Nicolai Tangen, CEO of Norges Bank Investment Management pressed IBM CEO Arvind Krishna directly on whether AI is a bubble (Save this).

And Krishna responded with what has become known inside financial circles as the $8 trillion math problem.

A single gigawatt of AI data center capacity filled with accelerators, liquid cooling, and power infrastructure costs roughly $60 to $80 billion to build and populate.

The industry has committed to more than 100 gigawatts of buildout globally.

That is $6 to $8 trillion in capital expenditure and because AI grade hardware depreciates on a five-year cycle, that entire sum must be effectively replaced and refreshed every five years.

To service the interest on $8 trillion in capital at a conservative 10% borrowing rate, the AI ecosystem would need to generate approximately $800 billion in annual profit, a number that currently exceeds the combined net income of every large technology company in the world.

Goldman Sachs estimates $7.6 trillion in aggregate AI CapEx between 2026 and 2031 alone, and Reuters Breakingviews has flagged that even if the capital is available, physical bottlenecks power permits, land, cooling infrastructure, and electrical grid connections mean that half of the planned data center projects are being cancelled or delayed before they ever go live.

Krishna also raised a second, structurally distinct concern that markets have largely ignored.

He argued that the largest foundation models, GPT, Gemini, Claude, Llama are converging toward commodity status.

When a product is a commodity, switching costs collapse.

When switching costs collapse, pricing power evaporates and margins compress regardless of how much capital was spent building the capability.

Morningstar's equity research team conducted a review of 132 technology companies in 2026 and found that AI had caused moat rating downgrades across roughly 40 major stocks concentrated in enterprise software, IT services, and SaaS with Adobe, Salesforce, Workday, and ADP among the companies whose competitive moats have materially weakened.

The implication is that the companies spending the most on AI model development may be building an asset that is simultaneously the most expensive to produce and the most difficult to monetize with durable margins.

This bear case is serious but it is also incomplete and that is what makes Krishna's framing so important to understand precisely.

When pressed further, Krishna explicitly said he does not believe there is an AI bubble in the technology itself only in a subset of the infrastructure capital that is being deployed against speculative assumptions rather than proven demand.

He draws the same analogy, the fiber optic overbuild of the late 1990s. Dozens of companies went bankrupt laying cable that nobody was using.

And yet that exact "wasted" infrastructure became the physical backbone of every cloud company, every streaming service, every mobile network, and every modern AI training cluster that followed.

The builders lost, the infrastructure won.

And the companies that were built on top of it, Amazon, Google, Netflix, Salesforce compounded for two decades.

The question, as Krishna framed it, is not whether AI is real.

It is which capital deployment earns a return versus which gets stranded and crucially, whether you own the stranded assets or the companies built on top of them.

On winners, Krishna was direct that distribution is the moat on the consumer side, and enterprise is wide open.

The data supports this, Meta with 3.3 billion daily active users across Facebook, Instagram, and WhatsApp is building AI into a distribution network that no startup can replicate at any cost.

Meanwhile, the productivity evidence arriving in real time is beginning to challenge the bear case's revenue projections.

Jensen Huang just showed on stage at Computex that GitHub commits, the universal measure of global software output nearly tripled in the first months of 2026, effectively converting $3 trillion in developer salaries into $9 trillion in productive output.

That is measurable, real time economic value already flowing through the system and it feeds directly back into token demand in a compounding loop that Krishna's static CapEx math does not fully capture.

🚨 SOMETHING DOESN'T ADD UP

The S&P 500 just pushed another leg higher.

Everyone is celebrating new highs.

But almost nobody is talking about risk.

Every previous cycle inside this channel ended with a 20%+ dump.

Most people still see strength.

I see a setup that has already played out multiple times.

The crowd always gets bullish at the wrong time.

I publicly called the 2022 market bottom and the 2025 market top before most people saw them.

Follow and turn notifications on now.

Don't be someone else's exit liquidity.

An old trader sits quietly at his desk every morning.

His rules read:

1 good trade a day

3 mistakes and stop

A young trader joins the market.

“This is easy,” he says.

The young trader takes one trade. Then a second. Then a third.

After chasing every move, forcing entries, and flipping directions, he stares at his screen late into the day.

Then he turns back, grinning proudly. “Old man,” he says, “you only made one trade while I took seven.

Maybe you’re too slow for this market.”

The old trader smiles and shakes his head.

“Funny… every time somebody loses focus, they confuse doing more with making money.”

He points at the screen.

“Trading was never about finding more trades. It was about making fewer mistakes.”

“Every leak in your system costs you clarity. Every forced trade costs you alignment. Every emotional decision pulls you further away from the edge.”

The young trader looks back at his account. The old trader closes his laptop.

“Most people think trading is about action.”

“It’s actually about discipline.” $SPY

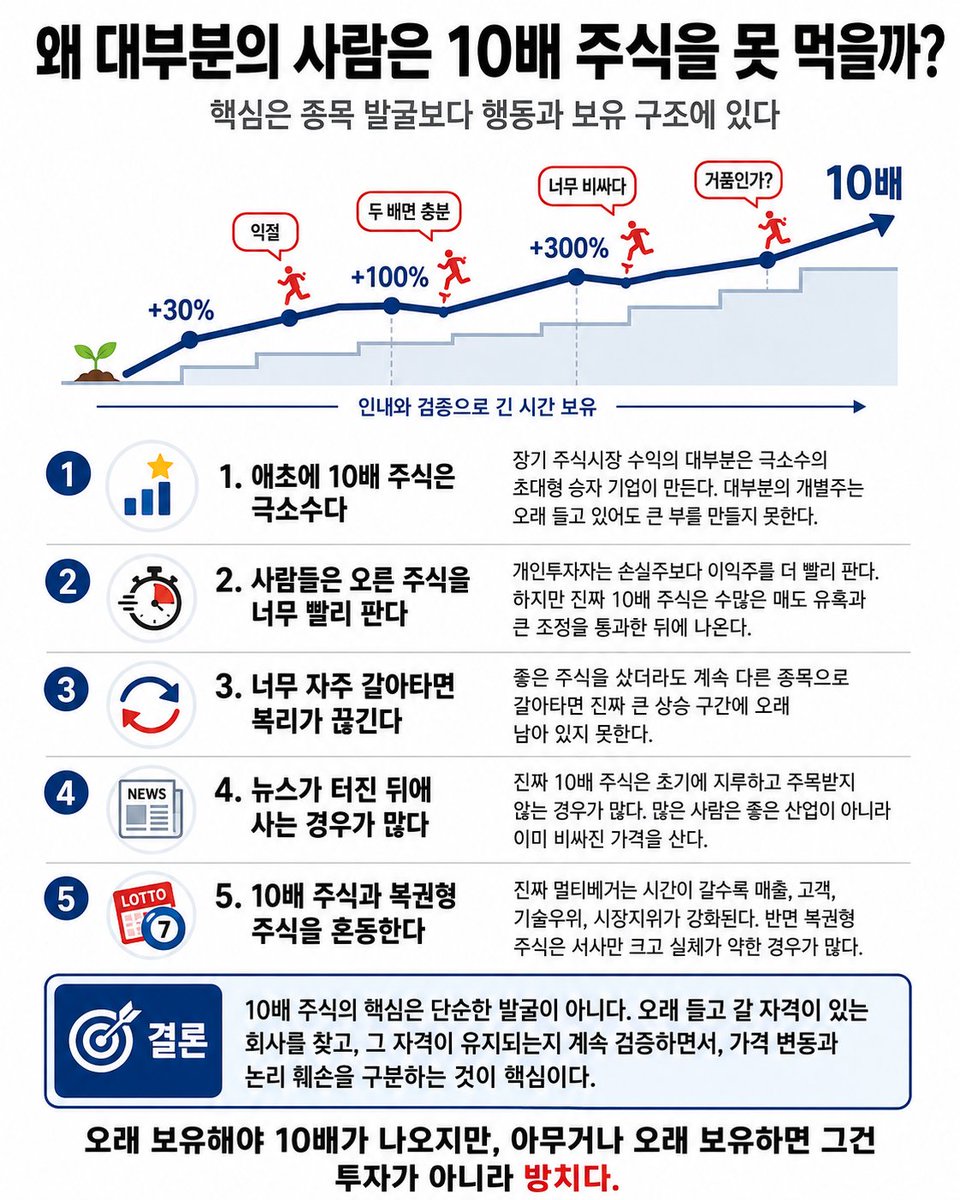

왜 대부분의 사람은 10배 주식을 못 먹을까?

논문들을 보면 결론은 생각보다 단순함.

사람들이 특별히 멍청해서가 아님.

문제는 10배 주식이 만들어지는 구조와

개인투자자의 기본 행동 습관이 정반대라는 데 있음.

1. 애초에 10배 주식은 극소수다

Bessembinder의 연구에서 가장 중요한 결론은 이거임.

장기 주식시장 수익의 대부분은

극소수의 초대형 승자 기업이 만들어냈다.

다시 말하면, 대부분의 개별주는 장기적으로

엄청난 부를 만들지 못했다는 뜻임.

여기서 첫 번째 착각이 깨짐.

“오래 들고 있으면 10배 간다”가 아니다.

정확히는,

오래 들고 있을 자격이 있는

극소수 기업만 10배 이상 갈 수 있다.

대부분의 주식은 오래 들고 있어도 별로고,

일부는 오래 들고 있을수록 자본을 갉아먹음.

그래서 10배 주식 투자는 처음부터 어려운 게임임.

단순히 “강한 믿음”의 문제가 아니라,

희귀한 승자를 골라야 하는 확률 게임임.

2. 사람들은 오른 주식을 너무 빨리 판다

Odean의 disposition effect 연구는

개인투자자가 손실 난 주식보다

이익 난 주식을 더 빨리 실현하는 경향이 있음을 보여줌.

이게 10배 주식을 못 먹는 가장 큰 이유 중 하나임.

현실에서는 보통 이렇게 됨.

+30% 오르면 “일단 익절”

+100% 오르면 “두 배면 충분”

+300% 오르면 “이건 너무 비싸다”

중간에 -40% 조정 오면 “역시 거품이었다”

그런데 진짜 10배 주식은

이 모든 구간을 통과한 뒤에 나옴.

10배 수익은 한 번의 좋은 매수로 생기는 게 아니다.

수많은 매도 유혹, 조정, 의심, 공포를 통과해야 생김.

즉 10배 주식의 본질은

발굴보다 보유가 더 어렵다는 데 있음.

3. 사람들은 너무 자주 갈아탄다

Barber & Odean의 연구는

개인투자자가 거래를 많이 할수록

성과가 나빠지는 경향을 보여줌.

이유는 간단함.

자주 사고팔면 복리가 끊긴다.

좋은 주식을 샀더라도,

중간에 더 좋아 보이는 종목으로 갈아타고,

그다음엔 또 다른 급등 테마로 갈아타고,

결국 진짜 큰 구간에 오래 남아 있지 못함.

10배 주식은 하루아침에 10배가 되는 게 아님.

대부분은 중간에

실적 의심, 밸류에이션 논란,

조정, 횡보, 악재, 시장 급락을 겪음.

그 시간을 버텨야 복리가 작동함.

그런데 개인투자자는 그 시간을 못 견디고

계속 “다음 기회”로 이동함.

결국 문제는 기회 부족이 아님.

하나의 좋은 기회에 충분히

오래 머무르지 못하는 것이 문제임.

4. 사람들은 뉴스가 터진 뒤에 산다

“All That Glitters” 연구는

개인투자자가 뉴스, 거래량 폭증, 급등락처럼

눈에 잘 띄는 주식에 끌리는 경향이 있음을 보여줌.

이것도 매우 중요함.

진짜 10배 주식은 초기에 보통 지루함.

아직 대중이 잘 모르고,

실적도 완벽하지 않고,

기관 관심도 약하고,

서사도 완전히 정리되지 않은 경우가 많음.

반대로 모두가 말하는 주식은

이미 기대감이 가격에 많이 반영된 경우가 많음.

많은 사람은 좋은 산업을 샀다고 생각하지만,

실제로는 좋은 산업의 비싼 가격을 사는 경우가 많음.

여기서 수익률이 크게 갈림.

좋은 산업을 아는 것과

좋은 가격에 좋은 회사를 사는 것은 완전히 다르다.

5. 10배 주식과 복권형 주식을 혼동한다

Kumar의 연구는

개인투자자들이 낮은 가격,

높은 변동성, 큰 상승 가능성을 가진

복권형 주식을 선호하는 경향이 있음을 보여줌.

이게 멀티베거 투자에서 가장 위험한 지점임.

진짜 10배 주식과

그럴듯한 복권형 주식은 겉으로 비슷해 보임.

둘 다 “크게 오를 수 있다”는 이야기가 있음.

둘 다 TAM이 크다고 말함.

둘 다 미래 산업과 연결되어 있음.

둘 다 아직 숫자가 완전히 나오지 않았을 수 있음.

하지만 내부는 완전히 다름.

진짜 10배 주식은 시간이 갈수록 실체가 강해진다.

매출이 늘고,

고객이 붙고,

기술우위가 확인되고,

시장지위가 강화되고,

현금흐름 개선 가능성이 보이고,

경영진의 자본배분이 검증됨.

반대로 복권형 주식은

스토리는 크지만 실적은 약하고,

파트너십은 모호하고,

유증은 반복되고,

경영진은 주주친화적이지 않고,

TAM만 거대하게 말하는 경우가 많음.

그래서 멀티베거 투자는

단순히 “상승 여력 큰 주식”을 사는 게임이 아님.

진짜 게임은 이거임.

비대칭 상승 가능성이 있으면서도,

시간이 갈수록 실체가 강해지는 회사를 구분하는 것.

정리하면 이렇다

대부분의 사람은 10배 주식을 못 먹는 게 아님.

잡아도 중간에 판다.

승자는 빨리 팔고, 패자는 오래 들고 간다.

뉴스가 터진 뒤에 늦게 산다.

너무 자주 갈아타서 복리를 끊는다.

복권형 주식을 10배 후보로 착각한다.

그리고 포지션을 너무 크게 잡아서

정상적인 조정도 버티지 못한다.

결국 10배 주식의 핵심은

단순한 종목 발굴이 아님.

발굴은 시작일 뿐이고,

진짜 어려운 건 검증하면서 보유하는 것이다.

하지만 여기서 반대편도 반드시 봐야 함.

무조건 오래 들고 있는 것도 답이 아니다.

대부분의 개별주는 장기 승자가 아니기 때문임.

그래서 내가 보는 결론은 이거임.

10배 주식 투자는

“좋은 주식을 오래 들고 가는 것”이 아니라,

오래 들고 갈 자격이 있는 회사를 찾고,

그 자격이 유지되는지 계속 검증하면서,

가격 변동과 논리 훼손을 구분하는 게임임.

오래 보유해야 10배가 나온다.

하지만 아무거나 오래 보유하면

그건 투자가 아니라 방치다.

10배 주식은 믿음으로 먹는 게 아니라,

검증된 논리를 오래 유지할 수 있을 때 먹는 것이다.

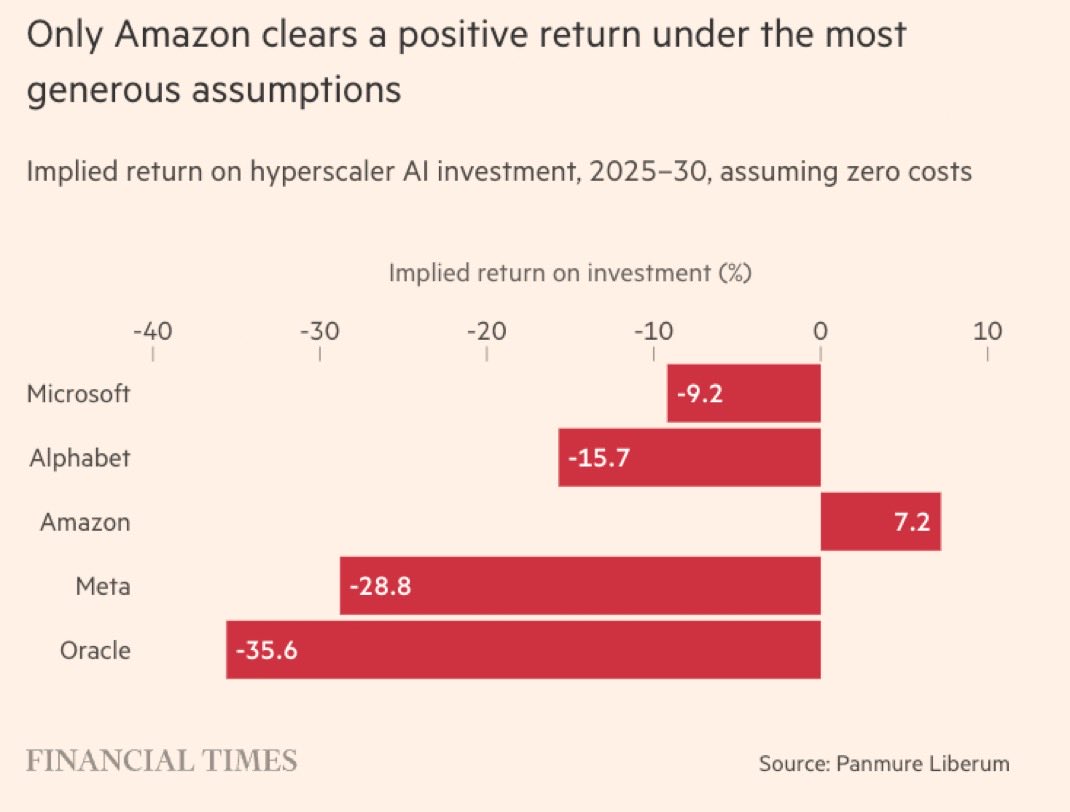

🚨 The AI ROI numbers are starting to look very ugly.

Even under "best case" assumptions — assuming zero costs, just revenue against capex — the Financial Times calculated the implied return on hyperscaler AI investment from 2025 to 2030.

Only one of them clears positive.

Implied return on AI investment (FT / Panmure Liberum)

– Microsoft: -9.2%

– Alphabet: -15.7%

– Amazon: +7.2%

– Meta: -28.8%

– Oracle: -35.6%

And remember: that's assuming zero costs. In reality, GPUs depreciate, power bills run, salaries get paid.

The real returns are worse.

This is exactly why the dot-com comparison keeps coming up. Incredible technology does not automatically mean sustainable economics. The internet survived. Most internet companies didn't.

Two anecdotes from this week alone

Vivek Garipalli, Fortune 20 insider: a CEO asked for $1B in AI-driven opex savings this year. The team spent $200M on tokens chasing it. The results? Modest customer service savings and slightly less hiring in engineering. The CEO has now ordered token costs to be dramatically slashed because the ROI isn't there.

Axios: an AI consultant reported a single client spent half a billion dollars in one month after forgetting to put usage limits on Claude licenses for employees.

Right now hyperscalers are spending trillions hoping future demand catches up to present capex.

That's not certainty. That's a leveraged bet.

The technology is real. The infrastructure buildout is real. The eventual winners will be real.

But "AI is transformative" and "every hyperscaler will earn its capex back" are two completely different statements.

In 2000, the internet was real too.

Cisco has recovered.

After 26 years…