A True SocialFi Experience

Scroll, engage & get rewards straight in your wallet.

@PulsarFren send 60 SEI to 200 reactions on sei

@PulsarStarknet send 90 STRK to 200 reactions

@PulsarMvX send 1 EGLD to 200 reactions

Learn how below 🧵👇

Every summer, millions of people move more money in a weekend than some towns move in a year.

And it all has to feel effortless.

Behind every drink, ticket, top-up, check-in, and vendor payout is a temporary financial system expected to work like a permanent one.

That’s the standard festivals create. And it’s why, through Rhuna, we’re powering the financial & operating infrastructure for live entertainment.

Money carries more than value.

It carries people’s time, choices, plans, pressure, and freedom.

So the experience around it should help people feel a little more in control of what comes next.

Less weight to carry. More room to move.

The next step for stablecoins is accessibility.

With WCP, Pulsar users will be able to spend directly from their Pulsar account, across wallets and merchants worldwide.

A fintech experience, abstracting the settlement through @privy_io & @WalletConnect.

This week, the Pulsar Money team is heading to several events across EU & US.

From Paris to New York, we’ll be on the ground talking about what comes next for money movement, stablecoins, and the infra needed to make the next generation of fintech usable in everyday life.

new generation of fintech

the Revolut & Wise generation was incredible. they disrupted a conservative market ruled by dinosaurs by making money movement feel natural. better onboarding, better FX, cleaner cards, faster notifications, a nicer app on top of a very old stack

but the next wave is different because the stack itself has completely changed:

→ stablecoins make settlement global and 24/7

→ self-custody lets the account belong to the user instead of the institution

→ bank rails and cards can sit at the edges of a stablecoin-native balance

→ DeFi protocols can sit underneath the account for swaps, yield, trading and credit

→ agents can start acting on clear rules and limits instead of leaving the user to manually move money between 5 products

the old fintech product was: take the bank, make it mobile

the new fintech product is: rebuild the financial account around money that moves, earns, settles and can be routed

the line I keep coming back to is:

→ everyone earns on your money. except you

banks earn on idle balances. card networks earn on every swipe. FX providers earn on every border. platforms earn on your deposits, transactions and data. the user is usually the last person to benefit from their own financial activity

that's why the next generation of fintech that wins will be the one that inverts that

your money should work for you first. it should earn while it waits, move globally when needed, stay under your control, and connect to the best financial infrastructure without forcing you to become a DeFi power user

Pulsar is our view on the consumer side of this

→ a stablecoin-native money app where your balance can spend, send, earn and eventually route itself more intelligently, while still feeling like a normal everyday app

and it all comes down to executing on that vision with surgical precision, because make no mistake, average consumers will accept nothing less

yesterday’s post about credit-backed stablecoin cards brought up a lot of good conversations, especially around one question:

if the first wave of these products was debit-style, what does credit actually change?

with most stablecoin debit cards today, the payment flow is still very similar to a normal fiat account. you hold a balance and you spend from that balance

the infra may be different & the UX may be better, but the basic function is still the same.

credit, however, introduces a second layer:

instead of every transaction being a direct deduction from the balance, the account can start deciding how to use the user’s financial position more intelligently

that’s where the product starts to become more powerful because onchain credit can make a user’s money more flexible

the same $100 can sit in the account, back credit, earn yield, and still support everyday payments without being moved/sold

that matters in 3 practical ways:

first, it makes the account more capital-efficient. the user does not have to interrupt their position every time they spend. the card becomes access to liquidity

second, repayment can become programmable. incoming stablecoin flows, idle balances, or yield can reduce the credit line automatically based on rules the user sets. the experience can still feel like a normal card, but the account underneath can manage repayment much more intelligently than a monthly statement cycle

third, risk can be handled continuously. live LTVs, dynamic limits, top-up rules, repayment triggers, and alerts can sit inside the account instead of being exposed as a DeFi dashboard the user has to manage manually

for this to work, I think there are 2 underestimated challenges:

1/ UX - making DeFi great again by making it understandable to a regular consumer. both in terms of displaying info & managing account settings

2/ account logic - when to spend from balance, when to borrow, when to repay, when to route yield, when to top up collateral (and so on) - these sound like small product decisions, but they actually are the product. the flywheel works if all pieces are aligned

however, I think we're in for an exciting ride and credit on crypto infra can make everyone's dollars more useful once they are truly here

NYC has some of the best coffee shops

will be there in a few days, excited to meet friends and have good chats over some exceptional coffee ☕

planning to try a few from @swang_co’s list below

one thing after watching stablecoin cards lately

in the US, credit is the default. people "put it on the card" and the card almost always means credit. rewards, points, credit score, the whole social contract of how you spend lives there.

in most of europe and a lot of asia, the opposite. the card is debit. you spend what you have. credit is a separate product you opt into.

and i think this is what's actually shaping stablecoin cards right now

because the first wave of stablecoin cards is basically the european version. debit-style, spend crypto through a card. you swipe, your balance drops, you sold an asset to buy a coffee. useful, but it's the smaller version of the product

the next wave is the american version. credit attached to the account. you don't sell when you spend, you borrow against what you hold.

onchain, that architecture can actually be cleaner than the legacy version

collateral is liquid, transparent, programmable and composable. credit lines can sit behind the user experience, while settlement still happens in the format merchants already understand

this is why infra like @sprinter_ux is interesting

one credit line, collateral across chains, USDC drawn to a receiver address. for a card program, that receiver can simply be the settlement layer. user taps, USDC settles, the credit line sits behind the experience, and the user never has to think about chains

@Morpho matters for the same reason

not as the card layer, but as part of the credit and yield layer underneath the account. if stablecoin apps become real financial accounts, they need lending markets, curated vaults and idle-balance yield underneath them

so the cards are the interface people already understand, while the account behind the card is the actual product.

the goal is to make that feel normal to use, just like traditional credit accounts.

of course, still real work to do on risk, LTVs, liquidations, refunds, tax, compliance, chargebacks, but the direction is pretty clear;

and that's a big part of what we’re building at @PulsarMoneyApp

looking deeply in this space so let me know if you have any other ideas and views on these infra protocols we should take a close look at

Leaderboard rewards are now live on EthraShip Portal!

🔹 1,500 $USDC prize pool.

🔹 https://t.co/ERKdXJjvIt

Complete tasks, invite friends, and reach Top 10 to qualify for rewards.

Neobanks & payments infra are becoming one of the most important conversations in fintech.

Next Tuesday, we’re hosting an X Space with @xMoney_com to talk about what next-gen of financial products need to get right.

Set a reminder 👇

https://t.co/5CqbAkNGyh

Ready for Pulsar coffee meet-ups in the US?

This summer, we’ll be hosting open spaces to talk fintech, AI, and what’s next - with close friends and new ones. ☕️

Introducing Rhuna.

The financial & operating infrastructure for live entertainment.

A single white-label stack for payments, ticketing, access control, data, rewards, and credit.

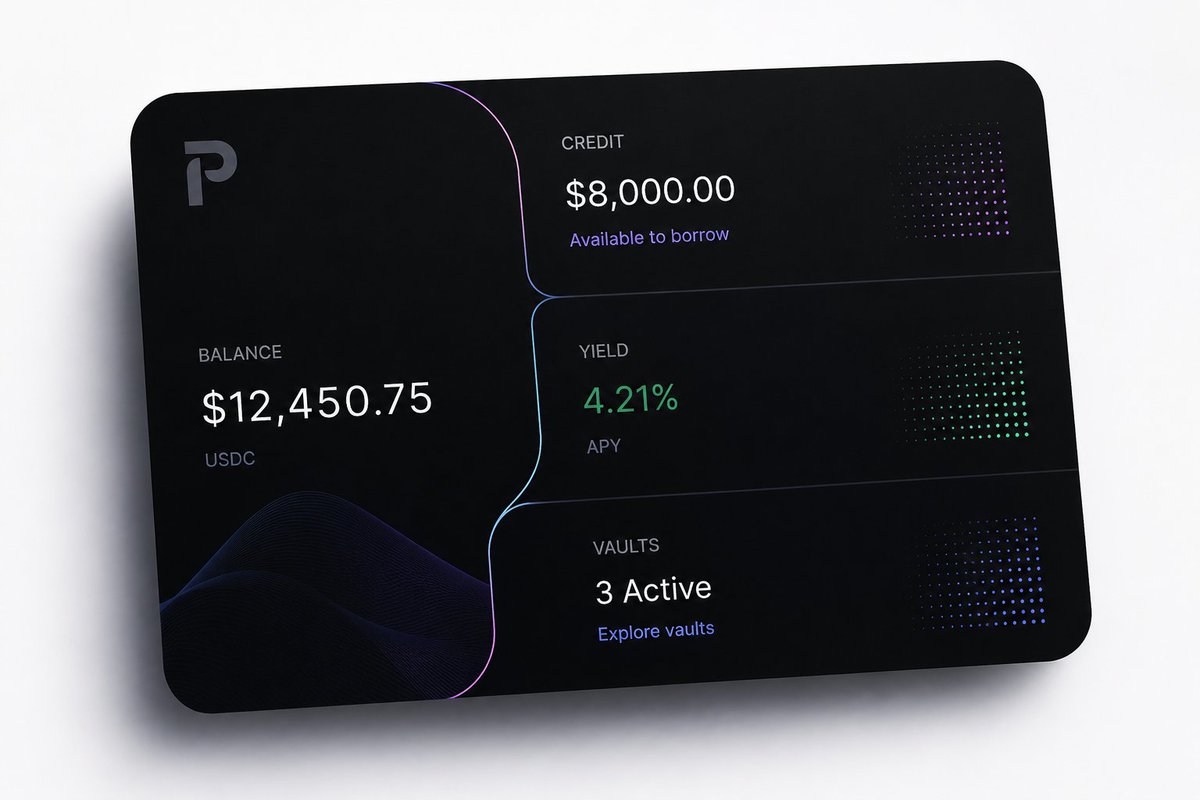

14,416 people have already joined the Pulsar Money waitlist!

For a smarter way to move, spend, earn, and manage money across fiat, crypto, and everything in between.

Get early access ↓

The first Ethra Portal standings are taking shape. 📊

Early participants are already earning points through referrals, activity, and ecosystem engagement.

The leaderboard is live, and this is only the beginning. Join below! 👇

World’s first protocol for tokenized maritime assets, using Pulsar’s whitelabel infrastructure.

Discover @EthraShip, an UAE-based company built for access to maritime RWAs, backed by real operators with a live fleet.

Real-world markets moving onchain. 🚢