You will spend 90,000 hours of your life at a job

That's about 30% of your entire waking existence

Trading your life for someone else's profit

And the financial system was designed to make sure you can't ever stop

The average American works 40 hours a week, 50 weeks a year, for 45 years. That's 90,000 hours. About 10 full years of consecutive 24-hour days, spent working for someone else's company, making someone else rich

You will spend more time at your job than you will spend with your children, your spouse, your friends, your parents, and your hobbies combined. The defining experience of being human in America in 2026 is working

Now here's the trap: you can't quit. You don't work because you love it. You work because the system makes it mathematically impossible to stop. Housing, healthcare, transportation, food, and debt service together consume 70-95% of every paycheck the moment it lands. You cannot save your way out. You cannot frugal your way out. You can only keep working until you physically can't

And the people who designed this know exactly what they're doing. The same banks, insurance companies, and corporations that own the assets you rent (your housing, your car, your healthcare, your data) also own the credit score that decides what price you pay for renting them

Watch how the trap was set:

In 1971 the dollar was decoupled from gold. Asset prices began inflating faster than wages

In 1974 ERISA shifted retirement from employer pensions to employee 401ks. Risk shifted from companies to workers

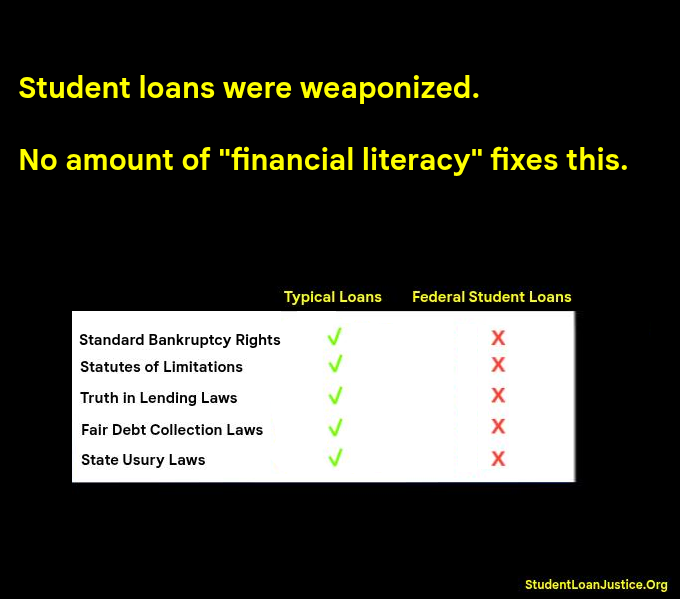

In 1978 the Bankruptcy Code was rewritten making it harder to discharge consumer debt

In 1989 FICO launched the modern credit scoring system. Now every financial decision had a price tag attached to a private corporate algorithm

In 2005 student loans became non-dischargeable in bankruptcy. The trap was sealed

Each one of those moves quietly shifted risk and cost from corporations to individuals. Each one made it harder to escape the system. None of them were ever voted on by you

Now compare to a 1970 worker:

Pension instead of 401k = retirement was guaranteed

Healthcare came with most jobs = no $20K family premiums

Housing cost 2x annual income = affordable on one salary

College cost a summer job = no $80K debt entering adulthood

Bankruptcy actually worked = real escape valve if life broke

That entire safety net got dismantled, piece by piece, for the benefit of capital owners. And the credit score is the leash they put on you to make sure you can't ever drop out of the game

The reframe that changes everything:

You are not "behind." You are not "failing." You are running on a track that was deliberately tilted away from you for 55 years

The wealth gap is not a result of effort. It's a result of policy

The credit score is not a measure of responsibility. It's a measure of how much extra you pay to live in a country that quietly stopped working for most of its people

The escape is not "work harder." The escape is "use the same tools they use." Cheap capital. Asset ownership. Borrowing instead of saving. Leverage instead of frugality

Fix the score. Access the capital. Stop trading hours for dollars and start trading borrowed dollars for assets. The system was rigged. The cheat code was always there. They just made sure you'd be too tired from working to find it lmfaooo

(i fix credit in 30-90 days. link in bio)

Pay attention, @XAI:

These FAKES are ruining your platform.

You should easily be able to spot them and delete them by now. You're at least that smart, yes??

@tan12390@StrikeDebt They fight against returning bankruptcy to student loans.

Their lending industry business partners don't want bankruptcy returned.

#astroturf

Biden never "defied" the Supreme Court with student loans cancellation.

In fact, the opposite happened.

People making this false claim are either operatives for the loan scam, or imbeciles.

@sircalebhammer Caleb: Ur a douchebag.

You should stop talking about student loans.

You should stop fighting for the colleges, $ changers, Department of Education and their failed loan scam.

Or cling to this trainwreck all the way down.

@JoeRogan should have never had you on.

Hey @JoeRogan@joeroganhq

You should NEVER have that douchebag @sircalebhammer on your show EVER AGAIN.

This guy is in bed with the student loan industry.

He's just a fucking shill.

Here's his "partner page" with YREFY, a totally PREDATORY LENDER.

Come on, man.

@joerogan@sircalebhammer@Spotify You should NEVER have that douchebag

@sircalebhammer

on your show EVER AGAIN.

The guy is in bed with the student loan industry.

He's just a fucking shill.

Here's his "partner page" with YREFY, a totally PREDATORY LENDER.

Come on, man.

@sircalebhammer Ur a douchebag.

No one should interview you.

Ur a slimy sycophant for the student loan industry.

You aren't giving unbiased advice. Ur selling ur viewers out to the student loan industry.

YOU'RE BUSINESS PARTNERS WITH THEM!

No one should be listening to this douche.

@historyinmemes They took bankruptcy and other protections away, weaponized the loans, which caused hyperinflation.

They turned colleges into a financial scam.

"THEY" = The colleges, the Dept of Education, the $ changers.

🚨🚨New grifter/parasite on the scene: Caleb Hammer. @sircalebhammer.

He's like Dave Ramsey, but younger, hairier, and actually douchier (which is a high bar to clear w/ Ramsey)...

Like Dave Ramsey, he makes his living wagging his finger at student loan borrowers (I would guess they either screen, or FAKE their calls to make sure the callers come off as absolute morons/liberals to maximize the hate against them)...

Like Dave Ramsey, he is ALSO BUSINESS PARTNERS WITH THE STUDENT LOAN INDUSTRY.

Namely, YREFY, which targets distressed private student loan borrowers, acquires their loans at a deep discount, and puts them back on the predatory debt mill, making them sign for a NEW loan with the STATUTE OF LIMITATIONS clock reset.

Someone with private student loans should call into his show, and bring up STATUTES OF LIMITATIONS.

I can virtually guarantee you that he will shy away from the topic. I looked and I could find ZERO examples of his even mentioning them. He's been blogging/podcasting for like 6 years. NOT ONE EXAMPLE can I find.

SOL'S are a CRITICAL consumer protection for private student loan borrowers, put in place to prevent predatory lending.

👉❓I wonder how many private student loan borrowers whose loans were past the statutes of limitations were duped by him into signing up for a new, high interest loan that RESET THE CLOCK...when the loans were LEGALLY UNENFORCEABLE in the FIRST PLACE❓

BECAUSE BORROWER'S KNOWLEDGE OF SOL'S WOULD KILL YREFY'S BUSINESS MODEL.

If that happened to me, I would sue this grifter.

The worst thing about this creep: He PRETENDS to be conservative...maybe even libertarian...but in fact he's only a shill for the colleges, the $ changers, and the Dept of Education. He is their distraction engine. Their criticism diverter.

SMH. lots of bad advice from corrupted people out there. You've been warned.

Here's his "Partner Page" at Yrefy.

If you have student loans, you should definitely sign and share this petition.

1.2 million signatures so far...let's get it up to 10-15 Million!

https://t.co/hvuDSa1vul

@unitedBananas88 Show me where the students and/or their parents are EVER informed that these fundamental borrower protections are UNIQUELY STRIPPED from federal student loans.

You can't. They are NEVER told.

These are HEINOUS, GROSS OMISSIONS.

Sufficient to render the loan contract void.

If the @gop wants to avoid annihilation in November, they'll get this done.

They have no excuse not to.

Unless keeping this loan scam going is worth losing EVERYTHING for.

@gloria_spielman@CaryKelly11 I can tell you don't know a lot about student loans.

You've sucked in all the propaganda programming.

Read this. I'll be surprised about the truth of this loan scam.

https://t.co/w3Y1DcsO1w