About Lithium Companies doing business in Argentina, and Lithium Business, EV ESS. DYOR, NOT financial advice. Not a recommendation to buy or sell securities.

For the first time in 123 years, Argentina has achieved a sustained fiscal surplus without being in default. We are one of only 5 countries in the world in this position.

LONG LIVE FREEDOM, DAMN IT...!!!

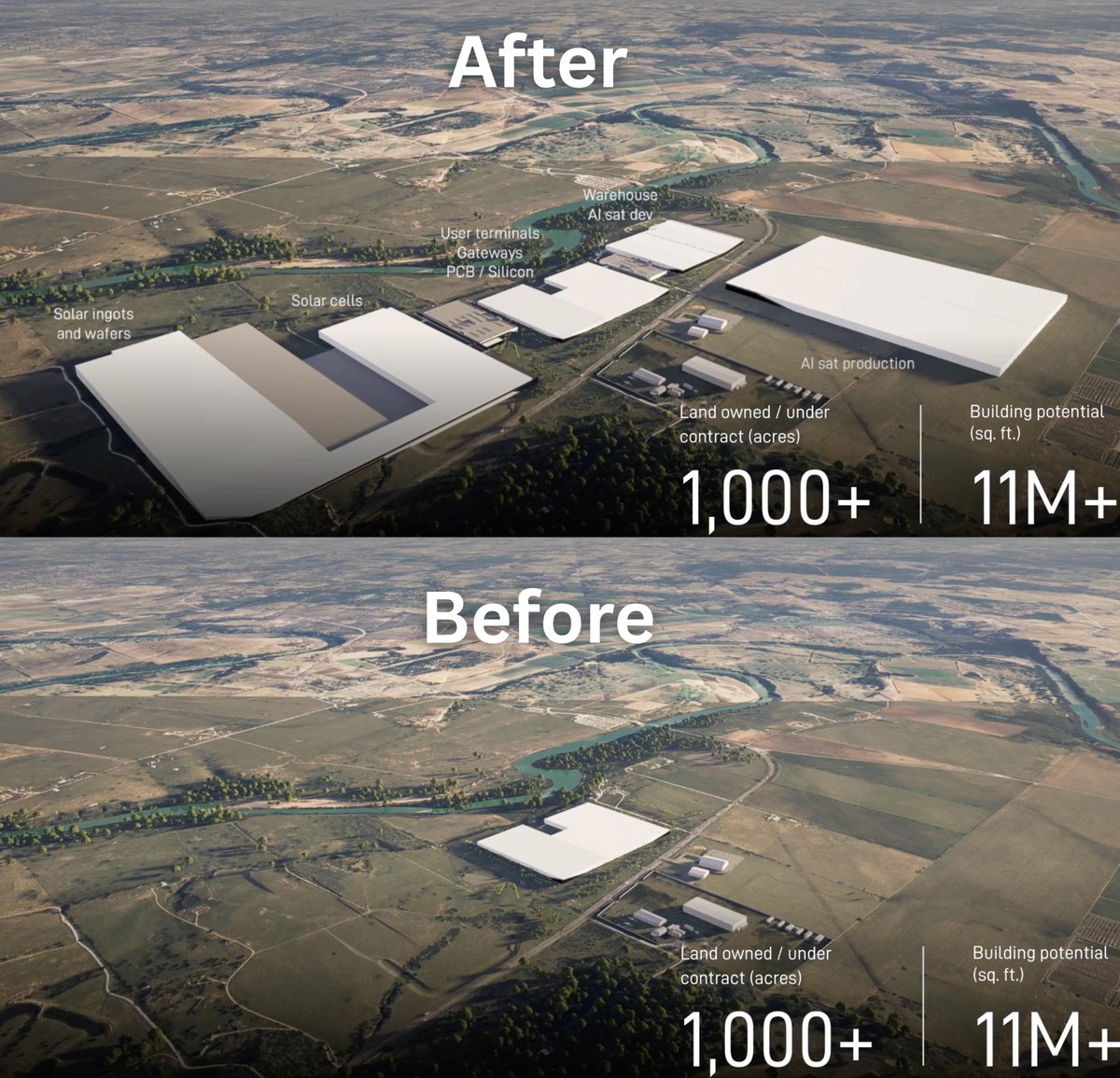

Bastrop, Texas will soon become home to one of the largest solar cell and wafer production facilities in North America with @SpaceX's new investments in the area, creating thousands of jobs.

The solar facility is already under construction, and the AI sat facility is expected to start initial production by the end of 2027.

🚨🇦🇷 | ARGENTINA SERÁ PRÓSPERA: Gracias al éxito del plan económico de Milei junto a la implementación del RIGI, la inversión extranjera directa en el sector minero se disparó un 88% con respecto a 2023, alcanzando el récord histórico de 17.645 millones de dólares.

With the formalization of RIGI approval for Cauchari-Olaroz Stage 2 now complete, our focus remains on advancing the project and completing the next phase of development planning. This milestone further reinforces Argentina's commitment to supporting strategic investment in its critical minerals sector.

#Lithium #Argentina

EL NUEVO RIGI APROBADO EN JUJUY QUE AUMENTARÁ LA PRODUCCIÓN DE LITIO

La inversión de 1.241 millones de dólares de la empresa Minera Exar para la ampliación de la planta del proyecto de litio Cauchari Olaroz, en la provincia de Jujuy, incrementará la producción hasta 85.000 toneladas al a��o y creará alrededor de 1.800 empleos directos e indirectos.

No coffee today as I spat it out reading Goldman Sachs' lithium supply table which popped up in my twitter feed.

What i find most intriguing about this table is that it states the majority of lithium supply will come from China itself, in particular internal lepidolite and brine.

In my opinion, this is unrealistic and the numbers don't quite seem logical. Lets break down the lepidolite numbers:

They are predicting that 462,000t of LCE will be produced internally from Chinese lepidolite in the year 2030.

Using a previous post of mine (i'll put the link in the comments below), for a lepidolite ore of grade 0.55%, you need approximately 14 tonnes of lepidolite to get SC6 equivalent. Roughly 6 tonnes of SC6 is needed for 1 tonne of LCE.

You need around about 14 * 6 = 84 tonnes of lepidolite ore grading 0.55% to get 1 tonne of LCE... 🤯

84 * 462,000t LCE = 38,808,000 tonnes of ore grading 0.55% to meet 2030 yearly output prediction alone. That's 6 years away...

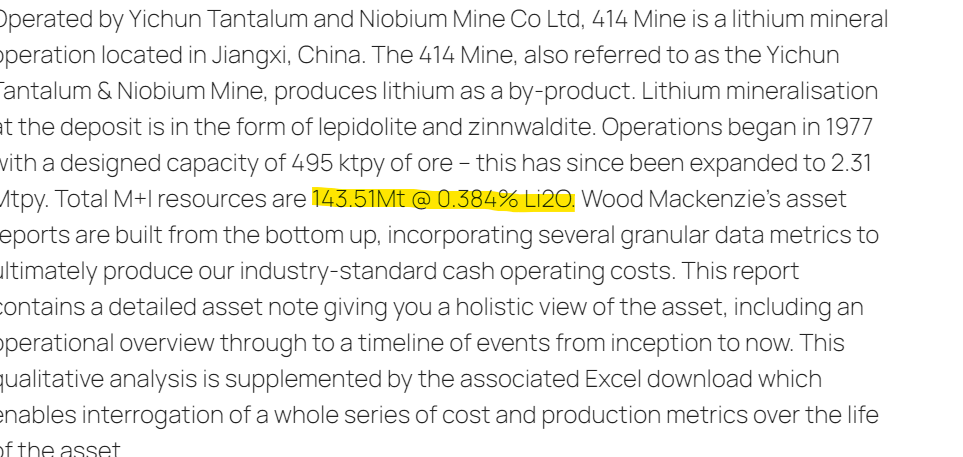

The largest documented lepidolite mine within China is the "414 Mine". Approximately has 130Mt @ 0.38% li2O. That's roughly equivalent to a #GL1 Manna deposit in terms of contained lithium. Plug the above 0.38% into the previous calc and you're almost processing half of China's biggest documented lepidolite deposit yearly... Defies logic for me.

Also, the above is just talking about pure tonnage. The waste products (which i've touched on in previous posts) from the deleterious elements (iron, fluorine, potassium, etc.) within lepidolite will be astronomical. There are already reports of converters sending ore back and tailing storages blowing out in size. How is it going to look when you are processing 38Mt+ of low grade lepidolite ore a year?

Lepidolite contains more deleterious elements than spodumene, is generally lower grade, is slower and more difficult to process, especially in the leaching stage. I'm sticking to my view that the lepidolite deposits and stockpiles get exhausted soon and that the processing of lepidolite is a short term attempt by China to squash the market. IMO there is no chance lepidolite will ever be cheaper than spodumene to process and it isn't a realistic solution to meet future lithium demand. Cheers for reading.

NUEVO RIGI PARA INCREMENTAR LA PRODUCCIÓN DE LITIO EN JUJUY

Se aprobó la adhesión al RIGI del proyecto de ampliación de la planta de litio Cauchari Olaroz, en la provincia de Jujuy, por 1.241 millones de dólares de la empresa Minera Exar.

La obra permitirá llevar la producción de litio a 85.000 toneladas al año y generará 1,787 puestos de trabajo directos e indirectos.

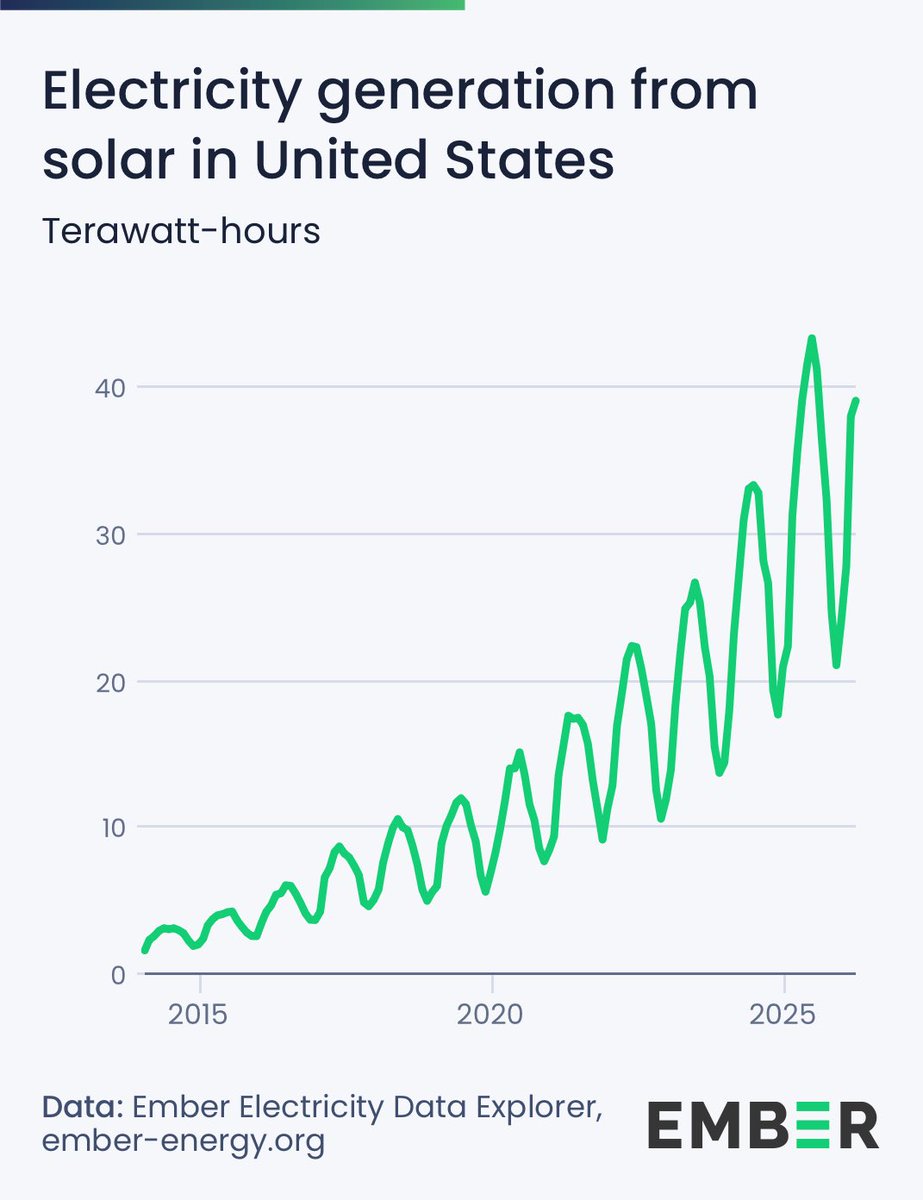

It’s always just one chart away…winter solar output in the US is now the same as summer output was 3 years earlier.

The US has good solar conditions even in winter (and it’s complementary with wind in the winter as well).

In 2020, EVs made up just 4% of all car sales globally.

Their share rose to 25% in 2025 – and is set to grow close to 30% this year.

And by 2035, even without any new policy announcements, EVs could account for about half of global car sales ��� https://t.co/NkYY60UsFL

Gas spent 20 years owning the evening peak. Batteries took a year to crash the party.

That's disruption. Not gradual, but a rapid shift in who supplies grid's most valuable hours.

The battle was never about total generation. It was about the peak & batteries are winning it.

Running high grade + heavy load feels effortless in the Tesla Semi. Enough power to maintain speed when climbing, and regenerative braking making descents save and controllable. All while in silence.

.@GalanLithium's pitch is simple: don’t build the whole carbonate complex first. Produce chloride, generate cash flow, scale later.

HMW is commissioned, funded to production, and has a buyer.

JP Vargas and Ross Dinsdale unpack the milestone, offtake and next steps. $GLN

📺: https://t.co/9ScfdNhe64

A couple of days have passed now and I’ve slowly recovered from reading the GS supply table. Some more ramblings on the current lithium market whilst I sip my morning coffee (managed to get this one down).

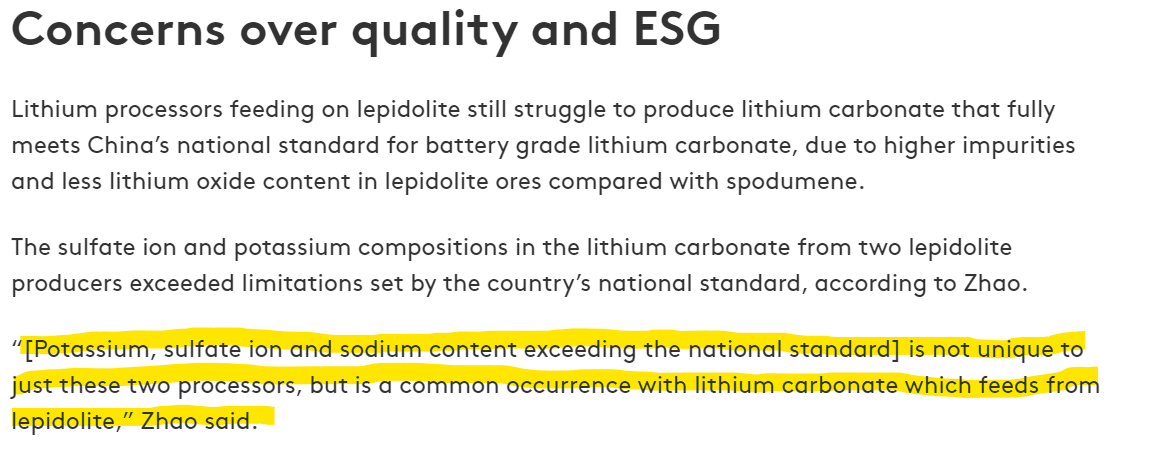

Following on from my previous post regarding lepidolite production within China. The Chinese have shown that they are willing to mine spodumene at a near loss. It seems they aren’t too bothered about losses at the mining stage if it means greater control over the market. Alita with the whole Bald Hill mine debacle, were allegedly selling Spod concentrate from Bald Hill well below the current market price (70% under) to their Chinese offtake partner… See screenshotted article below.

So why is China suppressing the price with low grade internal sources? I believe Its to bide time to build stakes in overseas, high quality lithium plays, predominantly Africa given the Australians and Canadians aren’t willing to play ball. Chris and Gina are well aware of this, and its most likely they are aware that the lepidolite reserves are a short term band-aid solution.

As per my last post, you need roughly 84 tonnes of lepidolite ore to make 1 tonne of LCE. The contained lithium content of these low grade lepidolite mines is miniscule. The numbers below speak for themselves.

‘414 Mine’ has 130Mt @ 0.38% li2O.

Contained lithium = 0.0038 x 130Mt = 0.494 Mt li2O. That’s roughly 1.22Mt of LCE.

Compare that to Kathleen Valley. 156 Mt @ 1.4%.

Contained lithium = 0.014 * 156Mt = 2.184 Mt li20. That’s roughly 5.4Mt of LCE

So the ‘414 Mine’ is around 20% of Kathleen Valley in terms of contained lithium…😅

Also its not just about size, its how quickly can you get it out of the ground. $LTR for example is going to be a 4mtpa operation for 700,000kta SC6. You’ll need a 14.7mtpa operation to get the equivalent output from lepidolite grading 0.38% (414 Mine grade). And that's just the initial beneficiation stage...🤯

What we are seeing now is very similar to what happened with Iron ore. The Chinese attempted to use low quality, internal iron ore in order to manipulate the price. This turned out to be unsustainable and the price of Iron ore increased overtime.

I believe we are seeing this again with in the form of Lepidolite. Its almost déjà vu in fact, the iron ore price plummeted 70-75% to a low of $37 a tonne in Dec 2015. Goldman Sachs' predicted the iron ore price to touch $35 a tonne in 2017 & 2018. The opposite happened and the price went ballistic. See chart below.

Happy Friday everyone and cheers for reading.

The IEA now forecasts global EV sales topping 23M in 2026. Funny thing? Now only 2.6M below my own projections.

Consensus keeps chasing reality upward as China scales harder, battery costs fall & EV disruption compounds faster than most expected.

Good old fashioned disruption!

https://t.co/JvMRSNxJ3G

$GLN – First processed lithium chloride at HMW; commissioning complete. Ramp-up enabled by 10,000 t LCE inventory Phase 1 expansion on track for H1 2027

https://t.co/DJD5aawVcg #Lithium#ASX#Mining#Argentina