@SSage57465@Funmentalist Hey stocksage.

The expectation is (as well as IREN's) is that all of Prince George (50), Horizon 1-4, 50MW at Childress, and 80MW at Mackenzie be operational and billing by the end of 2025.

I believe they're on track. The individual site unit economics are below.

Yes!

Keep up man! You're spam posting about IREN without actually knowing the fundamentals.

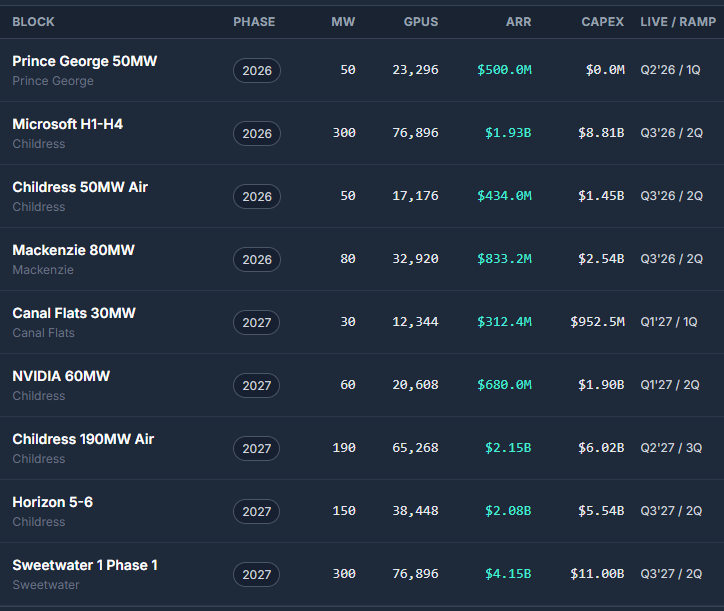

2026 roadmap

Prince George (50MW)

Horizon 1-4 (300MW)

Childress 50 Air (50MW)

Mackenzie (80MW)

2027 roadmap

Canal Flats (30MW)

NVIDIA 60 (60MW)

Childress 190 Air (190MW)

Horizon 5-6 (150MW)

Sweetwater1 Phase1 (300MW)

The 3.7B ARR target only includes the 2026 roadmap. Nothing else.

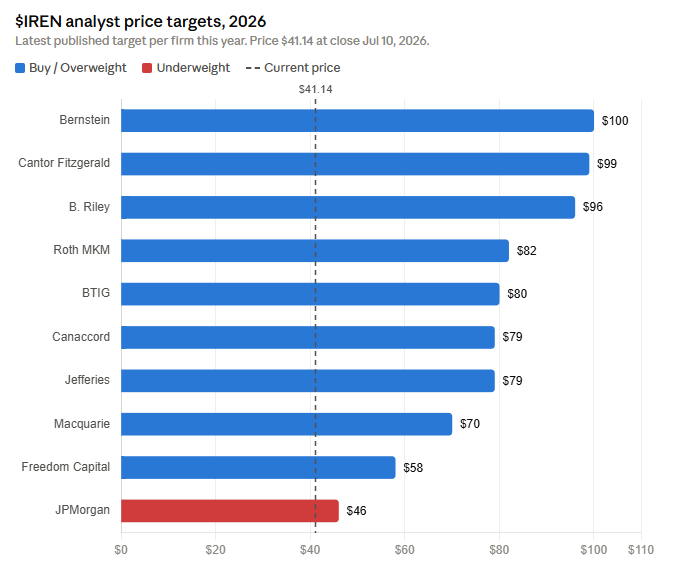

$IREN is down almost 50% from its all time highs, yet analysts keep raising their price targets.

Ten firms, average target around $81, roughly double the current price.

> Cantor just went from $77 to $99.

> B. Riley from $88 to $96.

> Bernstein is holding at $100.

JPMorgan (the biggest bear on Wallstreet) is the only sell rating on the street, and even their $46 target is above where the stock trades today.

Buy the fear?

@FransBakker9812 Frans, thanks as always. On a different topic, Anthropic is looking for 1.5 GW DC in Australia by 2027. Since IREN's Bundey site is scheduled for energization in 2028, do you think there's any realistic chance they could accelerate that timeline into 2027 and secure a contract ?

골드만삭스 "AI 인프라 투자, 2031년까지 7조6000억달러 전망"

——————————————————

골드만삭스가 2026년부터 2031년까지 글로벌 인공지능 인프라에 약 7조6000억달러의 자본이 투입될 것으로 전망했습니다.

골드만삭스의 기본 시나리오에 따르면 AI 관련 자본지출은 컴퓨팅 장비, 데이터센터, 전력 인프라를 중심으로 매년 빠르게 확대될 것으로 예상됩니다.

연간 투자 규모는 2026년 7650억달러에서 2027년 1조110억달러로 증가하며 처음으로 1조달러를 넘어설 전망입니다.

이후 2028년 1조2200억달러, 2029년 1조3920억달러, 2030년 1조5790억달러로 늘어난 뒤 2031년에는 1조6360억달러에 이를 것으로 추산됐습니다.

2026년부터 2031년까지 연평균 성장률은 약 16%에 달합니다.

다만 투자 증가율은 초기 급증 이후 점차 둔화될 것으로 예상돼, 2030년대 초반에는 AI 인프라 투자가 폭발적인 확장 국면에서 안정적인 성장 국면으로 전환될 가능성을 시사합니다.

——————————————————

전체 투자금의 약 3분의 2, 컴퓨팅에 집중

골드만삭스는 향후 AI 인프라 투자에서 가장 큰 비중을 차지하는 분야로 컴퓨팅을 지목했습니다.

컴퓨팅 부문에는 GPU와 AI 가속기, 서버, 네트워크 장비, 메모리와 관련 부품 등이 포함됩니다.

컴퓨팅 관련 투자액은 2026년 4940억달러에서 2027년 6610억달러, 2028년 8080억달러, 2029년 9340억달러로 늘어날 전망입니다.

2030년에는 1조730억달러로 처음 1조달러를 넘어선 뒤 2031년에는 1조1270억달러에 이를 것으로 예상됩니다.

6년간 컴퓨팅 부문에 투입되는 누적 자본은 약 5조1000억달러로, 전체 AI 인프라 투자액의 약 67%를 차지합니다.

이는 향후 AI 자본지출 사이클의 가장 큰 수혜가 반도체, 서버, 고속 네트워크, HBM 메모리와 관련 부품에 집중될 가능성이 높다는 의미입니다.

특히 AI 모델 학습뿐 아니라 추론 서비스가 확산될수록 지속적으로 더 많은 연산 자원이 필요하기 때문에, 컴퓨팅 투자 수요는 장기간 이어질 가능성이 큽니다.

——————————————————

데이터센터 투자도 2배 가까이 확대

골드만삭스는 데이터센터 건설과 설비 투자 역시 꾸준히 증가할 것으로 전망했습니다.

데이터센터 관련 자본지출은 2026년 2320억���러에서 2027년 3000억달러, 2028년 3530억달러, 2029년 3930억달러로 확대될 것으로 추산됐습니다.

2030년과 2031년에는 각각 4330억달러와 4360억달러에 이를 전망입니다.

6년간 누적 데이터센터 투자액은 약 2조1470억달러로, 전체 투자액의 약 28%를 차지합니다.

다만 2030년 이후 데이터센터 투자 증가 폭이 크게 둔화된다는 점은 주목할 필요가 있습니다.

이는 대규모 데이터센터 건설이 2020년대 후반에 집중된 뒤, 이후에는 신규 부지 개발보다 기존 시설의 가동률 개선과 장비 교체가 더 중요한 변수로 부상할 가능성을 보여줍니다.

——————————————————

전력 투자는 규모보다 전략적 중요성이 더 커

전력 인프라 부문은 전체 투자액에서 차지하는 비중은 상대적으로 작지만, AI 데이터센터 확장의 핵심 제약 요인으로 평가됩니다.

골드만삭스는 전력 관련 투자액이 2026년 390억달러에서 2027년 500억달러, 2028년 590억달러, 2029년 650억달러로 증가할 것으로 전망했습니다.

2030년에는 720억달러, 2031년에는 730억달러까지 확대될 것으로 예상됩니다.

6년간 누적 전력 투자는 약 3580억달러로, 전체 AI 인프라 투자액의 약 5% 수준입니다.

그러나 이 수치에는 발전소뿐 아니라 송배전망, 변압기, 배전 설비, 비상전원과 에너지 저장장치 등 광범위한 인프라 수요가 포함될 수 있습니다.

AI 데이터센터는 막대한 전력을 지속적으로 소비하기 때문에 전력망 연결 지연과 발전 용량 부족이 실제 투자 집행 속도를 결정하는 병목으로 작용할 가능성이 큽니다.

——————————————————

AI 경쟁, 모델에서 산업 인프라 경쟁으로 이동

골드만삭스의 이번 전망은 AI 산업의 경쟁 무대가 단순한 소프트웨어와 모델 개발을 넘어 대규모 산업 인프라 투자로 이동하고 있음을 보여줍니다.

AI ��업과 클라우드 사업자는 더 높은 성능의 모델을 개발하는 것뿐 아니라 이를 안정적으로 운영할 수 있는 반도체, 데이터센터와 전력 공급망을 동시에 확보해야 합니다.

결국 향후 AI 시장의 경쟁력은 알고리즘 성능뿐 아니라 자본 조달 능력, 장비 확보, 전력 조달과 데이터센터 건설 속도에 의해 결정될 가능성이 높습니다.

누적 투자액의 대부분이 컴퓨팅 부문에 집중된다는 점을 고려하면 엔비디아와 AMD를 비롯한 AI 가속기 기업뿐 아니라 HBM 메모리, 광통신, 네트워크 스위치, 서버와 냉각 시스템 업체에도 구조적인 수요가 이어질 수 있습니다.

데이터센터와 전력 투자 확대는 건설, 발전, 변압기, 가스터빈, 원자력과 에너지 저장장치 산업으로 수혜 범위를 넓힐 가능성이 있습니다.

다만 골드만삭스가 제시한 수치는 기본 시나리오에 따른 추정치인 만큼 실제 ��자 규모는 AI 서비스의 수익화 속도, 자금 조달 비용, 전력 공급 여건, 규제와 인허가 진행 상황에 따라 달라질 수 있습니다.

그럼에도 2031년까지 7조6000억달러에 이르는 자본 투입 전망은 AI가 단일 기술 사이클을 넘어 반도체와 전력, 건설과 자본시장을 동시에 움직이는 장기 산업 투자 사이클로 진입하고 있음을 보여줍니다.

$IREN

Are You Positioned for What's Coming?!

I’ve said it before: IREN’s Annual Recurring Revenue (ARR) is fundamentally simple. It is a predictable pipeline of GPU batch purchases and their associated revenue streams layered linearly on top of one another.

2026 ARR Roadmap

🔹Prince George: 23,296 GPUs → $500M ARR

🔹MSFT H1–H4: 76,896 GPUs → $1.933B ARR

🔹Mackenzie: 32,290 GPUs → $833.2M ARR

🔹Childress 50: 17,176 GPUs → $434M ARR

EOY 2026 Target: 150K+ GPUs → $3.7B ARR

2027 ARR Roadmap

The playbook for 2027 is identical: stacking successive hardware batches and compounding the revenue.

🔹Canal Flats: 12,344 GPUs → $312.4M ARR

🔹NVIDIA 60MW: 20,608 GPUs→ $680M ARR

🔹Childress 190 Air: 65,268 GPUs → $2.15B ARR

🔹Horizon 5-6: 38,448 GPUs → $2.08B ARR

🔹Sweetwater P1: 76,896 GPUs → $4.15B ARR

EOY 2027 Total - 363,852 GPUs → $13.07B ARR

To project these numbers, my model relies on some key assumptions:

1. Canal Flats utilizes the same unit economics as Mackenzie.

2. Childress 190MW Air utilizes the same unit economics as NVIDIA 60MW.

3. Horizon 5–6 and Sweetwater 1 (Phase 1) will debut VR200s.

I model the hourly rate for Vera Rubin chips at a significantly higher $6.16/hr. This premium accounts for both higher baseline Capex costs for those GPUs (significantly higher) and IREN’s ability to capture a small portion of the massive performance multipliers inherent to the Rubin architecture, and the marked improvement in GPU hourly rates over the last 9 months.

Buckle-up buttercup.

🚀🚀🚀🚀

(Imagine selling right before this ramp. YFA 🤦♂️)

$IREN 핵심 내용

Agrippa_Inv 글을 요약해봤습니다.

항상 좋은 글 감사합니다.

1. 왜 계약 체결이 느린가

$NBIS, $CRWV 대비 대형 계약(수백 MW급) 체결이 느린 이유는 수요 부족이 아니라 전략적 선택.

지금 당장 온라인 가능한 용량은 프리미엄을 받을 수 있는 반면,

6~12개월 뒤 가동 예정 용량을 미리 파는 건 가격 할인 + 고객 풀 축소(하이퍼스케일러 위주로만 팔리게 됨)를 의미함.

2. 고객 선별 전략

신용도뿐 아니라 스케일업 가능성까지 까다롭게 심사 중.

Mirantis 인수 완료 후 고마진 매니지드 클라우드 서비스 관련 LOI/고객사 확보 다수 확보했다는 정황.

3. Sweetwater 캠퍼스 지연 이유

VR200(Rubin) 세대용으로 배정되어 있어 Rubin 공급이 본격화되는 연말~내년 초까지 대기 중.

동시에 Childress(Horizon) 빌드에서 얻은 교훈(비용/속도 효율화)을 Sweetwater에 온전히 적용하려는 의도로 해석됨

“느리게 시작해서 지수적으로 확장”하는 패턴은 채굴 시절부터 이어진 $IREN의 특징.

4. 단기 캐탈리스트

3월에 확보한 B300 5만 대(Mackenzie ~33k, Childress ~17k)는 연말까지 완전 계약/설치 전망.

8월 실적 발표 즈음 계약 발표 가능성 높음 — GPU 임대료 상승 감안 시 연말 ARR 가이던스($3.7B)가 $3.9~4.1B로 상향될 가능성 언급.

5. 2027 파이프라인

Childress 190MW, Canal Flats 30MW, Horizon 5-6 150MW, Sweetwater 1 300MW 등 추가 계약 여지.

하이퍼스케일러/프론티어랩 대상으로 연내 일부 사전계약 가능성 존재.

✅ 총정리

장기 투자 관점에서 전략에 공감함

그러나 경영진의 로드맵 공개 수준이 다소 폐쇄적인 것은 아쉬움

Reflecting on $IREN

Over the last couple of days I spoke with multiple people in close contact with $IREN's management team, including investors who attended the RAISE Summit this week.

Given the insights I've gathered, I think it's an appropriate time to reflect on $IREN and share my latest thoughts.

It's no secret that $IREN has been somewhat slow on the commercial side, at least relative to the likes of $NBIS and $CRWV. I for one thought we'd have seen a Sweetwater deal by now, let alone substantial parts of the remaining Childress capacity pre-contracted.

So what's stopping $IREN from signing these multi-hundred MW deals?

In short, nothing is really "stopping" them. It comes down more to a few factors shaping their decision to hold off where other cloud providers perhaps wouldn't.

Based on management's comments both on and off camera, I can confidently say demand truly isn't the issue. Cloud capacity in this market is sparse and supply can't keep up. In fact, I've heard $IREN could easily sell out 100% of its 2027 capacity today if it wanted to.

The catch is that selling capacity which won't come online for another 6, 9, or 12 months yields significantly less than capacity arriving sooner. Customers want capacity today, and they're willing to pay a substantial premium for it.

So while selling far into the future might prop up the stock, commercially it may not be the most prudent strategy in this environment. That dynamic can obviously shift over time, but given how far supply sits behind demand, it won't change overnight, and as it stands, holding off as long as possible yields better long-term returns.

Not only do returns shrink the further out you pre-contract, but the available buyer pool shrinks with it. Selling capacity well into the future means gatekeeping much of the smaller, higher-margin clientele while mostly attracting the lower-paying hyperscalers.

As we know, $IREN is increasingly moving up the stack, effectively cutting out the middle-man that hyperscalers represent, as evident in their recent Mirantis acquisition. On that note, $IREN apparently has multiple LOIs and customer commitments for high-margin managed cloud services set to take effect once the Mirantis deal closes over the coming weeks.

I've now also heard several times that $IREN takes customer selection and contract structure extremely seriously. Creditworthiness matters, but management also wants clients that can scale their compute demand substantially as $IREN ramps capacity. The only near-term downside is that this due diligence takes time, yet the longer-term advantages of the approach are obvious.

Beyond contract timing and customer selection, I believe some of it also comes down to operational reasons.

We know the 1.4 GW Sweetwater campus is earmarked for the upcoming VR200 (Rubin) capacity, whose supply won't ramp until late this year into early next. That partly explains why the site isn't up and running already, since all they could lease out right now would be current Blackwell generation.

The flip side is that $IREN could simply build "Horizon-style" capacity at Sweetwater, the same style they're currently developing at Childress, since those facilities are fully capable of housing next-gen Rubins, and have them ready by early next year, right as NVIDIA fully ramps Rubin production.

And while $IREN is already doing foundation work at Sweetwater, it could still easily take another 3-4 quarters before we see operational capacity there.

So what's the holdup?

I believe a major reason for the slow ramp at Sweetwater is that they want to implement lessons learned from their Horizon build-outs at Childress, making the Sweetwater process more efficient, less costly, and thus more economical.

Here I want to give a big shoutout to my friend @FransBakker9812, who found that $IREN has recently developed proprietary methods to make elements of the construction process significantly more streamlined, saving time and cost across all future liquid-cooled builds.

He shared more specifics on that with his "Research” and “Founding” subscription tiers, which I recommend checking out.

I firmly believe what some might see as a relatively slow ramp, given $IREN's starting position, is management's way of doing things right. Start with the first liquid-cooled buildouts in Horizons 1-4, implement lessons from one Horizon batch to the next, then apply the full set of process and workflow improvements at Sweetwater.

This closely mirrors what $IREN has always done since its mining era, when it started small and progressively scaled its construction operations in both size and speed. A true construction flywheel.

Interestingly, I've just heard that $IREN plans to develop Sweetwater 1, Sweetwater 2, and the 1.6 GW Oklahoma site in parallel over the coming years. That shows just how exponential their construction ramp really is.

In short, I believe holding out on the next wave of contracts comes down to a few factors:

1) Signing well ahead of commissioning means giving up pricing upside and attracting only a small subset of clients.

2) Customer selection and contract structure are a big part of $IREN's long-term strategy. It takes more time than simply selling to the highest bidder, but should build stronger customer relationships over the long run.

3) Scaling construction in a controlled manner, carrying critical lessons from current builds into the next. Slow start, exponential growth curve.

None of this means we won't see any deals this year, but it does add color on why commercial progress on closing deals has been slower than many of us expected.

As for deal activity and my current expectations there, it helps to step back and consider how $IREN's near-term capacity is structured.

We should expect the 50k B300 units $IREN procured back in March to be fully contracted and installed by year-end, roughly 33k at Mackenzie and another ~17k at Childress. Apparently first deliveries for Mackenzie have already arrived and are being installed.

Given this progress, I'd expect $IREN to announce having contracted substantial parts of these air-cooled Blackwells by August earnings at the latest. This is the low-hanging fruit.

And worth noting, since $IREN first gave ARR guidance for that capacity, GPU rates across the board have moved up substantially. If they sign anything close to what they landed with the 60 MW NVIDIA deal, their year-end guidance of $3.7B should climb to at least $3.9-$4.1B.

Beyond this, there's plenty of 2027 capacity that could get contracted later this year, including 190 MW of air-cooled capacity at Childress, 30 MW at Canal Flats, 150 MW of liquid-cooled Horizon 5-6, and 300 MW of liquid-cooled capacity at Sweetwater 1.

We don't have guidance on when this capacity comes online next year or what the ramp schedule looks like, but since liquid-cooled greenfield development takes longer than retrofitting existing air-cooled buildings (currently mining BTC), I'd expect the remaining 220 MW of air-cooled capacity to come online within the first couple of quarters of 2027.

For that reason, I think the odds those few hundred MW get pre-contracted later this year are relatively high.

The trickier part is the 150 MW of Horizons 5-6 and the 300 MW of liquid-cooled Sweetwater capacity. I think there's a decent shot at least one of the two gets pre-contracted in 2026, especially if it's for a hyperscaler or a frontier lab, which are far more inclined to sign a few quarters ahead.

Either way, it's just a matter of time until contracts start flowing. It's clear to me that $IREN is playing the long game and isn't compromising long-term upside for short-term euphoria in the share price. As a long-term investor, I fully support that.

I do wish, however, that $IREN were a bit more open about strategy and roadmap. It's obvious they're holding their cards close to the chest, but I find management has been overly vague on strategy.

It takes investors like me piecing the puzzle together to make sense of how $IREN plans to scale into the next hyperscaler. Ironically, management does share a fair bit of interesting and useful information if you get the chance to meet them in person, yet on earnings calls they come across as overly reserved.

That said, the future looks bright, and I have no reason to get overly concerned about disappointing price action. With a bit of luck we're in for a string of positive catalysts, starting with the Horizon 1 handoff in a couple of weeks.

I also want to take a moment to thank @OMCapitalGroup, who did an excellent job gathering information and insights while attending RAISE this week.

If it weren't for his work, I wouldn't be nearly as informed, so big props to him for taking the time to travel all the way to Paris for $IREN due diligence and then going out of his way to keep me updated with everything he picked up, even putting some of my own questions to management directly.

He's relatively new to X, but he told me he's going to start posting shortly and jump into Frans' spaces more often. Do me a favor and give this fella a follow.

Have a good one, cheers! ✌️

Thumbnail Credit (enhanced version): @AndyDTrades

Back from the Paris @RaiseSummit I wrote a recap. It was two days full of datacenters, neoclouds, custom inference chips, networking and optics, open weights, and many interesting companies. Where we are and where we are heading.

https://t.co/qwlliDf62i

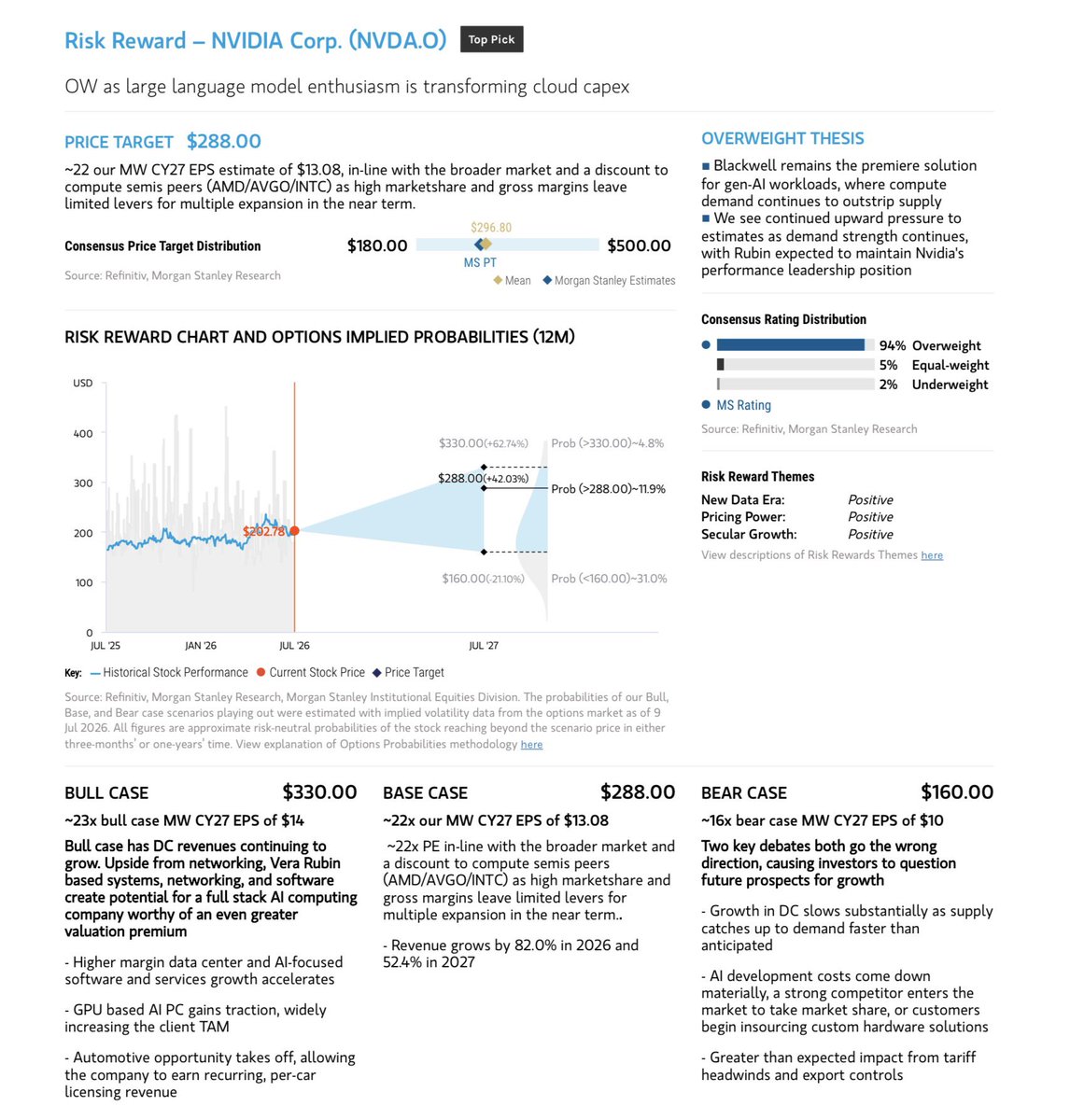

New report from MS’s $NVDA NDR with Jensen

Most interesting part IMO was re. NVIDIA’s share of compute for @AnthropicAI:

“Growth within AI labs, which they said make up about 20% of total demand currently. Notably, one of the more prominent frontier models was developed mostly on an ASIC, so NVIDIA had minimal exposure, but that has risen to close to 50%, while other frontier models continue to be mostly on NVDA.”

>MS is relaying that Nvidia’s share of computing for Anthropic has risen from *negligible* to now close to 50% - in a very short period of time at that (wonder how much the SpaceX deal boosted this up)

Other key takeaways:

• Growth accelerating near $100B/qtr

• Compute share rose despite ASICs

• Sovereign/neocloud/enterprise may outgrow hyperscalers

• Rubin Ultra ships in 2027

• 50%+ of cash flow returned

MS reiterates NVIDIA as their top pick in semi’s/$288 PT

I would buy these companies for these reasons:

1. $IREN is projected to 4x its revenue in 2027 and $NVDA partnership is cornerstone of the potential re-rate. ((One of Leopold Aschenbrenner stocks)

2. $ONDS is in a pre-rate stage going from $50.7M in revenue in 2025 to nearly $1B in 2027.

3. $TE projected to nearly 8x its operating cash flow in 2027. (One of Leopold Aschenbrenner stocks)

4. $MSFT is trading at its lowest valuation since 2023.

5. $NVDA is projected to more than double its FCF in 2027.

6. $META has the highest potential to double in 12 months of all Mag 7.

7. $CRWV is projected to nearly 3x its profits in 2027. (One of Leopold Aschenbrenner stocks)

8. $MP EPS is projected to 5x in 2027.

9. $BTDR is one of the most undervalued neoclouds in the sector with approximately 3GW capacity.

10. $KTOS is projected to 4x its profits in 2027.

11. $HIMS is expected to more than double its EPS in 2027.

12. $OSCR is projected to grow its profits by 50% in 2027 after returning to profitability in 2026.

Morgan Stanley , 엔비디아(Nvidia) NDR 보고서 $NVDA

투자의견 Overweight, 목표주가는 288달러 , 반도체 업종 Top Pick

강세 시나리오: 목표주가 330달러

NVIDIA 경영진과 진행한 NDR에서는 성장 속도가 다시 빨라지고 있으며, 동시에 성장원이 더욱 다변화되고 있다는 점에 대한 높은 자신감이 강조됐다.

1. 앞으로도 성장 가속이 가장 중요한 초점

NVIDIA 경영진은 현재의 성장세를 유지하는 수준이 아니라, 앞으로 성장률이 더 빨라지는 것을 핵심 목표로 제시했다.

이미 회사의 매출 규모가 매우 커졌음에도 성장률 둔화를 전제로 하지 않고 있다는 점이 중요하다.

2. 성장원이 폭넓게 다변화되고 있음

NVIDIA가 제시한 성장 동력은 다음과 같다.

1)AI 연구소에서의 점유율 상승: 현재 NVIDIA 전체 수요의 약 20%를 차지하는 것으로 설명

경영진은 주요 frontier model 중 하나가 과거에는 대부분 ASIC을 사용해 개발됐기 때문에 NVIDIA의 노출도가 매우 낮았지만 해당 모델과 관련한 NVIDIA의 비중이 최근 거의 50% 수준까지 상승했다.

2) 기존 hyperscaler의 지속적인 AI 투자

3) neocloud 사업자 확대

4) 일반 기업 고객의 AI 도입

5) 국가 주도형·sovereign AI 투자 확대

즉, Microsoft·Meta·Amazon·Google과 같은 기존 대형 고객에 대한 의존도가 ���아지는 방향으로 고객 기반이 넓어지고 있다.

3. Hyperscaler는 여전히 강한 성장축

기존 hyperscaler 수요는 여전히 매우 강하다.

여기에 GPU뿐 아니라 다음 제품들이 추가되면서 NVIDIA가 공략할 수 있는 시장인 SAM이 확대되고 있다.

-Spectrum-X와 InfiniBand를 포함한 네트워킹

-NVLink 및 스위칭

-Vera CPU

-독립형 CPU 랙

-AI에 최적화된 서버 시스템

NVIDIA가 단순한 GPU 공급업체에서 AI 데이터센터 전체 컴퓨팅 플랫폼 공급업체로 확장

4. 부지·전력·지정학이 고객 의사결정의 핵심이 됨

현재 AI 인프라 투자에서 가장 중요한 제약은 단순한 GPU 가격이 아니다.

데이터센터를 지을 수 있는 부지

공급 가능한 전력

냉각 및 관련 인프라

국가별 수출 규제와 지정학

데이터 주권 및 보안

이러한 요인들이 고객의 구매 결정을 좌우하고 있다.

이에 따라 장기적으로는 기존 hyperscaler보다 국가 주도 AI 프로젝트와 neocloud 사업자들의 성장률이 더 높아질 수 있다.

5. 가치주 투자자 유입이 valuation gap 축소에 중요

NVIDIA는 지금까지 대표적인 고성장주로 평가됐지만, 앞으로는 가치 중심 투자자들에게도 다음 요소를 강조하려는 것으로 보인다.

막대한 현금흐름

높은 수익성과 시장점유율

빠르게 낮아지는 미래 P/E

GPU를 넘어선 사업 다각화

장기간 지속될 AI 인프라 수요

Morgan Stanley는 가치주 투자자들의 참여가 늘어나면 NVIDIA가 동종 업체 대비 받고 있는 valuation gap이 축소될 수 있다고 평가했다.

6. 자체 ASIC과 NVIDIA의 성장은 동시에 가능

Morgan Stanley는 다음 두 가지가 동시에 사실일 수 있다고 판단한다.

첫째, hyperscaler들은 자체 ASIC을 계속 개발하고 배치할 것이다.

둘째, 그럼에도 NVIDIA는 AI 컴퓨팅 사업에서 매우 큰 비중을 계속 유지할 것이다.

즉, 자체 ASIC 확대를 반드시 NVIDIA 점유율의 급격한 하락으로 볼 필요는 없다는 판단이다.

Morgan Stanley가 접촉한 업계 관계자들도 NVIDIA 경영진의 주장을 뒷받침했다.

��은 워크로드에서 실제 토큰당 비용이 가장 낮은 솔루션은 여전히 NVIDIA라는 것이다.

7. Overweight의 핵심 근거

Blackwell은 생성형 AI 워크로드의 최상위 솔루션

Morgan Stanley는 Blackwell이 생성형 AI 워크로드에서 여전히 가장 우수한 솔루션이라고 평가했다.

AI 컴퓨팅 수요가 공급을 계속 웃돌고 있어 제품 판매를 위한 수요 확보보다 얼마나 빠르게 공급을 늘릴 수 있는지가 더 중요한 상황이다.

실적 추정치에는 계속 상향 압력이 존재

AI 수요가 지속적으로 증가하면서 매출과 EPS 전망치가 추가로 상향될 가능성이 있다.

Blackwell 이후에는 Rubin이 NVIDIA의 성능 우위를 유지할 것으로 전망했다.

즉, Blackwell 수요가 끝난 뒤 성장 공백이 생기는 것이 아니라, Vera Rubin으로 이어지는 연간 제품 출시 주기가 성장의 연속성을 제공한다는 판단이다.

8. 강세 시나리오: 목표주가 330달러

데이터센터 매출이 예상보다 계속 빠르게 성장한다.

특히 성장의 중심이 GPU에만 머무르지 않고 다음 영역으로 확대된다.

-네트워킹

-Vera Rubin 기반 시스템

-CPU

-AI 소프트웨어

-AI 서비스

이 경우 NVIDIA는 단순한 반도체 회사가 ���니라 완전한 full-stack AI 컴퓨팅 회사로 평가

$IREN

If the expected handoff of H1 on July 19 happens, it will be the first milestone

It will be the first newly built, liquid-cooled AI data center constructed specifically for a hyperscale customer

Then we have H2, H3, and H4 that were originally said to be deployed through 2026 and confirmed in May to be delivered by EOY 2026

This should start delivering $1.94B/year once completed ($9.7M/MW)

If this happens without any problems, the stock will finally be re-rated, and rightfully so

The AI DATA CENTER CRASH is becoming increasingly likely.

$IREN and other names are on the verge of another 40% correction.

For now, I remain slightly bullish on $IREN, with a target of approximately $100 (left chart).

However, if the stock fails to defend the 0.786 retracement at $38.68, my bearish scenario (right chart) comes into play.

In that case, I expect prices between $28 and $14 next.

Both scenarios currently have an almost equal probability. At current levels, $IREN is definitely not a buy.

The short-term structure is weak and does not appear impulsive.

$NBIS and $CRWV must also defend their current levels. Otherwise, things could get ugly.

Both stocks could face corrections of 40–60%.

@anandragn@nanotitan28 I think the current weakness in the stock is largely due to short sellers. Stocks like this are hard to predict because a single contract announcement can trigger a massive gap up.

$IREN

Holy short interest batman!

Newest short interest print shows an additional 11.5M shares were added short in the last 2 weeks of June.

Now up to 76M+ shares short or 22.5% of the flow.

Record high!

Show em' something @danroberts0101 !