Portfolio Update May 17, 2025

I genuinely think I've found a stock that can appreciate 50%+ over the next 6-12 months.

My newest holding Fiserv is a VERY boring payments company growing >15% and trading at around 16x forward earnings. It has quite a complex business model spanning 6 segments.

General Points:

The bulk of the thesis relies on Clover which is their POS system similar to $XYZ's Square Terminals or $TOST's Toast system. This segment of the business although only about 15% of revenues makes up for more than half of the incremental growth –– naturally it's the centre of attention for investors.

What's important to note here, is Clover in of itself grows by pulling on 3 levers as highlighted by the CFO.

- Sell more hardware

- Volume growth (more payments)

- Sell more value-added services to their installed based / get installed based to buy value-added services to begin with (24% penetration)

The mix of these 3 levers results in 30% revenue growth for Clover. Management has guided for $3.5B revenue in 2025 and $4.5B in 2026 (a negligible de-acceleration to 29% and 28% growth).

Elephent in the room:

The stock is down 30% from the all time highs in February purely off the back of a temporary 1-2 quarter issue as outlined by the CFO and this issue is more financial engineering than material problems for the company on a going forward basis (will explain in a video later on). If you're curious I recommend you listen to the CFO's recent appearance at the 53rd JPMorgan Global Tech Conference.

Fundamentals :

The company trades at around 16x forward EPS and 19x EV/EBIT which is one of the lowest valuations this decade. Revenue growth company wide should be in the low teens (primarily driven by 30% growth in Clover)

And by that line of thinking, EPS growth should be in the mid to high teens range primarily driven by a consistent 5-7% buyback as well as some margin expansion –– gives me $BKNG vibes honestly.

Moat & Segments:

They have a leading 40% market share in the core banking solutions segment within the US. This segment encompasses approximately half of the revenues and has 99%+ client retention. The catch is it's only growing at 6% organically.

I think the retention rate speaks for itself in terms of how impossible the switching costs are for their bank customers. Naturally, this segment is the cash-cow of the business.

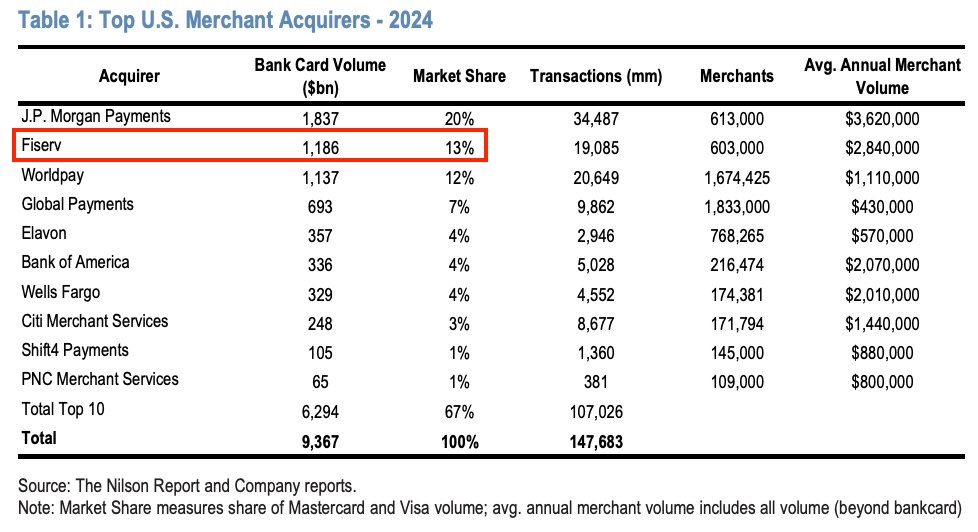

They also are the #2 player in the Merchant Acquirer space behind JPMorgan. They acquired First Data in 2019 to get this position. This segment of their business is the second fastest growing part of the company at around 13% organic revenue growth.

Again, generally a "wide-moat" segment because of the switching costs but it should be mentioned there are newcomers like $ADYEN that have taken a lot of incremental market share almost exclusively with e-commerce.

But I would assume, this segment can continue to growth along-side the industry's volume growth given how entrenched they are and because their profit pools are different from players like Adyen or Stripe.

Alas, Fiserv also operates the 3rd largest debit rails behind Mastercard and Visa. This segment is roughly 4% of revenues and is in decline. Not central to my thesis at all and frankly I wouldn't mind if they sold it off the P.E or something –– kind of how I treat Google's Network business. Meh.

Activity:

I Sold Mastercard $MA in 2 equal tranches at $580 and $582 on Thursday and Friday to buy Fiserv $FI at a $162.59 cost basis ( $158 then $167 ).

Now, Mastercard is a FANTASTIC business don't get me wrong. I literally made a video calling it a "never-sell" stock (hypocritical considering I just sold LOL).

But, I think the way my investment strategy has shifted, I have taken some parts of the Bill Ackman style, which I would summarize as:

'Buy and hold STRONG moat companies with solid growth prospects. If things change, or if you have drastically better opportunities feel free to sell and replace'

So, when I get the same growth, same industry, with half the business being just as wide-moat (core banking). Then, most the growth is coming from a narrower moat segment ( $MA VAS vs. $FI Clover ), at HALF THE VALUATION. I'm gonna bite.

If at some point down the line the valuation disconnect narrows, for eg: 30 PE vs 25 PE. Id be more inclined to switch back. I think the idea that 'you must buy and hold forever' is a bit silly. If you see clear evidence of a better opportunity at a better price and the moat isn't too much of a sacrifice... why the hell not?

Granted, that does't mean jump at every opportunity under the sun. But things that I'm comfortable with and can understand. At the end of the day, I'm trying to maximize my own returns.

And I strongly believe given the historically low valuation, $FI has MASSIVE upside in the event of a multiple re-rating in the next call it 6-12 months. My investment isn't hinging on that, even if the multiple stays at 16x that means more buybacks = bigger EPS boost and thus the stock will appreciate even more from the boosted EPS. But we'll see.

All in all, next to no downside IMO and something like 50%+ upside if it were to re-rate to 25x PE. I will re-evaluate if I'm going to hold or swap if and when that happens.

All the best, do your own due diligence. Video out soon. Cheers, NFS

FinChat is the lead sponsor of this year's Ben Graham European Value Investing Conference in Lisbon this October!

We're giving away a free ticket (worth $400€) if you reply with *any* FinChat chart from the platform for the next 48 hours.

The S&P has more than doubled the performance of $KO shares since Buffett said this ( 600% vs 270% )

I don’t think those buybacks at 40 PE were that accretive after all. Same could likely be said about $AAPL buybacks at 40 PE

ServiceNow at 18x sales isn’t cheap...

But consider:

- 20% revenue growth

- Leader in ITSM & ITOM

- 98% retention, used by 90% of the Fortune 500

That kind of quality deserves a premium, no? $NOW

Intuit's revenue has re-accelerated nicely over the past 8 quarters.

Key growth drivers:

- Mailchimp: +18% YoY

- QuickBooks Online: +21% YoY

- Credit Karma: +31% YoY

Stock up 22.5% over the past month $INTU