Here’s a common mistake made in crypto re: “midcurving”

Nobody means “human population midcurve”, they mean “crypto midcurve”. Move your curve over one standard deviation — and no I didn’t mean to the right, you midwit

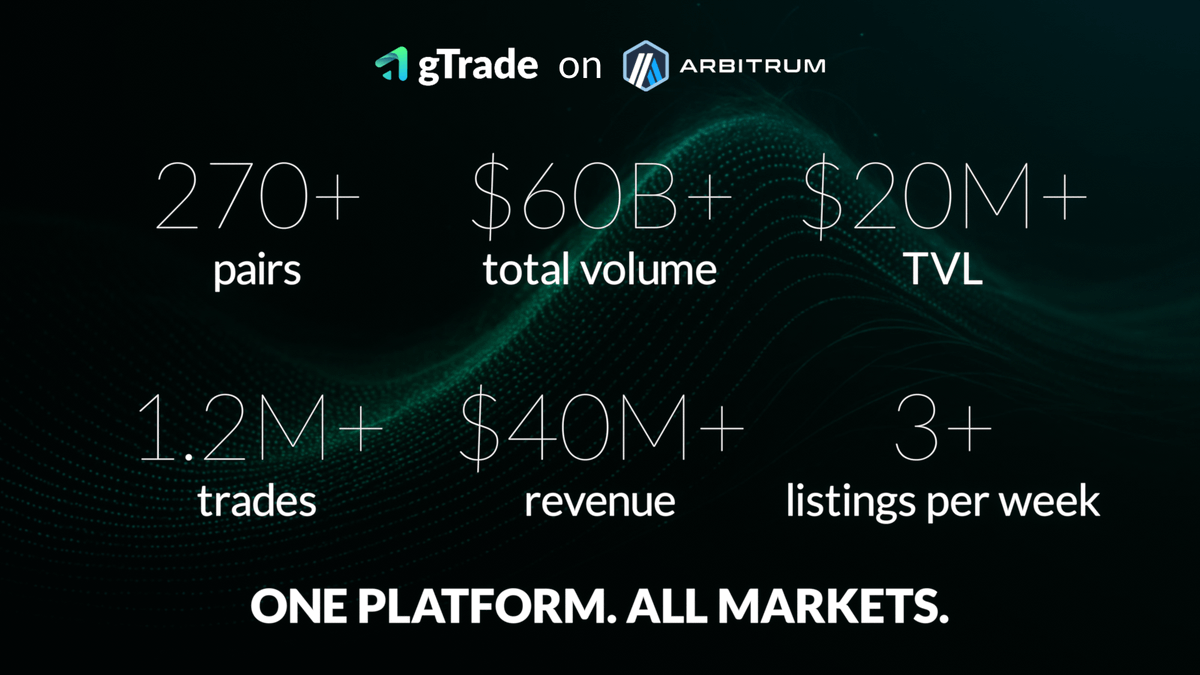

$GNS remains an outright fire risk

@GainsNetwork_io consistently top 20 crypto projects for real earnings, but only top 800 for market cap

The majority of that yield *market buys* the token to be burnt, currently torching supply to the tune of ~25% per year 🔥

Supply shock?

“Sir… another 500,000 $GNS has been burned. Should we stop it?”

“No. Let the burn continue.”

“…Yes, Mr. Seb.”

Total Supply: 29,482,349 and dropping.

Watch the burn for yourself ➡️ https://t.co/tws6QzILVl

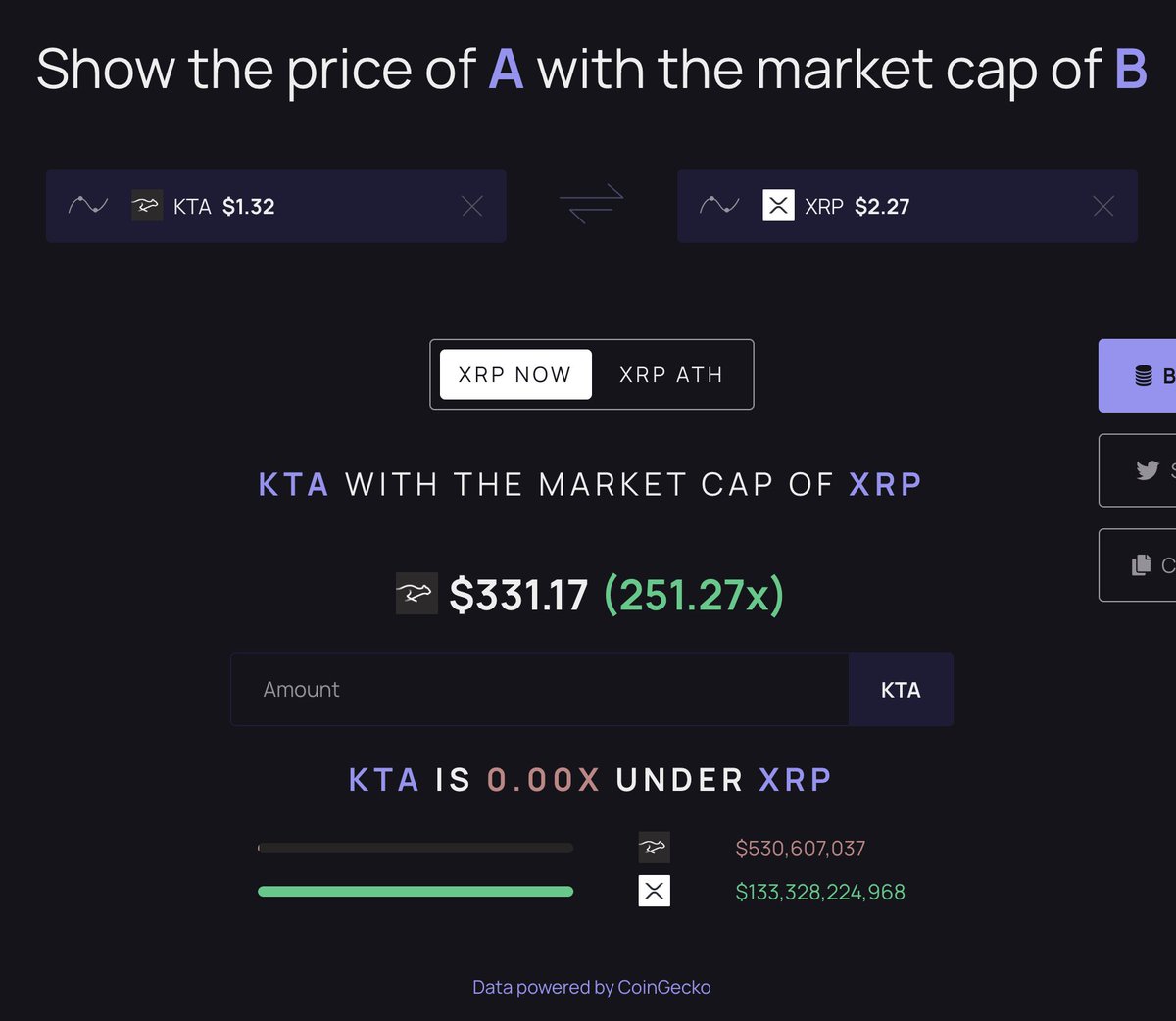

$KTA post incoming:

When you look at scams all day, it's easy to think that everything is a scam. Our opinions are influenced by our lived experiences.

This isn't the first keeta fud and it won't be the last. It needs a pullback anyway, random buyers are up 7-8 figs (and people try to claim this wasn't a fair launch, lol). There is no other asset (other than BTC) that I am holding with as much long term confidence. Explaining why below.

If you don't know why XRP/Ripple has the valuation that it does, it's worth looking into. To summarize - traditional banking rails suck. Blockchain technology is undoubtedly a faster, more modern, and easier to set up way to send money across the globe. But SWIFT can't just replaced by anything - banks are subject to an incredible number of regulatory and compliance requirements, not to mention security is the topmost priority. Fully decentralized networks just aren't reasonable for a company that has to deal with KYC and the multitude of regulatory requirements.

Enter Keeta.

Built in KYC. Compliance & Regulatory understanding and knowhow.

Ty Schenk and co worked on Nano (RaiBlocks if you're old enough) almost a decade ago. And it was the fastest and easiest to use blockchain of the time - hell, it still has a small but dedicated community. What went wrong? It was too idealistic - what sustains a network with no fees? But the DAG architecture has always had incredible potential due to its speed and scalability. And now, the team has had 10 years to refine it, and make it fully scalable purely on existing cloud service providers.

Eric Schmidt investing and backing Keeta is just one of many interesting things about this company; trying to say that this single point brought this company to a billion dollar valuation is asinine. But it shines a light on the fact that the team is connected to the right people. I could write the best, fastest, most efficient, scalable, reliable money transmitting product right now that also prints gold bars out of thin air, and without the right connections, no one will use it. The ex-CEO of Google's involvement gives Keeta a foot in the door. Not a guarantee, but a shot.

Existing banking rails have to go. Have you ever sent an international wire? Enjoy the $50 fee, dealing with the intermediary bank, and with settlement time of a few days.

Ripple has known that this is the case for years. That is why they are where they are. But you know what? The tech sucks. It's slow, it's painful. Keeta has more than just the speed advantage though - it's got the proper connections & partnerships, and it's got the compliance features that banks don't just want, but NEED. Compliance is not optional. Regulatory scrutiny on banks is not going away any time soon.

Token supply and team holdings have been covered ad nauseum by Ty and team members in the Discord, so I won't go over it. Could this whole thing fail miserably? Sure. But if you can see the potential, don't fall for ragebait. Don't listen to the guy who claims that he's the first person to access a testnet that's been live for a month. Make your own decisions. Do your own research.

Keetard out.