SK하이닉스 일본 주재원 계신 분이랑 커피챗 내용 간단하게 공유

1. 메모리 수요가 너무 강력해서 일본 고객들에게 줄 메모리가 없다.

미국이랑 중국 고객 주고 나면 일본에 줄 물량이 없다고 함. 그래서 일본업체들 찾아가서 매번 쓰미마셍 고개 숙인다고 함.

2. 메모리 부족으로 닌텐도 같은 전자제품 가격 계속 올리는 중.

메모리가 없어서 난야 같은 업체 뿐만아니라 윈본드 같은 업체도 찾는중.

CXMT는 기가바이트 통해서 이미 소비자용 제품으로 들어가고 있다고 함.

3. 일본에 있는 CXMT 한국엔지니어를 통해 듣기로는 CXMT 설계능력이 생각보다 엄청 뛰어나다고 함. 2-3년 격차가 아니라 그보다 더 좁혀질것 같다고 함. 진짜 중국의 똑똑한 인재들이 밤낮 안가리고 일한다고 함.

한국도 경계해야 할듯.

4. 메모리 가격은 계속 인상 중.. 몇프로인지는 밝힐 수 없지만 계속 인상중. 오늘 엔비디아 소캠에 메모리 줄었다는 이슈로 주가가 내리는데 메모리 가격은 오히려 올라서 영업이익은 계속 올라갈 전망.

*개인적으로 걱정되는건 이런 메모리 가격 상승이 Capex 투자 부담으로 이어져서 AI 싸이클이 빨리 끝날까봐 걱정임. 구글도 채권찍고 있고 빅테크들도 현금이 떨어져 가는게 걱정됨.

*투자권유, 매수,매도 추천 아닙니다.

💡 Codex Tip: Just ask Codex for automations

Codex can schedule for itself and also update those automations.

- Ask it to do something later in the same thread

- Have it do the same thing it just did but on a regular basis

- Have it review your existing automations and improve them

- Clean up unnecessary / ineffective automations

In my case I still had some automations running on GPT-5.4 so I had Codex update them

Identify the dominant theme.

Align with the macro narrative.

Allocate along structural industry trends.

Validate positioning with incremental flows.

Control pace through style rotation.

Orderbook L2 updates

Left -Proliquid APIs

Right -Hyperliquid APIs

If you want to step up in your trading on Hyperliquid and take better informed decisions...

https://t.co/GO9ytT4yV6

codex power-user best practices:

- a few different "pulse" threads that run every morning to check the status of stuff i care about, e.g. proof metrics, all company meetings, etc

- a "log" thread for ongoing, everyday activity i want to track. for me that's my "writing log"—want to track what im writing about, and working on from piece to piece

- "inbox" thread which gathers all of my emails right now, but eventually will pull in all of the main important things from each "pulse" thread

- "router" thread which knows about all of the other threads, and is also hooked up to my email to push emails into each thread appropriately

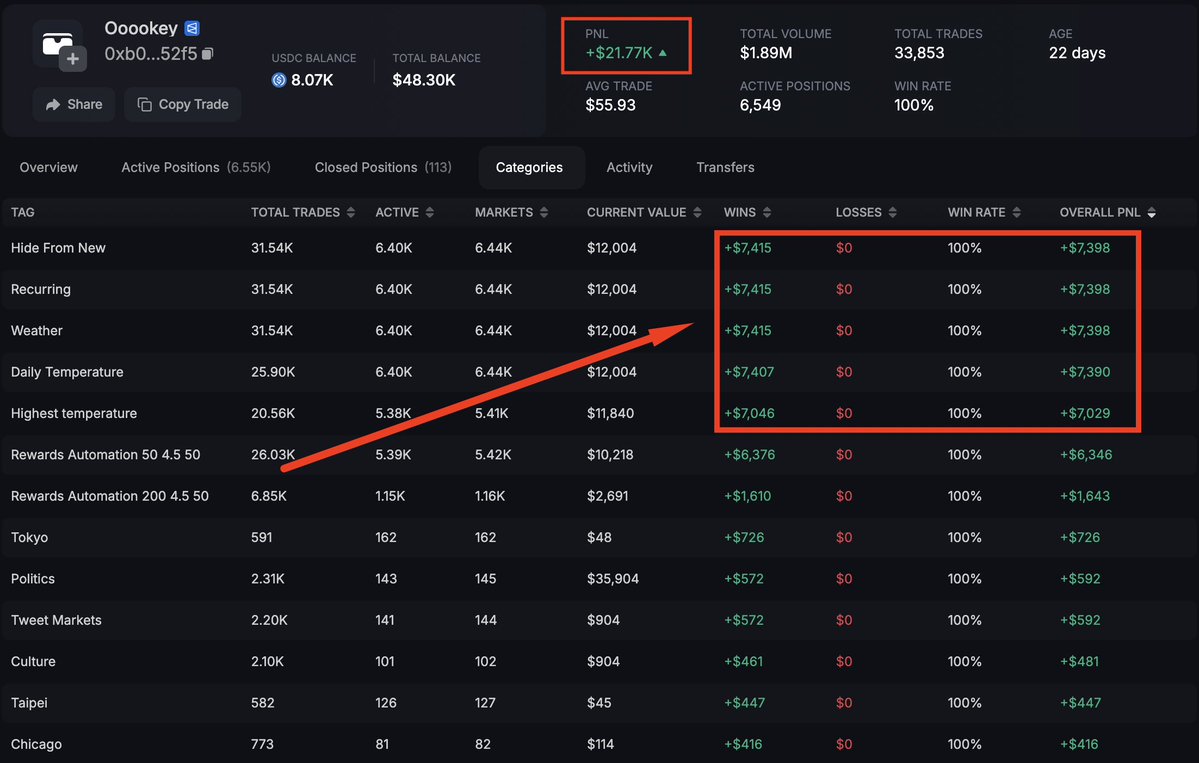

Forget crypto. This guy just made $738 → $3,454 on weather.

Meet Oooookey. 7,462 predictions on Polymarket and a perfectly straight profit chart going straight to the top.

Profile: https://t.co/UU3OkpFr5D

His secret? Meteorological alpha.

He buys undervalued city temperature forecasts for pennies (30-40¢) and rides them to a guaranteed $1. No stress, just steady daily profit. But most likely, software helps him.

Best active hits:

$848 → $2,106 (Madrid Temperature)

$358 → $1,154 (Hong Kong Temperature)

$741 → $1,253 (Seoul Temperature)

Want the same? 3 steps:

1. Open → https://t.co/ciLwjiRNBf

2. Select the Copy Trade tab.

3.Paste this trader's wallet and start copying it.

Photonics is nuanced and using ChatGPT/Gemini makes you miss all of it:

1. $SIVE is actually a chokepoint and partially a bottleneck.

The reason it's a chokepoint is leading CPO/optical hyperscaler players go through Sivers, likely:

Ayar. Celestial. Lightmatter. Lightelligence. Poet.

If you take out Sivers, you literally can't make some of their products + delay their roadmap by years.

As many are sole/primary source but are heading the direction on multi-source.

As for the bottleneck argument: Win Semi is the bottleneck for scaling laser production.

But... the nuance is when you have capacity allocated for the next few years.

You become part of the bottleneck itself if players fight you for allocation of finished lasers.

That's the nuance people miss with capacity allocation dynamics.

It's like saying $SNDK is not part of the NAND bottleneck when Kioxia makes all of it.

But when Sandisk has the ultimate control of output supply, they become the bottleneck + have all the pricing power.

Sivers controls output supply of CW lasers given allocations, and as seen with $LITE earnings, CW laser is currently bottlenecked as everyone seems to be stuck producing EMLs.

2. Like how LLMs always uses em-dashes.

You can tell when people use AI when they always use the same "CW is a dumb interchangeable laser" argument or compare "power" specs after conflating different architectures.

That's why your "analysts" using AI will get this wrong over and over.

There's CW lasers... and then there's a specific architectural design that Sivers achieves with DFB lasers.

If you compare power specs with $LITE vs. Sivers, Lumentum wins in isolation. But they're completely different laser architectures.

All the leading CPO players like Ayar, chose $SIVE for an architectural reason for high power, low thermal, laser arrays. $JBL 1.6T LRO also made one of the most dramatic moats cited by their fireside chat, using Sivers lasers.

If you think CW lasers are interchangeable with Sumitomo/Furukawa, and others. And can be plug-and-play... i don't know what to tell you?

Again: $SIVE makes architecturally unique CW lasers for leading CPO players.

3. I'm not sure how many times I need to say this:

$SIVE for 2024-2025 has been going through development contracts. People using TTM revenue or former P/S metrics are using completely the wrong metrics, when there's volume ramp in 2027.

It's the same with $AAOI which volume ramps in H1 2027.

$AEHR which volume ramps after qualification.

$LPK that volume ramps after qualification.

This is just missing qualification cycles in semiconductors and how to model financials currently.

As for the $LITE comparisons (which was also my long last year):

$LITE literally started off selling laser dies before acquisition of Cloud Lite and other downstream optical engine components.

This is where $SIVE is at today with starting off in the laser chokepoint for CPO:

People are modeling laser revenue off very isolated TAM projections. Meanwhile Sivers is targeting M&A to expand revenue for TAM projections.

This is not a simple component FAU + ramp valuation modeling over with a Taiwanese company.

Since Laser companies like $LITE, $COHR are known to downstream expand to make their lasers more valuable, then vertically integrate (fabs, assembly) afterward.

Again, Sivers worked with Ayar and these types of companies before they all became billion dollar companies. I have high conviction knowing they know what to acquire down the ELS/optical engine stack + pluggable transceiver for TAM expansion.

It's just annoying when I get people who don't understand the nuances backseat commenting wrong things about my longs.

I got the same thing about $AXTI is not a bottleneck! InP isn't needed! China! back at $14.

Now it's $140

I got the same thing about $AAOI "is going down 50%!" back at $65. or "AOI management is shady at $30".

Now it's $170

I got the "there's nothing new with $SOI" back at $45.

Now it's $170.

I think I'm one of the few who actually understands the nuances with photonics, since I did call out $LITE, $TSEM, Innolight, $AXTI, $AAOI, $SOI, that outperformed both photonics markets and overall markets over the past year.

And now I'm long on $SIVE.