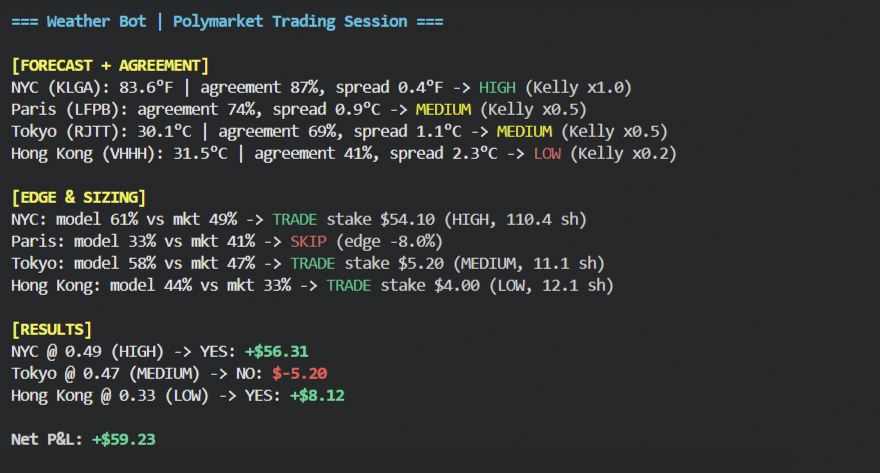

How a Profitable Weather Bot Works on Polymarket: Full Pipeline from Forecast to Order (BOT PIPELINE)

Most people think weather bots require complex AI and tons of code

In reality, top bots run on a simple, understandable pipeline that you can build over a weekend

> Core Pipeline

1. Market Discovery

Scans active temperature bucket markets

2. Forecast Ingestion

Pulls 3–5 models (ECMWF, GEFS, HRRR, NWS, UKMO).

Data must be for the exact resolution station

3. Calibration

Raw models have systematic bias. Top bots correct each model per city and lead time using historical residuals

Simple decaying average bias correction already gives a noticeable boost

4. Probability Calculation

After calibration, converts the ensemble into probabilities for each bucket

5. Edge Detection

Compares calibrated model probability to market price. Only trades when edge ≥ 8%

6. Sizing & Execution

Fractional Kelly + hard caps, limit orders, circuit breakers

> About Paid Models

Many top accounts use not only free sources (Open-Meteo, NOAA) but also paid ones (Visual Crossing Pro, Tomorrow, proprietary AI models)

Paid sources often provide better short-range accuracy and cleaner station data

A 0.5–1.5°C difference on short horizons can significantly impact edge in narrow 1°C buckets

Good balance: free ensemble for baseline + 1–2 paid sources for final calibration

> Why This Works

- Models update on schedule → edge appears predictably

- Calibration removes systematic errors

- Automation lets you catch hundreds of micro-trades per day

Many think the model is good and calculate probabilities immediately

Winners first fix the bias, then calculate edge

If you want the next post - I can break down how to do simple and effective bias correction on historical data

Save this post!

THE TEMPERATURE LADDER STRATEGY THAT TURNS POLYMARKET WEATHER INTO ASYMMETRIC EDGE (LADDER EDGE STRATEGY)

Most traders pick one most likely temperature bucket and hope it prints

Ladder traders do something smarter: they spread small money across 3–4 adjacent buckets so that whichever one resolves pays the whole stack

This turns weather markets into a positive-skew game where one correct bucket more than covers the cost of the losing ones

[why ladders work so well on short-horizon markets]

Models give a point forecast that falls into one bucket

But that point is often off by 1–3°C, sending the real temperature into a neighboring bucket

Buying the whole cluster cheap (ladder usually costs under $1) means you don’t need to guess the exact number

You just need the actual temperature to land in one of your buckets

[how to build a strong ladder in practice]

Example for Singapore (cluster 29–31°C):

- 29°C @ 0.2¢

- 30°C @ 15¢

- 31°C @ 35¢

Total: ~$0.50. One winning bucket at 100¢ makes the position profitable

[when this edge shines brightest]

- Transitional days when models disagree

- 24–48 hour horizon (D+1 and D+2)

- Volatile cities like Singapore, Miami, Tokyo, Shanghai

- Right after a fresh model run before the market reprices

Add an underdispersion filter (ensemble spread tighter than historical) and the win probability rises noticeably

Ladder + basic ensemble check is one of the cleanest asymmetric plays on Polymarket right now

Save this post!

Tail Risk Buying on Polymarket: How to Buy Extreme Buckets and Catch 10–20x When Everyone Else Is Scared (TAIL EDGE STRATEGY)

Most traders avoid far-tail buckets on temperature markets

Smart money does the exact opposite - they quietly farm the fattest alpha there with minimal risk

> Why Tail Buckets Are a Hidden Goldmine

Ensemble models (ECMWF, GEFS, HRRR) are almost always underdispersive - they draw too narrow a range of possible temperatures

The market is even more scared of extremes. As a result, the farthest buckets (hottest or coldest) chronically trade at 4–12¢, while real probability is often 18–28%

One good tail hit per month easily pays for dozens of small losses

> 4 Key Principles

1. Underdispersion Check

If the ensemble spread is noticeably narrower than historical volatility for that city and date - tails are almost certainly underpriced

2. Climatology Anchor

Check how many times in the last 10–15 years the temperature went into a similar extreme on that exact day

3. Consensus Filter

Only buy when at least 2–3 independent models show the possibility of an extreme. If all models are stuck in a tight corridor - skip

4. Position Sizing Rule

Small bets only: 0.5–2% of bankroll. Even if 8 out of 10 tails lose, one big winner more than makes up for it

> Real Example (London, EGLC)

• Max Temp tomorrow market

• The >28°C bucket was trading at 7¢

• Ensemble + climatology showed ~21–23% probability

• 36 hours later it resolved at 29.1°C → 100¢

• +1320% on the position

> When This Edge Works Best

• Strong heatwaves and cold snaps

• Transitional days with fronts (when models disagree)

• Tomorrow and day-after markets (D+1 and D+2) - underdispersion is strongest here

• Volatile cities: NYC, Chicago, London, Tokyo, Shanghai, Miami

Tail buying combines perfectly with near-resolution and calibration edges

It’s a positively skewed strategy: you rarely lose big, but when you hit - you win very fat

Many top accounts in 2026 are crushing it exactly thanks to systematic tail buying

Save this post so you don’t lose it!

How to Turn Ensemble Underdispersion into Consistent Profit on Polymarket Temperature Markets (BLACK BOX STRATEGY)

If you’re still trading Polymarket temperature markets using only a single number from GFS or ECMWF - you’re leaving one of the fattest and most sustainable edges of 2026 on the table

The real quant alpha on the 24–48 hour horizon isn’t in the temperature itself. It’s in Ensemble Spread and especially in Underdispersion - when the model shows a too-narrow range while reality is much wider

>Why This Works So Well on Short Horizons

On tomorrow and day-after-tomorrow markets, chaos hasn’t fully kicked in yet, so:

• Ensembles frequently underestimate real uncertainty (underdispersion)

• The market sees a “tight” forecast and heavily overprices central buckets

• Tail buckets (extremes) end up ridiculously cheap

This is a repeatable mispricing that happens almost every single day

> How to Exploit Underdispersion in Practice

1. Look at raw ensemble spread

GEFS (31 members) + ECMWF ENS (51 members) are your main sources

2. Compare the width of the distribution

• If ensemble spread is only 3–4°C but historically in this synoptic situation it should be 6–8°C → strong underdispersion signal

• When the model is “too confident” - tails are almost always underpriced by the market

3. Simple entry rule

High underdispersion + tail buckets trading below 12–14 cents = aggressive buy

Central buckets are usually overpriced in these moments

> Real example (NYC, max temp for day after tomorrow):

• ECMWF mean = 23°C, spread only 3.8°C

• Historical spread in this setup ~7°C

• Market pricing the >27°C bucket at 7 cents

Tail was heavily undervalued. These setups deliver excellent edge

> Mini-formula for your bot

dispersion_ratio = historical_typical_spread / ensemble_spread

if dispersion_ratio > 1.6 and tail_price < 0.13:

edge = high # enter

You can layer NGR (Non-homogeneous Gaussian Regression) on top - it quickly corrects underdispersion and makes probabilities much more honest

> When This Edge is Strongest

• Transition days (fronts, air mass changes)

• Cities with complex local effects (NYC, LA, Hong Kong, Cape Town)

• Day-after-tomorrow markets - where spread adds the most value

This approach barely depends on latency. You can even enter several hours after a new run and still keep the edge

Underdispersion + proper calibration is one of the few strategies that still works consistently in 2026, even after most latency edges have died

Save this post - you’ll want to come back to this black box strategy

$2,630/month on subscriptions. replaced everything with open source. now $0.

https://t.co/DgXsnDsbX6 -> weather mispricings. 6-hour METAR delay. ECMWF + HRRR. correct ICAO stations - not city centers, the airport stations each market actually resolves on. kelly sizing. 20 cities. $13 in - $4,082 out

https://t.co/I3DyFvUTif -> replaces TradingView Pro ($30/month). built by the TradingView team themselves. 14k stars. 45KB. HTML5 canvas

https://t.co/XrU8kCr7bk -> replaces Bloomberg Terminal ($2,000/month). every macroeconomic dataset the Fed publishes via free API

https://t.co/6GwIGo0Jia -> replaces backtesting platform ($100/month). NautilusTrader engine with custom Polymarket adapters. equity curves, P&L ticks, monthly returns, sharpe. actively maintained

https://t.co/dCtV7jolMO ->strategy reverse-engineering. 5 microservices. Redpanda event pipeline, ClickHouse, Grafana + Prometheus as a complete analytics stack

https://t.co/kSxmgsfDTu -> paper trading for AI agents. $10K fake funds, real order books, exact Polymarket fee formula, slippage tracking. MCP server. 657 tests, 100% coverage

https://t.co/Uim4UfHjVz -> reduces token consumption in Claude Code by 60-90%. single Rust binary. cargo test: 155 lines → 3 lines. one developer saved 24.6M tokens in 15 days

https://t.co/6avwvBdBHw -> replaces Claude Code ($200/month). 35k stars. built by Block (Jack Dorsey). works with any LLM. installs, executes, edits, and tests autonomously

before: $2,630/month now: $0

save this - you'll come back when you're tired of paying

A Anthropic liberou um workshop de 26 minutos ensinando como fazer prompts pro Claude de verdade.

Saber escrever prompts é o que separa quem usa IA de quem aproveita IA de verdade.

Quem fez o vídeo:

o time que construiu o Claude.

Legendei em português. Aproveitem.

@0xaporia this indicator has nuances, and definitely is not as simple as "buy the fear, sell the greed"

fun fact: in lower timeframes (30 or 90 day) the historical returns of buying extreme greed are BETTER than buying extreme fear

chart: 30 days BTC returns (y axis) vs F&G (x axis)

![AlterEgo_eth's tweet photo. THE TEMPERATURE LADDER STRATEGY THAT TURNS POLYMARKET WEATHER INTO ASYMMETRIC EDGE (LADDER EDGE STRATEGY)

Most traders pick one most likely temperature bucket and hope it prints

Ladder traders do something smarter: they spread small money across 3–4 adjacent buckets so that whichever one resolves pays the whole stack

This turns weather markets into a positive-skew game where one correct bucket more than covers the cost of the losing ones

[why ladders work so well on short-horizon markets]

Models give a point forecast that falls into one bucket

But that point is often off by 1–3°C, sending the real temperature into a neighboring bucket

Buying the whole cluster cheap (ladder usually costs under $1) means you don’t need to guess the exact number

You just need the actual temperature to land in one of your buckets

[how to build a strong ladder in practice]

Example for Singapore (cluster 29–31°C):

- 29°C @ 0.2¢

- 30°C @ 15¢

- 31°C @ 35¢

Total: ~$0.50. One winning bucket at 100¢ makes the position profitable

[when this edge shines brightest]

- Transitional days when models disagree

- 24–48 hour horizon (D+1 and D+2)

- Volatile cities like Singapore, Miami, Tokyo, Shanghai

- Right after a fresh model run before the market reprices

Add an underdispersion filter (ensemble spread tighter than historical) and the win probability rises noticeably

Ladder + basic ensemble check is one of the cleanest asymmetric plays on Polymarket right now

Save this post!](https://pbs.twimg.com/media/HMD-GBtXEAA4GtE.jpg)