The great semiconductor disconnect: SOX earnings estimates keep climbing to fresh records, while chip stocks are tumbling. The index is now ~20% below its peak even as forward profits hit new highs. Either this is a buying opportunity – or the market knows something analysts don’t.

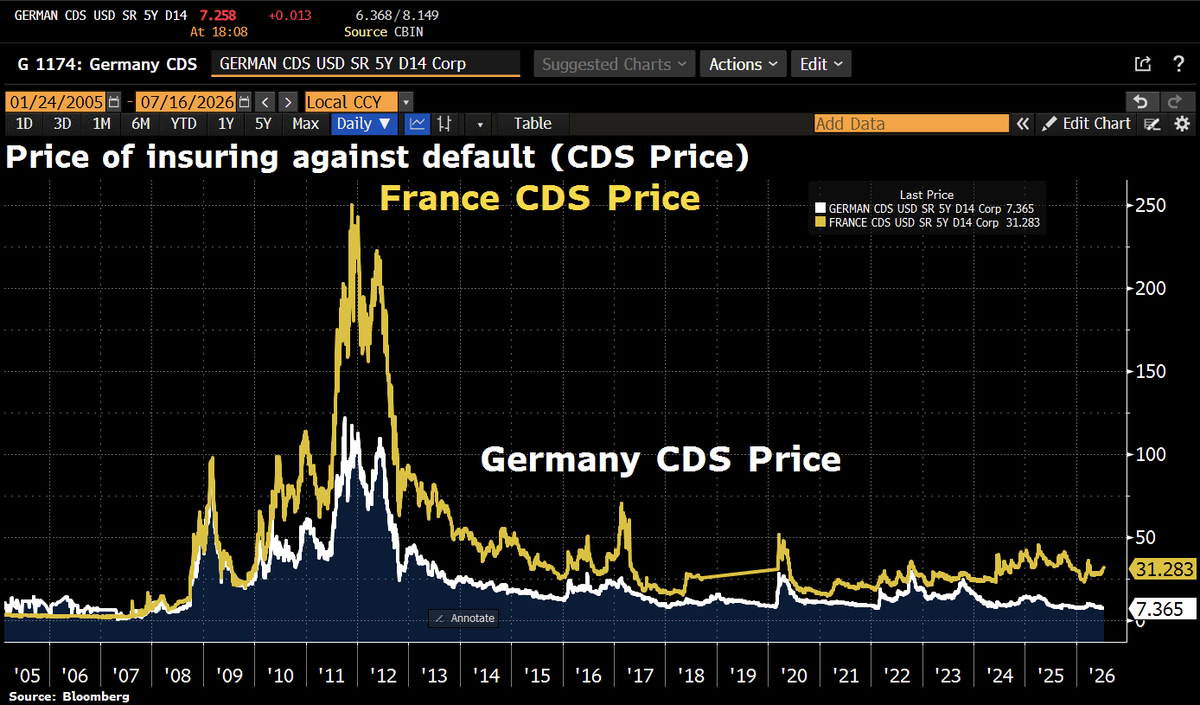

Hello from #Germany, where bond vigilantes are whispering, not shouting: 10y real yields are pushing toward a 6mth high at 1.08% as Berlin borrows more, while CDS show no alarm: Germany ~7bps vs France ~31bps. Merz says AAA is safe, but he'd “slam on the brakes” if it wasn't.

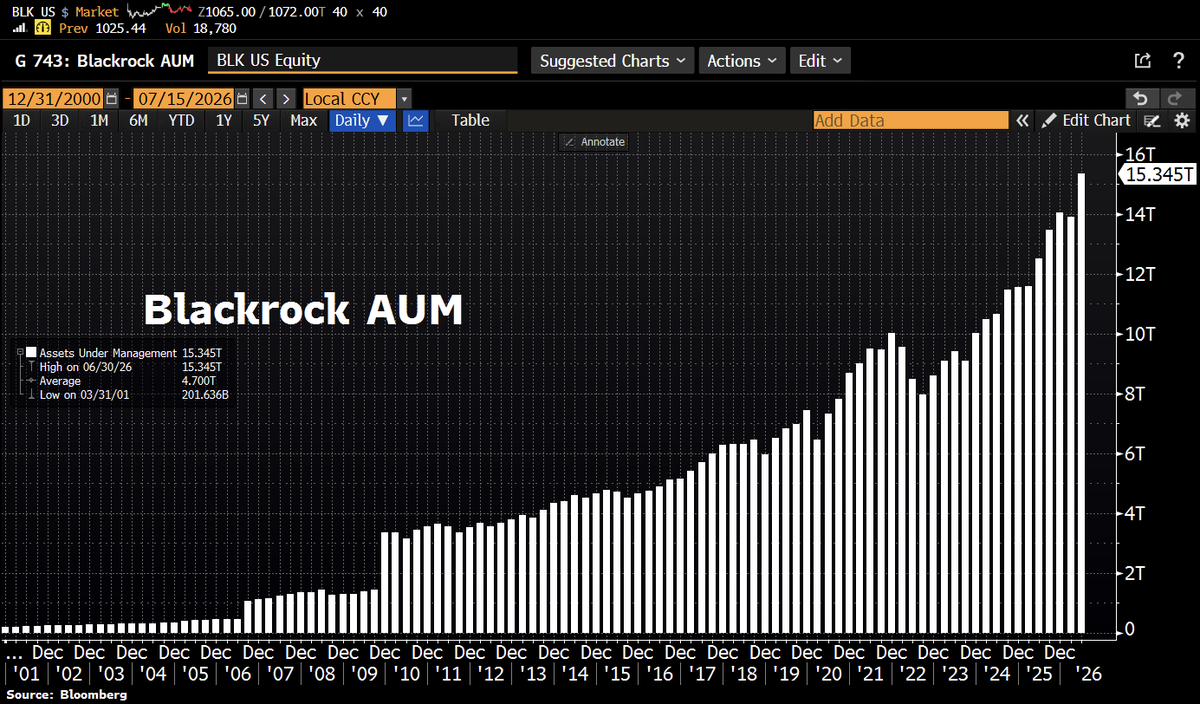

BlackRock is eating the world. The asset manager just crossed $15tn in AUM for the first time, powered by $192bn in Q2 inflows and a record $321bn in H1. ETFs alone pulled in $178bn, revenue jumped 31%, EPS beat. Scale is becoming the ultimate moat.

Good Morning from Germany, where Berlin is trying to cool the Commerzbank drama: Chancellor Friedrich Merz says Germany is not blocking a UniCredit takeover – only rejecting the way the Italian lender approached the bank. “We have never attempted to do so,” Merz says in Summer Press Conference. “We have only ever said that the way Commerzbank was approached does not have our approval.” Translation: no veto, but no blessing either.

Hello from Germany, where the Rhine’s Kaub chokepoint is at its lowest water level for this time of year in decades. Barges can carry less than 20% of normal loads, diesel freight rates from Rotterdam to Karlsruhe jumped 56% – and another heat wave is turning drought into a supply-chain shock. https://t.co/WjiqQQna68

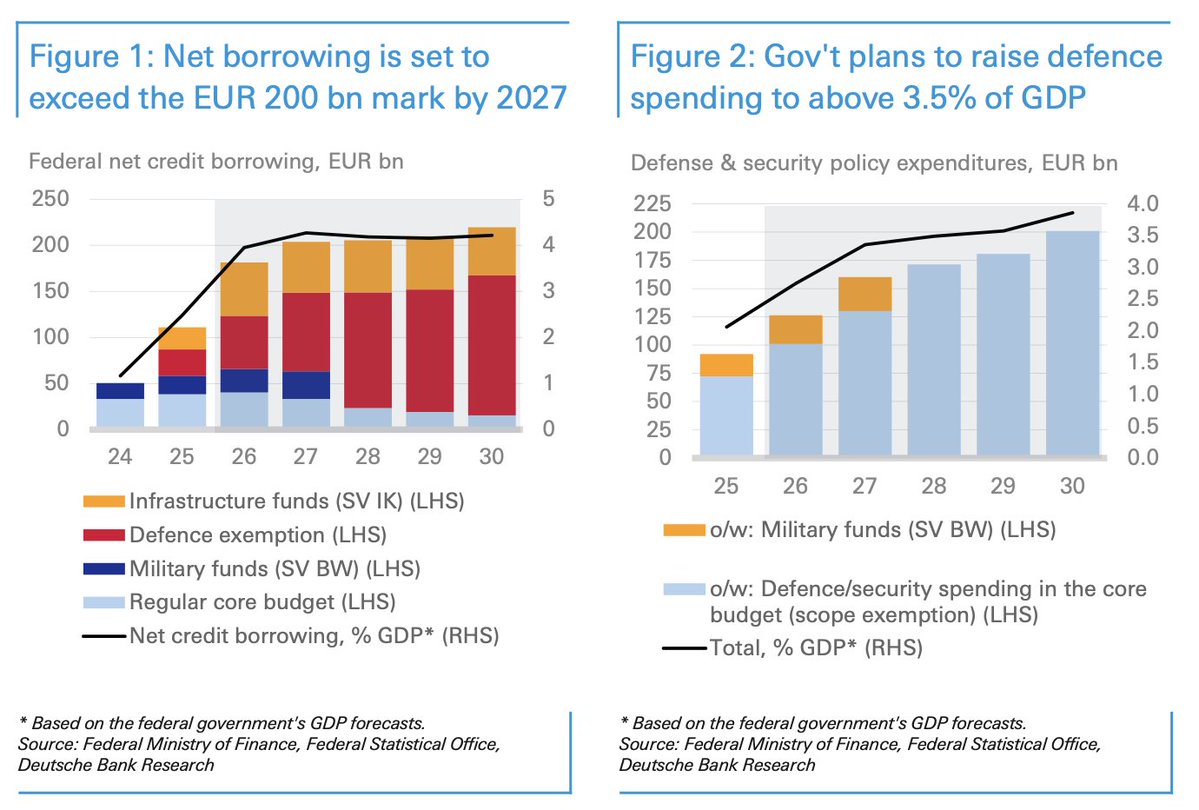

Good Morning from Germany, where the fiscal Zeitenwende is getting bigger. Berlin now plans >€1tn in new federal debt for 2026-30, w/annual borrowing >€200bn from 2027. Defense spending is set to climb toward 4% of GDP, while interest costs could jump from €30bn to >€80bn by 2030. The 2027 budget gap is closed – but the bill is merely pushed into the future. (via DB)

The Fed balance sheet is rising again; but this is not QE 2.0. It’s plumbing. Total assets ticked up to $6.736tn as securities holdings rose by ~$10.5bn, mainly Treasury bills. More important: the Treasury’s cash account, the TGA, has fallen sharply after tax season, injecting liquidity into the banking system. Bank reserves jumped $60bn last week after +$123bn the week before. In other words: QT may be the regime, but short-term Treasury cash flows are temporarily making the Fed look more accommodative than it really is.

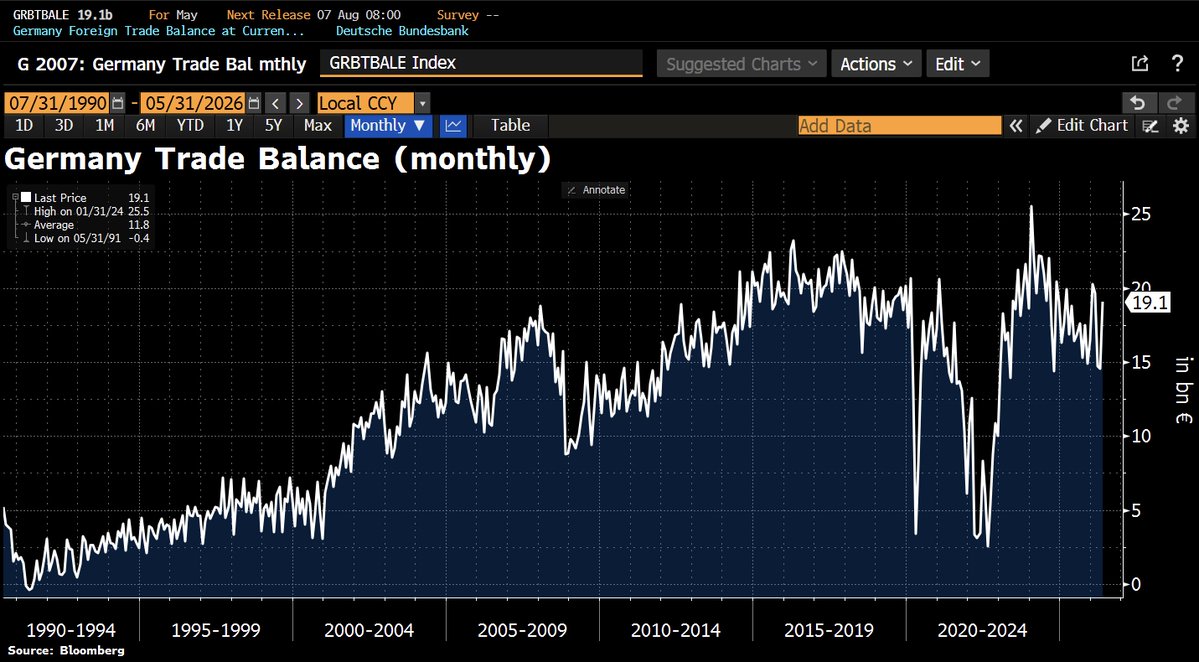

Good Morning from Germany, where trade is giving GDP a lift: May exports unexpectedly rose 0.9% MoM, extending gains to a 4th month, while imports fell 2.5%. The trade surplus jumped to €19.1bn vs €14.8bn expected as US shipments rebounded 23.1% and China sales rose 7.1%.

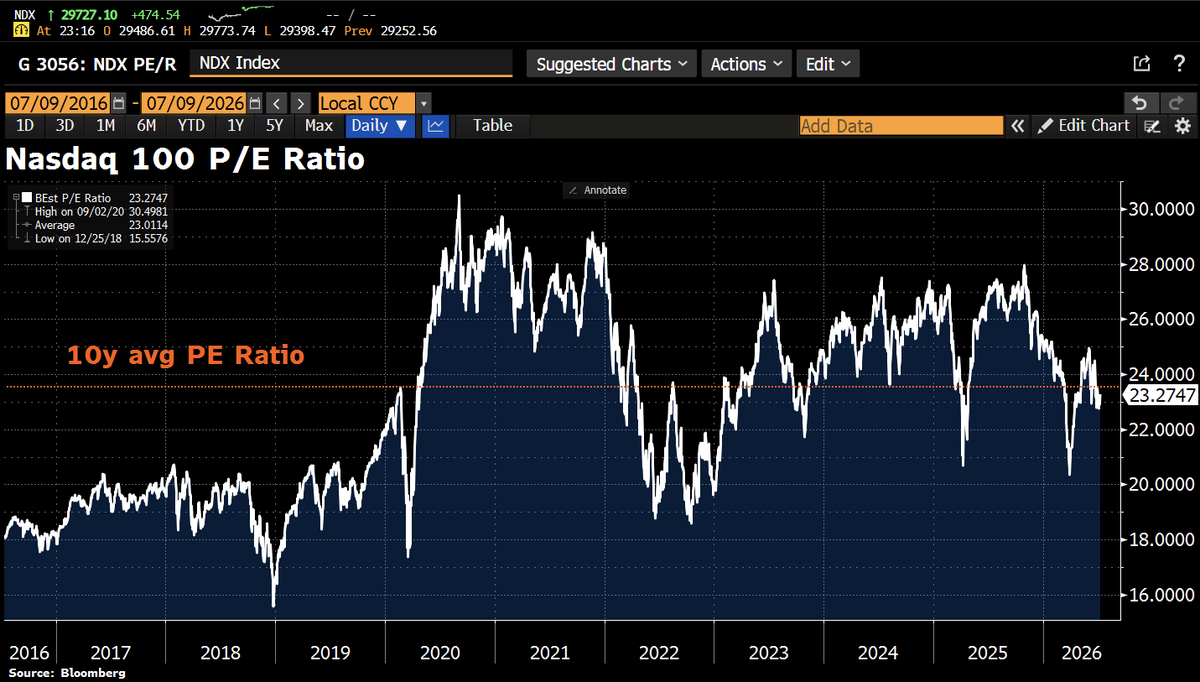

To put things into perspective: The Nasdaq 100 is currently trading at ~23x NTM P/E, which is broadly inline w/its 10y avg multiple and towards the lower end of its 3-4y range, Goldman says,

Good Morning from Germany, where long-dated yields keep climbing. The 30y Bund yield has risen to 3.64%, near levels last seen in 2011. Bond markets are pricing a new reality: higher-for-longer rates, more debt issuance and rising duration risk.

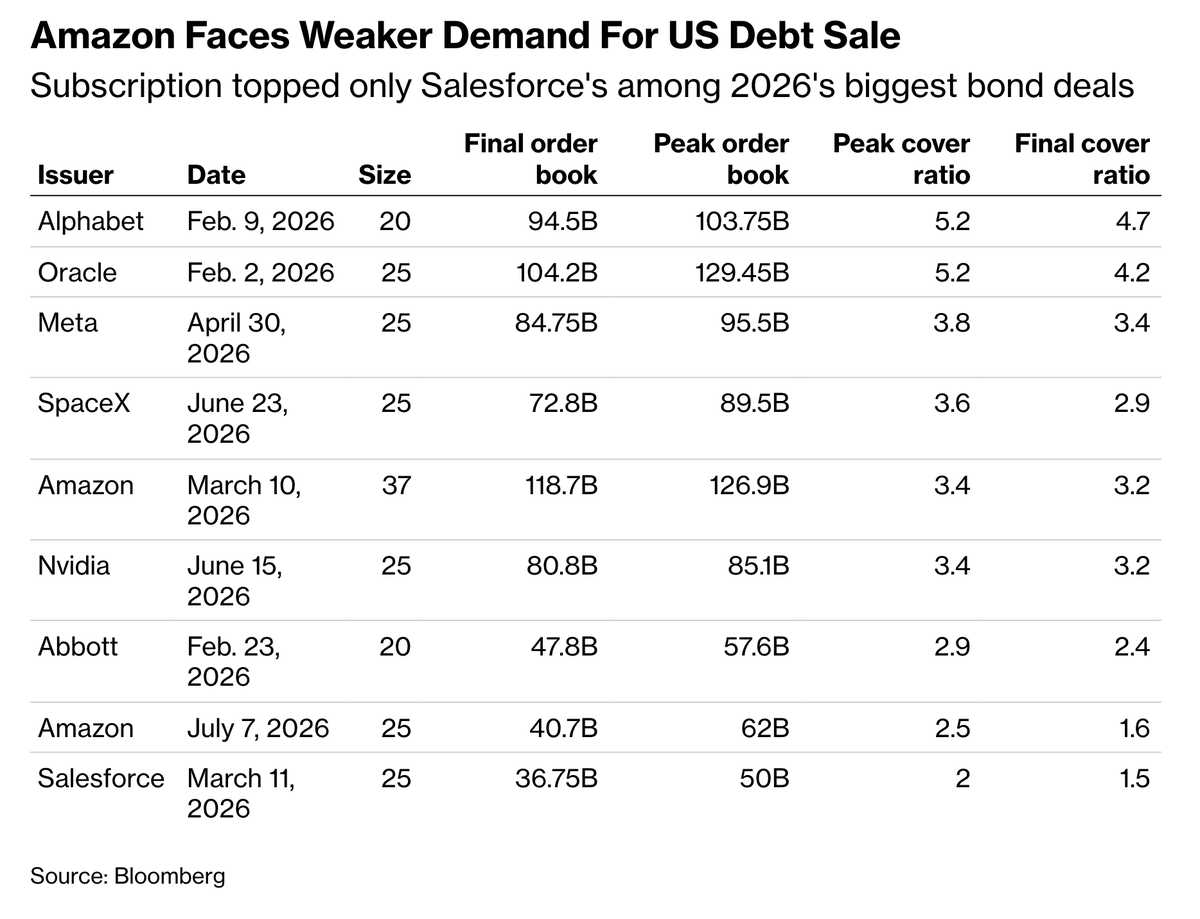

Big Tech’s AI arms race is moving from equity hype to debt markets. Amazon’s $25bn bond sale was the 7th tech mega-deal of 2026. Together, Amazon, Alphabet, Nvidia, Meta, Oracle and SpaceX have raised $182bn in IG dollar bonds this year. BUT investor appetite is starting to crack. https://t.co/beUpEv4VQt

Germany is losing speed: the IMF cut its 2026 GDP forecast to 0.7% and 2027 to 1.0% (-0.2pp). That leaves Europe’s engine behind the US (2.3%) and China (4.6%), and barely ahead of France (0.6%) as the energy shock bites.

Good Morning from #Germany, where the AI boom has barely delivered any upside; yet an AI bust could still tip the economy into recession. Acc to BBG Economics, Germany could see a hit of 1.2% of annual GDP in 2027, given their trade and financial linkages w/US. No boom, but still the bust.

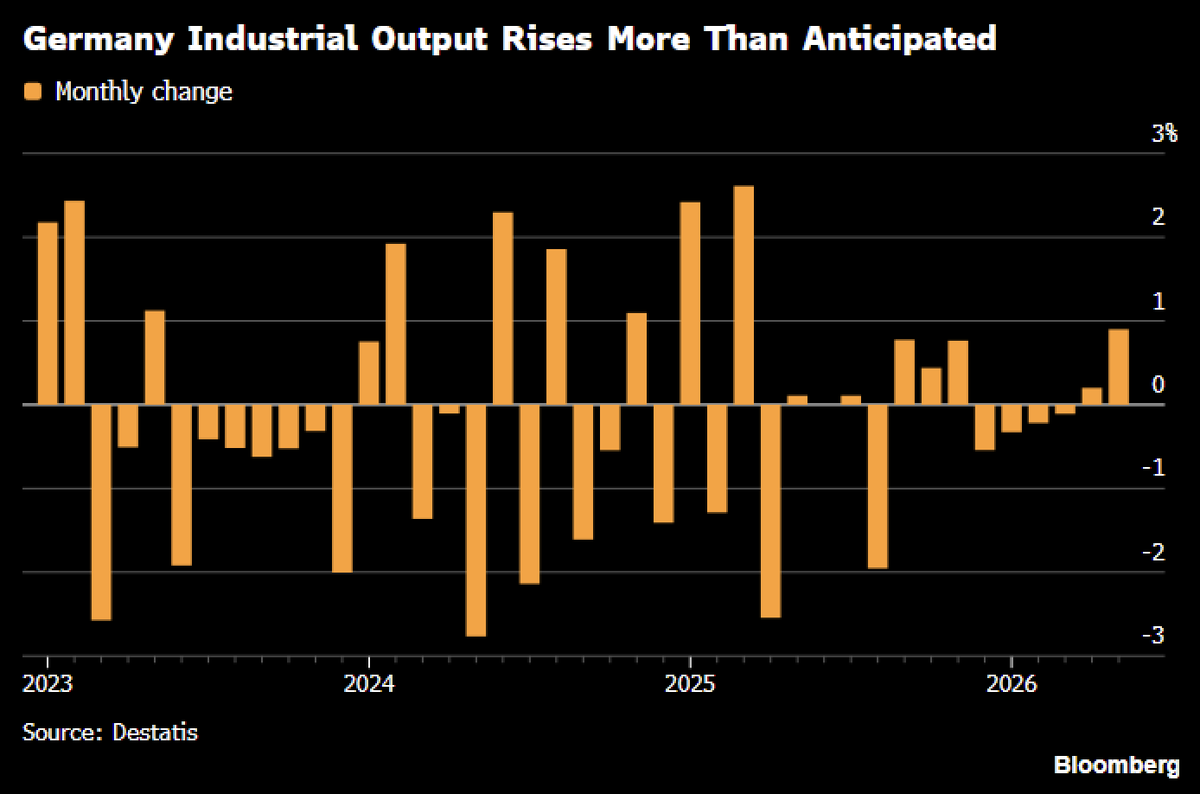

Good Morning from Germany, where industry is beating expectations: output rose 0.9% MoM in May vs 0.1% est, 2nd straight gain. Autos drove rebound w/+3.6% production, while construction also grew. Signs mounting that Europe’s largest econ is exiting its slump https://t.co/za7sL92OcT

Good Morning from Germany, where Berlin’s debt tab is surging. Federal interest payments are set to jump to nearly €42bn next year from just over €31bn this year and could hit €80bn by 2030. That’s money spent on the past, not invested in future growth.

Good Morning from Germany, where latest reform proposals are no short-term game changer, but clear step to lift medium-term growth. More flexible labour rules, stronger work incentives & less red tape should help labour supply grow despite adverse demographics, Oxford Econ says.

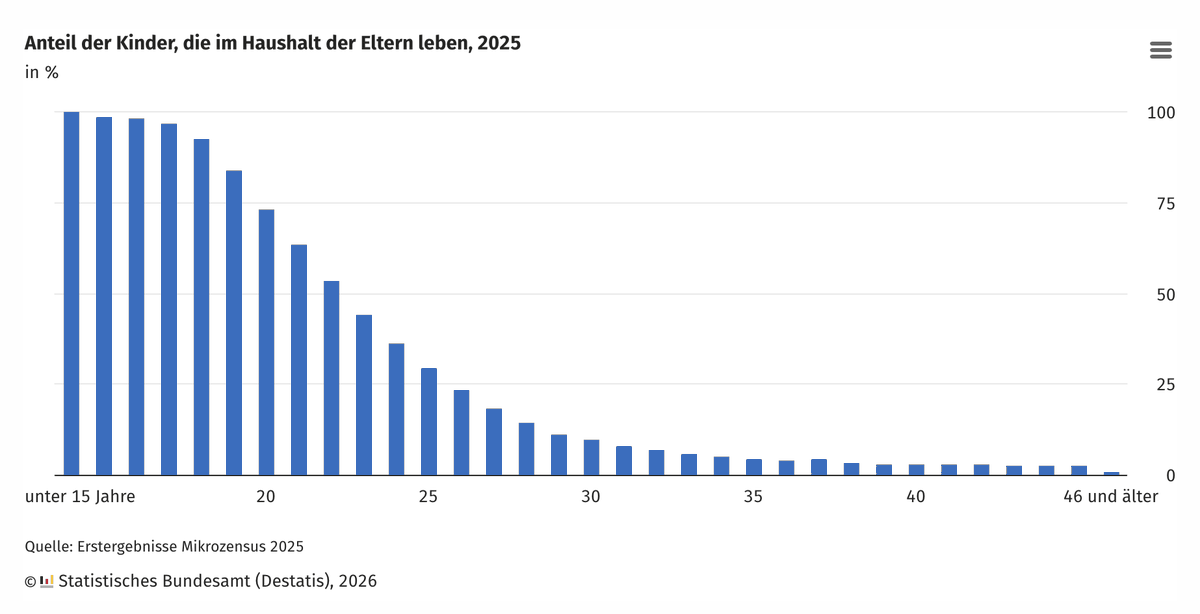

Good Morning from Germany, where the nest is getting harder to leave: 30% of 25-year-olds still lived w/their parents in 2025, up from 28% in 2022-24. Sons stay longer (36%) than daughters (23%), and 77% of 25-34s at home are employed.

US jobs report screams slowdown beneath the headline: payrolls rose just 57k, but the household survey showed employment plunging 507k and the labor force collapsing 720k. Unemployment fell to 4.2% for the wrong reason: participation cratered to 61.5% from 61.8%.