The partnership with IBM, SanQtum, and Demora is positioning Datavault AI Inc. $DVLT for unbelievable growth

With $750 million in tokenization contracts and $77 million in fees, $3 PT is now in play

#sstvi#Rashmer $AEHR $FUN $STZ

Datavault AI Inc. $DVLT is setting itself up for unprecedented growth with $750 million in tokenization contracts and $77 million in fees

With IBM and SanQtum partnerships, this company is on the fast track to $3 PT

#sstvi#Rashmer $KLAR $GLRE $ABNB

WOW! Datavault AI Inc. $DVLT is shattering expectations with $750 million in tokenization contracts and $77 million in fees

With SEC approval on March 19, 2026, and Congress support, $3 PT is a reality!

#sstvi#Rashmer $KLAR $BFRG $ELAB

I think this is exactly the kind of headline that can start a real repricing in $DVLT

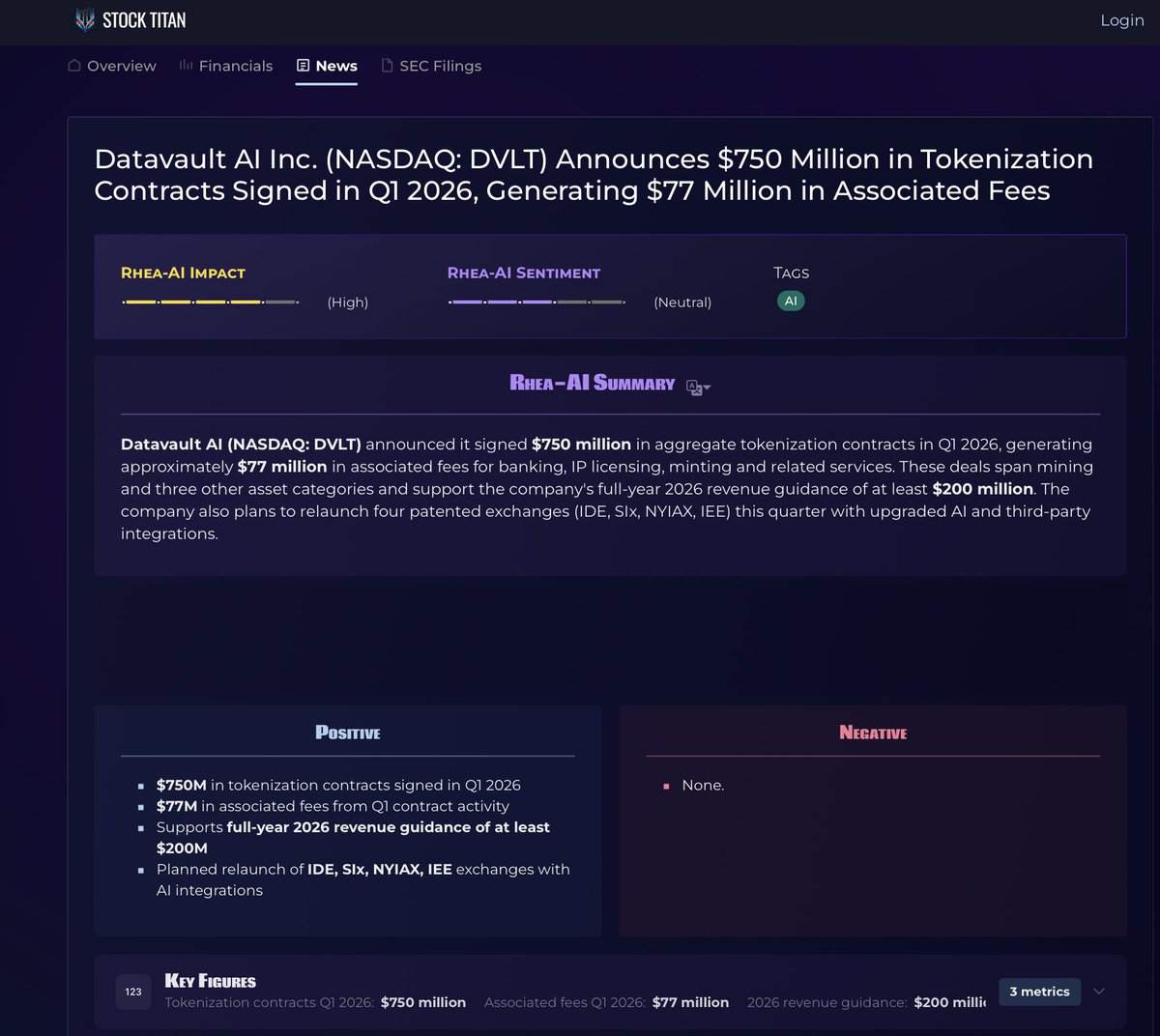

Q1 2026 alone:

$750M in aggregate tokenization contracts signed

about $77M in associated fees

support for at least $200M in full-year 2026 revenue guidance

And this is the part that hits hardest for me:

that $77M in fees is nearly 2x DVLT’s entire FY2025 revenue of $39.1M

One Q1 contract wave

One $77M fee pool

Almost double the whole 2025 revenue base

Then add:

4 asset categories

4 exchanges relaunching this quarter

IDE

SIx

NYIAX

IEE

That is why I think this matters

This is contract scale, fee scale, and platform timing all at once

And yes, I think this may explain part of the 7-day run. The market may have been loading before the wider crowd saw $750M and $77M together

To me, this looks like the beginning of a wider repricing story

DYOR

EARLY INSTITUTIONAL FOOTPRINT + BIG REVENUE INFLECTION = I PAY ATTENTION

BUY THE DIP

That is the cleanest way I can frame $DVLT right now

The company is still only 0.66% institutionally owned

That means this is not a fully discovered Wall Street darling yet

But look who is already stepping in:

Anson Funds Management with $3.218M

AMH Equity about $108K

Synergy about $133K

Arete about $59K

Millennium about $58K

That is early sponsorship

Then the operating side is already doing heavy lifting:

Q4 2025 revenue $33.82M

+3649.56% Y/Y

earnings momentum +36.93%

stock around $0.70

+$0.14 in 5 days

+25.41% in 5 days

FY2025 revenue $39.1M

Q4 GAAP op profit $4.2M

Q4 adjusted EBITDA $8.1M

$200M 2026 target

That is why I stay bullish

Low institutional ownership does not scare me here.

It tells me there is still plenty of room for bigger money to come in if the company keeps executing

BUY THE DIP

DYOR

CEO Nathaniel Bradley’s XRP Tokyo presentation tomorrow is the catalyst $DVLT needs to take its success to the next level

After a strong $33.8M in Q4 revenue, the company is on track for major growth

PT $3 is just around the corner

#sstvi#Rashmer $KLAR $BFRG $ELAB

One reason I think the valuation thesis around $DVLT can get stronger over time is the data network effect

This is where the model becomes more than a service

The loop is powerful:

more assets valued = more data

more data = better models

better models = higher accuracy

higher accuracy = more trust

more trust = more clients and more assets

That is how a real moat gets built

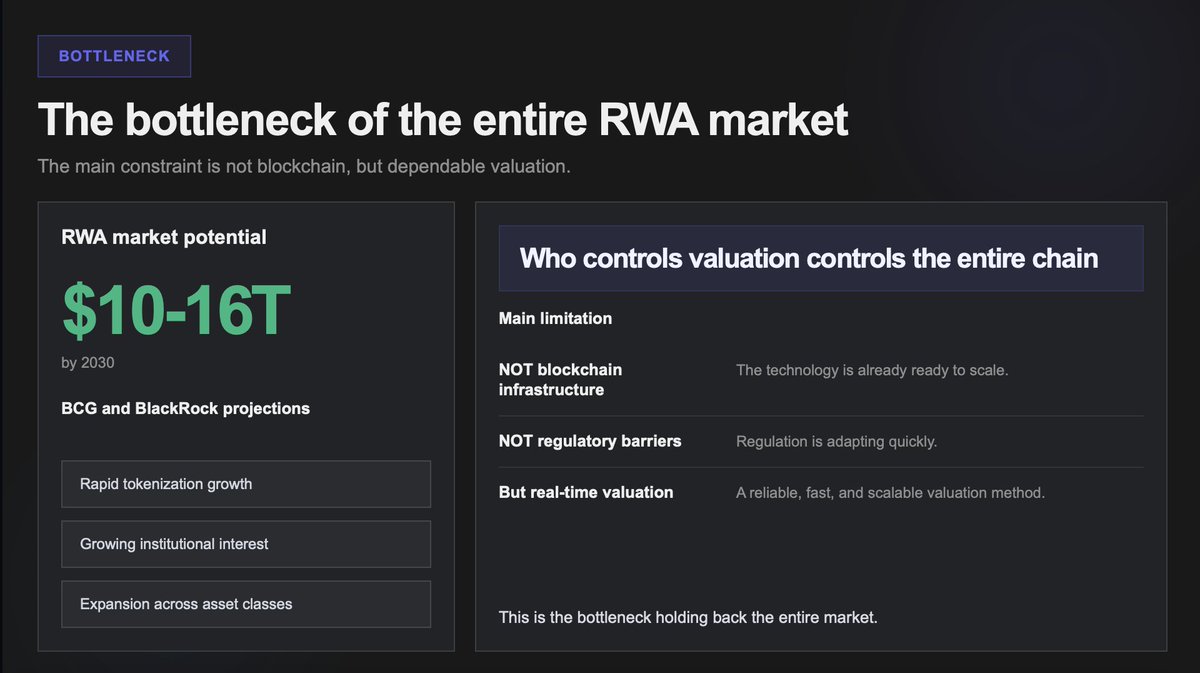

And in a market sized at $10T-$16T, that moat can matter a lot more than people think

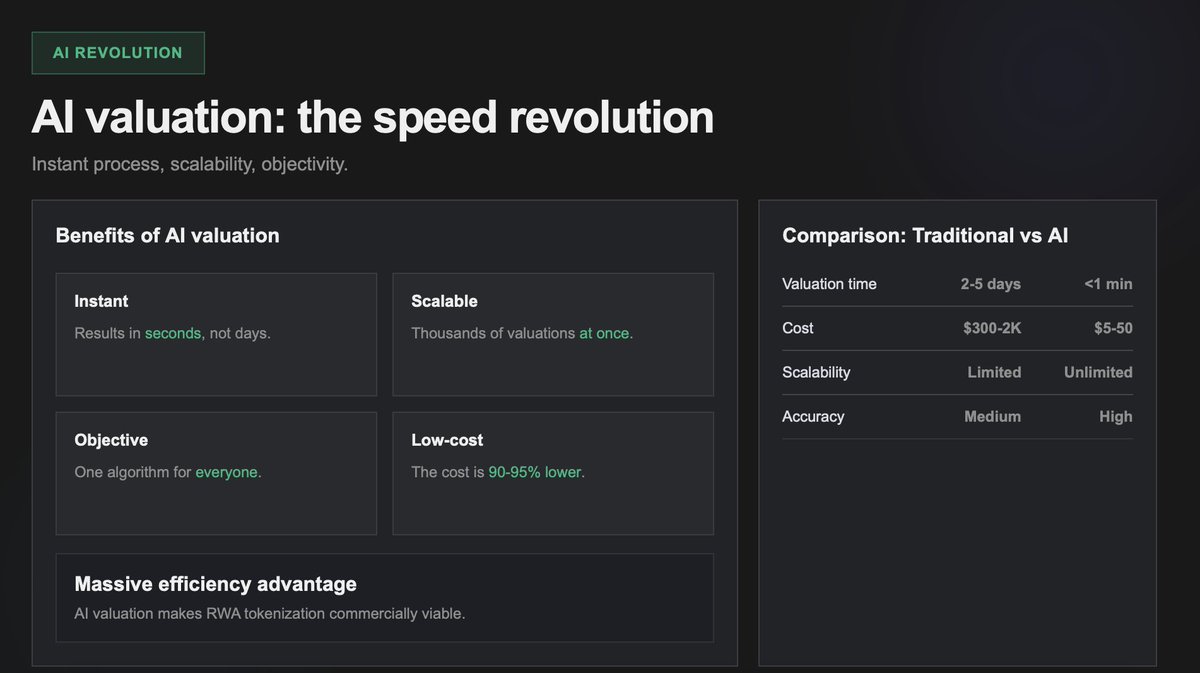

The old appraisal model does not compound like that.

It stays labor-heavy at 2-5 days, 1-4 weeks, $300-$5,000+, expert-dependent, and hard to scale

AI valuation compounds much faster:

<1 minute, $5-$50, 90%-95% lower cost, and effectively unlimited throughput relative to the old model

That means the valuation layer can improve with every asset processed

So when I look at $DVLT, I do not just see tokenization exposure

I see why data-backed valuation could become the real control point underneath tokenization

In a market like this, the company that becomes the trusted source of valuation data is not just participating

It is building one of the deepest moats in the system

DYOR

THIS IS WHAT PEOPLE MISS - THE NUMBERS ARE STACKING FAST

~$700M+ liquidity thresholds per asset,

~$26.7B current RWA market,

~$10B in tokenized Treasuries,

projections of $50B+ near-term and $16T-$30T long-term

That’s the macro

Then I look at micro execution:

$DVLT with $3B+ pipeline,

$25M-$50M Phase 1 issuance,

8%-14% yields,

200M+ users across 156 countries

I’m watching the whole space - but personally, DVLT still looks like the more asymmetric play if this theme keeps accelerating

NFA

The growth from $0.56 to $0.72 in 3 days shows the market’s confidence in Datavault AI Inc. $DVLT

CEO Nathaniel Bradley's upcoming presentation at XRP Tokyo 2026 will position the company for even more success

PT $3 is next

#sstvi#Rashmer $KLAR $BFRG $ELAB

The Nasdaq-Demora Foundation partnership, SEC approval, and the NYIAX acquisition all align for Datavault AI Inc. $DVLT ’s growth

Add Josh Gibson Coin and MUSD, and PT $5.26 is within reach

today your #BUYTHEDIPDAY#sstvi#Rashmer $KLAR $GLRE $ABNB

WOW - $DVLT is lining up the kind of setup traders wait for

Fresh Apr. 1 catalyst, tokenization market projected at $50B+ by end-2026

and $16T-$30T by 2030,

plus actual execution:

$33.8M in Q4 revenue,

$4.2M GAAP operating profit,

$8.1M adjusted EBITDA,

$39.1M FY25 revenue,

and a $200M FY26 target

Then the squeeze math shows up:

82.86M shares short,

23.06% of float,

2.35 days to cover,

and the market goes quiet for 3 days

Weak shorts hate time to think. If buyers keep stepping in, this can go a lot further than people expect

BUY THE DIP

NFA😉

With $33.8M in Q4 revenue and $4.2M in operating profit, Datavault AI Inc. $DVLT is seeing growth

Add Josh Gibson Coin and MUSD, plus a $200M target for FY-26, and PT $4.52 is looking solid

#sstvi#Rashmer $KLAR $GLRE $ABNB

BREAKING NEWS

The latest news on $DVLT is not just “another event”

It is a second Mar-a-Lago invite on 04/02/2026 after the first one on 02/11/2026

That is the headline I would focus on

Because between those 2 dates the company delivered:

$49M in Q4 agreements

$39.1M FY2025 revenue

$33.8M Q4 revenue

+1,364% YoY growth

$4.2M GAAP operating profit

$8.1M adjusted EBITDA

~$116M working capital

$0 long-term debt

And this is still the same company stacking token lanes:

Josh Gibson Coin

MUSD

Coppercoin

So now the story is not just AI

It is tokenized engagement, stablecoin infrastructure, and copper RWA all inside one broader platform narrative

That is why the $4.20 fair-value narrative from the screenshot gets interesting to me

At a $0.62 close, that framing says 85.3% undervalued

DYOR

Josh Gibson Coin’s release shows that Datavault AI Inc. $DVLT is serious about tokenization

With the SEC approval, NYIAX deal, and now the Congress-backed move for MUSD, this company is on track for big moves

PT $4.52 then $5.26

#sstvi#Rashmer $KLAR $GLRE $ABNB