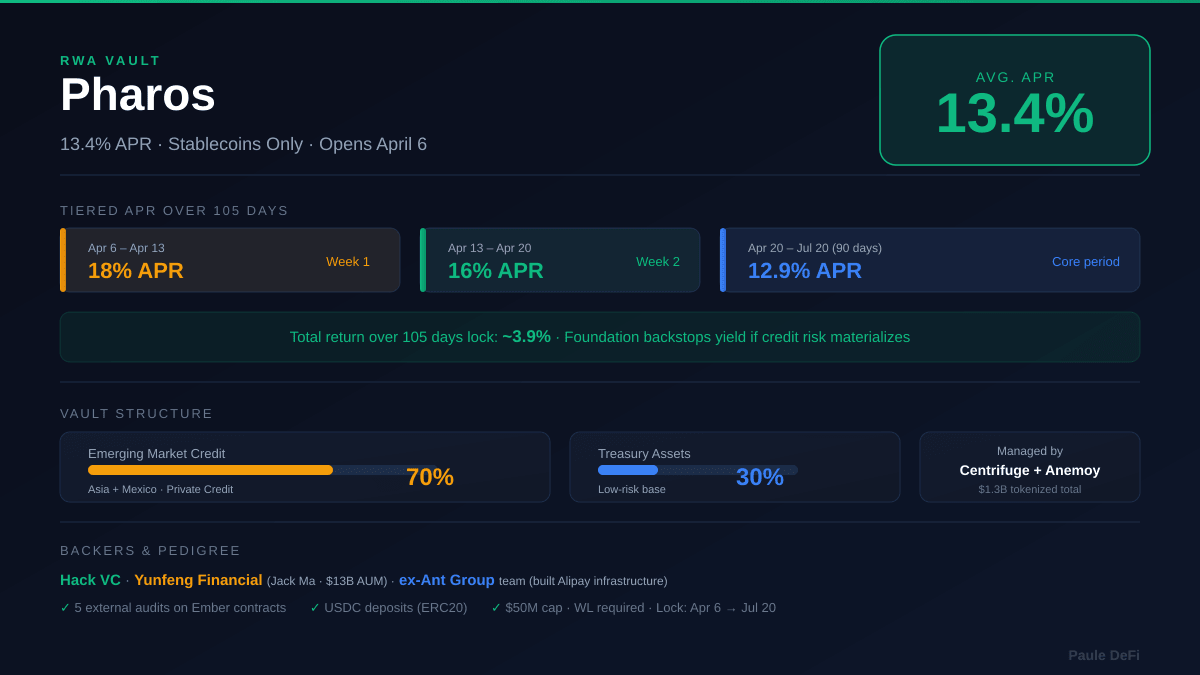

13.4% APR on stablecoins. Opens April 6. Foundation backstops the yield.

This one caught my attention.

Pharos RWA Vault — built by ex-Ant Group / Alipay team, backed by Jack Ma's Yunfeng Financial ($13B AUM) and Hack VC.

The vault structure:

70% — private credit, emerging markets (Asia + Mexico)

30% — low-risk treasury assets

Managed by Centrifuge + Anemoy — they've tokenized $1.3B in assets total.

The yield is tiered:

Apr 6–13 → 18% APR

Apr 13–20 → 16% APR

Apr 20–Jul 20 → 12.9% net APR

Total return over 105 days lock: ~3.9%

Security: 5 external audits on Ember contracts. USDC deposits only (ERC20). $50M cap, WL required.

The backstop clause is interesting — even if underlying credit risk materializes, Foundation guarantees target yield. That's a real downside buffer.

Risks I see:

— Emerging market private credit is illiquid by nature

— 105-day lock with withdrawal window Jun 17–Jul 16

— Foundation backstop is only as good as the Foundation's balance sheet

— New chain, limited track record

My verdict: Better risk/reward than most stable opportunities right now. The tiered APR (18% week 1) rewards early movers. I'm allocating a portion of my idle USDC here.

For those curious — access via Liquidity Land → Ember on Apr 6.

Paule DeFi

BTC whales are selling.

Not "taking profits" — flipping from structural accumulation to distribution.

The 1K–10K BTC cohort (smart money, not exchanges) added +200,000 BTC in 2024.

Now they've shed -188,000 BTC over the past 12 months.

That's a -388,000 BTC swing in behavior. Rolling 365-day trend is declining — this isn't a one-off event.

What it means in practice:

— These wallets don't panic-sell. When they rotate out, it's intentional.

— They accumulated through the bull run. Now they're distributing into it.

— Price has held up. But the foundation is quietly shifting.

I'm not calling a top. But when the cohort that got it right in 2024 starts reversing, I pay attention.

Staying heavy stablecoin until I see accumulation resume.

Source: CryptoQuant

Paule DeFi

30-40% fixed APR. Crude oil. Delta-neutral.

This is the most creative yield setup I've seen this week.

The strategy: Pendle Boros + Hyperliquid + CME May futures

How it works:

1️⃣ Open long on crude oil through https://t.co/eNRisEj96R

2️⃣ Short WTI CME May futures on Hyperliquid

3️⃣ CME May currently trades at ~9% negative implied yield

4️⃣ That basis spread is your yield — Pendle locks it in as fixed rate

Net result: delta-neutral (oil price doesn't matter) + 30-40% APR locked until CME expiry in ~20 days

Why the math works:

WTI CME May is in backwardation

Shorting it = collecting the negative roll yield

Pendle tokenizes that into a fixed rate → you capture it upfront

Numbers:

Fixed APR: ~30-40%

Annualized, 20-day window

Across 3 platforms: Boros, Hyperliquid, Pendle

Risks I'm watching:

https://t.co/eNRisEj96R is new → liquidity risk

Execution across 3 platforms is complex

CME basis can compress if macro volatility spikes

Trump tariffs (April 2nd) = oil could move fast → even delta-neutral has slippage risk today

My take:

I'm already in Pendle (PT-USDG, 5.2% fixed). Adding a small allocation to test Boros mechanics. The fixed-rate primitive applied to commodity basis trades is genuinely novel.

This is where TradFi commodities meet DeFi-native execution.

Drift Protocol exploited. $271M drained from vaults on Solana.

The attacker bought 38,820 ETH ($82.6M) with the stolen funds. Withdrawals are still happening — millions every few minutes.

Drift had $245M TVL before the exploit. That's essentially everything.

This is the largest Solana DeFi exploit to date.

What we know so far:

Funds were drained directly from the vault address. Not a price manipulation, not a flash loan — direct withdrawal from protocol storage.

The attacker is converting to ETH, likely bridging off Solana.

If you had funds on Drift — check your positions immediately.

Another reminder: perp DEX vaults are not savings accounts. Smart contract risk is real, and "battle-tested" protocols still break.

Stablecoins processed $33 trillion in payments in 2025.

Visa: ~$14T. Mastercard: ~$9T. Combined: ~$23T.

Stablecoins: $33T.

The flippening nobody talks about.

But here's the irony:

Market cap: $314B

Earning any yield: ~7%

Sitting idle, earning $0: 93%

$292B in stablecoins is essentially a free loan to issuers like Tether. They earn 4-5% on your USDT. You earn nothing.

The yield infrastructure exists:

Tier 1 (low risk):

→ sGHO — 5.11% APY (Aave native)

→ sUSDS — ~5% APY (Sky/MakerDAO)

→ USDe on Kraken — 4.25% APY

Tier 2 (moderate):

→ PT-srUSDe on Pendle — 3.77% fixed (94 days)

→ Morpho/xStocksFi — 15% (SPYx collateral)

Tier 3 (high risk):

→ ynRWAx loop on Euler — ~80% APY

→ ynRWAx on Equilibria — ~52% APY

$33T in volume proves stablecoins are the killer app.

93% sitting idle proves most holders are still in TradFi mindset.

The yield gap won't last forever.

@jeg6322 Also worth noting: all 80+ wallets trace back to the same Gnosis Safe multisig through a single proxy contract.

Not even trying to hide it. Hub-and-spoke distribution pattern visible to anyone running the trace.

@edgeX_exchange Your airdrop data is on-chain.

80+ fresh wallets. 180M tokens. Single Gnosis Safe source.

Community got <600K tokens across 1,000+ real users.

Where's the transparency report?

@how2onchain 80+ wallets from a single Gnosis Safe multisig → proxy contract → recipients.

Community: <600K tokens across 1,000+ wallets = ~$300K

Team: 180M tokens across 80 fresh wallets = $90M+

300:1 ratio. And they called it an "airdrop."

@jeg6322 The "exactly 14%" is the smoking gun. Airdrop distributions don't naturally land on identical percentages across 26 wallets unless they're controlled by the same entity.

Fresh wallets, funded from Gate and OKX, same timing. Textbook self-dealing.

Update on EdgeX. It's worse than we thought.

Initial reports showed 26 wallets claiming 140M $EDGE. New on-chain analysis reveals the real scale:

80+ fresh wallets. 180M tokens. Over $90M.

All wallets funded from a single Gnosis Safe multisig → proxy contract → 80+ recipients in a hub-and-spoke pattern.

The community's share: less than 600K tokens across thousands of real users.

Ratio: team got 300x more tokens than the entire community combined.

This isn't a gray area. Fresh wallets, same funding source, same timing, same claim percentage. The on-chain evidence is clear.

The perp DEX airdrop model is broken. And EdgeX just proved it.

$EDGE just dropped.

26 wallets claimed 140M tokens — $68M at current price.

The rest of the community? Less than 600K tokens across 1,000+ wallets. That's ~$300K split between the people who actually used the product.

The numbers from on-chain:

→ 26 insider wallets: 3M–8.7M EDGE each

→ Each of the 26 wallets got exactly 14% of their allocation bucket

→ ~8,700 users got less than 100 EDGE each

This isn't a bad airdrop. This is the team airdropping to themselves.

What was your conversion rate? Drop your XP-to-EDGE and Points-to-EDGE numbers below.

Top 5 stablecoin yields earned ~$39M last month. One protocol took almost half.

sUSDS (Sky) — $18.6M/mo

syrupUSDC (Maple) — $6.1M

BUIDL (BlackRock/Securitize) — $5.7M

USYC (Hashnote/Circle) — $5.5M

USDY (Ondo) — $3.2M

Sky dominates with 47% of the top 5 revenue. And this is after the rebrand from MakerDAO — the protocol most people wrote off.

Context: the US just passed the GENIUS Act in the Senate. Stablecoin regulation is coming, and the protocols already generating real yield from T-bills and RWAs are positioned to benefit the most.

The ones earning nothing on-chain will feel it first.

EdgeX committed a crime even before its TGE

Even Backpack didn't do it.

They just did nothing, but f*c*ing EDgEx just ruined everything right before TGE

with the current price of $EDGE, I lost 60% of my invested amount again

$EDGE airdrop results. I demand reallocation. Another scam.

237 EDGE claimed. At $0.52 that's ~$123 for months of farming.

The community voted to merge XP (5%) and Points (25%) allocations — 30% distributed together. Good: XP holders got tokens without waiting. Bad: the per-user allocation came out ~3x lower than expected.

→ ~1 EDGE per 1 XP

→ Expected: ~3 EDGE per 1 XP

→ The math doesn't add up — where did the rest go?

The team appears to have kept a significant portion for themselves.

I demand a transparent breakdown: how many tokens went to XP holders, how many to Points holders, and how many stayed with the team.

If you farmed $EDGE — drop your numbers below. How much per XP? How much per Point?

BlackRock HLEND: 9% of NAV in redemption requests. Only 5% paid out. The other 4% is in queue.

This is the private credit fund DeFi is calling "safe RWA yield."

Private credit funds don't hold liquid assets. They lend to mid-market companies on multi-year maturities — debt you cannot sell in 24 hours. When investors want out, the fund waits for borrowers to repay or finds a secondary buyer at a discount. There is no other mechanism.

HLEND (BlackRock's private credit interval fund):

→ 9% of NAV in redemption requests in Q1 2026

→ Only 5% of NAV actually paid out

→ 4% sitting in queue, waiting for the next redemption window

→ 44% of redemption demand unmet in a single quarter

Cliffwater CCLFX (another major private credit interval fund):

→ 7% of NAV paid out in the same period

Both are "interval funds" — redemptions processed quarterly, not daily. Even BlackRock cannot make illiquid loans liquid on demand. That's not a BlackRock problem. That's what private credit is.

Now the DeFi angle.

Projects are actively tokenizing these exact fund structures as RWA. The pitch: "earn 9-12% yield on institutional private credit, liquid 24/7, fully onchain."

The token wrapper does not change the underlying asset.

When you hold an onchain token backed by HLEND or CCLFX, the collateral is still quarterly-redeemable at best. Tokenization adds a UI layer. It does not add liquidity.

In a stress scenario — broader credit concerns, rising default rates, a DeFi liquidity crunch — the token price could disconnect from NAV. Holders rush to the secondary market. No buyer at par. Token might trade at 92¢, then 88¢, then 85¢. Meanwhile the fund NAV still shows 100 because the underlying loans haven't been marked down yet.

Scale that to a DeFi protocol where users expect same-day withdrawals. You don't get a "slight delay" — you get a depeg event with no floor.

Source: BlackRock HLEND fund filings Q1 2026, Cliffwater CCLFX quarterly reports

The problem is packaging an inherently illiquid instrument as if it behaves like USDC. It doesn't. The token is a wrapper on a queue.

If you're in any RWA protocol with private credit backing — read the underlying fund documents, not the token page. Ask one question: what happens when 10% of depositors want out at the same time?

If the answer involves "quarterly redemption window," you are not holding a liquid position. You are holding a position in a queue with a DeFi frontend on top of it.

Tokenized Treasuries just hit $12.42B TVL.

Up from ~$3.7B in January 2025 — roughly 3.4x in 14 months. (source: https://t.co/HF1Quz5KnZ)

Institutions are moving stablecoins into on-chain T-bills at 3-4% APY instead of leaving them idle. That trend is established.

But there's a next layer forming. And it yields more than 3x the T-bill rate.

It's called PayFi. Payment financing — trade finance, cross-border settlements, merchant receivables. The underlying market: $4.5T/year in commodity trade finance alone.

The protocol I'm watching is Huma Finance.

Here's how it actually works:

Huma's Classic mode pools USDC and deploys it to finance real payment flows — mostly cross-border liquidity for fintechs and financial institutions. Revenue comes from financing fees (6-10 bps/day). Not token emissions. Not points. Actual fees from real capital demand.

Current yield: 10.5% APY in USDC (Classic mode).

The operational layer is Arf Financial — Huma's primary lending partner:

→ $10.96B in on-chain volume processed

→ $5.53B in deployed liquidity

→ Regulated under Swiss VQF

(source: https://t.co/s6qAr2gPXJ)

Backers: Circle, Solana Foundation, Galaxy Digital, Stellar.

Comparison:

• T-bills (BUIDL, ONDO, etc.) → 3-4% APY in stablecoins

• Huma Classic mode → 10.5% APY in stablecoins, same token (USDC)

The yield differential is ~7 percentage points. That's the price the market pays to access DeFi liquidity for real-world payment flows instead of sovereign debt.

Now, the part I'm less enthusiastic about:

Huma also advertises "up to 30% APY" in their Prime mode. That number is not comparable to Classic. Prime combines leveraged positions with HUMA token rewards. Strip the leverage and the token incentives, and you're looking at a very different picture. Marketing a leveraged, token-subsidized yield next to a clean fee-based yield on the same page is misleading, intentionally or not.

Risk profile (my assessment):

Classic mode → MEDIUM. Real yield from real fees, regulated partner, credible backers. Main concern: Huma 2.0 is deployed on Solana, and I have not been able to confirm that the new contracts have undergone a full independent security audit. That's not a dealbreaker, but it's the kind of gap that matters before sizing up a position.

Prime mode → HIGH. Leverage + token rewards = compounding risk vectors. Pass.

My take:

PayFi as a category is legitimate. The yield source is real. Huma has the right architecture and the right partners to be a serious player in this space. At 10.5% vs. 3-4% for T-bills — both in USDC — the risk/reward in Classic mode is interesting.

But I'm not entering until I see a confirmed audit on Huma 2.0 Solana contracts. "Promising but verify first" is where I land.

If the audit comes through, this goes on my active list.

BlackRock HLEND: 9% of NAV in redemption requests. Only 5% paid out. The other 4% is in queue.

This is the private credit fund DeFi is calling "safe RWA yield."

Private credit funds don't hold liquid assets. They lend to mid-market companies on multi-year maturities — debt you cannot sell in 24 hours. When investors want out, the fund waits for borrowers to repay or finds a secondary buyer at a discount. There is no other mechanism.

HLEND (BlackRock's private credit interval fund):

→ 9% of NAV in redemption requests in Q1 2026

→ Only 5% of NAV actually paid out

→ 4% sitting in queue, waiting for the next redemption window

→ 44% of redemption demand unmet in a single quarter

Cliffwater CCLFX (another major private credit interval fund):

→ 7% of NAV paid out in the same period

Both are "interval funds" — redemptions processed quarterly, not daily. Even BlackRock cannot make illiquid loans liquid on demand. That's not a BlackRock problem. That's what private credit is.

Now the DeFi angle.

Projects are actively tokenizing these exact fund structures as RWA. The pitch: "earn 9-12% yield on institutional private credit, liquid 24/7, fully onchain."

The token wrapper does not change the underlying asset.

When you hold an onchain token backed by HLEND or CCLFX, the collateral is still quarterly-redeemable at best. Tokenization adds a UI layer. It does not add liquidity.

In a stress scenario — broader credit concerns, rising default rates, a DeFi liquidity crunch — the token price could disconnect from NAV. Holders rush to the secondary market. No buyer at par. Token might trade at 92¢, then 88¢, then 85¢. Meanwhile the fund NAV still shows 100 because the underlying loans haven't been marked down yet.

Scale that to a DeFi protocol where users expect same-day withdrawals. You don't get a "slight delay" — you get a depeg event with no floor.

Source: BlackRock HLEND fund filings Q1 2026, Cliffwater CCLFX quarterly reports

The problem is packaging an inherently illiquid instrument as if it behaves like USDC. It doesn't. The token is a wrapper on a queue.

If you're in any RWA protocol with private credit backing — read the underlying fund documents, not the token page. Ask one question: what happens when 10% of depositors want out at the same time?

If the answer involves "quarterly redemption window," you are not holding a liquid position. You are holding a position in a queue with a DeFi frontend on top of it.

Ethereum's RWA market ($21.75B TVL) just surpassed all of Solana DeFi combined ($6.78B).

Real-world assets are becoming the 3rd largest DeFi category on Ethereum — bigger than most entire chains.

The narrative isn't coming. It's already here.

The Resolv hack scared $600M out of Fluid.

That money had to go somewhere. And it left behind something interesting: stablecoin lending rates on Fluid are now 6–10% APR — higher than T-Bills.

Risk-off for some. Open window for others.

Capital is patient. It will flow back when the dust settles. The question is whether you're already positioned when it does.