The claim isn't wrong—it's accurate for monetary sovereign governments (like the US, UK, or Japan) that issue their own fiat currency.

Operationally: Govt spends by instructing the central bank to credit reserves/bank accounts first (money creation). Taxes later debit accounts (money destruction). Tax receipts aren't transferred to "fund" outlays; the Treasury's Fed account isn't a constraint like a household checking account.

Taxes instead: create demand for the currency, curb inflation by draining excess money, redistribute resources, and discourage certain behaviors.

This challenges the "taxes pay for spending" household analogy, but central bank balance sheets and Fed/Treasury operations confirm it (see MMT descriptions and actual reserve accounting). For non-sovereign govts (e.g., eurozone states), it's different—they do need to "fund" via taxes/bonds.

@DropSiteNews So @DropSiteNews is echoing the WaPo's use of the myth that taxpayers fund the u.s. govt. Reputable indy news sites need to correct this kind of neoliberal propaganda not reinforce it.

1/18 There are many activists like myself trying to change the economic narrative. But there is hope. Here are some influential media, political, & economic commentators whose individual efforts are helping to replace the cancerous narrative of "taxpayer's money"👇🧵

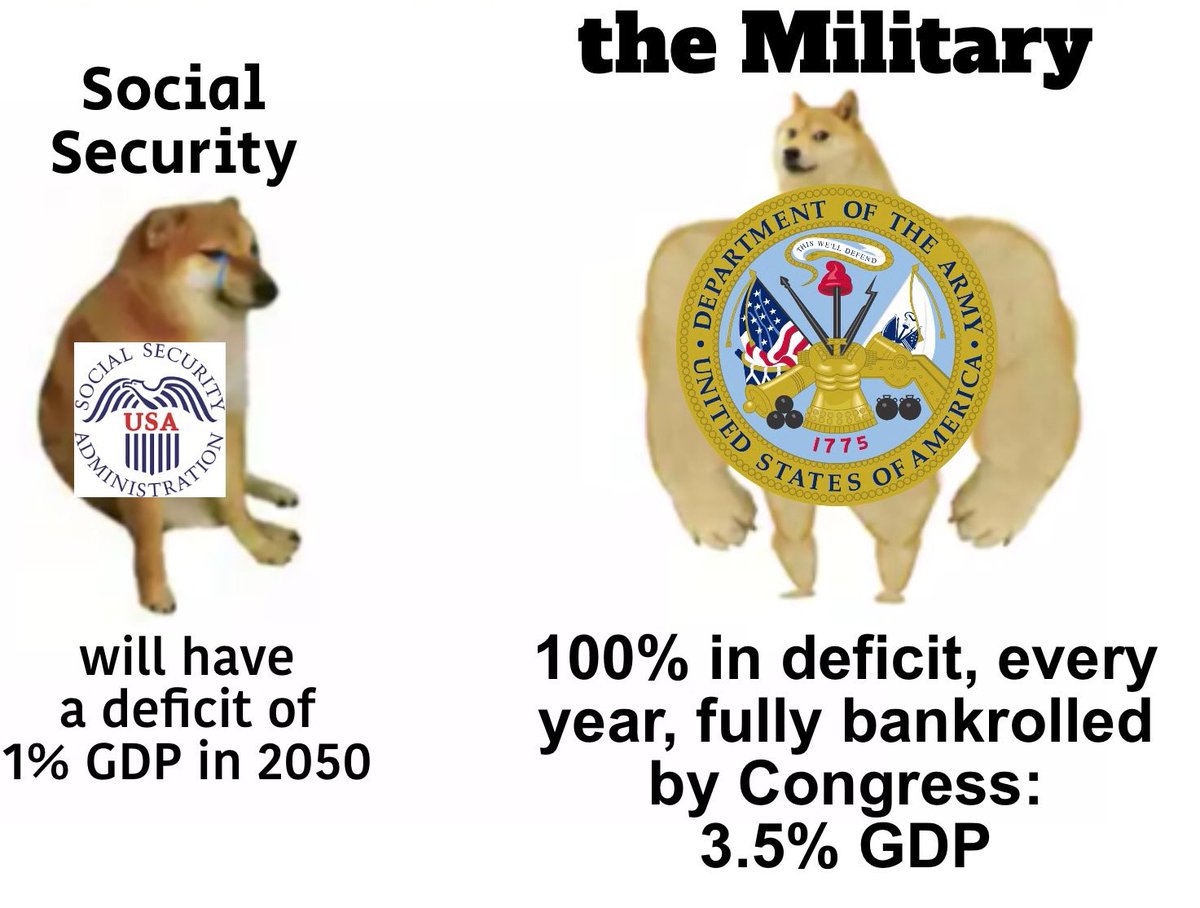

Now, watch how none of the fiscal hawks will scream about trillions being transferred by the central bank to the banking sector. Why?

Because there is a comfortable alliance between the financial sector, mainstream economists, the media, and governments.

As long as the sovereign money creation power is used to protect financial interests and enrich those at the top, it is considered “prudent policy.”

But the moment that same monetary capacity is proposed to create jobs, strengthen public services, or improve the lives of ordinary people, suddenly the deficit becomes a catastrophe, and the sky is supposedly falling. The hypocrisy is impossible to ignore.

If you made a dollar a sec you’d have $1 million in 12 days, you’d have $1 billion in 32yrs & $1 trillion in 31,710yrs or 5X longer than human civilization. New rightwing thing is acting like there’s an incremental difference between 5X longer than human civilization and 12 days

Misconceptions about degrowth are making the rounds once more.

This is degrowth: a planned reduction of excess energy and resource use.

Degrowth's views on GDP echo those of Kuznets, GDP's inventor, who said GDP growth isn't an end worth pursuing for its own sake.

We will pay for the #GreenNewDeal in the same way we paid for World War Two. We can do it without causing #inflation, without bankrupting the country & without any tax burden on hardworking people. #CallTheirBluff#MMT

A clip from our @PayForGND conf @Harvard_Law conference.

Actually, if the government doesn’t give you a patent monopoly, you won’t get very rich, but like Jonas Salk, you will have done a great thing for humanity.

Remember when Musk challenged the World Food Program to explain how he could solve world hunger with just $6 billion, they did, and he just completely ignored them?

Michigan Governor Gretchen Whitmer caught on a hot mic talking about the controversial Al data center being built despite overwhelming opposition: "We're used to people saying 'f*ck no!', and then doing it anyway."

The idea that prosperity emerges simply by removing rules and barriers assumes that markets naturally organize themselves into efficient outcomes.

Every successful market economy relies on a framework of institutions. Property rights, contract enforcement, accounting standards, banking regulation, product standards, professional certification, and consumer protection laws all shape how markets operate. None of these arise automatically from voluntary exchange alone.

This does not mean every regulation is good. Many are outdated, inefficient, or captured by special interests. But the existence of bad regulations is not evidence against regulation itself any more than the existence of bad businesses is evidence against markets.

The relevant question is always institutional design. Which rules enhance competition, transparency, and productive activity? Which rules merely protect incumbents? Which rules create trust and reduce uncertainty?

Reducing every discussion to government versus markets misses the point. Markets are themselves institutional creations. The debate is about what kinds of institutions produce the best outcomes, not whether institutions should exist at all.

@ryangrim Sidenote: Keynes also said "Anything we can actually do, we can afford" maybe remember that before your next use of "taxpayer money" & the household myth on Breaking Points.

Taxes don't pay for state pensions for any other form of public spending. Their primary functions are inflation control and redistribution. Pensioners boost effective demand and 'basket of activities' productivity in the service sector, which helps businesses and creates wealth, wages and taxes. Constantly answering economic illiteracy is so tiresome.