Comment "real" & RT if you agree:

❣️ Our community caused MetaMask to add PulseChain as a default network—next to ETH.

🆘 Now help us prove to X @premiumbusiness that PulseChainConf is a real organization and we are respectfully waiting for our $1,000/mo badges to be approved/restored.

Welcome back to #PulseChainLawSchool everyone! Let’s learn some more Latin:

“Falsus in uno, falsus in omnibus.”

This is a well-known Latin phrase in law, and it means that if someone is found to be lying about one thing, it is reasonable to conclude that they shouldn’t be believed about anything else.

Which brings me to today’s topic: The SEC, and more specifically, settling with the SEC, which is materially different than settling with any other government agency or private party.

The easiest way to describe today’s issue is to quote from the 5th Circuit Court of Appeals in SEC v Novinger, 40 F.4th297 (5th Cir. 2022):

“Since 1972, the SEC has prohibited defendants who settle civil enforcement actions without admitting guilt from publicly denying the allegations in the complaint filed against them. The SEC enacted this no-deny policy, which is codified at 17 C.F.R. 202.5(e), after determining that it was important to avoid creating, or permitting to be created, an impression that a decree is being entered or a sanction imposed, when the conduct alleged did not, in fact, occur. Id. Under the policy, a refusal to admit the allegations is equivalent to a denial, unless the defendant or respondent states that he neither admits nor denies the allegations. Id.”

(FYI, whenever you see “Id” in a case, it means it’s referencing the case it cited immediately prior. This just saves time typing the same case name and citation over and over when you cite it multiple times in a row.)

The short version: If you settle a case with the SEC, you are *never* allowed to deny the allegations they made against you, even if they’re complete bullshit and you only settled because they offered you a minimal fine and it would have cost you 10,000x that amount to fight them in court. If you do speak out (even if you speak the truth), the SEC can reopen the case against you.

Does this seem fundamentally unfair? Absolutely.

Does it seem like a 1st Amendment violation? Absolutely.

So let’s ask a very important question: Why does the SEC think it still deserves to have this policy enforced by courts when it’s racking up a history of legally questionable or outright illegal actions?

By “legally questionable,” I don’t even mean actions that could be reasonably interpreted as incompetence, such as completely f*cking up with ZZZZ Best, Enron, Madoff, FTX, or Alameda. As bad as those failures were, there’s still an argument an attorney could make in court for the actions the SEC took or didn’t take without the judge laughing at them.

I don’t even mean “legally questionable” in the sense of going after favorable news treatment by filing legally problematic complaints, because THAT’S LITERALLY THEIR GOAL. Andrew Vollmer, former SEC deputy general, said the SEC only “wants headlines and therefore it needs to have eye-popping civil penalty numbers” as opposed to effective business regulatory policies.

But incompetence and politics are one thing, deliberately taking illegal and/or unethical actions are another. Let’s take some recent examples:

Deliberately Withholding Exculpatory Evidence:

In United States v. Mahaffy, 693 F.3d 113 (2d Cir. 2012), the SEC deliberately withheld 30 interview transcripts from the Defendant that contained exculpatory information. I’ve attached a part of the ruling in the Douglass Mackey case below where the 2nd Circuit addresses this. You don’t withhold exculpatory evidence by accident. This was a deliberately illegal and unethical action by SEC attorneys. As far as I know, nobody lost their job from this.

Lying to the Court:

The SEC straight-up lied to the Court in order to obtain a Temporary Restraining Order (TRO) in its case against Debt Box. TROs, for those unfamiliar, are issued ex parte, which means one party (in this case, the SEC) goes into court and tells a judge that “if you don’t do this right now, without letting the other side even know about these proceedings, there will be irreparable harm.” See the judge’s November 30, 2023, order in SEC v. Dig. Licensing (Debt Box) 2:23-cv-00482-RJS-DBP (D. Utah, Nov 30, 2023). In fact, the SEC didn’t just lie about one thing in that case, they lied to the court repeatedly, as the court outlines in detail. As far as I know, nobody lost their job from this. You can google the actual order if you want, but here’s an article summarizing it: https://t.co/SP3xOq4vmd

Acting in an “Arbitrary and Capricious” manner:

The SEC has also been found to have acted in an “arbitrary and capricious” manner in two recent cases: Chamber of Commerce v. SEC (5th Circuit) and in the Grayscale case in the DC Circuit.

What does “arbitrary and capricious” mean? Well, basically, an agency action may be set aside only if it is “arbitrary, capricious, an abuse of discretion, or otherwise not in accordance with law.” 5 U.S.C. § 706(2)(A). The arbitrary-and-capricious standard is “highly deferential” and “presumes the validity of agency action.” Nat'l Ass'n of Clean Air Agencies v. EPA, 489 F.3d 1221, 1228 (D.C. Cir. 2007). “Highly deferential” means you have to f*ck up really, really, really bad to overcome that standard, because the courts are going to start off by presuming you’re not f*cking up at all, much less really, really, really bad. As far as I know, nobody lost their job from this.

Let’s sum up where we are so far:

We have a federal agency, the SEC, that has exactly zero issues with lying to judges, withholding exculpatory evidence, and repeatedly acting improperly with respect to its obligations under the Administrative Procedures Act. Oh, and let’s not forget the general incompetence over the past decade or two.

--> So what on God’s green earth would make anyone with more than two firing neurons believe that the SEC is being honest with opposing counsel, other judges, or defendants in other cases?

“Falsus in uno, falsus in omnibus,” remember? If they’re lying to one judge, defendant, or defense attorney, we can reasonably believe it’s happening a lot more, can’t we?

Maybe people believe the SEC because they keep settling with defendants who never speak out against them! So the SEC must be doing things right if no defendants ever claim they were wrongfully prosecuted, right? If you’re an average citizen who doesn’t know any better, this sounds like an objectively reasonable conclusion.

But we know better, don’t we?

Richard Heart has been a staunch Freedom of Speech advocate long before I even heard his name. The Pulsechain sacrifice was for people who also shared his belief in Freedom of Speech, and it showed that there are plenty of us out there. Maybe the SEC finally picked the wrong door here, and it will be Richard’s case that gets rid of this ridiculous policy forever.

With that backdrop, let’s look at what judges have to say about this SEC policy.

Recent court rulings have shown that judges are (finally) beginning to question the SEC’s policy of “STFU or we’ll bend you over again.” A SDNY judge in 2022 wrote a pretty damn solid takedown of the SEC’s policy and I encourage everyone to read it. It’s not that long, but it’s worth your time I promise you: https://t.co/bg6xiDcx5o

Unfortunately for the defendant here, the judge noted he was bound by 2nd Circuit precedent in the Romeril case, but his final paragraph illustrates his concerns:

“What is the SEC so afraid of? Any criticism, apparently—or, rather, anything that may even “create the impression” of criticism—of that governmental agency. Accordingly, while the Court will approve the Consent Agreement at the request of the parties, consistent with Romeril, 15 F.4th at 172, it does so with reluctance in light of the SEC’s continued and misguided practice of restraining speech. After all, speech “is the means to hold officials accountable to the people,” Citizens United v. FEC, 558 U.S. 310, 339 (2010), and is “essential to effective democracy,” Whitney v. Cal., 274 U.S. 357, 377 (1927) (Brandeis, J., concurring).”

Next up, I found a judge in a 2010 case criticizing this policy, noting that “[o]nly one thing is left certain: the public will never know whether the SEC’s charges are true.” SEC v Vitesse Semiconductor 1:10-cv-09239 (SDNY Dec 10, 2010). I’m personally a big fan of letting people have all the information they need to decide things for themselves. When the government shuts down one side entirely, people don’t get the opportunity to evaluate all necessary information and come to their own conclusions, and that’s wrong on every single possible level.

And recently, two judges in the 5th Circuit in SEC v Novinger stated that nothing in the opinion they issued “approves of or acquiesces in the SEC’s longstanding policy that conditions settlement of any enforcement action on parties’ giving up First Amendment rights” and that “a more effective prior restraint is hard to imagine.”

A “prior restraint” is when the government proactively limits or forbids someone’s speech. Prior restraints are the most onerous form of government suppression, and courts generally severely limit when the government can impose them.

Incredibly, the 5th Circuit also noted that they were informed of a petition filed with the SEC “to review and revoke this SEC policy…filed nearly four years ago” and that the “SEC never responded to the petition.” Those two judges ended with this: “Given the agency’s current activism, I think it will not be long before the courts are called on to fully consider this policy.”

The phrase “current activism” is what caught my eye here, and it means that the Courts are starting to recognize SEC enforcement actions for what they are: more of a political weapon than anything that can be mistaken for investor protection.

Bottom line:

The SEC was formed with the intent of protecting investors, and probably still does that once in a while.

But its current staff includes attorneys who lie to judges, act unethically, withhold evidence, fail to follow their own procedures, and ignore legitimately-filed petitions asking for a review of their policies indefinitely. This should result in the SEC losing the benefit of any doubt, in any court, anywhere. And it should finally force courts to consider whether their settlement policy forcing Defendants to give up their 1stAmendment rights is Constitutional.

After all, consider the following hypothetical scenarios in which the SEC could reopen a case against a crypto founder after settling with them under their own policy:

1. The SEC relies on a whistleblower to initiate a case against some crypto founder, which it then sues for fraud. The founder doesn’t have the resources to litigate so they settle. Later, they learn that the SEC withheld exculpatory evidence, and the founder never would have settled if they had known. Why should this founder be prevented from criticizing the allegations he now knows were based on the SEC’s illegal or unethical acts?

2. Or what if that whistleblower falsified, altered, or simply made-up evidence that the SEC used to force a settlement? If the founder learned that the evidence wasn’t legitimate or authentic after settling, how is it fair or in the interests of anyone, anywhere, to impose a gag order on him so he can’t share that information with the world?

The “STFU forever” policy needs to be struck down not only because it’s unconstitutional to begin with, but also because the SEC is an activist agency with an obvious anti-crypto agenda that will stop at nothing to win, including lying to courts and withholding evidence from defendants.

Go get them, @RichardHeartWin. We’re all behind you.

See you all at the #PulseChainTour in Vegas next week. I’m looking forward to meeting many of you and seeing and hearing about all the great things on the horizon for this ecosystem.

As always, nothing I say is legal advice.

#HEX #PLS #PLSX

Some people have been doxing Satoshi of #Bitcoin fame by leaking their emails with him. A stricter documents retention/deletion policy would help you not violate the privacy of someone you claim to respect. Consider your own documents policy now. Courts can and do force you to give up documents you possess, sometimes at the behest of frivolous lawsuits. Why harm Satoshi?

AVAX stopped working for ~5 hours.

John Deaton (Pro crypto) is running against Elizabeth Warren (Anti crypto) in Massachusetts.

The SEC has been sued in Texas. The complaint reads well and has great quotes from the relevant precedents. https://t.co/trKswi2VaJ

The $UNI token is still trying to figure out what PulseX already figured out. PulseX buy and burn is cool. Or hot? It burns amirite.

PulseChain, HEX, & PulseX continue to operate wonderfully why so many other things fail.

Did you know that: ETFs allow price to decouple from actual supply. ETFs are like adding a fiat inflation bug to an asset...inflation controlled by the exchange authority.

BTC has had a conventional ETF since 2021.

Gold ETF was launched in 1974 (50 years ago)

Look into HEX#

🚨 JUST HAD AN AMAZING TALK WITH @BenArmstrongsX

✅ He said “I’m going to do everything to make sure $HEX #HEX/#PulseChain are adopted, let’s grow!”

✅ He also said “I wouldn’t be in the HEX/PulseChain community if it wasn’t for you Corey.”

✅ I onboard close friends❤️!

@IOHK_Charles I'm sure guvmnt debasing the value of our currency has no effect on companies cutting costs to acquire more units to compete/survive 🙃👎🏼

The people lose up, down, left, right, forwards, and back.

Here is your first class on growing your X/Twitter Account.

Today we learn how to make MEMES the EXTREMELY LAZY (but impactful) WAY

https://t.co/IM1HsxTtA8

❤️💛💚💙

Imagine ignoring my 400 tweets and 15 videos telling you that PulseChain will flip Cardano.

It’s an entire 9x away.

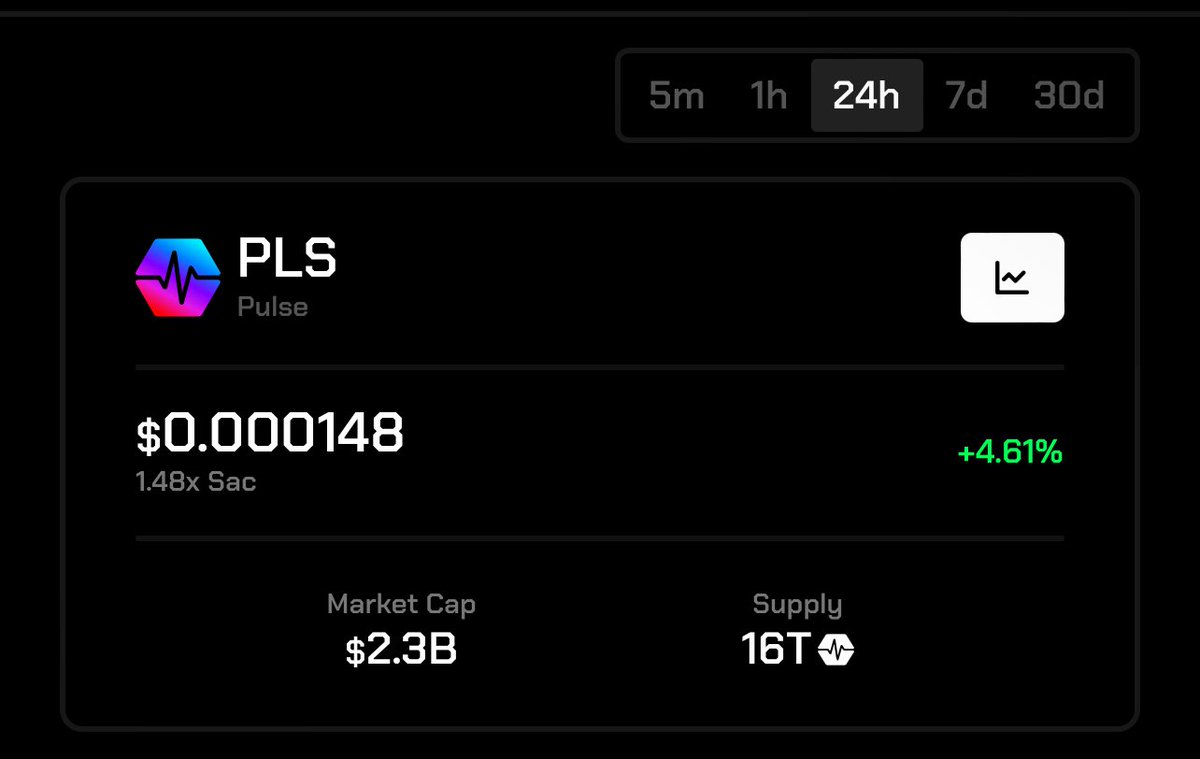

$PLS 9x flippening target for a Core Coin… big if true

![NuclearHerbs's tweet photo. Welcome back to #PulseChainLawSchool everyone! Let’s learn some more Latin:

“Falsus in uno, falsus in omnibus.”

This is a well-known Latin phrase in law, and it means that if someone is found to be lying about one thing, it is reasonable to conclude that they shouldn’t be believed about anything else.

Which brings me to today’s topic: The SEC, and more specifically, settling with the SEC, which is materially different than settling with any other government agency or private party.

The easiest way to describe today’s issue is to quote from the 5th Circuit Court of Appeals in SEC v Novinger, 40 F.4th297 (5th Cir. 2022):

“Since 1972, the SEC has prohibited defendants who settle civil enforcement actions without admitting guilt from publicly denying the allegations in the complaint filed against them. The SEC enacted this no-deny policy, which is codified at 17 C.F.R. 202.5(e), after determining that it was important to avoid creating, or permitting to be created, an impression that a decree is being entered or a sanction imposed, when the conduct alleged did not, in fact, occur. Id. Under the policy, a refusal to admit the allegations is equivalent to a denial, unless the defendant or respondent states that he neither admits nor denies the allegations. Id.”

(FYI, whenever you see “Id” in a case, it means it’s referencing the case it cited immediately prior. This just saves time typing the same case name and citation over and over when you cite it multiple times in a row.)

The short version: If you settle a case with the SEC, you are *never* allowed to deny the allegations they made against you, even if they’re complete bullshit and you only settled because they offered you a minimal fine and it would have cost you 10,000x that amount to fight them in court. If you do speak out (even if you speak the truth), the SEC can reopen the case against you.

Does this seem fundamentally unfair? Absolutely.

Does it seem like a 1st Amendment violation? Absolutely.

So let’s ask a very important question: Why does the SEC think it still deserves to have this policy enforced by courts when it’s racking up a history of legally questionable or outright illegal actions?

By “legally questionable,” I don’t even mean actions that could be reasonably interpreted as incompetence, such as completely f*cking up with ZZZZ Best, Enron, Madoff, FTX, or Alameda. As bad as those failures were, there’s still an argument an attorney could make in court for the actions the SEC took or didn’t take without the judge laughing at them.

I don’t even mean “legally questionable” in the sense of going after favorable news treatment by filing legally problematic complaints, because THAT’S LITERALLY THEIR GOAL. Andrew Vollmer, former SEC deputy general, said the SEC only “wants headlines and therefore it needs to have eye-popping civil penalty numbers” as opposed to effective business regulatory policies.

But incompetence and politics are one thing, deliberately taking illegal and/or unethical actions are another. Let’s take some recent examples:

Deliberately Withholding Exculpatory Evidence:

In United States v. Mahaffy, 693 F.3d 113 (2d Cir. 2012), the SEC deliberately withheld 30 interview transcripts from the Defendant that contained exculpatory information. I’ve attached a part of the ruling in the Douglass Mackey case below where the 2nd Circuit addresses this. You don’t withhold exculpatory evidence by accident. This was a deliberately illegal and unethical action by SEC attorneys. As far as I know, nobody lost their job from this.

Lying to the Court:

The SEC straight-up lied to the Court in order to obtain a Temporary Restraining Order (TRO) in its case against Debt Box. TROs, for those unfamiliar, are issued ex parte, which means one party (in this case, the SEC) goes into court and tells a judge that “if you don’t do this right now, without letting the other side even know about these proceedings, there will be irreparable harm.” See the judge’s November 30, 2023, order in SEC v. Dig. Licensing (Debt Box) 2:23-cv-00482-RJS-DBP (D. Utah, Nov 30, 2023). In fact, the SEC didn’t just lie about one thing in that case, they lied to the court repeatedly, as the court outlines in detail. As far as I know, nobody lost their job from this. You can google the actual order if you want, but here’s an article summarizing it: https://t.co/SP3xOq4vmd

Acting in an “Arbitrary and Capricious” manner:

The SEC has also been found to have acted in an “arbitrary and capricious” manner in two recent cases: Chamber of Commerce v. SEC (5th Circuit) and in the Grayscale case in the DC Circuit.

What does “arbitrary and capricious” mean? Well, basically, an agency action may be set aside only if it is “arbitrary, capricious, an abuse of discretion, or otherwise not in accordance with law.” 5 U.S.C. § 706(2)(A). The arbitrary-and-capricious standard is “highly deferential” and “presumes the validity of agency action.” Nat'l Ass'n of Clean Air Agencies v. EPA, 489 F.3d 1221, 1228 (D.C. Cir. 2007). “Highly deferential” means you have to f*ck up really, really, really bad to overcome that standard, because the courts are going to start off by presuming you’re not f*cking up at all, much less really, really, really bad. As far as I know, nobody lost their job from this.

Let’s sum up where we are so far:

We have a federal agency, the SEC, that has exactly zero issues with lying to judges, withholding exculpatory evidence, and repeatedly acting improperly with respect to its obligations under the Administrative Procedures Act. Oh, and let’s not forget the general incompetence over the past decade or two.

--> So what on God’s green earth would make anyone with more than two firing neurons believe that the SEC is being honest with opposing counsel, other judges, or defendants in other cases?

“Falsus in uno, falsus in omnibus,” remember? If they’re lying to one judge, defendant, or defense attorney, we can reasonably believe it’s happening a lot more, can’t we?

Maybe people believe the SEC because they keep settling with defendants who never speak out against them! So the SEC must be doing things right if no defendants ever claim they were wrongfully prosecuted, right? If you’re an average citizen who doesn’t know any better, this sounds like an objectively reasonable conclusion.

But we know better, don’t we?

Richard Heart has been a staunch Freedom of Speech advocate long before I even heard his name. The Pulsechain sacrifice was for people who also shared his belief in Freedom of Speech, and it showed that there are plenty of us out there. Maybe the SEC finally picked the wrong door here, and it will be Richard’s case that gets rid of this ridiculous policy forever.

With that backdrop, let’s look at what judges have to say about this SEC policy.

Recent court rulings have shown that judges are (finally) beginning to question the SEC’s policy of “STFU or we’ll bend you over again.” A SDNY judge in 2022 wrote a pretty damn solid takedown of the SEC’s policy and I encourage everyone to read it. It’s not that long, but it’s worth your time I promise you: https://t.co/bg6xiDcx5o

Unfortunately for the defendant here, the judge noted he was bound by 2nd Circuit precedent in the Romeril case, but his final paragraph illustrates his concerns:

“What is the SEC so afraid of? Any criticism, apparently—or, rather, anything that may even “create the impression” of criticism—of that governmental agency. Accordingly, while the Court will approve the Consent Agreement at the request of the parties, consistent with Romeril, 15 F.4th at 172, it does so with reluctance in light of the SEC’s continued and misguided practice of restraining speech. After all, speech “is the means to hold officials accountable to the people,” Citizens United v. FEC, 558 U.S. 310, 339 (2010), and is “essential to effective democracy,” Whitney v. Cal., 274 U.S. 357, 377 (1927) (Brandeis, J., concurring).”

Next up, I found a judge in a 2010 case criticizing this policy, noting that “[o]nly one thing is left certain: the public will never know whether the SEC’s charges are true.” SEC v Vitesse Semiconductor 1:10-cv-09239 (SDNY Dec 10, 2010). I’m personally a big fan of letting people have all the information they need to decide things for themselves. When the government shuts down one side entirely, people don’t get the opportunity to evaluate all necessary information and come to their own conclusions, and that’s wrong on every single possible level.

And recently, two judges in the 5th Circuit in SEC v Novinger stated that nothing in the opinion they issued “approves of or acquiesces in the SEC’s longstanding policy that conditions settlement of any enforcement action on parties’ giving up First Amendment rights” and that “a more effective prior restraint is hard to imagine.”

A “prior restraint” is when the government proactively limits or forbids someone’s speech. Prior restraints are the most onerous form of government suppression, and courts generally severely limit when the government can impose them.

Incredibly, the 5th Circuit also noted that they were informed of a petition filed with the SEC “to review and revoke this SEC policy…filed nearly four years ago” and that the “SEC never responded to the petition.” Those two judges ended with this: “Given the agency’s current activism, I think it will not be long before the courts are called on to fully consider this policy.”

The phrase “current activism” is what caught my eye here, and it means that the Courts are starting to recognize SEC enforcement actions for what they are: more of a political weapon than anything that can be mistaken for investor protection.

Bottom line:

The SEC was formed with the intent of protecting investors, and probably still does that once in a while.

But its current staff includes attorneys who lie to judges, act unethically, withhold evidence, fail to follow their own procedures, and ignore legitimately-filed petitions asking for a review of their policies indefinitely. This should result in the SEC losing the benefit of any doubt, in any court, anywhere. And it should finally force courts to consider whether their settlement policy forcing Defendants to give up their 1stAmendment rights is Constitutional.

After all, consider the following hypothetical scenarios in which the SEC could reopen a case against a crypto founder after settling with them under their own policy:

1. The SEC relies on a whistleblower to initiate a case against some crypto founder, which it then sues for fraud. The founder doesn’t have the resources to litigate so they settle. Later, they learn that the SEC withheld exculpatory evidence, and the founder never would have settled if they had known. Why should this founder be prevented from criticizing the allegations he now knows were based on the SEC’s illegal or unethical acts?

2. Or what if that whistleblower falsified, altered, or simply made-up evidence that the SEC used to force a settlement? If the founder learned that the evidence wasn’t legitimate or authentic after settling, how is it fair or in the interests of anyone, anywhere, to impose a gag order on him so he can’t share that information with the world?

The “STFU forever” policy needs to be struck down not only because it’s unconstitutional to begin with, but also because the SEC is an activist agency with an obvious anti-crypto agenda that will stop at nothing to win, including lying to courts and withholding evidence from defendants.

Go get them, @RichardHeartWin. We’re all behind you.

See you all at the #PulseChainTour in Vegas next week. I’m looking forward to meeting many of you and seeing and hearing about all the great things on the horizon for this ecosystem.

As always, nothing I say is legal advice.

#HEX #PLS #PLSX](https://pbs.twimg.com/media/GHl39XaawAAAe1f.png)

![NuclearHerbs's tweet photo. Welcome back to #PulseChainLawSchool everyone! Let’s learn some more Latin:

“Falsus in uno, falsus in omnibus.”

This is a well-known Latin phrase in law, and it means that if someone is found to be lying about one thing, it is reasonable to conclude that they shouldn’t be believed about anything else.

Which brings me to today’s topic: The SEC, and more specifically, settling with the SEC, which is materially different than settling with any other government agency or private party.

The easiest way to describe today’s issue is to quote from the 5th Circuit Court of Appeals in SEC v Novinger, 40 F.4th297 (5th Cir. 2022):

“Since 1972, the SEC has prohibited defendants who settle civil enforcement actions without admitting guilt from publicly denying the allegations in the complaint filed against them. The SEC enacted this no-deny policy, which is codified at 17 C.F.R. 202.5(e), after determining that it was important to avoid creating, or permitting to be created, an impression that a decree is being entered or a sanction imposed, when the conduct alleged did not, in fact, occur. Id. Under the policy, a refusal to admit the allegations is equivalent to a denial, unless the defendant or respondent states that he neither admits nor denies the allegations. Id.”

(FYI, whenever you see “Id” in a case, it means it’s referencing the case it cited immediately prior. This just saves time typing the same case name and citation over and over when you cite it multiple times in a row.)

The short version: If you settle a case with the SEC, you are *never* allowed to deny the allegations they made against you, even if they’re complete bullshit and you only settled because they offered you a minimal fine and it would have cost you 10,000x that amount to fight them in court. If you do speak out (even if you speak the truth), the SEC can reopen the case against you.

Does this seem fundamentally unfair? Absolutely.

Does it seem like a 1st Amendment violation? Absolutely.

So let’s ask a very important question: Why does the SEC think it still deserves to have this policy enforced by courts when it’s racking up a history of legally questionable or outright illegal actions?

By “legally questionable,” I don’t even mean actions that could be reasonably interpreted as incompetence, such as completely f*cking up with ZZZZ Best, Enron, Madoff, FTX, or Alameda. As bad as those failures were, there’s still an argument an attorney could make in court for the actions the SEC took or didn’t take without the judge laughing at them.

I don’t even mean “legally questionable” in the sense of going after favorable news treatment by filing legally problematic complaints, because THAT’S LITERALLY THEIR GOAL. Andrew Vollmer, former SEC deputy general, said the SEC only “wants headlines and therefore it needs to have eye-popping civil penalty numbers” as opposed to effective business regulatory policies.

But incompetence and politics are one thing, deliberately taking illegal and/or unethical actions are another. Let’s take some recent examples:

Deliberately Withholding Exculpatory Evidence:

In United States v. Mahaffy, 693 F.3d 113 (2d Cir. 2012), the SEC deliberately withheld 30 interview transcripts from the Defendant that contained exculpatory information. I’ve attached a part of the ruling in the Douglass Mackey case below where the 2nd Circuit addresses this. You don’t withhold exculpatory evidence by accident. This was a deliberately illegal and unethical action by SEC attorneys. As far as I know, nobody lost their job from this.

Lying to the Court:

The SEC straight-up lied to the Court in order to obtain a Temporary Restraining Order (TRO) in its case against Debt Box. TROs, for those unfamiliar, are issued ex parte, which means one party (in this case, the SEC) goes into court and tells a judge that “if you don’t do this right now, without letting the other side even know about these proceedings, there will be irreparable harm.” See the judge’s November 30, 2023, order in SEC v. Dig. Licensing (Debt Box) 2:23-cv-00482-RJS-DBP (D. Utah, Nov 30, 2023). In fact, the SEC didn’t just lie about one thing in that case, they lied to the court repeatedly, as the court outlines in detail. As far as I know, nobody lost their job from this. You can google the actual order if you want, but here’s an article summarizing it: https://t.co/SP3xOq4vmd

Acting in an “Arbitrary and Capricious” manner:

The SEC has also been found to have acted in an “arbitrary and capricious” manner in two recent cases: Chamber of Commerce v. SEC (5th Circuit) and in the Grayscale case in the DC Circuit.

What does “arbitrary and capricious” mean? Well, basically, an agency action may be set aside only if it is “arbitrary, capricious, an abuse of discretion, or otherwise not in accordance with law.” 5 U.S.C. § 706(2)(A). The arbitrary-and-capricious standard is “highly deferential” and “presumes the validity of agency action.” Nat'l Ass'n of Clean Air Agencies v. EPA, 489 F.3d 1221, 1228 (D.C. Cir. 2007). “Highly deferential” means you have to f*ck up really, really, really bad to overcome that standard, because the courts are going to start off by presuming you’re not f*cking up at all, much less really, really, really bad. As far as I know, nobody lost their job from this.

Let’s sum up where we are so far:

We have a federal agency, the SEC, that has exactly zero issues with lying to judges, withholding exculpatory evidence, and repeatedly acting improperly with respect to its obligations under the Administrative Procedures Act. Oh, and let’s not forget the general incompetence over the past decade or two.

--> So what on God’s green earth would make anyone with more than two firing neurons believe that the SEC is being honest with opposing counsel, other judges, or defendants in other cases?

“Falsus in uno, falsus in omnibus,” remember? If they’re lying to one judge, defendant, or defense attorney, we can reasonably believe it’s happening a lot more, can’t we?

Maybe people believe the SEC because they keep settling with defendants who never speak out against them! So the SEC must be doing things right if no defendants ever claim they were wrongfully prosecuted, right? If you’re an average citizen who doesn’t know any better, this sounds like an objectively reasonable conclusion.

But we know better, don’t we?

Richard Heart has been a staunch Freedom of Speech advocate long before I even heard his name. The Pulsechain sacrifice was for people who also shared his belief in Freedom of Speech, and it showed that there are plenty of us out there. Maybe the SEC finally picked the wrong door here, and it will be Richard’s case that gets rid of this ridiculous policy forever.

With that backdrop, let’s look at what judges have to say about this SEC policy.

Recent court rulings have shown that judges are (finally) beginning to question the SEC’s policy of “STFU or we’ll bend you over again.” A SDNY judge in 2022 wrote a pretty damn solid takedown of the SEC’s policy and I encourage everyone to read it. It’s not that long, but it’s worth your time I promise you: https://t.co/bg6xiDcx5o

Unfortunately for the defendant here, the judge noted he was bound by 2nd Circuit precedent in the Romeril case, but his final paragraph illustrates his concerns:

“What is the SEC so afraid of? Any criticism, apparently—or, rather, anything that may even “create the impression” of criticism—of that governmental agency. Accordingly, while the Court will approve the Consent Agreement at the request of the parties, consistent with Romeril, 15 F.4th at 172, it does so with reluctance in light of the SEC’s continued and misguided practice of restraining speech. After all, speech “is the means to hold officials accountable to the people,” Citizens United v. FEC, 558 U.S. 310, 339 (2010), and is “essential to effective democracy,” Whitney v. Cal., 274 U.S. 357, 377 (1927) (Brandeis, J., concurring).”

Next up, I found a judge in a 2010 case criticizing this policy, noting that “[o]nly one thing is left certain: the public will never know whether the SEC’s charges are true.” SEC v Vitesse Semiconductor 1:10-cv-09239 (SDNY Dec 10, 2010). I’m personally a big fan of letting people have all the information they need to decide things for themselves. When the government shuts down one side entirely, people don’t get the opportunity to evaluate all necessary information and come to their own conclusions, and that’s wrong on every single possible level.

And recently, two judges in the 5th Circuit in SEC v Novinger stated that nothing in the opinion they issued “approves of or acquiesces in the SEC’s longstanding policy that conditions settlement of any enforcement action on parties’ giving up First Amendment rights” and that “a more effective prior restraint is hard to imagine.”

A “prior restraint” is when the government proactively limits or forbids someone’s speech. Prior restraints are the most onerous form of government suppression, and courts generally severely limit when the government can impose them.

Incredibly, the 5th Circuit also noted that they were informed of a petition filed with the SEC “to review and revoke this SEC policy…filed nearly four years ago” and that the “SEC never responded to the petition.” Those two judges ended with this: “Given the agency’s current activism, I think it will not be long before the courts are called on to fully consider this policy.”

The phrase “current activism” is what caught my eye here, and it means that the Courts are starting to recognize SEC enforcement actions for what they are: more of a political weapon than anything that can be mistaken for investor protection.

Bottom line:

The SEC was formed with the intent of protecting investors, and probably still does that once in a while.

But its current staff includes attorneys who lie to judges, act unethically, withhold evidence, fail to follow their own procedures, and ignore legitimately-filed petitions asking for a review of their policies indefinitely. This should result in the SEC losing the benefit of any doubt, in any court, anywhere. And it should finally force courts to consider whether their settlement policy forcing Defendants to give up their 1stAmendment rights is Constitutional.

After all, consider the following hypothetical scenarios in which the SEC could reopen a case against a crypto founder after settling with them under their own policy:

1. The SEC relies on a whistleblower to initiate a case against some crypto founder, which it then sues for fraud. The founder doesn’t have the resources to litigate so they settle. Later, they learn that the SEC withheld exculpatory evidence, and the founder never would have settled if they had known. Why should this founder be prevented from criticizing the allegations he now knows were based on the SEC’s illegal or unethical acts?

2. Or what if that whistleblower falsified, altered, or simply made-up evidence that the SEC used to force a settlement? If the founder learned that the evidence wasn’t legitimate or authentic after settling, how is it fair or in the interests of anyone, anywhere, to impose a gag order on him so he can’t share that information with the world?

The “STFU forever” policy needs to be struck down not only because it’s unconstitutional to begin with, but also because the SEC is an activist agency with an obvious anti-crypto agenda that will stop at nothing to win, including lying to courts and withholding evidence from defendants.

Go get them, @RichardHeartWin. We’re all behind you.

See you all at the #PulseChainTour in Vegas next week. I’m looking forward to meeting many of you and seeing and hearing about all the great things on the horizon for this ecosystem.

As always, nothing I say is legal advice.

#HEX #PLS #PLSX](https://pbs.twimg.com/media/GHl39VzasAAOA40.png)

![NuclearHerbs's tweet photo. Welcome back to #PulseChainLawSchool everyone! Let’s learn some more Latin:

“Falsus in uno, falsus in omnibus.”

This is a well-known Latin phrase in law, and it means that if someone is found to be lying about one thing, it is reasonable to conclude that they shouldn’t be believed about anything else.

Which brings me to today’s topic: The SEC, and more specifically, settling with the SEC, which is materially different than settling with any other government agency or private party.

The easiest way to describe today’s issue is to quote from the 5th Circuit Court of Appeals in SEC v Novinger, 40 F.4th297 (5th Cir. 2022):

“Since 1972, the SEC has prohibited defendants who settle civil enforcement actions without admitting guilt from publicly denying the allegations in the complaint filed against them. The SEC enacted this no-deny policy, which is codified at 17 C.F.R. 202.5(e), after determining that it was important to avoid creating, or permitting to be created, an impression that a decree is being entered or a sanction imposed, when the conduct alleged did not, in fact, occur. Id. Under the policy, a refusal to admit the allegations is equivalent to a denial, unless the defendant or respondent states that he neither admits nor denies the allegations. Id.”

(FYI, whenever you see “Id” in a case, it means it’s referencing the case it cited immediately prior. This just saves time typing the same case name and citation over and over when you cite it multiple times in a row.)

The short version: If you settle a case with the SEC, you are *never* allowed to deny the allegations they made against you, even if they’re complete bullshit and you only settled because they offered you a minimal fine and it would have cost you 10,000x that amount to fight them in court. If you do speak out (even if you speak the truth), the SEC can reopen the case against you.

Does this seem fundamentally unfair? Absolutely.

Does it seem like a 1st Amendment violation? Absolutely.

So let’s ask a very important question: Why does the SEC think it still deserves to have this policy enforced by courts when it’s racking up a history of legally questionable or outright illegal actions?

By “legally questionable,” I don’t even mean actions that could be reasonably interpreted as incompetence, such as completely f*cking up with ZZZZ Best, Enron, Madoff, FTX, or Alameda. As bad as those failures were, there’s still an argument an attorney could make in court for the actions the SEC took or didn’t take without the judge laughing at them.

I don’t even mean “legally questionable” in the sense of going after favorable news treatment by filing legally problematic complaints, because THAT’S LITERALLY THEIR GOAL. Andrew Vollmer, former SEC deputy general, said the SEC only “wants headlines and therefore it needs to have eye-popping civil penalty numbers” as opposed to effective business regulatory policies.

But incompetence and politics are one thing, deliberately taking illegal and/or unethical actions are another. Let’s take some recent examples:

Deliberately Withholding Exculpatory Evidence:

In United States v. Mahaffy, 693 F.3d 113 (2d Cir. 2012), the SEC deliberately withheld 30 interview transcripts from the Defendant that contained exculpatory information. I’ve attached a part of the ruling in the Douglass Mackey case below where the 2nd Circuit addresses this. You don’t withhold exculpatory evidence by accident. This was a deliberately illegal and unethical action by SEC attorneys. As far as I know, nobody lost their job from this.

Lying to the Court:

The SEC straight-up lied to the Court in order to obtain a Temporary Restraining Order (TRO) in its case against Debt Box. TROs, for those unfamiliar, are issued ex parte, which means one party (in this case, the SEC) goes into court and tells a judge that “if you don’t do this right now, without letting the other side even know about these proceedings, there will be irreparable harm.” See the judge’s November 30, 2023, order in SEC v. Dig. Licensing (Debt Box) 2:23-cv-00482-RJS-DBP (D. Utah, Nov 30, 2023). In fact, the SEC didn’t just lie about one thing in that case, they lied to the court repeatedly, as the court outlines in detail. As far as I know, nobody lost their job from this. You can google the actual order if you want, but here’s an article summarizing it: https://t.co/SP3xOq4vmd

Acting in an “Arbitrary and Capricious” manner:

The SEC has also been found to have acted in an “arbitrary and capricious” manner in two recent cases: Chamber of Commerce v. SEC (5th Circuit) and in the Grayscale case in the DC Circuit.

What does “arbitrary and capricious” mean? Well, basically, an agency action may be set aside only if it is “arbitrary, capricious, an abuse of discretion, or otherwise not in accordance with law.” 5 U.S.C. § 706(2)(A). The arbitrary-and-capricious standard is “highly deferential” and “presumes the validity of agency action.” Nat'l Ass'n of Clean Air Agencies v. EPA, 489 F.3d 1221, 1228 (D.C. Cir. 2007). “Highly deferential” means you have to f*ck up really, really, really bad to overcome that standard, because the courts are going to start off by presuming you’re not f*cking up at all, much less really, really, really bad. As far as I know, nobody lost their job from this.

Let’s sum up where we are so far:

We have a federal agency, the SEC, that has exactly zero issues with lying to judges, withholding exculpatory evidence, and repeatedly acting improperly with respect to its obligations under the Administrative Procedures Act. Oh, and let’s not forget the general incompetence over the past decade or two.

--> So what on God’s green earth would make anyone with more than two firing neurons believe that the SEC is being honest with opposing counsel, other judges, or defendants in other cases?

“Falsus in uno, falsus in omnibus,” remember? If they’re lying to one judge, defendant, or defense attorney, we can reasonably believe it’s happening a lot more, can’t we?

Maybe people believe the SEC because they keep settling with defendants who never speak out against them! So the SEC must be doing things right if no defendants ever claim they were wrongfully prosecuted, right? If you’re an average citizen who doesn’t know any better, this sounds like an objectively reasonable conclusion.

But we know better, don’t we?

Richard Heart has been a staunch Freedom of Speech advocate long before I even heard his name. The Pulsechain sacrifice was for people who also shared his belief in Freedom of Speech, and it showed that there are plenty of us out there. Maybe the SEC finally picked the wrong door here, and it will be Richard’s case that gets rid of this ridiculous policy forever.

With that backdrop, let’s look at what judges have to say about this SEC policy.

Recent court rulings have shown that judges are (finally) beginning to question the SEC’s policy of “STFU or we’ll bend you over again.” A SDNY judge in 2022 wrote a pretty damn solid takedown of the SEC’s policy and I encourage everyone to read it. It’s not that long, but it’s worth your time I promise you: https://t.co/bg6xiDcx5o

Unfortunately for the defendant here, the judge noted he was bound by 2nd Circuit precedent in the Romeril case, but his final paragraph illustrates his concerns:

“What is the SEC so afraid of? Any criticism, apparently—or, rather, anything that may even “create the impression” of criticism—of that governmental agency. Accordingly, while the Court will approve the Consent Agreement at the request of the parties, consistent with Romeril, 15 F.4th at 172, it does so with reluctance in light of the SEC’s continued and misguided practice of restraining speech. After all, speech “is the means to hold officials accountable to the people,” Citizens United v. FEC, 558 U.S. 310, 339 (2010), and is “essential to effective democracy,” Whitney v. Cal., 274 U.S. 357, 377 (1927) (Brandeis, J., concurring).”

Next up, I found a judge in a 2010 case criticizing this policy, noting that “[o]nly one thing is left certain: the public will never know whether the SEC’s charges are true.” SEC v Vitesse Semiconductor 1:10-cv-09239 (SDNY Dec 10, 2010). I’m personally a big fan of letting people have all the information they need to decide things for themselves. When the government shuts down one side entirely, people don’t get the opportunity to evaluate all necessary information and come to their own conclusions, and that’s wrong on every single possible level.

And recently, two judges in the 5th Circuit in SEC v Novinger stated that nothing in the opinion they issued “approves of or acquiesces in the SEC’s longstanding policy that conditions settlement of any enforcement action on parties’ giving up First Amendment rights” and that “a more effective prior restraint is hard to imagine.”

A “prior restraint” is when the government proactively limits or forbids someone’s speech. Prior restraints are the most onerous form of government suppression, and courts generally severely limit when the government can impose them.

Incredibly, the 5th Circuit also noted that they were informed of a petition filed with the SEC “to review and revoke this SEC policy…filed nearly four years ago” and that the “SEC never responded to the petition.” Those two judges ended with this: “Given the agency’s current activism, I think it will not be long before the courts are called on to fully consider this policy.”

The phrase “current activism” is what caught my eye here, and it means that the Courts are starting to recognize SEC enforcement actions for what they are: more of a political weapon than anything that can be mistaken for investor protection.

Bottom line:

The SEC was formed with the intent of protecting investors, and probably still does that once in a while.

But its current staff includes attorneys who lie to judges, act unethically, withhold evidence, fail to follow their own procedures, and ignore legitimately-filed petitions asking for a review of their policies indefinitely. This should result in the SEC losing the benefit of any doubt, in any court, anywhere. And it should finally force courts to consider whether their settlement policy forcing Defendants to give up their 1stAmendment rights is Constitutional.

After all, consider the following hypothetical scenarios in which the SEC could reopen a case against a crypto founder after settling with them under their own policy:

1. The SEC relies on a whistleblower to initiate a case against some crypto founder, which it then sues for fraud. The founder doesn’t have the resources to litigate so they settle. Later, they learn that the SEC withheld exculpatory evidence, and the founder never would have settled if they had known. Why should this founder be prevented from criticizing the allegations he now knows were based on the SEC’s illegal or unethical acts?

2. Or what if that whistleblower falsified, altered, or simply made-up evidence that the SEC used to force a settlement? If the founder learned that the evidence wasn’t legitimate or authentic after settling, how is it fair or in the interests of anyone, anywhere, to impose a gag order on him so he can’t share that information with the world?

The “STFU forever” policy needs to be struck down not only because it’s unconstitutional to begin with, but also because the SEC is an activist agency with an obvious anti-crypto agenda that will stop at nothing to win, including lying to courts and withholding evidence from defendants.

Go get them, @RichardHeartWin. We’re all behind you.

See you all at the #PulseChainTour in Vegas next week. I’m looking forward to meeting many of you and seeing and hearing about all the great things on the horizon for this ecosystem.

As always, nothing I say is legal advice.

#HEX #PLS #PLSX](https://pbs.twimg.com/media/GHl358QbkAAYYjz.jpg)

![NuclearHerbs's tweet photo. Welcome back to #PulseChainLawSchool everyone! Let’s learn some more Latin:

“Falsus in uno, falsus in omnibus.”

This is a well-known Latin phrase in law, and it means that if someone is found to be lying about one thing, it is reasonable to conclude that they shouldn’t be believed about anything else.

Which brings me to today’s topic: The SEC, and more specifically, settling with the SEC, which is materially different than settling with any other government agency or private party.

The easiest way to describe today’s issue is to quote from the 5th Circuit Court of Appeals in SEC v Novinger, 40 F.4th297 (5th Cir. 2022):

“Since 1972, the SEC has prohibited defendants who settle civil enforcement actions without admitting guilt from publicly denying the allegations in the complaint filed against them. The SEC enacted this no-deny policy, which is codified at 17 C.F.R. 202.5(e), after determining that it was important to avoid creating, or permitting to be created, an impression that a decree is being entered or a sanction imposed, when the conduct alleged did not, in fact, occur. Id. Under the policy, a refusal to admit the allegations is equivalent to a denial, unless the defendant or respondent states that he neither admits nor denies the allegations. Id.”

(FYI, whenever you see “Id” in a case, it means it’s referencing the case it cited immediately prior. This just saves time typing the same case name and citation over and over when you cite it multiple times in a row.)

The short version: If you settle a case with the SEC, you are *never* allowed to deny the allegations they made against you, even if they’re complete bullshit and you only settled because they offered you a minimal fine and it would have cost you 10,000x that amount to fight them in court. If you do speak out (even if you speak the truth), the SEC can reopen the case against you.

Does this seem fundamentally unfair? Absolutely.

Does it seem like a 1st Amendment violation? Absolutely.

So let’s ask a very important question: Why does the SEC think it still deserves to have this policy enforced by courts when it’s racking up a history of legally questionable or outright illegal actions?

By “legally questionable,” I don’t even mean actions that could be reasonably interpreted as incompetence, such as completely f*cking up with ZZZZ Best, Enron, Madoff, FTX, or Alameda. As bad as those failures were, there’s still an argument an attorney could make in court for the actions the SEC took or didn’t take without the judge laughing at them.

I don’t even mean “legally questionable” in the sense of going after favorable news treatment by filing legally problematic complaints, because THAT’S LITERALLY THEIR GOAL. Andrew Vollmer, former SEC deputy general, said the SEC only “wants headlines and therefore it needs to have eye-popping civil penalty numbers” as opposed to effective business regulatory policies.

But incompetence and politics are one thing, deliberately taking illegal and/or unethical actions are another. Let’s take some recent examples:

Deliberately Withholding Exculpatory Evidence:

In United States v. Mahaffy, 693 F.3d 113 (2d Cir. 2012), the SEC deliberately withheld 30 interview transcripts from the Defendant that contained exculpatory information. I’ve attached a part of the ruling in the Douglass Mackey case below where the 2nd Circuit addresses this. You don’t withhold exculpatory evidence by accident. This was a deliberately illegal and unethical action by SEC attorneys. As far as I know, nobody lost their job from this.

Lying to the Court:

The SEC straight-up lied to the Court in order to obtain a Temporary Restraining Order (TRO) in its case against Debt Box. TROs, for those unfamiliar, are issued ex parte, which means one party (in this case, the SEC) goes into court and tells a judge that “if you don’t do this right now, without letting the other side even know about these proceedings, there will be irreparable harm.” See the judge’s November 30, 2023, order in SEC v. Dig. Licensing (Debt Box) 2:23-cv-00482-RJS-DBP (D. Utah, Nov 30, 2023). In fact, the SEC didn’t just lie about one thing in that case, they lied to the court repeatedly, as the court outlines in detail. As far as I know, nobody lost their job from this. You can google the actual order if you want, but here’s an article summarizing it: https://t.co/SP3xOq4vmd

Acting in an “Arbitrary and Capricious” manner:

The SEC has also been found to have acted in an “arbitrary and capricious” manner in two recent cases: Chamber of Commerce v. SEC (5th Circuit) and in the Grayscale case in the DC Circuit.

What does “arbitrary and capricious” mean? Well, basically, an agency action may be set aside only if it is “arbitrary, capricious, an abuse of discretion, or otherwise not in accordance with law.” 5 U.S.C. § 706(2)(A). The arbitrary-and-capricious standard is “highly deferential” and “presumes the validity of agency action.” Nat'l Ass'n of Clean Air Agencies v. EPA, 489 F.3d 1221, 1228 (D.C. Cir. 2007). “Highly deferential” means you have to f*ck up really, really, really bad to overcome that standard, because the courts are going to start off by presuming you’re not f*cking up at all, much less really, really, really bad. As far as I know, nobody lost their job from this.

Let’s sum up where we are so far:

We have a federal agency, the SEC, that has exactly zero issues with lying to judges, withholding exculpatory evidence, and repeatedly acting improperly with respect to its obligations under the Administrative Procedures Act. Oh, and let’s not forget the general incompetence over the past decade or two.

--> So what on God’s green earth would make anyone with more than two firing neurons believe that the SEC is being honest with opposing counsel, other judges, or defendants in other cases?

“Falsus in uno, falsus in omnibus,” remember? If they’re lying to one judge, defendant, or defense attorney, we can reasonably believe it’s happening a lot more, can’t we?

Maybe people believe the SEC because they keep settling with defendants who never speak out against them! So the SEC must be doing things right if no defendants ever claim they were wrongfully prosecuted, right? If you’re an average citizen who doesn’t know any better, this sounds like an objectively reasonable conclusion.

But we know better, don’t we?

Richard Heart has been a staunch Freedom of Speech advocate long before I even heard his name. The Pulsechain sacrifice was for people who also shared his belief in Freedom of Speech, and it showed that there are plenty of us out there. Maybe the SEC finally picked the wrong door here, and it will be Richard’s case that gets rid of this ridiculous policy forever.

With that backdrop, let’s look at what judges have to say about this SEC policy.

Recent court rulings have shown that judges are (finally) beginning to question the SEC’s policy of “STFU or we’ll bend you over again.” A SDNY judge in 2022 wrote a pretty damn solid takedown of the SEC’s policy and I encourage everyone to read it. It’s not that long, but it’s worth your time I promise you: https://t.co/bg6xiDcx5o

Unfortunately for the defendant here, the judge noted he was bound by 2nd Circuit precedent in the Romeril case, but his final paragraph illustrates his concerns:

“What is the SEC so afraid of? Any criticism, apparently—or, rather, anything that may even “create the impression” of criticism—of that governmental agency. Accordingly, while the Court will approve the Consent Agreement at the request of the parties, consistent with Romeril, 15 F.4th at 172, it does so with reluctance in light of the SEC’s continued and misguided practice of restraining speech. After all, speech “is the means to hold officials accountable to the people,” Citizens United v. FEC, 558 U.S. 310, 339 (2010), and is “essential to effective democracy,” Whitney v. Cal., 274 U.S. 357, 377 (1927) (Brandeis, J., concurring).”

Next up, I found a judge in a 2010 case criticizing this policy, noting that “[o]nly one thing is left certain: the public will never know whether the SEC’s charges are true.” SEC v Vitesse Semiconductor 1:10-cv-09239 (SDNY Dec 10, 2010). I’m personally a big fan of letting people have all the information they need to decide things for themselves. When the government shuts down one side entirely, people don’t get the opportunity to evaluate all necessary information and come to their own conclusions, and that’s wrong on every single possible level.

And recently, two judges in the 5th Circuit in SEC v Novinger stated that nothing in the opinion they issued “approves of or acquiesces in the SEC’s longstanding policy that conditions settlement of any enforcement action on parties’ giving up First Amendment rights” and that “a more effective prior restraint is hard to imagine.”

A “prior restraint” is when the government proactively limits or forbids someone’s speech. Prior restraints are the most onerous form of government suppression, and courts generally severely limit when the government can impose them.

Incredibly, the 5th Circuit also noted that they were informed of a petition filed with the SEC “to review and revoke this SEC policy…filed nearly four years ago” and that the “SEC never responded to the petition.” Those two judges ended with this: “Given the agency’s current activism, I think it will not be long before the courts are called on to fully consider this policy.”

The phrase “current activism” is what caught my eye here, and it means that the Courts are starting to recognize SEC enforcement actions for what they are: more of a political weapon than anything that can be mistaken for investor protection.

Bottom line:

The SEC was formed with the intent of protecting investors, and probably still does that once in a while.

But its current staff includes attorneys who lie to judges, act unethically, withhold evidence, fail to follow their own procedures, and ignore legitimately-filed petitions asking for a review of their policies indefinitely. This should result in the SEC losing the benefit of any doubt, in any court, anywhere. And it should finally force courts to consider whether their settlement policy forcing Defendants to give up their 1stAmendment rights is Constitutional.

After all, consider the following hypothetical scenarios in which the SEC could reopen a case against a crypto founder after settling with them under their own policy:

1. The SEC relies on a whistleblower to initiate a case against some crypto founder, which it then sues for fraud. The founder doesn’t have the resources to litigate so they settle. Later, they learn that the SEC withheld exculpatory evidence, and the founder never would have settled if they had known. Why should this founder be prevented from criticizing the allegations he now knows were based on the SEC’s illegal or unethical acts?

2. Or what if that whistleblower falsified, altered, or simply made-up evidence that the SEC used to force a settlement? If the founder learned that the evidence wasn’t legitimate or authentic after settling, how is it fair or in the interests of anyone, anywhere, to impose a gag order on him so he can’t share that information with the world?

The “STFU forever” policy needs to be struck down not only because it’s unconstitutional to begin with, but also because the SEC is an activist agency with an obvious anti-crypto agenda that will stop at nothing to win, including lying to courts and withholding evidence from defendants.

Go get them, @RichardHeartWin. We’re all behind you.

See you all at the #PulseChainTour in Vegas next week. I’m looking forward to meeting many of you and seeing and hearing about all the great things on the horizon for this ecosystem.

As always, nothing I say is legal advice.

#HEX #PLS #PLSX](https://pbs.twimg.com/media/GHl39Y4b0AAS_nP.jpg)