Much of the popular investor narrative around AI presupposes that there aren't diminishing returns to LLM development.

If there are diminishing returns, then the economic advantage of having a 6-month lead for frontier models will shrink over time.

This would be a huge problem for the frontier labs. People who use LLMs don't interact with other users of the LLM, so being the first to have a large installed base of users is unlikely to produce the sort of natural monopolies one sees in, say, social media.

What you end up with is a fairly competitive environment for AI systems. Great for the consumer, but not so great for the Open AI or Anthropic.

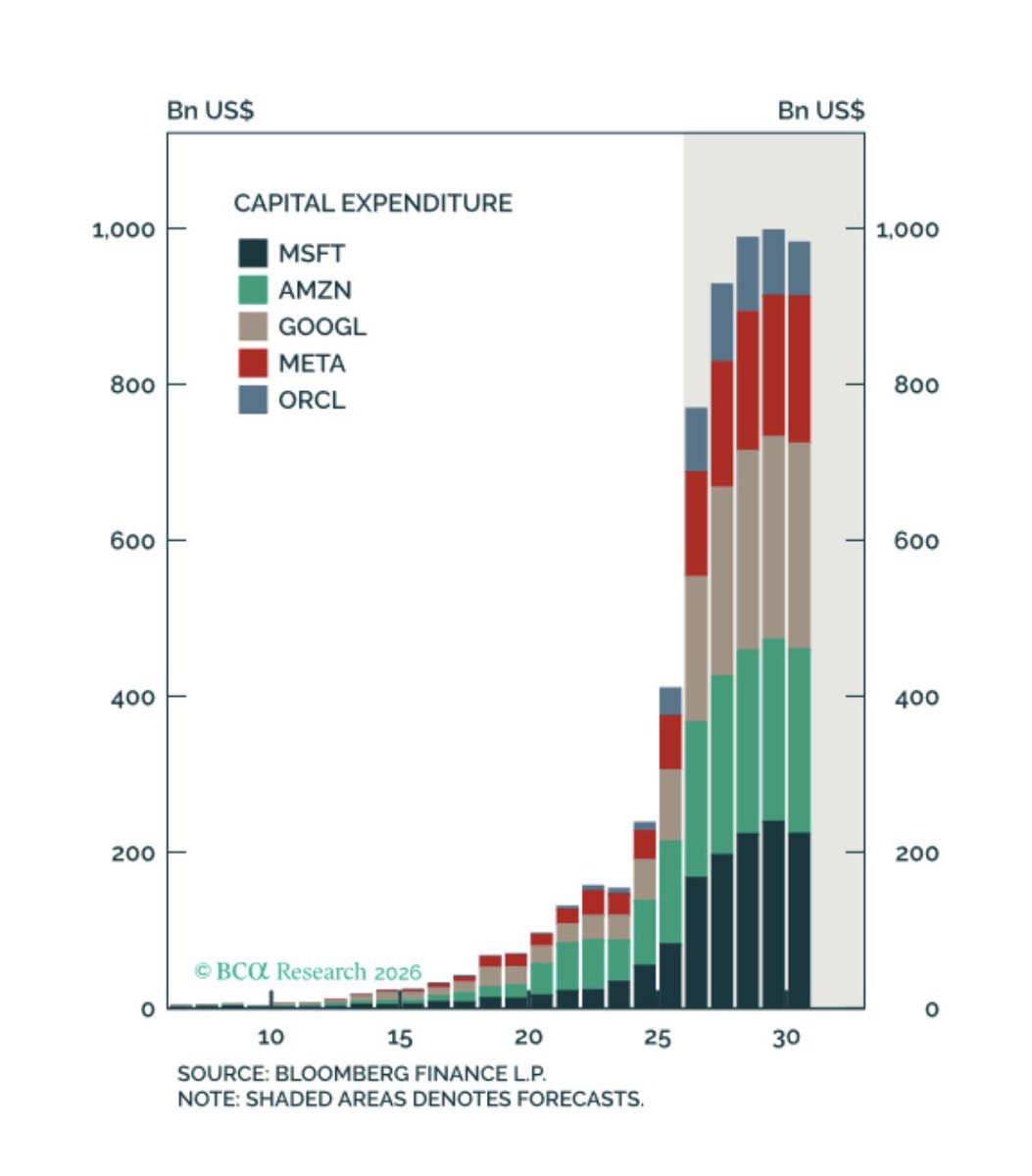

Cross-ownership among AI companies is artificially inflating profits. The “other income” category was equal to 40% of hyperscaler operating profits in Q1, mainly reflecting mark-to-market gains on their holdings of private companies such as Anthropic and OpenAI.

Hyperscaler free cash flow is expected to fall to nearly zero in 2026 but then surge to $700 billion in 2030 despite $1 trillion in ongoing capital spending. Sure!

A lot of investors take Jevons’ paradox for granted. But up until recently, IT hardware spending was flat-to-down as a share of GDP, even as Moore’s law continued to hold. Why? Because prices usually fell more quickly than the volume of sales rose.

Looks like we may finally have a "peace deal" in Iran. I am skeptical it will last very long but will refrain from adding hedges tomorrow. Too much risk of a blow off rally.

Perhaps it is fitting that this happened on the same day as the SpaceX IPO, but my model just sent an “emergency sell” signal. I’m not as bearish as my model, but I will still be increasing hedges Monday morning.

Clients can read the whole note here:

https://t.co/396t84ASUg

I got a lot of flack when I said this before, but I continue to think that model providers will end up being a lot like airlines: Critical for the global economy but highly commoditized, with huge capex requirements and low (and often negative) margins.

@tombuffett1@StockcoachPB It’s part of my process, but not the only source. The model is not particularly good at picking up certain things such as Trump’s policies on trade/war, as well as the impact of AI.

Higher inflation is causing nominal and real retail sales to diverge. The good news is that gasoline prices have fallen about 40 cents from their highs, which should lead to a tamer CPI print in June. The bad news is that the cease-fire is really a “less-fire” and could easily become a “more-fire”.

As the chart below shows, the cost per token is now falling. This suggests that companies are becoming increasingly cost-conscious and are turning to cheaper models for their AI needs.

The Chicago Fed’s early estimate for May retail sales based on big data points to a significant inflation-adjusted decline of 1.3%. Higher oil prices beginning to bite?

And in terms of the most relevant analogy to AI’s impact on the employment and the speed of the impact on us labor share decline, i don’t think it is other GPT (like electricity).

Rather, the comparable will be the globalization wave led by China. As AI (like trade) forces specialization along comparative advantage (in tasks) and essentially reorganized the production process.

Open AI proposes a Public Wealth Fund. No details on whether such fund would be buying OpenAI shares at a $2 trillion valuation, or whether OpenAI would be magnanimously granting free shares to the public. I have my hunch on which one it is.