I discovered a new framework for understanding the housing bubble, the financial crisis, and costly housing markets.

See my substack link for ongoing analysis.

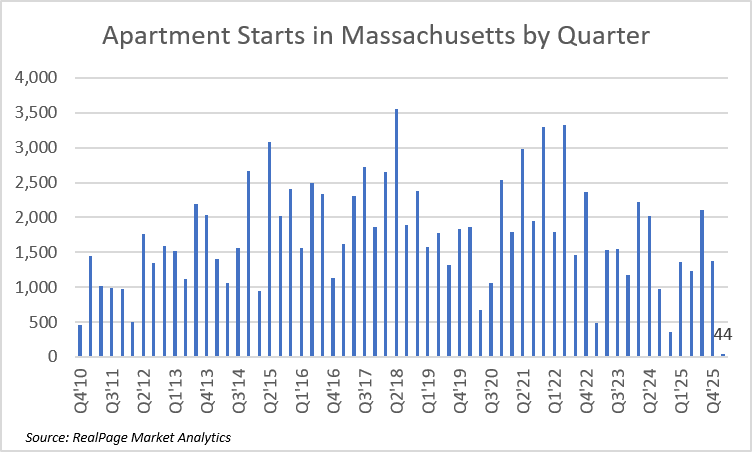

Only 44 apartment units started construction in Q1'26 across Massachusetts' three largest MSAs.

That's the lowest going back at least 15 years, likely longer.

Why? Rent control doing what rent control does, and it hasn't even passed yet.

@loganb Also, if it's labor costs, then the land should be cheap, especially if there are a bunch of process obstructions with local land use regulations.

If the land isn't cheap, then high costs are not binding at all.

A short thread on property taxes here in Florida.

In 1995, the median home in St Pete was $100,000 and the total millage rate was 24.5 mills. After deducting the then-$25k homestead exemption, your assessment would be $75,000 and you'd pay $1,837.50 in property tax on that home

Contrary to the low information discourse on here (and I'm not dissing the OP here, he knows) not a single one of California YIMBY's sponsored bills this session concerns zoning.

Here's what we're actually doing:

1. Ending frivilous condo defect litigation

2. Allowing condo presale fijancing

3. Lowering/limiting transfer taxes

4. Creating a revolving loan fund

5. Lowering ADU impact fees

6. Streamlining subdivisions

7. Requiring upfront on/offsite improvement disclosures

8. Allowing a second detached ADU statewide

9. Creating a standard entitlement application

10. Increasing residential code threshold to 10 units

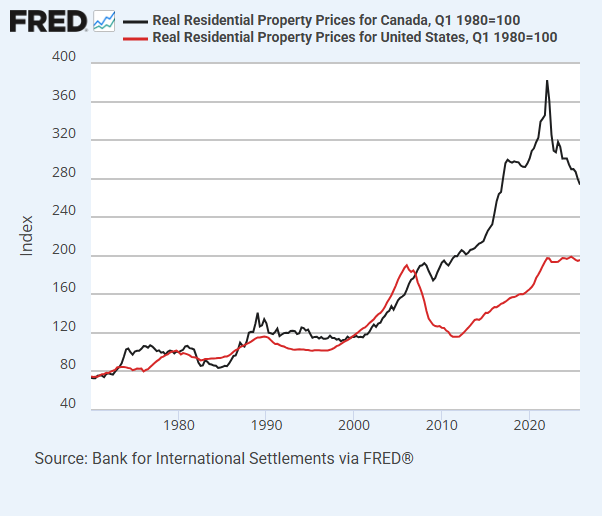

@ParkSlopeFlngsm@armsq17 There was no limit to the devastation those policy choices could have imposed on working class homeowners in Atlanta. There was no mechanism through which they might say, “Maybe we were wrong and we should let up on this a bit.”

@ParkSlopeFlngsm@armsq17 The reason the crisis was so deep is that whatever downsides were going to happen after 2007 had already been blamed on 2006 excesses, so the crisis caused by their policy choices created confirmation bias. “Wow! It was worse than we thought. We were more correct than we thought.

@ParkSlopeFlngsm@armsq17 Tighter lending collapsed demand from new buyers, which collapsed prices, which caused defaults when families faced negative financial issues related to the recession while their homes were deeply underwater.

@ParkSlopeFlngsm@armsq17 The difference between the US & Canada wasn't that we had a big bubble and they didn't. The difference is that we created a negative credit shock that made US homes far undervalued based on fundamentals.

https://t.co/DeVU4hsmh3

@ParkSlopeFlngsm@armsq17 And, hindsight 20 years later should make it clear that GSE finances and the Community Reinvestment Act are not what is making homes too expensive.

4/4

@armsq17@ParkSlopeFlngsm I agree that there was a credit boom before 2008 that was associated with some of the frothiness of the housing market, but all the post-it notes in my copy of FBD say something along the lines of "This is bs."

@Birdyword My theory is that it is really hard to have a recession when there is a housing shortage, because we won’t get the drop in housing starts that normally leads recessions.

So, 2023-2024 was what we get instead. Not quite a recession, & we are exiting it now. (See unemployment rate)

Research design about investors in housing should begin by defining them as "the absence of homeowners". Investors fill a gap. They don't drive markets.

The new literature on this is asking incoherent questions.

https://t.co/9rJ9WsjskO

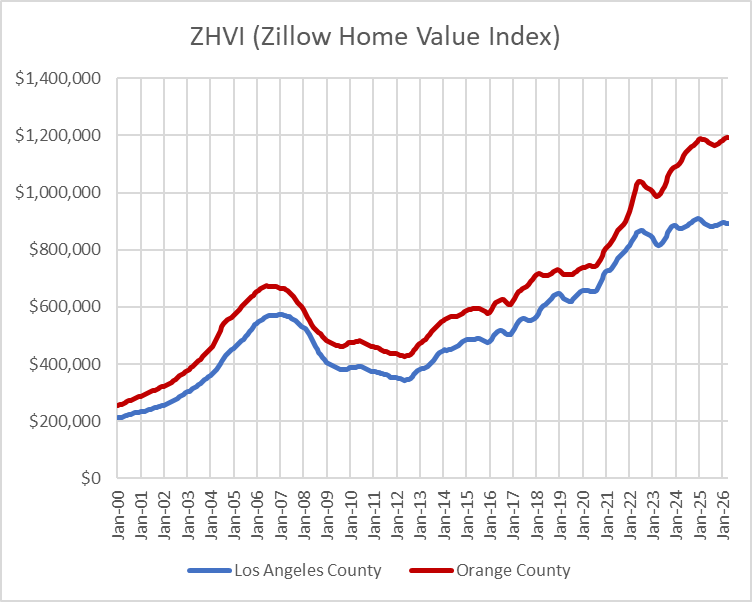

@ClayDesert@Noahpinion@soblackandblue I'm going to give Noah a pass here. It is true that jobs are in cities, and it has become harder to find affordable housing in cities.

In that tweet, I was complaining about asserting that NYC & LA are especially expensive because they have more good jobs than other cities.