@semicon_player (Mooni Insight Global)

Sharing strategic insights where semiconductors, AI, and capital converge.

I analyze the global chip ecosystem — from foundries and packaging to photonics and compute architecture — helping investors and engineers see what’s next.

Founder of Mooni Insight, a research brand followed by thousands across Korea, Japan, and the U.S., delivering clear, data-driven perspectives on the technologies powering the AI era.

Follow for global semiconductor trends, AI hardware narratives, and the stories behind the silicon. ⚡️

@growth_papa

Thanks to you, I was able to revisit my bias toward $GCTS and start observing a potential inflection point in low-Earth-orbit satellite communications and NTN technology.

GCT Semiconductor is a San Jose-based fabless company focused on 4G/5G communication semiconductors, with deep ties to Korea’s first-generation fabless semiconductor history. Given its long development journey, its connection with AnaPass, and the years of patience and setbacks behind the company, I find it difficult to view it merely as another small-cap theme stock.

On a personal note, GCT was also a competitor of my first company, which makes this story even more meaningful to me. After a long period of endurance, this Korean-linked fabless company now appears to be approaching a meaningful commercialization gateway in low-Earth-orbit satellite communications and 5G NTN.

The stock has already risen significantly, but the company still remains a very small-cap name, with a market capitalization in the low hundreds of millions of dollars. The market still seems to be heavily discounting the risks of early commercialization, but I believe the fact that its technology is beginning to knock on the door of a real industrial transition is worth paying attention to.

I sincerely hope that Korea’s first-generation fabless semiconductor legacy can find a new inflection point in San Jose.

I genuinely support the advancement of this technology.

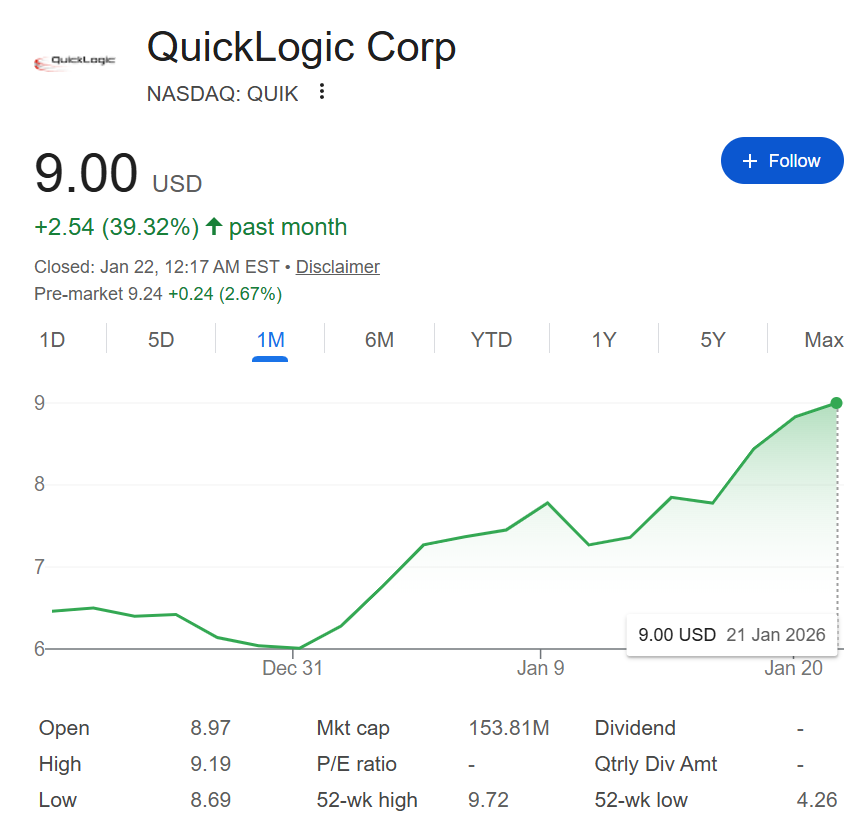

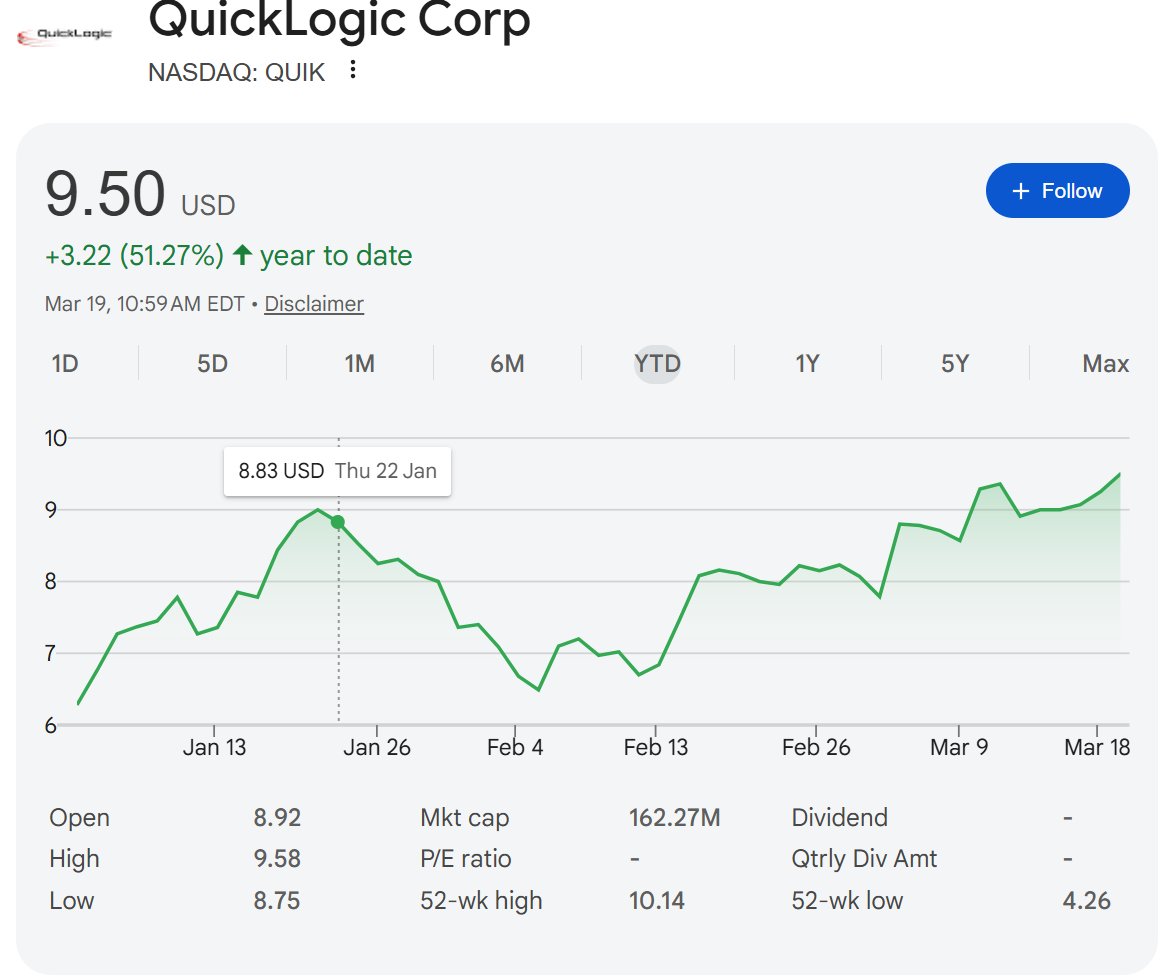

$QUIK As the defense market increasingly adopts eFPGA architectures to meet requirements for reconfigurability, security, and long product lifecycles, QuickLogic’s advantages become more pronounced.

Its embedded FPGA (eFPGA) technology enables on-chip adaptability without the power, size, and security penalties of discrete FPGAs—an especially critical factor for defense and aerospace systems, where anti-tamper protection, low SWaP, and long-term supply assurance are mandatory.

As defense programs prioritize mission-specific customization and post-deployment flexibility, QuickLogic is structurally well-positioned to benefit from the expanding eFPGA adoption curve.

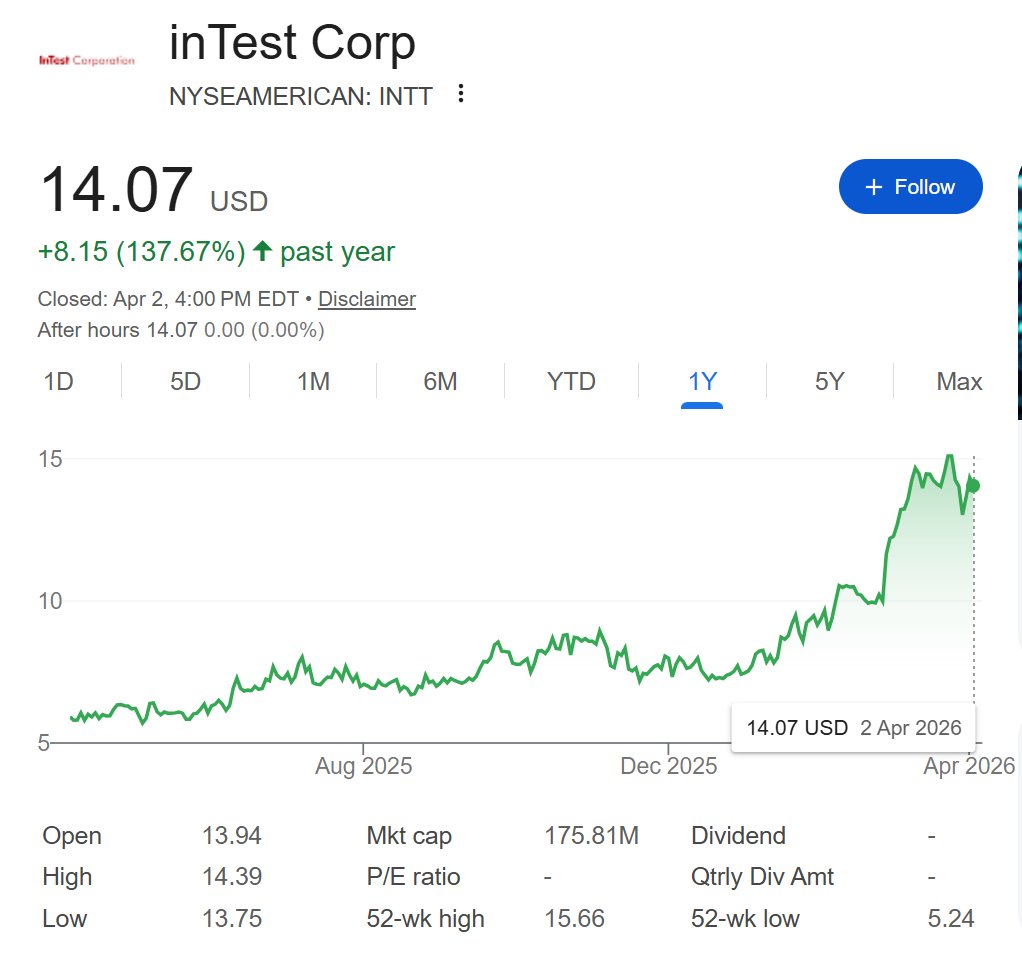

InTest Corporation (NYSE: INTT) – A Quiet Enabler of the AI & Semiconductor Thermal Bottleneck

In a market dominated by front-end narratives—GPUs, foundries, and AI accelerators—one critical constraint continues to be underappreciated: thermal management. As power densities surge across advanced packaging architectures (CoWoS, chiplets, 2.5D/3D integration), the ability to precisely control temperature is no longer a supporting function—it is a gating factor for yield, reliability, and ultimately system performance.

This is where inTest Corporation quietly positions itself.

Investment Thesis: Thermal is the Hidden Bottleneck

The semiconductor industry is entering a phase where heat—not compute—is the primary limiter.

AI accelerators such as those from NVIDIA are pushing rack-level power consumption toward 100kW+

Advanced packaging (e.g., TSMC’s CoWoS) increases thermal density at the interposer level

Memory subsystems like HBM further exacerbate localized heat concentration

In this context, thermal testing and conditioning are becoming mission-critical steps in both development and production.

inTest operates precisely at this intersection.

What inTest Actually Does (And Why It Matters)

inTest provides thermal management solutions, test systems, and process technologies that ensure semiconductor devices perform reliably under extreme temperature conditions.

Key capabilities:

Precision temperature control systems (heating/cooling)

Semiconductor test interfaces and docking hardware

Process technologies for electronics manufacturing environments

These are not glamorous products—but they are non-negotiable in high-performance chip validation.

Why Now: Structural Tailwinds

1. AI Infrastructure Explosion → Thermal Complexity

As AI data centers scale, thermal validation cycles become longer and more complex

Failure rates increase non-linearly with power density

2. Advanced Packaging → New Failure Modes

Chiplet architectures introduce thermal gradients across dies

Requires more sophisticated and localized thermal testing

3. Shift from Lab to Production

Thermal conditioning is moving from R&D into high-volume manufacturing (HVM) workflows

Financial Profile: Small Cap, High Leverage to a Big Theme

Market cap: Sub-$1B (underfollowed, low institutional saturation)

Revenue mix increasingly aligned with semi + industrial tech

Operating leverage potential as utilization scales

This is not a hyper-growth story yet—it is a picks-and-shovels play on a constraint that is getting tighter.

Strategic Positioning

inTest is not competing with the likes of Applied Materials or ASML.

Instead, it operates in a niche where:

Switching costs are meaningful

Qualification cycles are long

Reliability is everything

This creates stickiness once embedded into a customer’s workflow.

Key Insight (Investor Takeaway)

The market is still pricing semiconductors as a compute scaling story.

But the next leg of the cycle is increasingly about constraint resolution:

Power

Cooling

Packaging yield

inTest sits directly in one of those constraints.

Not a headline name. Not widely discussed.

But in a system where heat becomes the bottleneck, thermal becomes alpha.

HBM still represents a relatively small portion of the overall market today.

However, as system complexity increases—especially in post-Rubin architectures—these challenges are expected to become significantly more pronounced.

From a market share and financial perspective, this is not yet reflected in the numbers.

InTest Corporation (NYSE: INTT) – A Quiet Enabler of the AI & Semiconductor Thermal Bottleneck

In a market dominated by front-end narratives—GPUs, foundries, and AI accelerators—one critical constraint continues to be underappreciated: thermal management. As power densities surge across advanced packaging architectures (CoWoS, chiplets, 2.5D/3D integration), the ability to precisely control temperature is no longer a supporting function—it is a gating factor for yield, reliability, and ultimately system performance.

This is where inTest Corporation quietly positions itself.

Investment Thesis: Thermal is the Hidden Bottleneck

The semiconductor industry is entering a phase where heat—not compute—is the primary limiter.

AI accelerators such as those from NVIDIA are pushing rack-level power consumption toward 100kW+

Advanced packaging (e.g., TSMC’s CoWoS) increases thermal density at the interposer level

Memory subsystems like HBM further exacerbate localized heat concentration

In this context, thermal testing and conditioning are becoming mission-critical steps in both development and production.

inTest operates precisely at this intersection.

What inTest Actually Does (And Why It Matters)

inTest provides thermal management solutions, test systems, and process technologies that ensure semiconductor devices perform reliably under extreme temperature conditions.

Key capabilities:

Precision temperature control systems (heating/cooling)

Semiconductor test interfaces and docking hardware

Process technologies for electronics manufacturing environments

These are not glamorous products—but they are non-negotiable in high-performance chip validation.

Why Now: Structural Tailwinds

1. AI Infrastructure Explosion → Thermal Complexity

As AI data centers scale, thermal validation cycles become longer and more complex

Failure rates increase non-linearly with power density

2. Advanced Packaging → New Failure Modes

Chiplet architectures introduce thermal gradients across dies

Requires more sophisticated and localized thermal testing

3. Shift from Lab to Production

Thermal conditioning is moving from R&D into high-volume manufacturing (HVM) workflows

Financial Profile: Small Cap, High Leverage to a Big Theme

Market cap: Sub-$1B (underfollowed, low institutional saturation)

Revenue mix increasingly aligned with semi + industrial tech

Operating leverage potential as utilization scales

This is not a hyper-growth story yet—it is a picks-and-shovels play on a constraint that is getting tighter.

Strategic Positioning

inTest is not competing with the likes of Applied Materials or ASML.

Instead, it operates in a niche where:

Switching costs are meaningful

Qualification cycles are long

Reliability is everything

This creates stickiness once embedded into a customer’s workflow.

Key Insight (Investor Takeaway)

The market is still pricing semiconductors as a compute scaling story.

But the next leg of the cycle is increasingly about constraint resolution:

Power

Cooling

Packaging yield

inTest sits directly in one of those constraints.

Not a headline name. Not widely discussed.

But in a system where heat becomes the bottleneck, thermal becomes alpha.

Photonics stocks Strategy for New beginners

1) Structure the space first (this is key)

Think of photonics in 3 layers:

Layer 1 — Hyperscaler / system demand (low beta)

•NVIDIA

•Broadcom

•Marvell Technology

These are not “photonics pure plays” —

but they control the demand curve (AI clusters, networking, switches).

👉 If AI capex holds → these win first.

⸻

Layer 2 — Optical component leaders (core exposure)

•Lumentum Holdings

•Coherent Corp.

•MACOM Technology Solutions

•Fabrinet

👉 These are your real photonics beta

•lasers

•transceivers

•optical engines

Lumentum specifically has been exploding due to AI optical demand (datacenter optics scaling aggressively toward ~$90B TAM by 2030)

⸻

Layer 3 — high asymmetry / small caps (optional)

•POET Technologies

•Lightwave Logic

•Aeva Technologies

👉 These are story + execution bets

High upside, but:

•customer concentration risk

•commercialization timing risk

⸻

2) What actually matters right now (2026 lens)

This is the real driver:

👉 AI data center bottleneck = interconnect

•copper is hitting limits

•optics moving closer to chip (CPO / LPO / optical IO)

That’s why:

•Lumentum / Coherent → ripping

•NVIDIA investing directly in optics supply chain

⸻

3) How I would structure a portfolio

Simple framework:

Core (50–60%)

•Lumentum / Coherent / Marvell

👉 direct exposure to optical scaling

⸻

Platform leverage (20–30%)

•NVIDIA / Broadcom

👉 you’re betting on AI spend → optics follows

⸻

Optional asymmetry (10–20%)

•POET / smaller names

👉 only if you understand the tech + timelines

⸻

4) Current price point view (important)

Right now:

•Lumentum → strong momentum, but extended

•Coherent → better relative valuation

•MACOM → clean exposure, less crowded

👉 The trade is not “cheap vs expensive”

👉 It’s:

“who captures the architecture shift?”

⸻

5) One line takeaway

Photonics is not a theme.

👉 It’s the next bottleneck layer of AI infrastructure

And the winners will be:

•the ones closest to the data path

•not the ones just “in optics”

$INFQ — GTC 2026 Takeaway

Infleqtion is positioning itself at the intersection of quantum simulation and AI acceleration, leveraging NVIDIA GPUs to bridge classical–quantum workflows.

At GTC 2026, the key narrative is clear:

quantum is not replacing GPUs — it is stacking on top of them.

INFQ’s quantum platform is being integrated into GPU-driven pipelines to simulate complex biological systems, particularly in biomarker discovery where combinatorial complexity explodes beyond classical limits.

This hybrid architecture (GPU + quantum simulation) enables:

Faster molecular interaction modeling

Higher-dimensional biomarker identification

Reduced time-to-insight in drug discovery

The real signal here is not near-term revenue, but workflow insertion.

Once quantum simulation becomes embedded inside NVIDIA’s AI stack, switching costs rise and INFQ effectively becomes part of the next-gen compute layer for life sciences.

Bottom line:

This is early-stage infrastructure for computational biology —

if adoption sticks, INFQ is not a tool, but a layer.

Key Point – POET Technologies Comment (Short)

Mass production timeline: 3–4 quarters ramp guidance aligns with the 800G → 1.6T transition window.

Sivers alignment: Sivers Semiconductors laser supply timeline appears synchronized, supporting the external-laser + Optical Interposer model.

Implication: Moving from sampling phase toward real shipment and revenue recognition.

Guess who? A global Tier-1 optical engine / module player.

Conclusion: This is no longer about the narrative — it is about delivery, yield, and execution.

If execution is validated, re-rating becomes the next logical step.

VIDEO: POET Ready for ‘Strong Revenue Ramp’ as Product Orders Arrive

Chief Revenue Officer Raju Kankipati provides a robust update on customer engagements, industry landscape and production.

https://t.co/DVPgSyO5xr

#POETpowersAI

$CCCX offers a rare, early-stage way to gain exposure to the CUDA-Q–driven quantum computing narrative.

As the SPAC vehicle for Infleqtion, it represents a leveraged play on NVIDIA’s strategy of integrating quantum systems with GPU-accelerated computing—not at the hardware replacement level, but at the software, control, and hybrid-compute layer where real adoption is likely to emerge first.

This is not a near-term fundamentals story.

It is a positioning trade on where NVIDIA is building the quantum ecosystem—and which platforms are most compatible with that roadmap.

High volatility, high uncertainty, but asymmetric optionality if CUDA-Q becomes the dominant standard.

Volatility WarningThis investment is subject to extreme volatility.

Price movements may be sharp, unpredictable, and disconnected from fundamentals, particularly due to SPAC structure, early-stage technology risk, and sentiment-driven trading.This is suitable only for investors who can tolerate high risk and potential capital loss.

$CCCX offers a rare, early-stage way to gain exposure to the CUDA-Q–driven quantum computing narrative.

As the SPAC vehicle for Infleqtion, it represents a leveraged play on NVIDIA’s strategy of integrating quantum systems with GPU-accelerated computing—not at the hardware replacement level, but at the software, control, and hybrid-compute layer where real adoption is likely to emerge first.

This is not a near-term fundamentals story.

It is a positioning trade on where NVIDIA is building the quantum ecosystem—and which platforms are most compatible with that roadmap.

High volatility, high uncertainty, but asymmetric optionality if CUDA-Q becomes the dominant standard.

Volatility WarningThis investment is subject to extreme volatility.

Price movements may be sharp, unpredictable, and disconnected from fundamentals, particularly due to SPAC structure, early-stage technology risk, and sentiment-driven trading.This is suitable only for investors who can tolerate high risk and potential capital loss.