1/ Collateral Risk Assessment on @stakewise_io osETH

An new in-depth risk assessment has been completed with a detailed analysis of various risk factors.

Let's dive in👇:

https://t.co/OEK1Dn9NfD

This week we published an addendum to our collateral risk report on @OriginProtocol $wOETH from 12/23. Since then, OETH has transitioned from an LST-index token to an LST with native staking.

Read the full addendum here and summary below:

https://t.co/BsoFekf820

1/8

osETH Risk Report🌈

The @PrismaRisk is delivering quality work again with their latest report on @stakewise_io osETH!

Stay tuned to the governance forum in the coming days...👀

8/ We believe that osETH is a well rounded liquid staking token that is mature enough to be onboarded as collateral, pending the availability of a Chainlink price feed or the study of other viable strategies.

1/ Collateral Risk Assessment on @stakewise_io osETH

An new in-depth risk assessment has been completed with a detailed analysis of various risk factors.

Let's dive in👇:

https://t.co/OEK1Dn9NfD

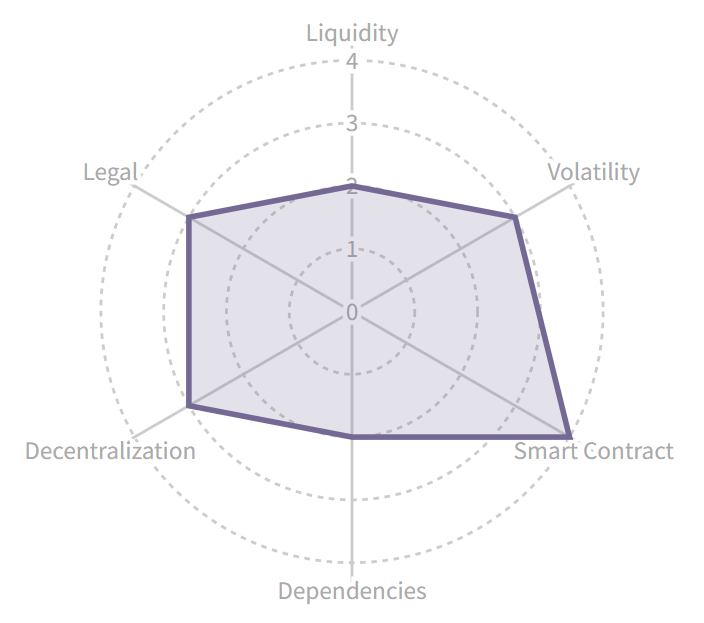

7/ The StakeWise V3 protocol is fairly decentralized and permissionless, with limited control from the StakeWise team over deployed contracts, and no control over vault contracts.

A 4/7 multisig is the owner of all but the vault contracts. Signers are known public entities.

6/ In less than a year, ETHx has grown its market share, experiencing significant user growth and DeFi utility has been added, Previous concerns are less significant, ETHx remaining relatively stable in its yield and peg.

While conservative, onboarding should be considered.

1/ Addendum to @staderlabs ETHx Collateral Risk Assessment🌈

The following addendum references the previous assessment of ETHx published on December 12, 2023. It serves to offer additional context and updates that have emerged since.

Let's dive in:

https://t.co/JH9HuXyQ1g

5/ One of the most important update is that an ETHx/ETH Chainlink price feed now exists, but with limited historical data.

The introduction of a Chainlink price feed presents a tangible improvement although the ETHx price feed is currently less than optimal.

8/ Despite its growth in recent months, users should exercise caution when dealing with ezETH, particularly as a collateral.

Once the EL and Renzo points program concludes or speculation subsides, ezETH may potentially face rapid exit demand that puts further pressure on the peg.

3/ A predominant share of ezETH is currently allocated within Pendle, leaving a mere approximate 4% of the token supply in DEXes.

In this context, ezETH may face significant challenges particularly during market stress periods.

7/ While the decentralization approach mirroring that of Lido seems practical at the outset, the lack of a publicly available strategy raises concerns about the commitment to diversification.

A governance token is not yet introduced and details on future distribution as well.