or 52 weeks in a year:

$1,000 per week = $52,000

$2,000 per week = $104,000

$3,000 per week = $156,000

$4,000 per week = $208,000

$5,000 per week = $260,000

$6,000 per week = $312,000

Singles and doubles do add up but sometimes hitting a home run here and there is nice 🤑

There are approximately 250 trading days a year

$100 a day = 25K

$200 a day = 50K

$400 a day = 100K

$500 a day = 125K

$1000 a day = 250K

Singles and doubles add up…

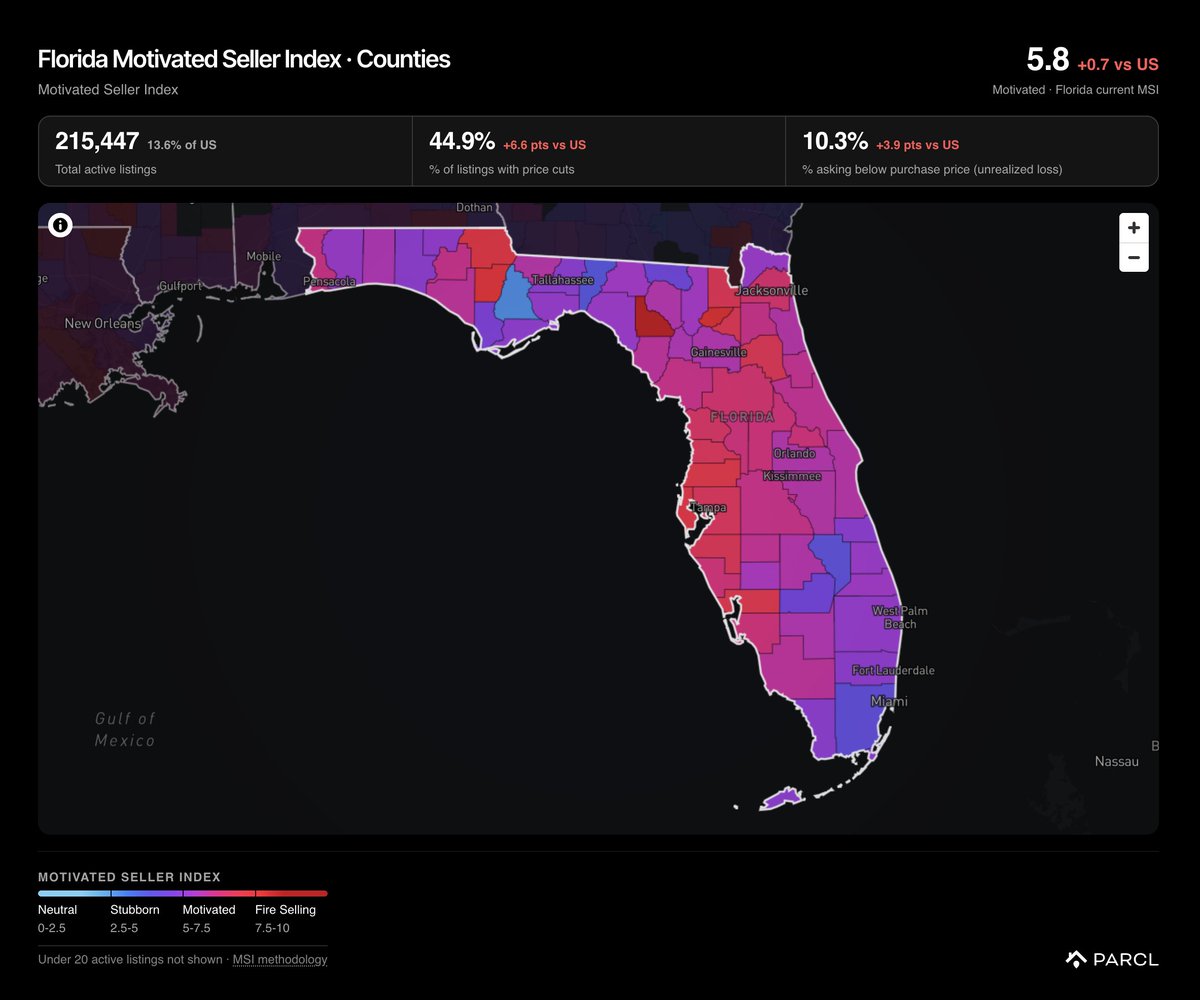

BREAKING: As of tonight, 1 in 7 homes for sale in America is in Florida - a state with only ~8% of the nation's homes.

The Florida for-sale market is flashing warning signs:

45% of listings have taken a price cut (6.6 pts above the national rate)

1 in 10 homes are selling for less than the original owner paid

U.S. housing demand is mired near record lows entering the Summer.

Reventure's housing demand index fell this week to a 10/100.

This corresponds to near-record-low interest in buying houses.

Mortgage Applications to buy, online home searches, and buyer sentiment all went in the wrong direction in June.

This suggests we should see stable to falling existing sales over the next couple of months.

Note that today's forward demand levels are better than at the lows in 2024, which is a positive.

However, any type of sustained breakout in buyer demand seems unlikely so long as prices remain this high.

Track this data for your ZIP on Reventure Mobile: https://t.co/9iDZkqlhE0

The homebuilder market is in its biggest recession since 2009.

Months of supply for homes under construction is now 14.8 months. Permitted homes not yet started have surged to a record 21.3 months.

Both are similar or worse than the 2008-09 housing bust.

Suggesting that future demand for new construction is in the tank.

The one exception is completed spec homes, where the months of supply is just 3.9 months.

Builders can still sell move-in-ready inventory, especially when paired with mortgage rate buydowns and incentives.

But anything further out in the pipeline is piling up.

The result: builders are struggling to justify tomorrow's construction, and this builder recession is likely to get worse. Don't be surprised if we see a big pullback in starts at some point.

Track building permit data by county on Reventure Mobile:

https://t.co/dBXshG2eiP

it's amazing how many listings in Florida currently have the word "Short Sale" in the listing description.

Over 1,200 currently.

I'm seeing some houses being cut in price as much as $100,000 to $150,000 from their 2022-2024 purchase price.

These are situations where agents are openly advertising that the seller is in default on their mortgage and is trying to liquidate the property.

Short Sales have risen over the last several years due to a downturn in prices in Florida, and low demand, combined with sky-rocketing costs for existing owners.

Meaning it's actually a good time to get in there and start submitting low-ball offers in Florida, as on some listings you can get pre-pandemic pricing.

Just make sure you understand if the market is going to drop further after you buy.

https://t.co/50vYuH8G3u to see our 2027 forecast.

JUST IN: ACROSS ALL ACTIVE US HOUSING LISTINGS AS OF THIS MORNING, 1 IN 5 SELLERS WHO BOUGHT IN 2022-23 IS NOW ASKING LESS THAN THEY PAID

The home buying class of 2022 bought at or near the top of the housing market. Today, 19% of them with a home on the market are listing at an unrealized loss - 10x the rate of sellers who bought before 2020, despite having nearly two-thirds as many homes on the market as that entire cohort.

The damage: $1.7 billion in unrealized losses, a median haircut of $30,000 per home.

One cohort. Half of every underwater listing in America.

Where it's worst: Austin. 59% of 2022-23 buyers selling there are asking less than they paid - a median $84,000 below their purchase price.

Unrealized loss = the seller's asking price is below what they originally paid.

Florida's population losses are compounding.

Miami had the 4th-largest population loss among U.S. metros in Q1 2026.

Orlando had the 6th biggest.

And Tampa lost more people than Chicago.

This data comes from Bank of America's internal account data and is a shocking revelation for anyone who thinks Florida's housing market is recovering.

People continue to leave Florida due to still high prices, soaring property taxes, and expensive insurance.

So much so that a state that was built on massive levels of in-migration of Americans is now losing people in its three biggest metro areas.

As a result, don't be surprised if Florida's housing market continues to correct until things become cheap enough to keep people from leaving.

Track migration by county at https://t.co/50vYuH88dW.

US home sellers are retreating from the market:

Delistings as a proportion of all US home listings rose to 5.8% in April, the highest since March 2020.

Excluding the 2020 pandemic, delistings have never been this high.

The absolute number of delistings rose +3.8% MoM, marking the 2nd consecutive monthly increase.

Atlanta led among the 50 most populous US metros, with 10.7% of April listings taken off the market, followed by San Jose at 9.3%, and Los Angeles and Dallas both at 7.8%.

This comes as inventory is rising faster than demand, with buyers gaining negotiating power and many sellers refusing to accept lower offers.

The housing market stalemate is intensifying.

Chicago lost the Bears this week. A team that's been in the city since 1921.

They didn't lose them to a bigger market or a better deal. The Bears decided they'd rather be a tenant in Indiana than deal with Illinois for one more year.

Think about how badly you have to run a place for that to be the smart move.

They lost them for two reasons.

The people running Illinois would rather villainize a builder than keep one. And they're bad at their jobs.

In 2021 the Bears spent $197M on the old Arlington Park racetrack.

Before they could break ground, Cook County valued the empty lot at $192M (Bears said $60M). They were salivating at the chance to extort a building that didn't even exist yet.

That fight dragged on for years.

The Bears were ready to put $2B into the stadium. All they wanted was a promise the county wouldn't reassess them into oblivion, plus $855M for infrastructure everyone uses. Roads, transit, utilities. A $3B project, two thirds of it private money pouring into Illinois.

Springfield had since 2021 to get this done. They dragged it to the final night of session, passed it through the Senate at 3:39AM, and the House went home without voting.

So now it's all gone.

The funniest part? This started because Cook County tried to grab the tax early. They knew a built stadium would pay $53M a year. Now they get under $4M on a vacant lot. No jobs, no buildout, no new anything.

Congrats on fighting for scraps and losing the whole prize.

Pritzker: they're "an $8.5B valued business" that doesn't need propping up.

But be smart for a second. Almost every NFL city throws in public money for a stadium. Not charity. The return is real. Tourism, hotels, restaurants, jobs, game days, property tax on a huge development. The math works.

Indiana did the math. While Illinois sat on it for years, Indiana passed a bill in months, put up $1B, and took the team.

And the Bears took a worse deal to get there. In Illinois they were going to own their stadium. In Indiana they rent it from the state. A team that wanted to build its own home gave up ownership just to escape Chicago.

Nobody won but Indiana. The Bears lost their stadium. Illinois lost the team, the $2B, and $53M a year in taxes.

Pritzker after they left: "I wasn't willing to give up billions of dollars of taxpayer money to give it to a billionaire-owned family or team."

There it is. "Billionaire-owned."

That's how Democrats talk about any business right before they run it out of town. Call them a billionaire, act like you're saving working families, take a victory lap while the tax base drives across the state line.

Meanwhile they're running the whole state into the ground. And you already know how this ends. You're living in it.

Pensions are $143B in the hole, worst in the country and not close. You pay $6,285 a year in property taxes, double the $2,969 national average, for a city that's $1.15B in the red. The mayor called its finances "the point of no return."

When you run things this badly, you sell what's left.

They leased the parking meters for 75 years to Morgan Stanley and a sovereign wealth fund in Abu Dhabi. Took $1.15B and burned through it in two years. The investors already made it all back, with 58 years left to collect.

Sold the Skyway. Sold the downtown garages. Every asset that made money, gone for one check.

But a fixed property tax rate for a team that's been here 106 years? That's "propping up billionaires."

Companies are leaving. Boeing for Virginia. Caterpillar for Texas. Citadel for Miami. In 2023 alone Illinois lost 56,000 people and $6B in income to other states. The ones who left earned a third more than the ones who moved in.

Indiana didn't outbid anyone. AAA credit, 16 years straight. A $676M surplus. Fourth-lowest debt per person in the country. They just weren't a disaster.

Illinois could have collected $53M a year. It chose zero. Ignore all the bad management but make sure to stick it to those evil, pesky billionaires.

BREAKING: MicroStrategy's, $MSTR, unrealized loss on its Bitcoin holdings rises to a record -$12.7 billion.

This puts the company's position down -$28 billion over the last 12 months.

Existing home sales over the first four months of 2026 were the lowest since 2009.

In April, 4.02 million existing houses were sold on an annualized basis according to the NAR's data.

This figure was below last year's and the lowest level since April 2009. (in the midst of the Great Financial Recession).

Buyers continue to exit the U.S. Housing Market because they don't want to pay today's sky-high prices, or can't afford to.

Making this the 4th straight year of recession-level home sales.

The pending sales figures in April/May suggest we might finally see a bump next month, but it's hard to think of that as more than a dead-cat bounce given how bad the first four months of the year were.

Lower prices are the only way buyers will come back.

U.S. homebuyer demand just hit its lowest level ever for the month of March.

According to NAR Pending Sales, contract signings fell yoy to an index of 73.7.

This was the worst monthly reading for March ever, even lower than 2008-09 crash.

Worst yet - demand proxied by contract signings is now 30% lower than pre-pandemic norms and 45% below pandemic peaks.

(even though there was a modest 1.5% monthly jump from February to March, which is barely perceivable in the long-run graph)

The story here is the same as it has been the last 3 years: buyers are on the largest buyer's strike in U.S. history, and it continues to get worse.

With the only solution being lower prices.

To see the areas where we think prices will drop most into 2027, download our app: https://t.co/pLvj026xCj