Most US investors won't look outside the S&P 500.

Most non-US investors won't look under a $5B market cap.

That means many high quality businesses that dominate a niche industry are simply ignored.

I'm finding ‘hidden gems’ with 20-30% ROICs and excellent owner-operators trading at 10x FCF.

As the market becomes increasingly focused on Large-Cap AI, the number of ‘hidden gems’ seems to be increasing.

That will change at some point, and the time to be prepared is beforehand.

1/ $XPEL pitch by @AltaFoxCapital

The only public pure-play in paint protection film, a niche, underpenetrated market (~5% US) where XPEL owns ~35% share. Its DAP pattern software locks in installers, and the strongest consumer brand with meangfull pricing power over peers.

$XPEL XPEL Announces Approximately $110 Million Manufacturing and Supply Chain Investment, Including Expansion of San Antonio Operations and Acquisition of Manufacturing Facility in China

Published my April web traffic report on $HAYPP today. As a teaser for the May report that I will publish in 2 to 3 weeks, I wanted to show this chart of hayppcom, one of their larger sites. By the looks of the current spike, we might soon be looking at their biggest site.

Essentially what the chart shows is that average volume for the site was 32% above last Q. And when we look at the ending value of the most recent data point, we see that their traffic is up a whopping 77% from last Q. Could be a temporary spike; however, it is still likely to lead to substantial sales.

More on the trends in my April report below.

$Haypp Group is seeing some strong surges in web traffic. With web traffic being highly correlated to revenue, Q2 could get interesting. Check out my blog that breaks down each site's data.

I think I am now the most bullish on $Haypp I have been since the 2024 Q4 lows.

Massive surge in web traffic across the group.

FDA guidelines strengthen the story substantially; more authorized SKUs means more inventory for Haypp's platforms to sell.

Chatter on X is roughly 1/4 of what it was six months ago. Nobody is paying attention.

On the flipside, regulation is always tricky and it is hard to know what exactly will happen in the near term.

The biggest signal in an earnings call is often a number management used to disclose and quietly stopped.

$XPEL's Q1 is a good example.

For several quarters, management has not disclosed OEM channel revenue. On the call last week they said that OEM is "just under 7%" of group revenues — about $8.0mm.

Two years ago that number was $4.6mm.

That's 74% growth.

This could be a very big deal in the long run.

The biggest lever to XPEL’s growth remains increasing awareness of PPF. OEMs and dealers are the natural point of sale and could become XPEL’s biggest sales channel.

The cash flow statement also revealed capex of $9.7mm in Q1 — more than the entire $4mm spent in 2025.

It appears that XPEL's manufacturing build-out has begun.

Full breakdown at the link in the first comment — including why the Tesla deal in July last year was the inflection point for the OEM channel.

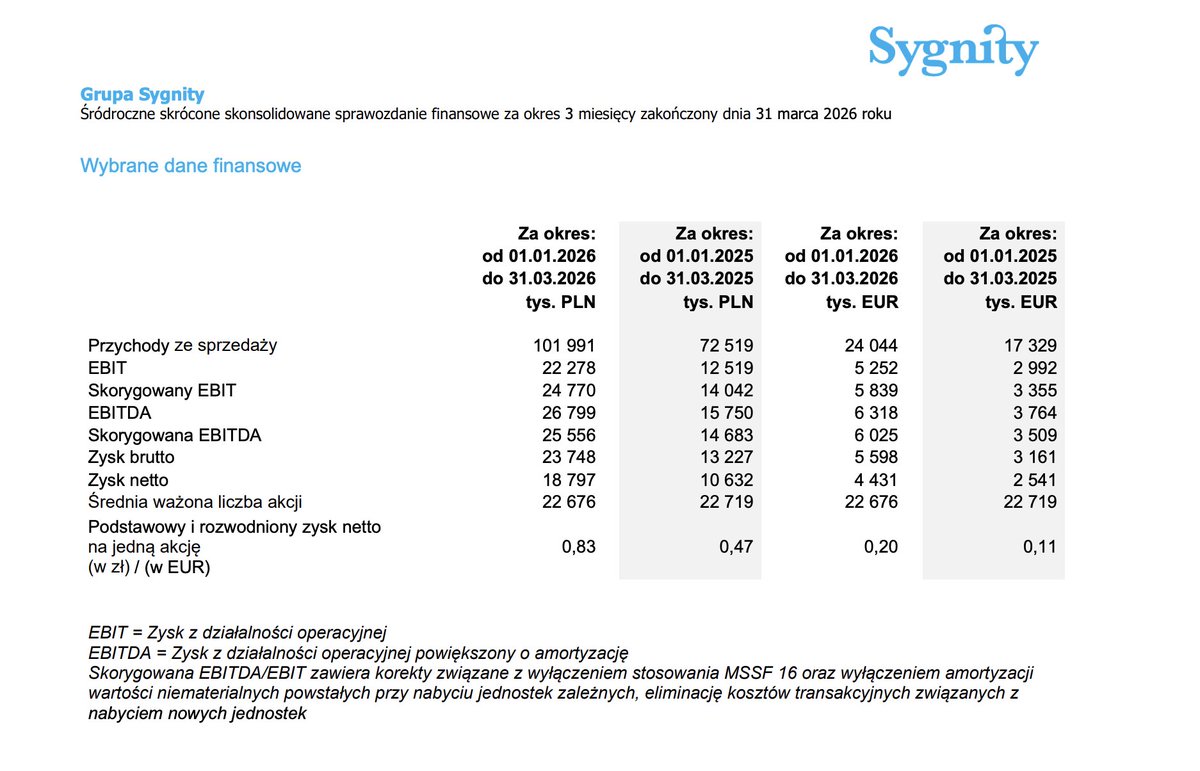

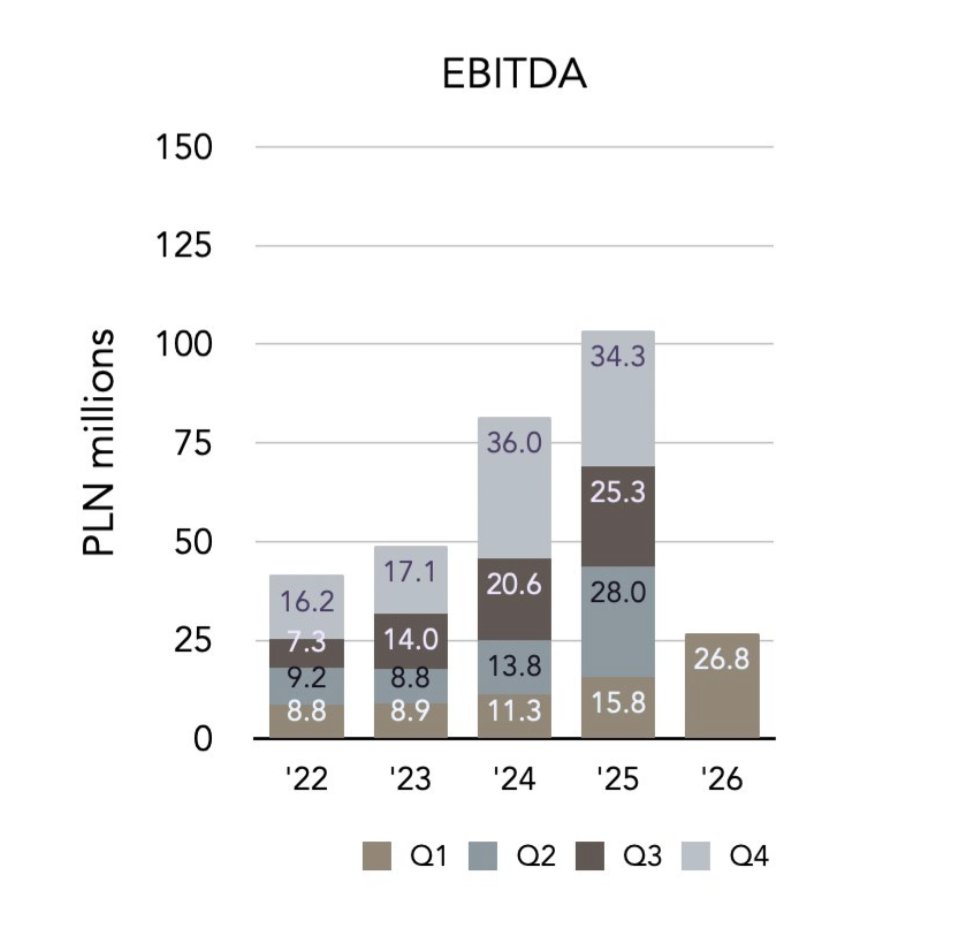

Sygnity Q1 final numbers are out $SGN.WA

Revenues PLN 101.9 million +41% y/y

EBITDA PLN 26.8 million +70% y/y

Net Income PLN 18.8 million +77% y/y

CFO PLN 24.6 million +84% y/y

Margins continue higher

Many people might still find the FDA news a bit cryptic and struggle to translate it into price action. For $HAYPP the FDA announcement essentially means a lowering of WACC and an expansion of the terminal multiple.

We are talking roughly 200 to 300 bps reduction of WACC pre FDA announcement. I have been using something around 20% to discount Haypp; the FDA news pushes it toward 17 to 18%. Terminal multiple expands in an equal way.

And we know the US will represent a large majority of future cash flow, so the impact compounds.

Simple napkin math says this news alone could impact the stock roughly 20 to 40% as investors redo their calcs over the coming months. So far we have seen 11%.

Updated my $HAYPP deep dive. The thesis in 6 points:

1/ Nicotine pouches are a generational consumer shift. Pouches are cleaner, cheaper, discreet, and healthier than smoking. The global category can 30x over the next two decades. Haypp is the only pure-play online way to own it.

2/ Haypp is the dominant online retailer in every market it operates in; typically 4 to 7x larger than the next competitor in organic visibility. First-mover, in-house SEO and GEO, and an AI-assisted content engine that competitors cannot replicate quickly.

3/ The real moat is data. Every can sold feeds Media & Insights, which sells reports and decision support to PMI, BAT, TPB, and others. M&I is close to 10% of revenue at much higher margins. Over time it can become the second profit pillar.

4/ The FDA shift is the most important regulatory development in years. ZYN PMTA, on!Plus authorizations, the accelerated pouch pilot, and the May 8 2026 enforcement guidance materially de-risk the US category. Regulatory tail risk has been the single biggest reason the sector traded at compressed multiples.

5/ Valuation is reasonable. Haypp trades around 1x sales. Hit the 2028 targets (8.000 MSEK revenue, 5,5% +/-1,5% EBIT margin) at a 15 to 20x multiple and you get roughly 3x the current market cap. 30% annualised returns over the next 3 to 4 years does not require heroic assumptions.

6/ Catalysts are stacking. First North to main market uplisting (likely soon), FDA-driven sector reheating, Swedish retail flows recovering, and eventually a US listing in 2028 to 2029. Each one independently rerates the stock.

Full deep dive in the post below. Free to read.

$HAYPP Q1 webcast notes.

NP 70% of sales. Media and Insights 11,6% of revenue, grew 40% YoY, main driver of stable gross margin. 2x 2024 revenue target by 2028 reaffirmed, Q2 acceleration hinted.

US NP volume +123%, UK +103%. Active customers +66% in Growth, +5% in Core. Snus decline moderated to -4%. Vape +119% in Sweden and Germany.

Low EBIT this year expected, US and UK headcount investment continues. Overhead intensity to moderate. EBIT expansion into 2027 and 2028.

Growth gross margin higher than Core because Sweden is more competitive. More oxygen in Growth markets justifies the investment posture.

US assortment expanding fast, more FDA approvals expected. Paid ads beyond SEO running. UK Bill tightens market and lifts Haypp's relative media value. UK warehouse automation live this summer.

Taxes seen as tailwind, NYC ~2 USD per can pushes consumers online. AOV down because manufacturers cut prices to Haypp, volumes up. UK 20mg cap not a real constraint, delivery matters more than mg.

Beating CMD 2025 expectations. On track for 2028. Full piece on the blog later.

$CPH.TO Solid update, particularly on costs and the bottom line.

- SG&A down 42% YoY driven by significant reduction in US headcount and roll off of litigation expenses.

- Would like to see more from the topline (4%, and only 1% excluding 50% bump in Absorica). But 3% Natroba growth while slashing costs is nevertheless positive

- Net result is $7.7m EBITDA at an enviable 62% margin. Best result since the acquisition despite this being a seasonally weak period. Even cutting quarterly Absorica revenue by 50% on this cost structure, I think you can conservatively annualize this figure, which gets you close to $32 m EBITDA for 2026 - putting the stock at ~10x.

- Debt fully paid down with >$70m of liquidity incl revolver capacity. Ample room for M&A and buybacks. Taking longer than hoped for another deal, but it's certainly not due to a lack of effort internally. Hard to not be accretive at this multiple and the company's discipline on managing costs. No doubt it will come.

- Per the call, Craig's been speaking to Moberg again and that optionality appears very much alive. Could be huge.

$cph.to

Cipher Pharmaceuticals Reports First Quarter Results

MANAGEMENT’S DISCUSSION AND ANALYSIS For the three months ended March 31, 2026

https://t.co/4NnqF9E4i4

Did $XPEL just annouce it is building out its own manufacturing?

The company previously said it would increase gross margins by 10ppts to 52-54% and EBIT margins to mid/high 20s% by the end of 2028.

This would be done via M&A, JVs, capex, or a combo.

XPEL just annouced strong Q1 results, and the CF statement contained a clue:

Capex increased to $9.7mm in Q1, up from $4mm in the whole of 2025.

It seems the manufacturing build out has begun.

Let's see on the earnings call at 11am.

If you're interested in learning more, I recently published an article going through the economics of the build-out, and the growth opportunity for XPEL (link in the next comment).