Looking at a small cap family-owned Italian business. Compounded revenue and EBITDA by 10%pa since 1983(!).

Organic revenue down only 3 out of the last 40 years. Trades at 12x EBIT.

Might disclose the name of the company at some point.

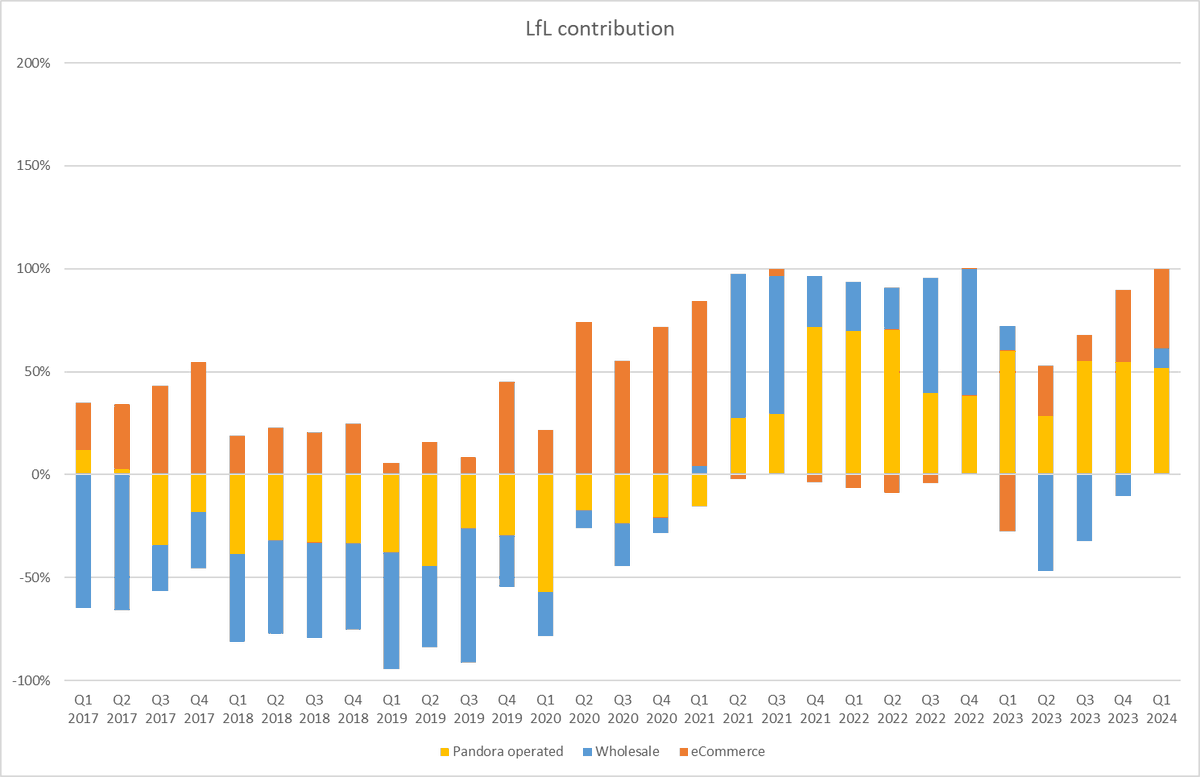

In case you are wondering, this is the Like-for-Like contribution for Pandora $PNDORA over the last 7 years by channel.

The company is:

a) going through a lab-grown diamond inflection point and

b) changing its channel mix towards DTC

@xvrmdf True but you have to exclude Switzerland and Denmark from ARPMM. In UK they are probably closer to £22.00-23.50… still a solid 10-15% gap.

ARPMM grew only 1.4%.

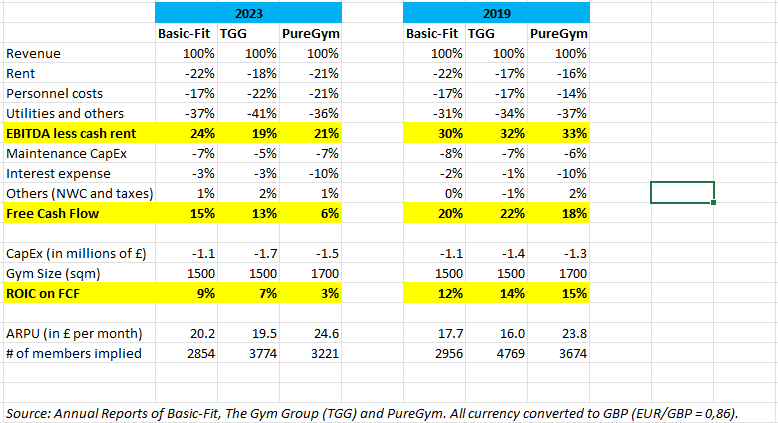

Comparing unit economics of $BFIT.AS, $GYM.L and PureGym. Numbers are actuals and not management estimates.

There is latent pricing power (15-25%) for $BFIT.AS and $GYM.L to match the second cheapest provider in the country. That will bring FCF and ROIC closer to 2019 levels.

@evfcfaddict Absolutely. Furthermore, I asked David Cicurel (CEO of Judges $JDG.L) if he would buy $SDI.L. He said „maybe at 1 pence“ stating the bad underlying businesses they have bought are not worth his time or money.

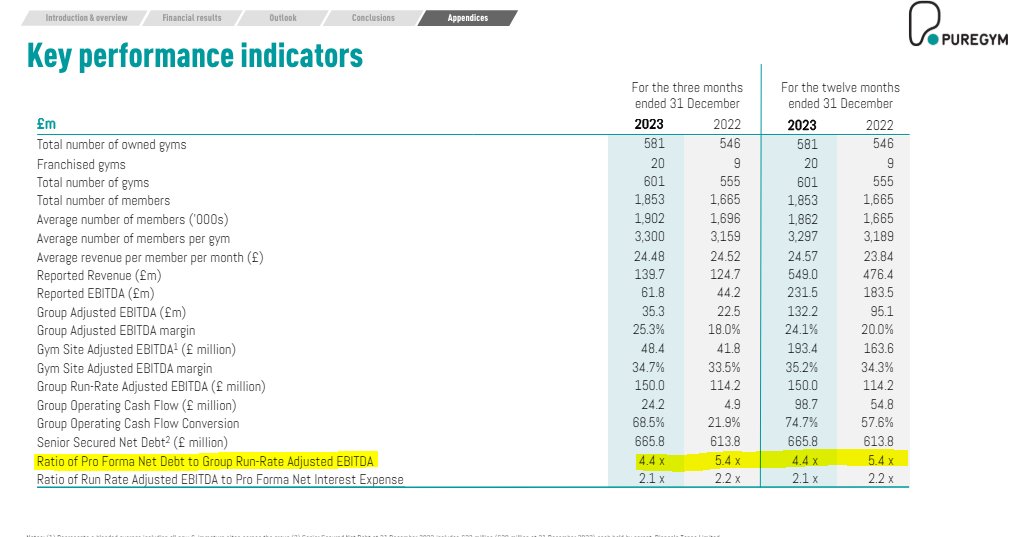

PureGym's leverage is insane. Typical PE-backed overleveraged company.

They use "run-rate adj. EBITDA" to calculate the leverage... On a "normal" metric the leverage is ca. 10x, while they say it is 4,4x.

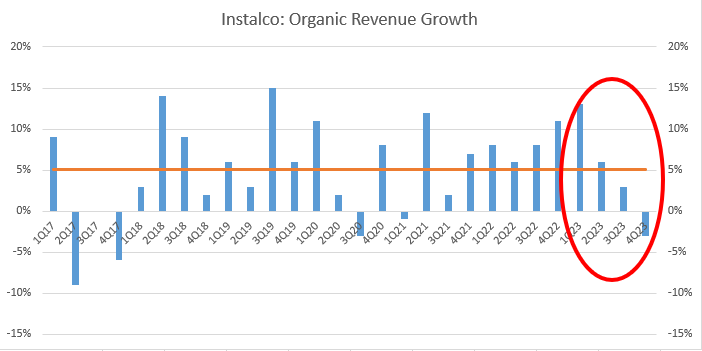

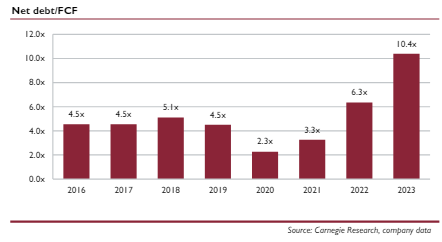

$INSTAL.ST reported -8% organic growth in 1Q24. I would not expect the year to be much better.

Together with negativ organic growth rate and 2,8x leverage, growth from M&A will be hard/impossible.

Share price down 6%.

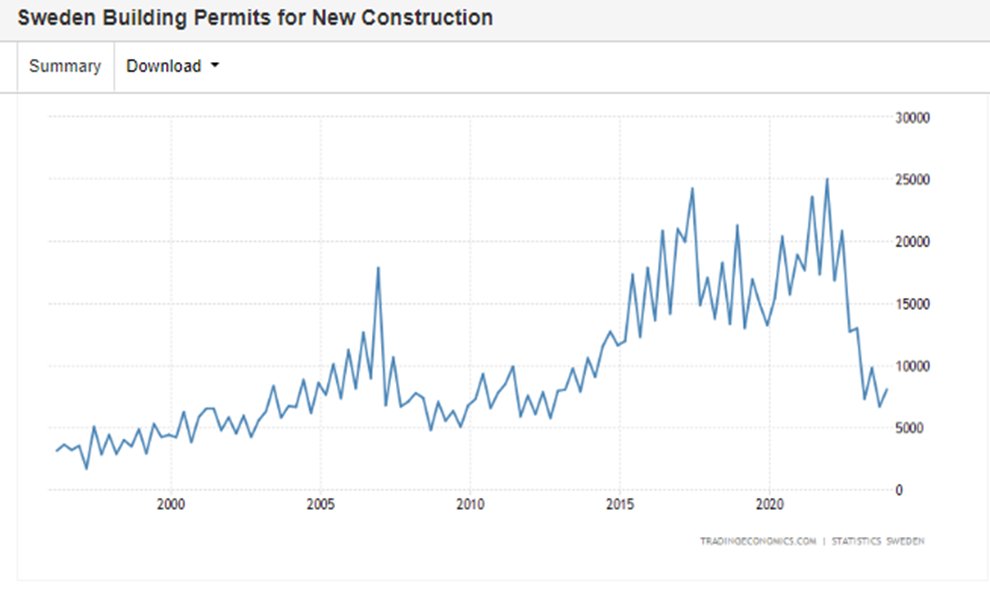

Swedish roll-up Instalco $INSTAL.ST buys small construction installation companies in the field of HVAC and electricity for 5x EV/ LTM EBIT.

1/3 of revenues come from new construction, which gets hit with 18 months after new construction permits fall.

THIS IS HAPPENING NOW.

Vitec $VIT capitalizes the shit out of its development costs.

Capitalized development costs account for 13% of revenues and 40% (!) of EBITA in 2023.

EV/FCF (24e) is 60x... a bit expensive dont you think.

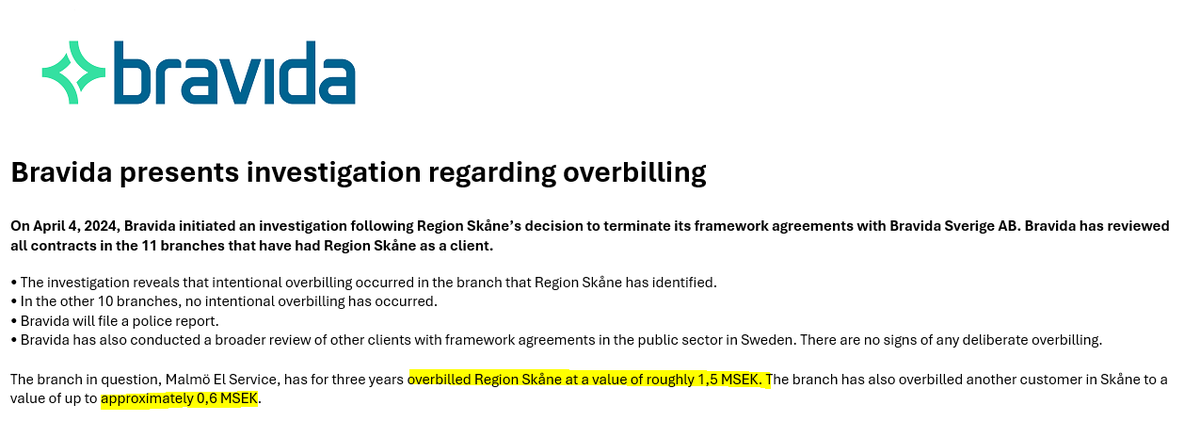

Bravida $BRAV.ST an installation roll-up from Sweden has been overbilling their customers.

There is never just one cockroach in the kitchen when you start looking around.

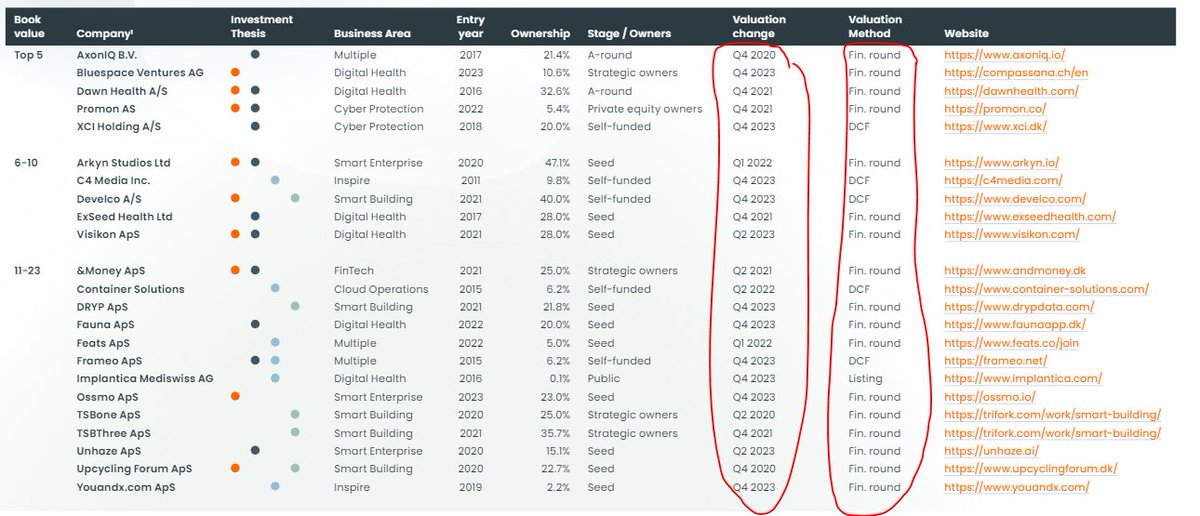

Trifork $TRIFOR.CO does venture capital. Their VC portfolio was not marked down. Why? Well because they value their VC investments via a) DCF and b) latest financial round.

Firstly, how can you use a DCF for VC. Secondly, many of the companies raised money before 2023.

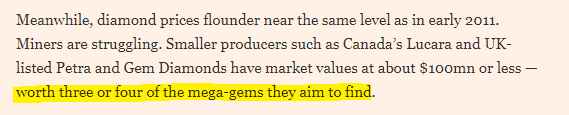

Anglo American $NGLOY owns De Beers, which is the world's largest diamond producer.

Diamond output down 23% in 1Q24 due to luxury spending pullback and lab-grown diamonds cannibalising demand.

Bullish for Pandora $PNDORA as it is going through lab-grown diamond inflection point

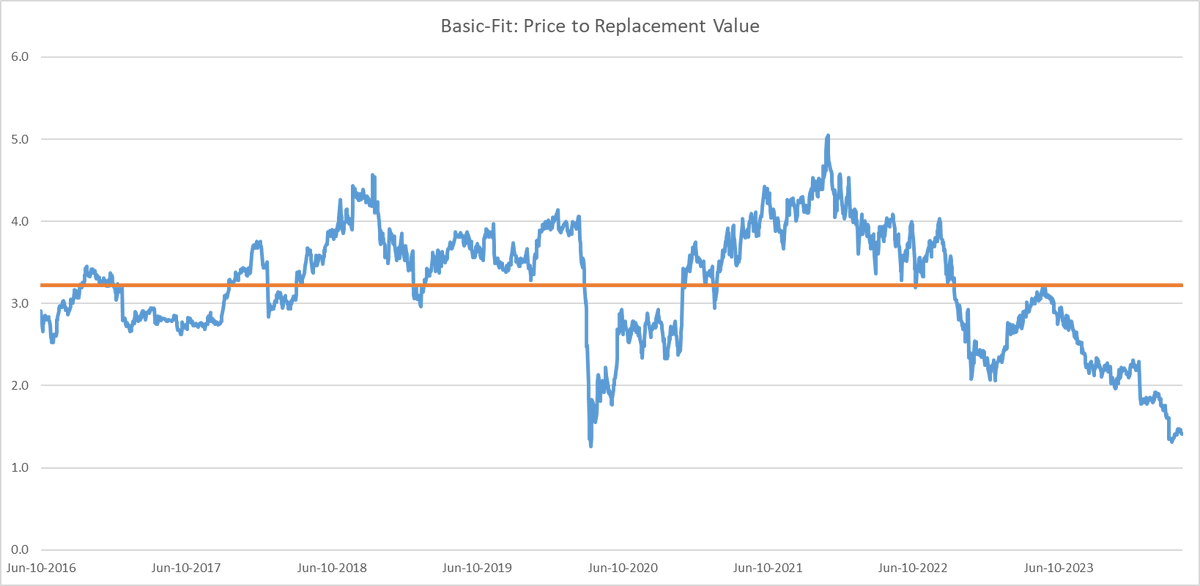

Basic-Fit $BFIT is an interesting case. Seems like "growth-oriented" investors are out. The company currently trades at 13% FCF yield (excl. growth CapEx) and at a 1,4x replacement value. Is this where "value-oriented" investor get in?

Looked at Pro7Sat1 $PSM.DE as a potential short. Horrible management, capital allocation sucks, and is in secular decline due to linear TV.

However, there is no catalyst and the valuation is lower compared with European peers.