.

But if you want to call the top in a bubble, you need a much stronger view on what the misconception is and what negative catalyst forces broad perception to align with realizing it than you do on valuation.

Nobody buying SK Hynix tonight will remember how hated it was not too long ago. When I wrote the below in January 2024, the dominant narrative was about the inescapable memory glut. MU & SK had been flat to down for a year while NVDA had tripled.

But…something that this cycle has taught me is that being early is a double-edged sword in more than just the classic “risk a drawdown before it works” way. I held on to these names for a little more than 2 years, but it’s pretty clear now that I sold too early.

Now, despite a 500%+ return, I’m wondering if selling in February means I’ll have to withstand the mindfuck of watching them 10x again (by next Tuesday, at this rate). I’m already debating with myself whether I should bite the bullet and get back in or if doing so will align perfectly with the exact top.

I love this game, but good lord does it mess with your mind!