Since the closure of the Strait of Hormuz caused the biggest flood of oil ever, now that it's reclosing, the glut should get even bigger

Gonna short oil so hard on Monday

When sci-fi and valuation fiction intersect, consider THE TWO RULES OF INVESTING:

Rule # 1: Never lose money.

Rule # 2: Never forget to not pay 125 times SALES on the first trading day for the most overhyped, overpromoted, overvalued, capital-intensive, largest IPO ever.

It was marketed and structured to open today much higher than yesterday’s insane $135/share, $1.8 trillion offering price. At the end of the day, price matters.

Ben Graham said it best: “The distinction between investment and speculation in common stocks has always been a useful one and its disappearance is a cause for concern.”

I have quite a bit of my net worth that I don't manage with dodge and cox very good track record over the last 50 years they are very overweight health care and financials.

Not one, not two, but three S&P 500 sectors are testing either Dot-Com or GFC extremes. Relative to the rest of the market, Healthcare is back to March 2000 specifically. Consumer Staples = Dec. 1999. The S&P 500 Financials sector just broke March 6, 2009.

@toiletkingcap I'm not a tech investor but Joseph Carlson's latest video made a very good case for Google saying that they're just beating everyone else to the trough for Capital before all These big ipos hit

People are asking me why I'm chilling & so relaxed about the oil prices not matching reality. Here's some brief thoughts.

The simple answer is I'm confident in my personal ability to predict long term macro trends in commodities. I've been doing this for years, and every time I hit a huge return it started just as frustrating as this one.

This is also why I'm trying to shitpost quality for you guys. It's to show you that at the end of the day, the fundamentals pull the future return higher.

Even if there is a deal tomorrow, the long term outlook for any undervalued oil producer is higher than their current price, assuming management don't fuck up.

Honestly, I haven't even been checking the charts much, other than buying a ton of Journey energy today because it pulled back such an unreasonable amount and I happened to be sent a screenshot of it down over 30% from recent peaks.

The last thing I'll say is this is basically (in my opinion) an investor's dream set up. We're making an asymmetric bet, in the worst case we lose maybe 20%. But in the expected case, where Iran refuse to surrender their uranium and the USA blockade continues, these undervalued oil companies with tax pools larger than their market caps (ensuring tax free sales) will give hilarious outsized returns.

Major facts:

1. Iran mined the strait and is still adding more mines since the USA attacked them while they did so within the last 72 hours.

2. The USA is still "defensively" (what a PR word!) bombing Iran.

3. The Iranians won't surrender their uranium. If they would, they wouldn't have been recently assassinated by the zionist empire. The remaining Iranians hold even stronger beliefs about the importance of uranium to a sovereign nations security.

Weak facts:

1. Iran wants a Lebanese ceasefire, this probably won't happen cuz Israel is, well, Israel. You know, the country that redefines the term "defends themself", to include "preemptively bombing anyone they feel like" and arbitrarily committing war crimes whenever they feel like it (examples include but are not limited to poisoning a supply chain so pagers blow up and maim whoever happens to be near them, including children, and outright sniping children in the head because why not, they're prehistoric animals anyway, right).

2. Trump can't pay Iran more than Obama paid them or he will lose all support from his base. Right now Iran is demanding 25bil. Will trump cave? Who knows, that's why this is a weak fact. He is the king of the TACO.

3. Iran want to remain in control of the strait, but technically, it's not theirs to control under current international law and the current status quo. The thing is, the international community won't care much since there's not much alternative. They necessarily must get on their knees for Iran cuz most of them need a boost to Arabian exports desperately.

All that said, everyone is a f*cking idiot. So don't be surprised if a deal gets made, but do know, that we've (almost surely) passed the point of no return. My opinion is that it's safe to value oil producers with $80 WTI price floor.

Of course, this could be the first time I'm wrong, but this feels like a hard time to end up wrong. I'm simply betting that Iran cares about its sovereignty.

Best,

G

Greg Abel didn't touch $MCO

Dev Kantesaria didn't touch $MCO

Chris Hohn is buying more $MCO

The stock is trading at 2024 levels, no signs of disruption, and the big boys aren't selling....solid company right there

The Royal Bank of Canada (TSX: RY) officially filed a Schedule 13G disclosing that they have crossed the threshold to hold 6.55% of the total outstanding float of Obsidian Energy $OBE $OBE.TO (specifically holding 4,415,116 shares).

Institutions and insiders now own ~35% of a little $1.175B CAD market cap company.

A company that $CNQ must buy (in my humble opinion) because $OBE's 700 contiguous sections are in the middle of their Athabasca expansion plans.

And I love,

@energyburrito@GavMcCracken

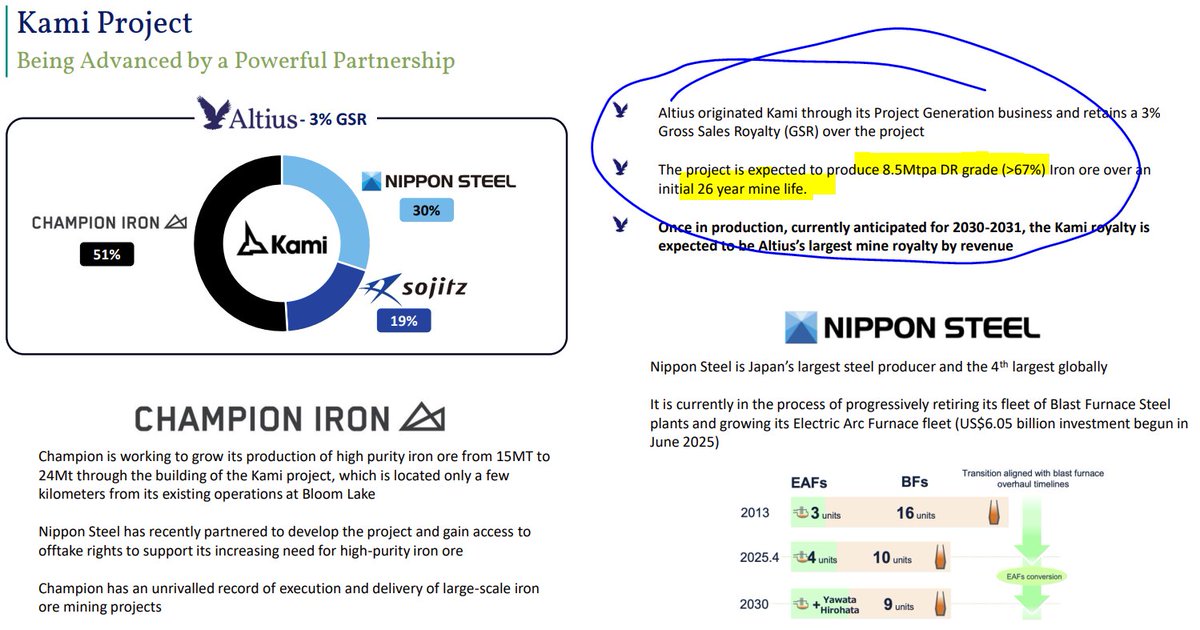

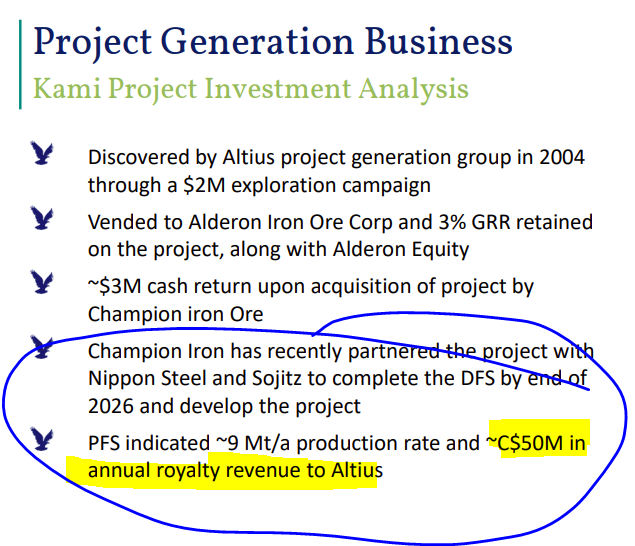

$tmcr 10x revs for 23yr dr iron ore asset

$als.to dr iron ore asset being built by $cia.to has 26yr mine life, throws off $50m/yr, and currently in sell-side models @ $150m nav

(and yes, total investment $2m)

My thoughts on $BRK

People overcomplicate $BRK because they try to value every piece perfectly down to the decimal. They debate price to book, intrinsic value formulas, and build giant spreadsheets modeling every subsidiary. Meanwhile I look at it much more simply. $BRK has roughly $400b in cash and around $300b in stocks.

That’s about $700b right there between cash and equities alone. So when the company is worth around $1t, you’re basically paying roughly $300b for everything else. That includes the railroad, the energy business, insurance operations, manufacturing, distribution, service businesses, and one of the greatest collections of operating assets ever assembled.

And honestly I think people massively underestimate the value of the insurance float. The float is one of the greatest financial assets ever created because $BRK gets access to enormous amounts of capital at extremely attractive economics. Most people do not fully understand how powerful that becomes over decades. That float has quietly fueled one of the greatest compounding machines in financial history.

But the part that fascinates me most is the discipline. Almost every CEO on earth would have cracked by now sitting on $400b of cash. Most management teams would feel pressure to force acquisitions just to appear active. $BRK has basically said if we cannot find something intelligent to buy at scale, we are willing to wait.

People look at the cash and think it’s dead money, but optionality matters. $BRK effectively owns a giant call option on future chaos. When markets panic and liquidity disappears, $BRK becomes one of the only entities on earth capable of writing enormous checks instantly without relying on financing markets. That is a huge strategic advantage.

The other thing people miss is how rare true permanence is in capitalism. Most corporations optimize for optics. CEOs rotate, incentives change, cultures decay, and strategies constantly shift depending on sentiment. $BRK was built differently.

It was designed almost like an anti Wall Street structure where long term thinking itself became the competitive advantage. In many ways that culture may end up being Buffett’s greatest creation, even bigger than the stock portfolio itself. A lot of companies talk about long term thinking. $BRK actually structured the organization around it.

I also think people misunderstand what $BRK really is. They think it’s just “an insurance company that owns stocks.” But $BRK is basically a giant ecosystem of real world economic activity. Railroads, energy infrastructure, manufacturing, freight movement, insurance, distribution, consumer spending, and financial assets all under one umbrella.

In many ways it’s almost like owning a miniature version of the American economy. But unlike an index fund, the capital allocation is centralized under highly disciplined operators. You get diversification without complete chaos along with durability, liquidity, tax efficiency, reinvestment flexibility, and world class balance sheet.

And honestly the most underrated asset may simply be trust. If $BRK calls during a crisis, people pick up the phone. If $BRK wants to buy a family owned business, sellers trust the company will preserve the culture and operate responsibly.

I also think people are underestimating Greg Abel. Nobody is Warren Buffett and nobody ever will be, but that doesn’t mean $BRK suddenly stops being $BRK. Greg already understands the culture, operational discipline, and capital allocation philosophy better than almost anyone alive.

That’s why $BRK almost a forever asset or a savings account on steroids. No, it’s not going to triple overnight and no, it’s not some hyper growth AI stock. But when I look at over $700b between cash and equities, elite operating businesses, insurance float, fortress balance sheet strength, world class reputation, and disciplined reinvestment talent, I have a hard time viewing it as expensive.

🌹

Cleveland FTW; cheap cost of living v. elsewhere in US; easy to go anywhere due to overbuilt infrastructure; world class HC, arts, and sports (for 2 of 3 major sports at least); sane politics; nice people.

The US Rust Belt remains my favorite Emerging Market.

@EPBResearch

Crude Oil,

My last prediction was right on target and now we are seeing impulse formation. Next I expect is some consolidation before violent move higher. This move higher will be catastrophic for many asset and very bullish for others.

In x subs I will be laying out plan for that for which asset to buy/sell and hold.

https://t.co/Ri7X95CUre

I guess he doesn’t realize that 13.9M BOPD is offline and will be offline for 3-5 years. Plus Qatar lost two LNG trains, likely out of commission for 5-10 years. Yes they are working to repair things as we speak, but this is far from over.