CFP. Author. Inventor. LIMRA Retirement Income Institute. Built GH2 EDGE™, patents pending. Wrote Maximize Your Medicare, and Maximize Your Retirement.

In October 2019, Linda Morales filed for Social Security at 62.

Her advisor said "turn it on to cover the gap."

Her benefit dropped 30% — permanent. By age 87, the cumulative loss is $187,340.

The advisor wasn't dishonest. He just never ran the numbers. 🧵👇(1/8)

https://t.co/hHwC2pu0bb

The catch: most of what softens it has to happen before — while both are alive and the wide brackets are open.

It's not fate. It's arithmetic. And arithmetic can be done in advance.

https://t.co/HY4Qh8BmH1

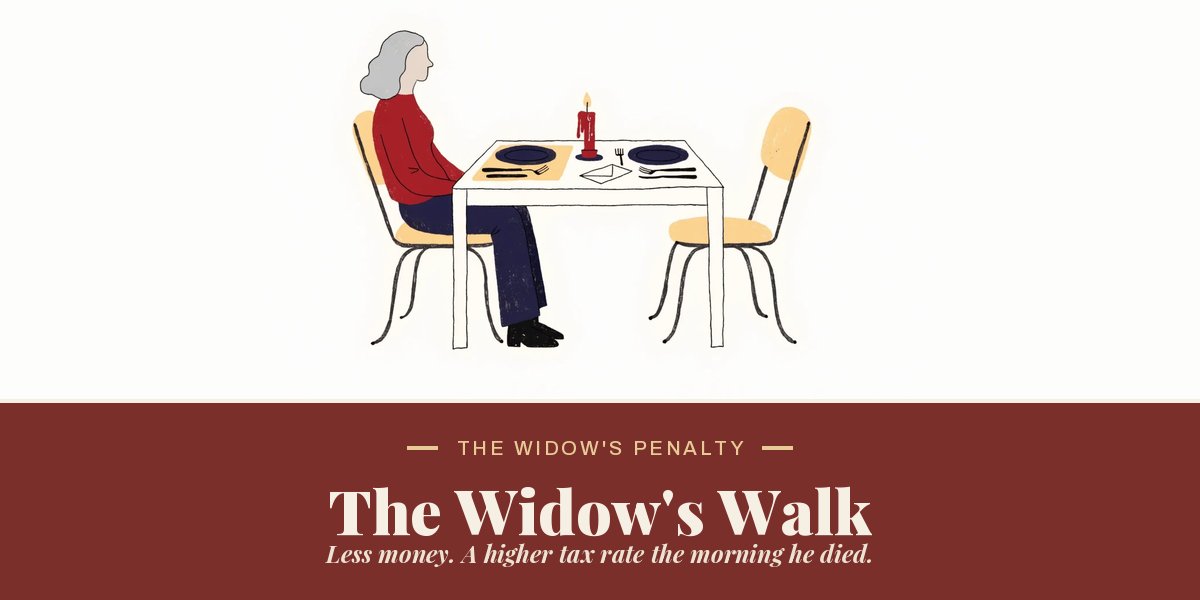

When her husband died, her income fell. Her tax bill went up.

It's called the Widow's Penalty, and almost no one says it out loud to the people it happens to. 🧵

https://t.co/9Yeu5kYNT3

Two Social Security checks become one. The brackets she shared as a couple cut nearly in half. The Medicare surcharge line drops too.

Less money, taxed at a higher rate — the morning she became a widow. She did nothing wrong. The rules just changed.

Shrey spelling 32 words in 90 seconds to win the Spelling Bee is the new greatest athletic accomplishment of 2026. I don’t even know how he said the letters that fast. Got a “Holy Mackerel” out of

@minakimes

@thoughtson_tech@ReadTheLion Agreed. People assigning a specific party/politician or attempting to find/promote an a la carte solution show how far off track the debate is. All said, difficult to accumulate the political will reqd to enact your recommendations.

A recent piece from 24/7 Wall Street discusses a significant decision faced by a 64-year-old single woman with a $1.1 million traditional 401(k) as she considers her bridge to claiming Social Security at age 70. The article effectively highlights various challenges she may encounter.

While the math and bridge concept presented are generally sound, and the awareness of IRMAA is accurate, the article concludes with a checklist of three actionable items for the week. However, this closing is crucial for reasons beyond the author's intention.

The checklist reflects the limitations of the available tools to address the household's actual problem. Each task is isolated, requiring different software, and fails to answer the overarching question posed.

Here are three areas where the article falls short:

- Regulatory regimes operate simultaneously rather than sequentially. The 2026 Roth conversion influences the 2028 IRMAA tier, which in turn affects the 2028 Medicare premium and the 2030 IRMAA tier. Checklists address these in order, but reality requires a simultaneous approach.

- Mortality is personal, not average. The article's break-even age relies on SSA cohort tables. Adjusting the household's longevity perspective by five years can significantly alter the optimal strategy.

- The Required IRR is the critical figure that remains unaddressed. It represents the minimum portfolio return needed for the plan to transition from infeasible to feasible.

For a deeper analysis, including questions to pose to your advisor instead of relying on the checklist, check out the full teardown on Substack.

Read the article: https://t.co/gnHCx7NpeE

**8/8**

*50 Retirement Mistakes That Cost Real Money* — out now on Amazon.

Each story shows the person, the decision, the cost, and the strategy that would have worked.

https://t.co/QDTVL7JsOm

In October 2019, Linda Morales filed for Social Security at 62.

Her advisor said "turn it on to cover the gap."

Her benefit dropped 30% — permanent. By age 87, the cumulative loss is $187,340.

The advisor wasn't dishonest. He just never ran the numbers. 🧵👇(1/8)

https://t.co/hHwC2pu0bb

**7/8**

Story 50 is the most important one.

The Murphys have a pension and Social Security that together exceed their expenses.

The optimizer ran their full grid. Its recommendation: do absolutely nothing.

Sometimes the answer is "stop worrying." But you only know that after you ask.

Retirement is just the first vertical.

The same architecture — coupled regulatory simulation at scale — applies to healthcare, education finance, state tax policy, housing, insurance.

Retirement was the hard one to build first. The next ones will follow.

#GH2EDGE

In 1994, William Bengen tested ~50 historical scenarios with one withdrawal strategy and one type of household.

He concluded 4% was a safe initial withdrawal rate.

That study became the foundation of how America plans retirement for the next 30 years.

For 4 out of 5 households, the textbook answer is the wrong answer.

Not because the textbook is bad. Because the textbook can't see them.

Same advice for everyone was never a planning choice. It was a computational ceiling.

The ceiling lifted.