@GernotWagner You're right. But please let's not make the perfect the enemy of... the possible... again. It will be perfectly clear within 12 months that $50 / tonne, or even $150 / tonne, aint gonna do it. But only if it's already in play...

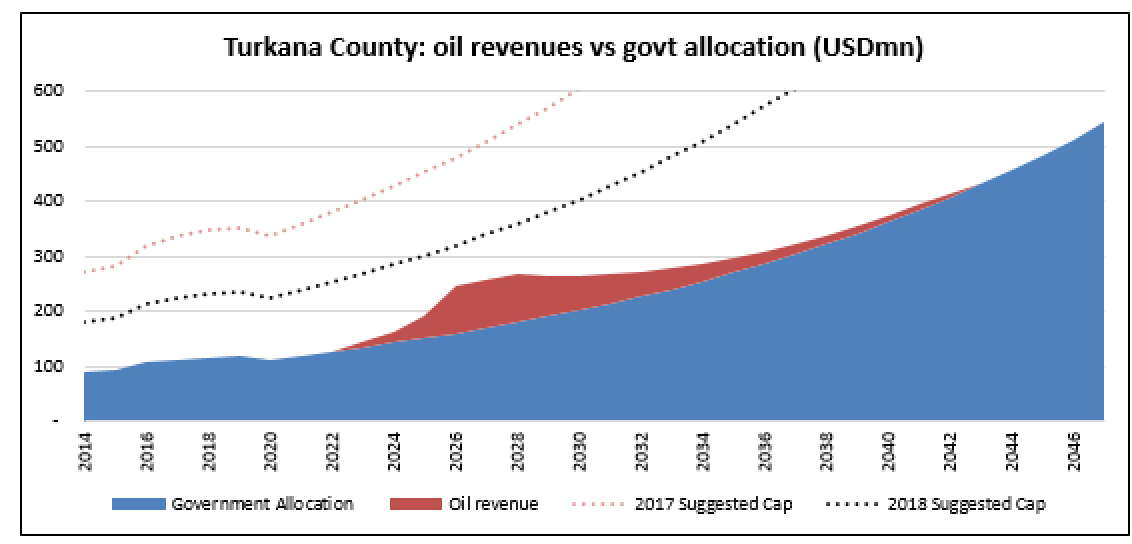

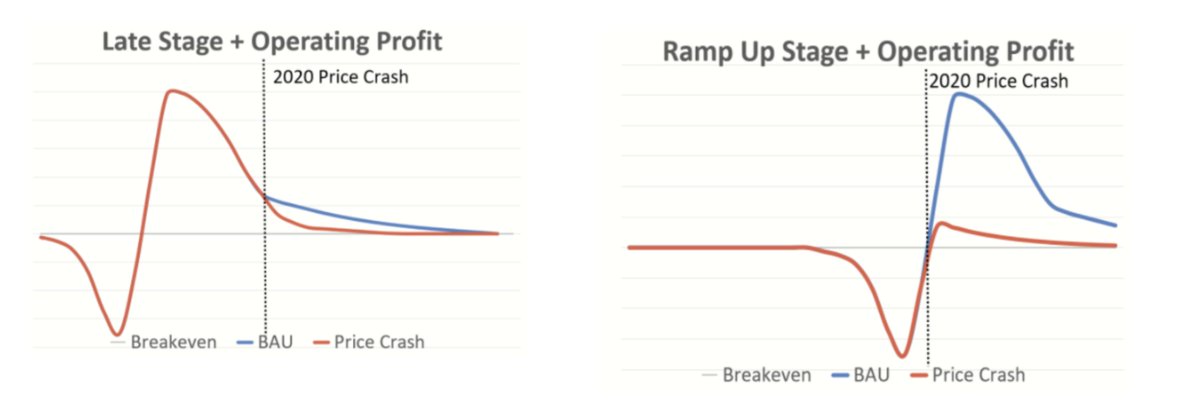

Our analysis with @InVhestia suggests under almost any realistic price scenario, the Turkana project would achieve a point forward negative NPV with production lower than 900 million barrels. @boell_stiftung

Our latest financial model is here: https://t.co/Tq1TWHjJjl

IRR for the contractors in Uganda and Kenya #oilprojects are low or inexistent under current market conditions suggesting either that neither will go ahead or that companies would see further concessions in the fiscal regime. Read our analysis here: https://t.co/Tq1TWH27UL

Our new analysis is up! #Kenya: No current price projection could make Turkana Foundation Stage commercially viable for the contractors. @Open_Oil and @InVhestia analysed the effects of the 2020 market conditions. Read more here: https://t.co/Tq1TWH27UL

@Open_Oil and @InVhestia revised their previous financial analysis of the Turkana Project (2018) to account for the effects of the 2020 market conditions and the likelihood of an FID: this is what we found: https://t.co/Tq1TWHjJjl

@boellza

To meet the targets of the #ParisAgreement most fossil fuel reserves will need to remain unburned. But how to incentivise reserves-rich countries to give up the often long-cherished dream of oil wealth? Our proposal here: https://t.co/Sb9k3TUH7O

#Climatechange

Compensating Indebted Countries for Keeping Fossil Fuels in the Ground, a proposal that could prevent up to 400 gigatonnes of carbon emissions at a cost varying between US$2 and US$10 per tonne. Read more here: https://t.co/Sb9k3UchZm @boell_stiftung @GDPC_BU @SOAS

Effective climate action requires leaving vast amounts of fossil fuels in the ground. But how can countries be compensated?

Our latest analysis published by @boell_stiftung is available here: https://t.co/Sb9k3UchZm

@GDPC_BU @SOAS

The government's published guidance range for the value of 49% of #Agyapa shares looks to be undervalued. #Ghana

Here is our latest analysis alongside recommendations for further discussions: https://t.co/TEHkDh305O

The innovative and -very criticised decision- to float 49% of #Agyapa into the international market could be worth US$ 1.47 billion #Ghana@EITIorg

Read our analysis and recommendations here: https://t.co/TEHkDhkAXm

Our latest analysis is out! What is the real value of Ghana's controversial decision to sell most of its royalties to private investors? More than expected by the government! @EITIorg#Agyapa

Find out here:

https://t.co/TEHkDhkAXm

Energy transition effect: Senegal's oil and gas reserves beyond first phase at risk of becoming stranded assets. Our latest analysis is available:

https://t.co/3vOMnXZglO

Petrosen dilemma: Exercising contractual equity right exposes Senegal to over a billion dollars more debt. There is a significant risk these loans might never be earned out, making them loss-making investments Our latest analysis here:

https://t.co/3vOMnXZglO

Les revenus offshore du Sénégal n'arriveront qu'après les années 2030 et ne seront pas transformationnels. Le secteur n'apportera pas une contribution significative aux finances publiques. Une analyse détaillée de l'économie du secteur se trouve ici:

https://t.co/W7m1S0SKof

Les projets pétroliers et gaziers du Sénégal vont-ils connaître une phase 2 ? L'analyse économique des projets suggère que cela n'arrivera pas et voici pourquoi :

https://t.co/W7m1S0SKof

Les revenus potentiels du pétrole et du gaz ne peuvent pas alléger la dette publique du Sénégal, qui s'élève à environ 15 milliards de dollars. Comprenez pourquoi dans notre analyse:

https://t.co/W7m1S0B9wH

Effet de la #transitionenergetique et de la pandemie #Covid-19 : Les réserves de pétrole et de gaz du Sénégal au-delà de la première phase risquent de devenir des actifs échoués. Notre dernière analyse est disponible : https://t.co/09lxazxYzn