I worked for a bank. Then I protested one and I lost my house for it.

That's where this starts. Where it ends is realizing the money is broken, and doing everything right still feels like falling behind because it is.

My whole story, and how it led me to the one place left to save that no one can print away.

— Zach 🧙♂️

Bitcoin Well pays me bitcoin every time my link clears a trade. Lands in my Lightning wallet the second it does.

Stack sats by sending people somewhere they actually own what they buy.

Grab your Welltag. Drop it in your bio. Done.

https://t.co/KOloio62Mw

Orange pill your aunt. Get paid in Bitcoin for it.

We just rebuilt our referral program. It's the best in the business, and it pays you up to 21% of the fee we earn. Not just once, but every time someone you referred makes a transaction.

Your mom. Your brother. The coworker who still calls it magic internet money. Send them your link, and when they buy real Bitcoin, you stack sats.

Open your account, hit Rewards, then Referrals. Your link is waiting.

Reid Hoffman bought Bitcoin in 2014. He hasn't sold a single sat in twelve years.

When asked what his exit price was, the LinkedIn co-founder said: "Is there such a thing as an exit price?"

You see, "exit price" is fiat-brain. It assumes Bitcoin is the trade and dollars are the destination. Hoffman flipped the script: he's already in the destination. The 12 years of holding aren't conviction. They're literacy. He understands what most people still won't admit. The thing you "exit into" is the thing being debased on purpose.

Rothbard called it correctly fifty years ago: paper money is not a savings vehicle, it's a managed loss. Hoffman ran the math in 2014 and never looked back.

You don't need a billionaire to validate self-custody. But it helps when the market keeps producing them.

Buy bitcoin. Hold your own keys. Stop asking when to leave. There's no exit from sound money.

The CEO of the biggest exchange in America just called the Bitcoin bottom at $60,000.

He might be right, but It changes absolutely nothing about what you should do.

This week, Coinbase CEO Brian Armstrong stated his instinct is that $60K is the floor, and he expects a "much higher" price by 2030. It is a reasonable macroeconomic take. But it is also just a guess from a man whose entire billion-dollar business model depends on you trusting his centralized database to hold your wealth.

Here is the trap in taking price advice from a custodian: If you believe his bottom call, buy on his exchange, and leave your wealth sitting there, you do not own Bitcoin. You own a corporate IOU and a screen that says $60,000. The fiat value on the screen is real. Your ownership is an illusion.

Interestingly, Armstrong also stated this week that U.S. accredited investor laws essentially make it "illegal to get richer, unless you're already rich". He is absolutely right about that. The legacy financial system is explicitly designed to gatekeep the upside and reserve it for the ruling class.

But relying on a centralized corporate exchange does not fix that problem; it just shifts who is holding your leash.

Bitcoin is the mathematical opt-out from both problems. There are no accreditation tests to hold absolute scarcity. There are no CEO price targets you need to trust. And most importantly, there is no platform standing between you and your money.

You don't need a billionaire's bottom call, you just need to hold your own private keys.

The CLARITY Act cleared committee today. Senator Lummis is telling the Senate not to quit at the 5-yard line, and more than 200 crypto companies signed a letter begging for the floor vote.

Good news for the industry. Worth being honest about what it actually is, though.

A market-structure bill draws lines around the middlemen. It tells Coinbase what it can list. It tells Circle how to back a stablecoin. It tells the SEC where its authority stops. It is a rulebook for the companies that hold your coins for you.

Your keys were never on the ballot. Self-custody didn't need a law last year. It doesn't need one in 2026. A node running in a closet has been enforcing its own rules this whole time, and not one senator gets a vote on it.

Clear rules can make the on-ramps safer. That's real, and it matters for anyone buying their first sats. Just don't mistake a cleaner cage for an open door.

The Senate is fighting over who gets to govern crypto. Bitcoin answered that question in the genesis block: nobody.

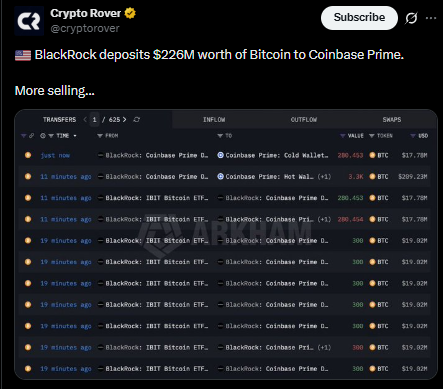

Your IBIT shares are not Bitcoin. This morning made that impossible to ignore.

BlackRock moved roughly $226 million of Bitcoin to Coinbase Prime, and the timeline split in half. One side is screaming "they're selling." The other is insisting it's fresh inflows. Both sides are arguing about the wrong thing.

It doesn't matter which one is right. Either way, not a single IBIT holder got a vote, a notice, or a key. The coins behind the largest Bitcoin ETF on earth sit on a custodian's books, get moved on the custodian's schedule, for the custodian's reasons. You own a share of a fund that owns coins Coinbase holds. Two layers of intermediary between you and a key you will never touch.

That's the trade the ETF asks you to make. Convenience now, control never. BlackRock spent decades getting between people and their assets, because the gap is where the fees live. Bitcoin was built to delete the gap. The ETF quietly sells it back to you, $226 million at a time.

A fund share rises and falls with the price. It cannot send one satoshi without permission.

Let BlackRock move their coins. While you hold yours.

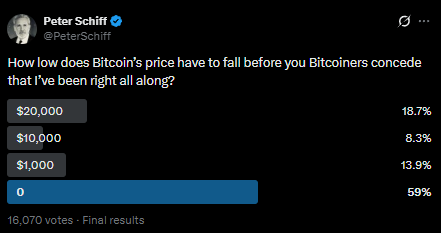

Peter Schiff ran a poll this weekend asking how far Bitcoin had to fall before holders would admit he was right. Most of them answered: never.

He called that a cult.

He's half right. By his rules, it is irrational. Schiff prices everything in dollars, so to him a saver who won't sell at any number has lost his mind. But the saver isn't playing Schiff's game. He isn't pricing his Bitcoin in a currency that has lost more than 90% of its purchasing power since the Fed was founded in 1913. He's measuring something Schiff can't put on a chart.

A man who holds his own keys doesn't need Bitcoin to hit a price to feel right. He already opted out of needing anyone's permission. That's the part Schiff reads as cult behavior. It isn't. A cult needs a leader to obey. Self-custody is the one financial position on earth with no leader, no central office, and no exit anyone can talk you out of.

Schiff thinks he's watching people refuse to admit a loss. He's watching people refuse to sell their sovereignty back to the system he works inside.

Gold bugs measure conviction in price. Bitcoiners measure it in custody.

@BitcoinMendo@bitcoinwell Both? I've heard the argument that Bitcoin isn't technically crypto but honestly not sure where I end up on that. Not knowledgeable enough about cryptography to be able to draw that line.

Before Bitcoin existed, the U.S. government decided that strong encryption was a weapon.

In 1991 a man named Phil Zimmermann wrote a program called PGP and gave it away for free, so ordinary people, not just governments and banks, could send a message no one else could read. Soon after it spread beyond U.S. borders, the Customs Service opened a criminal investigation. The charge they were chasing: exporting munitions without a license. The munition was math.

The investigation lasted three years. Zimmermann's answer was perfect. He published PGP's entire source code as a book through MIT Press, because the government can restrict exporting a weapon, but it cannot restrict exporting a book. Code is speech. In early 1996 they dropped the case without filing a single charge.

That fight is why Bitcoin can exist. The right to run cryptographic software you control, to hold a key the state cannot pry open, was won by people like Zimmermann years before Satoshi wrote a line of code.

Self-custody is just encryption applied to your money. Same math. Same right. Same fight.

Hold a key no government can open, and you are standing exactly where he stood.