Passive investing might become a bit like flying on Ryanair, where you show up at the airport with your dirt-cheap ticket and all of a sudden you get hit by a ton of fees you didn't anticipate.

The case for being a passive investor is still very strong. But the case always rests on fees. If index providers start adding hidden fees for passive investors by stuffing the index with overvalued stocks that haven’t seen real price discovery, the case for passive investing will inevitably become less compelling.

Here's my latest on the two-cent blog. Who's looking out for passive investors?

https://t.co/MOzWihz58a

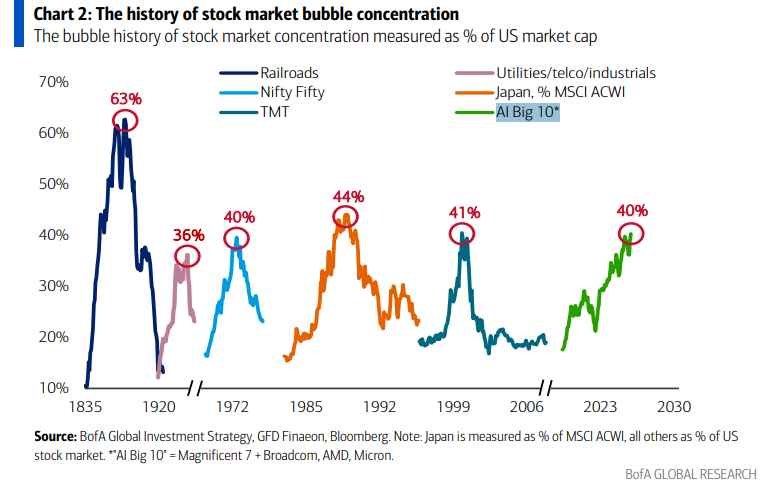

In 1972, there was a list of stocks you were supposed to buy and never sell.

They called them "one-decision stocks." You made one decision, to buy, and held forever. The quality was so obvious, the futures so certain, that price was considered irrelevant.

The Nifty Fifty. Coca-Cola, Disney, McDonald's, Xerox, Polaroid, IBM. The best companies in America.

At the peak, the group traded at 42x earnings, more than double the market. The most beloved names were worse:

– Polaroid: 91x earnings

– McDonald's: 86x earnings

– Disney: 82x earnings

– Avon: 65x earnings

Then 1973 arrived. Inflation. Rising rates. Recession.

As a Forbes columnist put it, "the Nifty Fifty were taken out and shot one by one."

– Coca-Cola: -69%

– Xerox: -71%

– McDonald's: -72%

– Avon: -86%

– Disney: -87%

– Polaroid: -91%, eventually bankrupt

These weren't bad companies. Most were genuinely great businesses that kept growing earnings for decades.

The companies were fine. The prices were not.

Here's the part that should keep you up at night.

If you had bought the Nifty Fifty at the absolute peak and held for 25 years, you would have roughly matched the market. The quality eventually bailed you out.

But you had to survive a 50-90% drawdown first, while everyone told you those one-decision stocks were finished.

"Buy quality and hold forever" is good advice.

"Buy quality at any price and hold forever" has ruined more patient investors than any crash.

It was never one decision. It was always the price.

Reden wir über den Bitcoin-Bärenmarkt 2026. Für HODL-Veteranen ist es einfach ein Abschwung, auf den nächstes Jahr ein Aufschwung folgt, und für Trader ist eh jede Vola gut, egal ob die Kurse nach oben oder nach unten gehen. Aber was, glaubt Ihr, muss passieren, damit Family Offices oder Stiftungsfonds wie Harvard je wieder bereit sind, Millionen in ein Asset zu stecken, mit dem sie das allokierte Vermögen binnen Jahresfrist halbiert haben? Und nein, das ist kein FUD. Ich stelle nur die unangenehmen, kritischen Fragen, die man als Finanzer stellen muss. Manche dachten, dass Bitcoin 2025 Teil der traditionellen Finanzwelt geworden sei. Das steht durch diesen Bärenmarkt infrage

Danke für die tolle Aufbereitung. Das passt perfekt zu der Studie „The Active Side of Indexing“, die ich neulich analysiert habe. Die Grafik zeigt ja eigentlich, dass wer heute per ETF in den S&P 500 investiert, de facto keinen „breiten, neutralen Markt“ mehr kauft, sondern eher ein Momentum Play auf die Mega Cap Techs.

Das ist per se weder gut noch schlecht, aber es zeigt die Illusion, dass rein passives Investieren derzeit nur Mitschwimmen ist, glaube das sollte man sich bewusst machen.

Mir kommt da folgender Gedanke: Wie lange hält diese historische Outperformance noch an, bevor möglicherweise ein „Reversion to the Mean“ stattfindet.

Wäre jetzt ein guter antizyklische Zeitpunkt, auf Equal-Weight umzuschichten, um von einer künftigen Aufholjagd der Marktbreite zu profitieren?

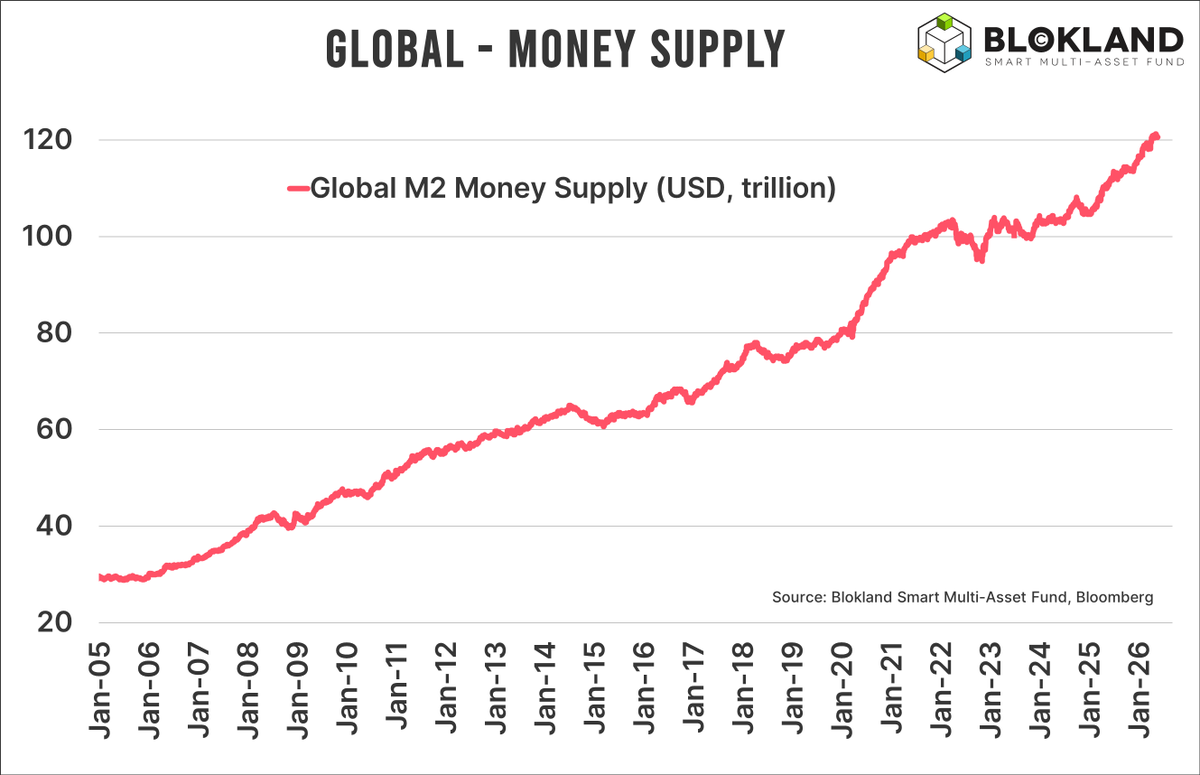

Global money supply is skyrocketing.

And this is without a crisis or major financial event.

Data on money supply is far from abundant and mostly fragmented, making it difficult to see what is happening at the aggregate level.

This chart shows you exactly that. Central banks, economies, governments, and markets are heading for an epic clash.

Markets want to push interest rates higher as inflation spikes again, confronting governments with their huge debt levels with a surge in interest costs. Meanwhile, to preserve the little credibility that remains, central banks are forced to adopt a hawkish tone, preparing for further rate hikes.

All this puts massive pressure on the refinancing machine. More than 70% of all financial transactions are about refinancing or rolling over existing debt. None of that goes into the real economy.

And this is exactly why money supply growth is at warp speed despite a major downturn. Even to prevent that downturn from happening, unprecedented levels of liquidity are required.

Libraries full of empirical data and studies have shown one thing: faster money supply growth almost always leads to higher inflation.

Buckle up!

THE GREATEST EXIT EVER 🚨

SpaceX will be the biggest wealth transfer in stock market history.

Not from rich to poor.

Not from poor to rich.

From passive ETF investors to SpaceX insiders.

You are not investing in SpaceX.

You are the exit liquidity.

@BcPoldi@GrowthMs U2

Rolling Stones

AC/DC

Cranberries

Nick Cave and the Bad Seeds

Geier Sturzflug

Depeche Mode

Bruce Springsteen & E-Street Band

Supertramp

New Model Army

(No ranking)

You may have noticed that the word for ‘night’ in many languages appears to be that language’s word for ‘eight’ with an ‘N' in front of it.

English: N + eight = Night

German: N + acht = Nacht

French: N + huit = Nuit

Spanish: N + ocho = Noche

Italian: N + otto = Notte

Portuguese: N + oito = Noite

⬇️