Partner at Avenir, where I invest in startups.

Here to bring some analytical irreverence, while trying to add a little information to the world.

Views my own.

With so much froth in the market (some of it grounded, some of it... not), I took some time to remind myself what investing is / what it is for.

Feels completely irrelevant now- which probably means it is more relevant than ever:

https://t.co/IZIdml07kb

Every day for the next long while, I'm going to tear down a new public software company and highlight the AI risks/opportunities around it- products launched to date, top startups, key quotes from earnings calls, etc.

Day 32: Atlassian $TEAM

Peak share price: $458.13 (Oct 29, 2021)

Share price today: $71.55 (-84%)

EV today: $18.5bn

ARR today: $6.34bn

NRR: 120%+ (for cloud business)

EV/ARR: 2.9x

GAAP Operating Margin: -3%

EV/Run-rate GAAP EBIT: N/A

Headcount: 21,407 (+27% Y/y) - Although Alassian announced a 10% RIF and headcount declined in March/April- a SaaS rarity.

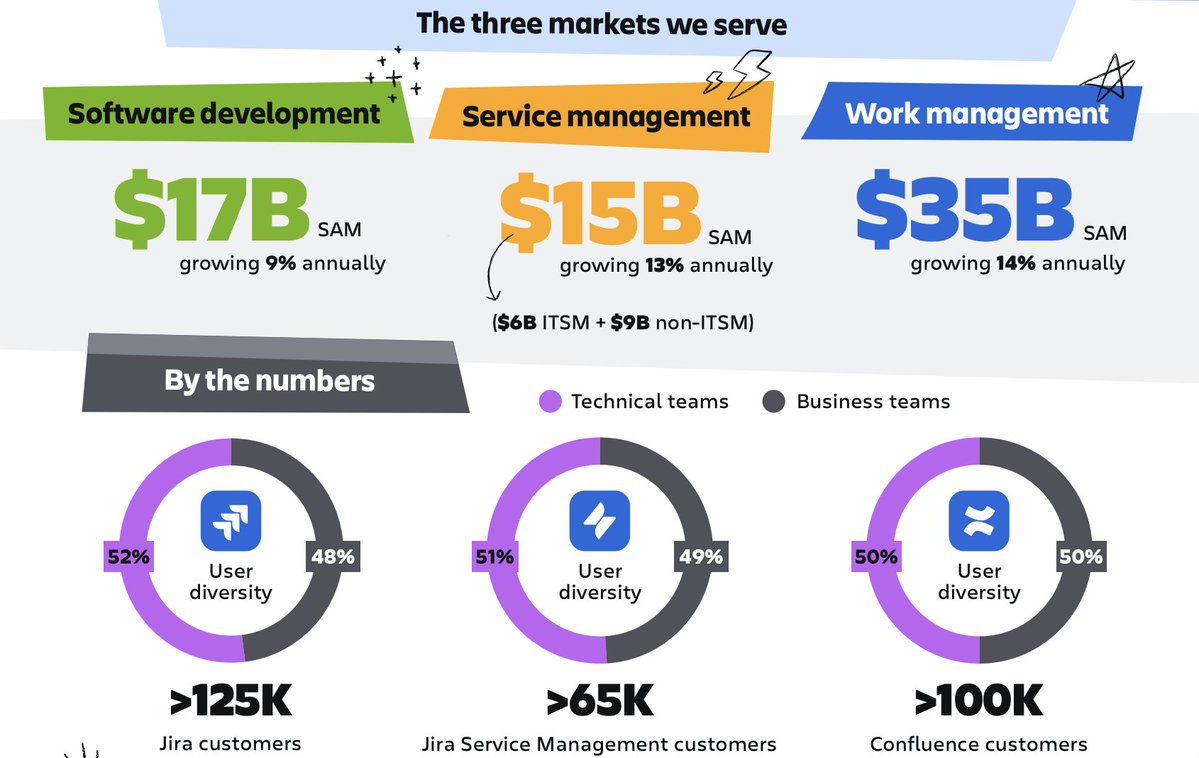

What Atlassian does:

Atlassian is the dominant platform for software teams to plan, build and operate software- issue tracking, sprint management, bug tracking, project management, etc.

Its core product, Jira, manages the above and also doubles as a wider enterprise operating system for managing ticket/issue-based workflows in departments like IT, legal, HR, etc.

It also offers Confluence, an internal wiki, Bitbucket, a competitor to Github/Gitlab, and various other products.

Key to understanding Atlassian's approach is that it took a relatively unique approach to selling software- Jira was available very, very cheaply (as low as $10/dev/year) and as such it reached ubiquitous usage with a remarkably low touch sales process. I remember the company swearing that it would never employ salespeople on its IPO roadshow- and while I think that was already technically false at the team, it highlighted the way rock-bottom pricing enabled widespread distribution and ubiquity. Today, aside from @linear, which has strong traction in modern companies/startups but is a small fraction of the size, Jira is the clear default for managing software development workflows within enterprises, with no close #2.

Also of note- Atlassian has gone through a relatively messy (but APRU increasing) SaaS transition, with cloud-based seats now accounting for 67% of revenue.

AI bear case:

The bear case for Atlassian has two planks:

1) SWE seat-count will decline, directly threatening its seat-based pricing model.

2) The way software is built will change fundamentally in a way that creates room for category disruption or obviation- as agents increasingly partner with humans to build software, a new system of record for managing the work will appear, perhaps built by Anthropic, OpenAI or some other AI for code vendor.

Beyond this, Atlassian has long had a reputation for being a relatively country-club-ish company with easy work-life balance and complications from having engineering split between the US and Australia. Management seems to have taken some steps to rectify this, but the ingredients to move quickly- a unified code base, simple product portfolio, obvious hero SKU, etc. don't seem to exist here.

Finally, Atlassian has historically been an SBC machine and runs at ~GAAP breakeven despite massive scale, limiting its ability to aggresively re-invest in the business.

AI bull case:

Atlassian is, without a doubt, the most scaled system of context for software today. Github/Gitlab have the codebase and history of changes, but Atlassian has the "why" behind the changes, the source of the issue/bug/etc. and plenty of context about how the team worked together to solve it. It also has a remarkable sticky ecosystem of plugins, integrations, etc. that is perhaps underappreciated and makes enterprise migration incredibly difficult.

The reality is, while AI for code accelerates the pace of software development dramatically, it is as important as ever to know WHAT to build, track what is being built, etc. As long as that is true, there is a clear place for Atlassian- and (perhaps) even a tailwind if I can remain the sinew between the humans involved in writing/managing code (and so far, they've shown no signs of going anywhere) and the agents that are amplifying their capabilities.

AI traction:

Atlassian hasn't disclosed any meaningful revenue/financial contribution from AI. Just some vanity stats.

Adjacent startup summary:

@linear is the most relevant startup, with 223 employees (+66% Y/y). Pre-AI, it was doing exceptionally well with ultra-modern companies but not really on a trajectory to upset Atlassian near-term- it will be interesting to see if AI can change that, as Linear has been predictably aggressive and tasteful about adding AI to its product.

The other biggest threat about be an AI for code platform getting so ubiquitous and embedded that replacing Atlassian feels like a natural progression. At present, Claude Code and Github Copilot are the two plausible contenders, but neither has moved aggressively in this direction yet.

Management Quotes:

"Rovo surpassed 5 million monthly active users of our AI capabilities. We're seeing firsthand every day how AI is transforming the way that work gets done, and we are directly benefiting as a business."

"When we look at the thousands of customers in our software teams using AI code generation tools, we found that they create 5% more tasks with Jira, have 5% higher monthly active users and expand their Jira seats 5% faster than those who don't use these AI coding tools."

"In less than 3 quarters, more than 1,000 customers have upgraded to our main AI monetization driver, the Teamwork Collection, purchasing more than 1 million seats to get the best AI platform and many more AI credits for their agents."

"The Forbes AI 50. I didn't want to cherry pick some stats. I just drew that over to my data science team and said how many of these -- the hottest startups -- AI start-ups in the world are our customers today? 60% are already our customers today."

Commentary:

What is remarkable in retrospect is that Atlassian, with a long history of bottom-up adoption, found no way to create a prosumer-y AI upsell opportunity while tens of billions of value were created right new to it by vibecoding tools, Claude Code, etc. At a minimum, it is hard to argue that this doesn't represent a colossal failure of imagination.

That said- the core business is strong, net retention is ticking up, and the AI bear case remains (as it is for so many software companies) more hypothetical than imminent. It's hard to envision a world anytime soon where there isn't a system of record for tracking software issues/bugs/sprints etc. and (thus far) it is hard to see how anyone is on a course to displace Atlassian as that system. That buys them time to adapt and find a way to harness AI to their benefit- otherwise they risk remaining as a decreasingly relevant part of the software development stack as agents proliferate and the importance of human coordination in managing software builds decreases.

@faggy_mcbutt Interesting- easy tweak. But overall the whole app only focuses on a relatively small set of “marginal” hands.

Wdyt, should I expand hand types?

Just spent an hour on an update to BetterAtBlackjack.

I'm confident this is now the best/fastest way to improve: only marginal set-ups, AI coaching, and a tracker of hands you've historically struggled with, etc.

Try it and lmk what you think:

https://t.co/LZCOnCwVby

There are a shocking number of investors who don't use Claude Code, Codex or even Cowork to any sophistication (connectors, etc.) and yet are expressing confident takes on AI.

Analogous to being long on the internet in 1999, but only based on what you've read in the newspaper.

@AspiringChef1 And yet, if it were possible for them to somehow be deeper on the chemistry/science, they should be in order to get an edge in an adversarial system, I'm sure you would agree.

AI COUNTER-NARRATIVE: Support hiring is growing, not shrinking.

US support job postings are up 9.4% YoY. Only 20% of companies actually cut headcount because of AI (Gartner).

The easy stuff AI automates took the least amount of time. On the hard stuff, AI is an accelerator, not a replacement.

We had a fun AI discussion at Avenir this morning.

To support that, I built a little "choose your own adventure" site with 4 toggles that lead to 16 scenarios + investment implications.

Check it out: https://t.co/zf8jxlc7rH and let me know what you think.

Feedback welcome!

Your estimate public software go-forward returns should be *lower* after the recent recovery in share prices.

There’s been no fundamental data point to drive it- the bull/bear case are the same as a few weeks ago.

If higher, you are letting prices tell you what to think.

I just disagree with this. I know it is hard. But if you anchor yourself in valuation, you actually have a prayer of holding through drawdowns, etc.

It's the only way to actually invest.

Had to write a whole essay to remind myself of this:

https://t.co/mUCyjbU0ax

Classically, this is true

But we are not in Kansas anymore.

Valuation is literally meaningless in a large number of cases. Prices are being set by a mob who can't read.

One day this might change but fr now, uncle 'Mo is the mayor of the town.

I agree with this! I say it mostly for myself.

I really do believe that the second you lose the "I might own this forever" mindset, you're at the mercy of forces beyond your control and you've left investing for something else.

Which is fine! Just have to be aware what game you're playing

@SethLiebert People who really believe in the businesses hold during drawdowns.

Yes! Because if the business is real, the odds of a recovery are dramatically higher.

@ck3xyz There are many very, very advanced investors- both in VC and in HFT/HFs.

Others have just sat out, feel ashamed of it and aren’t willing to invest the time to catch up.

Unfortunately getting harder and harder to fake it in conversations if you’re still a vanilla chat guy.