Vuelve a descender la inflación en Argentina. Los precios aumentaron un 2,1%, el ritmo más lento desde septiembre (y muy inferior al del período peronista previa).

Inflation is still half of what it was under Biden.

May CPI is 4.2% year-on-year, more than 2x the Fed target, driven by energy and agriculture.

First 16 months: 5.5% vs Biden’s 11.7%. Bring inflation down fast or risk losing both houses in November!

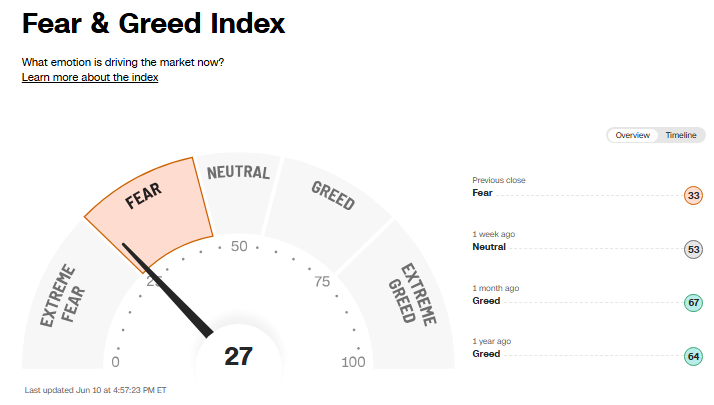

Rising Treasury yields are now the biggest threat to the equity market:

The 3-month correlation between the 10-year Treasury yield and the S&P 500 is down to -0.62, the lowest in at least 15 years.

This means that when Treasury yields rise, stock prices fall, and when yields fall, stocks rise.

By comparison, during the 2022 bear market, this correlation never crossed -0.50, making the current reading the most extreme negative relationship in decades.

Following the 2008 Financial Crisis, yields and equity prices moved in the same direction, supported by strong economic growth and earnings expectations.

Currently, rising yields reflect surging inflation fears rather than growth optimism, weighing on stock valuations rather than signaling economic strength.

Keep watching the bond market.

Argentina’s inflation slowed to the lowest level since September in a victory for President Javier Milei following a surge in March due to the Iran war-related energy shock. https://t.co/QRVhaQkxbO

Estoy enormemente honrado y agradecido con Alex Chafuen por citarme junto al @Fractal_Index. Entender la naturaleza de las guerras asimétricas, la forma en que operan los subversivos, el contexto y su dinámica, nos ayudan a encarar sus amenazas hoy en Bolivia y todo Occidente.

MUY IMPORTANTE

S&P acaba de subir la calificación de Argentina a B- de CCC+, luego de que Fitch tomara la misma decisión hace algunas semanas.

Esto no es un detalle menor.

Cuando dos de las tres calificadoras alinean su nota, el efecto sobre el universo de inversores elegibles se multiplica.

Muchos fondos institucionales requieren confirmación de al menos dos de las tres agencias para invertir en un país con calificación de por lo menos B-. Ahora tienen luz verde para invertir.

Miles de fondos que no podían tocar deuda argentina porque S&P y Moody’s aún la mantenían fuera del umbral B- ahora pueden hacerlo.

La mejora de S&P cierra el círculo.

Para los bancos internacionales, el impacto es concreto: los requerimientos de capital bajo Basilea III para operaciones con Argentina caen significativamente.

Prestar al país es ahora menos costoso en términos regulatorios, lo que amplía el universo de bancos dispuestos a abrir líneas de crédito.

Las compañías de seguros, que calibran su exposición en función de las notas de S&P en particular, ven caer el capital requerido por cada dólar invertido en instrumentos argentinos, mejorando el retorno sobre ese capital.

Para empresas y provincias que buscan financiarse en los mercados internacionales, el costo baja y las puertas se abren más.

El doble consenso entre calificadoras genera una señal de credibilidad que los inversores no pueden ignorar.

Cada punto de mejora en el rating se traduce en menos costo de financiamiento para el país, para las empresas grandes, empresas pequeñas y para las personas. En definitiva, para TODOS los argentinos.

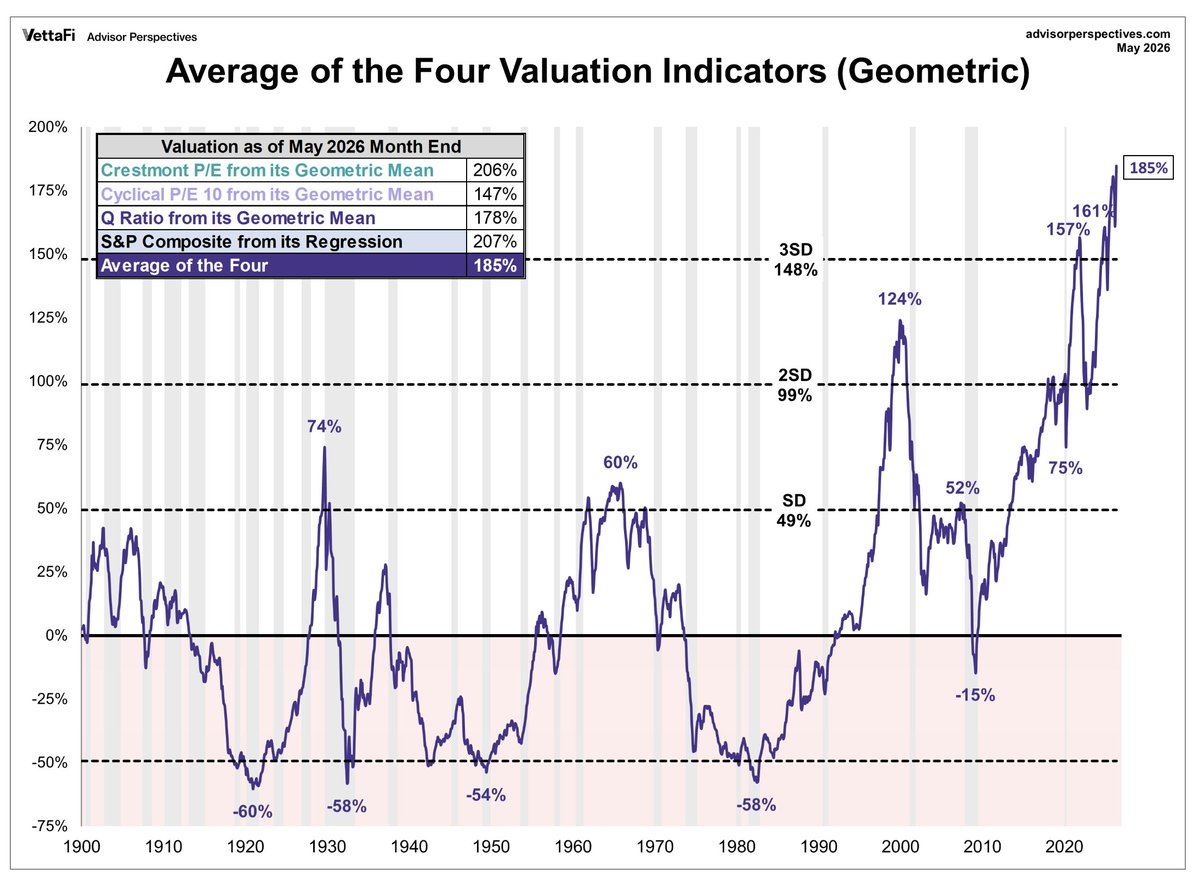

The current reading of 185% above historical fair value is the highest in the entire data series going back to 1900.

The purple line is the average of four long-term valuation measures, each expressed as a percentage above or below its historical geometric mean:

* Crestmont P/E

* Cyclically Adjusted P/E (CAPE/Shiller P/E)

* Tobin's Q Ratio

* S&P Composite Regression Model

Historically, when broad U.S. indexes reached extreme valuations, future leadership often came from:

* Small caps

* Value stocks

* International markets

* Commodity-related businesses

* Asset-heavy cyclical sectors

This is one reason many value investors today focus on areas trading at single-digit EBIT multiples while the major indexes trade at historically rich valuations.

Some of the best periods for value strategies occurred when the broad market was near valuation extremes and the valuation spread between glamour and neglected businesses was unusually wide.

Bolivia’s embattled President Rodrigo Paz signed a measure that clears the way for a more aggressive crackdown on anti-government protests that have rocked the country for more than five weeks https://t.co/loFJ3STHBa

Inflation in Europe is rising rapidly:

Eurozone Manufacturing PMI Input Prices spiked to 80 points in May, the highest since May 2022.

This also marks the largest monthly increase in costs for firms over the last 4 years.

Furthermore, PMI Output Prices surged to 62 points, the highest in 3.5 years.

The rate companies are increasing the prices they charge for goods they produce has surged +12 points, or +24%, since the start of 2026.

This surge has been primarily driven by rising energy and raw material costs.

Meanwhile, supply chain delays are up to the highest level since the pandemic supply squeeze of 2022, adding further pressure on prices.

As a result, factories are forced to pass higher costs on to customers, which will push inflation even higher over the next few months.

Price pressures across Europe are accelerating.